Although we have been writing about it for many years now, it may be worth updating for those who do not know about it, some of the advantages of having our investment portfolios deposited in banks in Luxembourg. For most, the most obvious advantage would be to be able to hold the money while avoiding country risk or the risk of insolvency of Spanish banks, with Luxembourg being the EU Wall Street par excellence, once London ceases to be so due to Brexit. However, there is a much more powerful reason to manage most of our financial wealth from Luxembourg. And that reason is access to any investment fund, private equity, real estate fund, etc. in the world, even if it is not registered for marketing in Spain.

.

This freedom of access is no trifle when one realises that only 10% of the existing funds worldwide have this registration with the CNMV in order to be marketed in Spain. Therefore, investors who do not have adequate advice will never be able to access a 90% of funds, which logically include some of the best managed funds in the world. Furthermore, no bank in Spain, not even to its private banking clients, offers just that 10% registered with the CNMV in its entirety, as the sales catalogues are usually limited to 2, 3 or 5 thousand funds, with the excuse that they belong to different trading platforms, etc. Therefore, the opportunity cost of magnificent investment options that the local investor cannot access is enormous. In fact, this condemnation of mediocre investment is one of the main reasons for the the causes of brick abuse in Spain, although we have already discussed it extensively in other articles.

.

The question many of you will ask is why most funds are not registered in Spain for marketing, or at least why the star funds managed by some of the world's leading managers do not do so. There are several reasons: among them are funds that do not consider marketing in Spain because it is expensive for the small volume they would achieve in our country. We must not forget that marketing in Spain, through the network of financial institutions and platforms that operate here, in many cases involves a cut of more than 50% of the commissions charged by the fund manager. In fact, some fund managers, such as Carmignac, decided at the time to create an ad hoc class in their funds for marketing in Spain, with higher fees than those applied to the rest of their classes, in order to satisfy the voracity of local financial institutions. At Carmignac, these classes were shamefully labelled with the «E» for Spain.

.

However, the marketers' bites are not the only reason that many international fund managers have for not registering their funds for sale in Spain. Another important reason is that the only doors that registration in Spain would open for them is to access Spanish retail clients, since larger or institutional clients can access funds that are not registered in Spain without great difficulty. Investors with a few million and who are well advised already have their own investment vehicles in banks abroad that allow them to access all types of funds beyond the CNMV's list of marketable funds. In other words, fund managers not registered in Spain do not need to register or pay any bribes to attract these Spanish millionaires.

.

There are also other reasons for some managers to disdain the Spanish retail investor market, such as specialisation in institutional clients or geographical remoteness. It is common that some managers from China, Thailand, India, etc., whose investors are essentially Asian, Middle Eastern or North American, do not prioritise attracting Spanish retail clients at all. And they usually focus on marketing in Europe through the British or German market, either for retail or institutional investors, but with higher volumes and lower bites than in Spain.

.

The consequence of all this is that the Spanish retail investor is condemned to a very limited portfolio of funds that have previously agreed to pay juicy commissions to the financial institutions that market them in Spain. And for these investors who do not have tens of millions, the fact of being able to invest much more modest amounts from Luxembourg, with exclusive personal vehicles that open the doors to any fund in the world, means the difference between mediocrity and brilliance of investments in terms of quality and results.

.

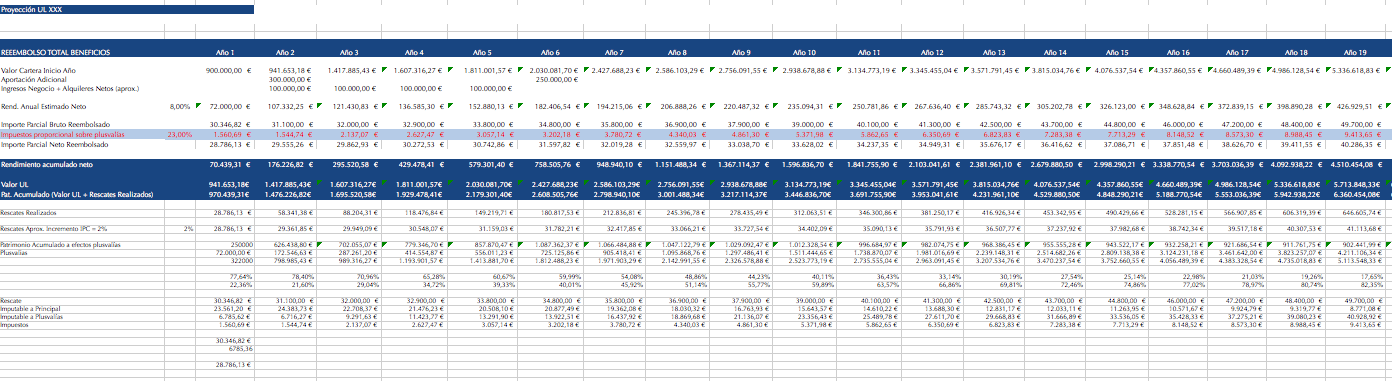

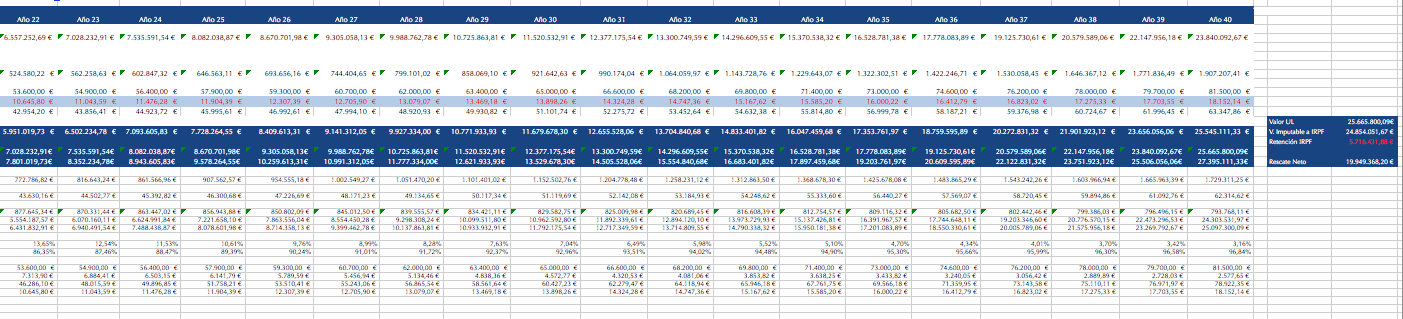

Luxembourg, as a good «EU friendly» financial centre, has various types of investment vehicles that adapt to the needs of each size and type of investor. But for the smaller investor, who is the most disadvantaged by the restricted range of funds to which he has access in Spain, there is a a personal and exclusive Luxembourg vehicle from which you can invest your portfolio with complete flexibility, from as little as 250,000 euros. Obviously not all retail investors have a minimum of 250,000 euros, but it is a huge step for the average investor to be able to put their investments on a par with those of any institutional investor with 10 or 20 million from as little as 1/4 million. And these vehicles not only allow access to any fund in the world, but also to any fund in the world. also allow for the deferral of capital gains generated within these vehicles indefinitely., The tax is only levied on the proportional part of the capital gain when it is decided to redeem part or all of the investment. In other words, once we have this minimum of 250,000 euros in our own investment vehicle, we will be able to buy and sell any fund, share or whatever we want, without paying tax on the capital gains until we need to withdraw all or part of our money. Taxation is exactly the same as when we buy any fund registered in Spain that is sold to us by the bank on the corner, but without the need to jump from one transferable fund to another within the limited list of funds registered with the CNMV, but with total and absolute freedom in the world universe of UCITS, non-UCITS, AIFMD, Private Equity, Real Estate Funds, shares and other financial products. This is why we chose a Luxembourg vehicle, totally «friendly» with the taxation and transparency of EU countries.

Luxembourg, as a good «EU friendly» financial centre, has various types of investment vehicles that adapt to the needs of each size and type of investor. But for the smaller investor, who is the most disadvantaged by the restricted range of funds to which he has access in Spain, there is a a personal and exclusive Luxembourg vehicle from which you can invest your portfolio with complete flexibility, from as little as 250,000 euros. Obviously not all retail investors have a minimum of 250,000 euros, but it is a huge step for the average investor to be able to put their investments on a par with those of any institutional investor with 10 or 20 million from as little as 1/4 million. And these vehicles not only allow access to any fund in the world, but also to any fund in the world. also allow for the deferral of capital gains generated within these vehicles indefinitely., The tax is only levied on the proportional part of the capital gain when it is decided to redeem part or all of the investment. In other words, once we have this minimum of 250,000 euros in our own investment vehicle, we will be able to buy and sell any fund, share or whatever we want, without paying tax on the capital gains until we need to withdraw all or part of our money. Taxation is exactly the same as when we buy any fund registered in Spain that is sold to us by the bank on the corner, but without the need to jump from one transferable fund to another within the limited list of funds registered with the CNMV, but with total and absolute freedom in the world universe of UCITS, non-UCITS, AIFMD, Private Equity, Real Estate Funds, shares and other financial products. This is why we chose a Luxembourg vehicle, totally «friendly» with the taxation and transparency of EU countries.

.

These vehicles are logically deposited in banks in Luxembourg, although as mere depositaries, it matters little that they are more solvent than Spanish banks, since we will only use them for the safekeeping of the vehicles and the portfolios with the fund units or shares that we are going to buy and sell in them.

.

As for costs, we have been able to fine-tune them over the years due to the growing volume of clients. And currently the total cost of a Luxembourg unit-linked vehicle for a small investor (minimum 250,000 eur) can be around 0,6-0,7% annual, The volume of vehicles in the market is significantly reduced as the volume increases. Furthermore, in certain circumstances, these vehicles also avoid the payment of Wealth Tax, which in some Autonomous Communities does not have a rebate.

.

Obviously, as Luxembourg is the financial centre of choice for the EU - replacing the City of London - any capital to be invested in such vehicles must have a justified origin, be fully declared and transparent, as Luxembourg's tax haven connotation is now completely behind us and definitively buried by the EU's own imperative.

.

In short, in 250,000 can access vehicles that cost less than 0.6-0.7%, that efficiently defer Capital Gains, that can save Wealth Tax, that allow access to investing in the best investment fund managers on the planet rather than just 10% of them, and with the banking and legal security of a world-class financial centre in the heart of the Eurozone. That is nothing, in these times of uncertainty, insolvency and disguised risks.

.

For those who see the remoteness of having their money in Europe as a handicap, I would like to remind you that, in addition to being able to manage it conveniently, swiftly and closely through Spanish advisors and professionals, having a Luxembourg investment vehicle is not exclusive. In other words, most investors combine a (more or less majority) part of their assets in Luxembourg with a part held in banks in Spain, as a temporarily invested treasury, which will be consumed or used over the coming quarters, semesters or even years.