Most investors know little or nothing about the inner workings of what is considered the best investment fund in the world, due to its stratospheric performance over more than 30 years, the Medallion Fund. We have therefore decided to write this article unveiling the information we have gathered and the ins and outs we learned when we visited its management, Renaissance Technologies, a couple of years ago. Despite the length of the article, we believe it will be very interesting for readers to learn about the background, inner workings, curiosities and eccentricities of this great group of scientists, who have been recognised as the best managers in the world for their ability to beat the market for decades.

.

.

According to Bloomberg, the size of the Medallion, which is the fund set aside for «...", has been reduced to the size of the Medallion.«friends & family».» The current owner's fund size is approximately $11 billion, which together with the other funds that Renaissance manages for an elite group of institutional clients, make up the $62 billion under management in total (figures as of January 2019).

.

We will now explain the origins and evolution of the world's best fund manager, and at the end of the article we will tell you about our personal visit to the Renaissance Technologies facilities, after passing both their due diligence and ours and thus becoming institutional clients of their funds.

.

The origin and evolution of Medallion and Renaissance performance:

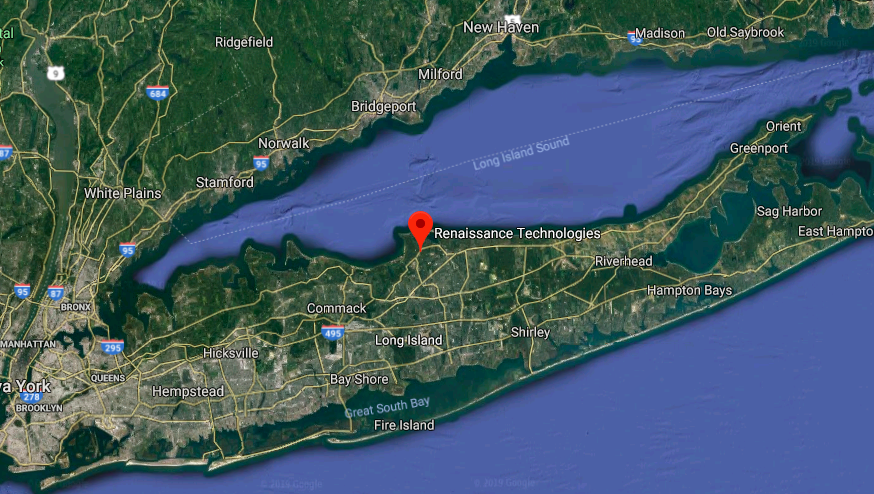

On the north shore of the luxurious Long Island, just a couple of hours' drive from Manhattan, lies the area popularly known as the Renaissance Riviera. Not for nothing are the biggest billionaires in the area scientists working for Renaissance Technologies in neighbouring East Setauket. This elite group created in 1988 what has been the biggest money-making machine in the financial world, the Medallion Fund. A quantitative fund that has far exceeded the returns of other legendary managers such as Ray Dalio or George Soros. And what is even more spectacular is that it has done so in less time and from a smaller size.

.

This fund almost never loses money. Its worst 5-year performance has been -0.5%. According to Andrew Lo, professor of finance at MIT and chairman of AlphaSimplex, another quantitative fund manager, «Renaissance is the financial and commercial version of the Manhattan Project«. Andrew Lo praises Jim Simons, the mathematician who founded Renaissance in 1982, for bringing so many scientists and intelligence together in a single enterprise. «They are the pinnacle of quantitative investing. No one is even close to their level.». Very few companies generate so much fascination, buzz and speculation. Everyone has heard of Renaissance and the mythical Medallion but hardly anyone knows what goes on in there. Apart from Simons, a somewhat more public figure who retired in 2009 with a personal fortune estimated at more than $16 billion, little is known about the rest of its small group of founding scientists, whose wealth exceeds the GDP of several countries.

.

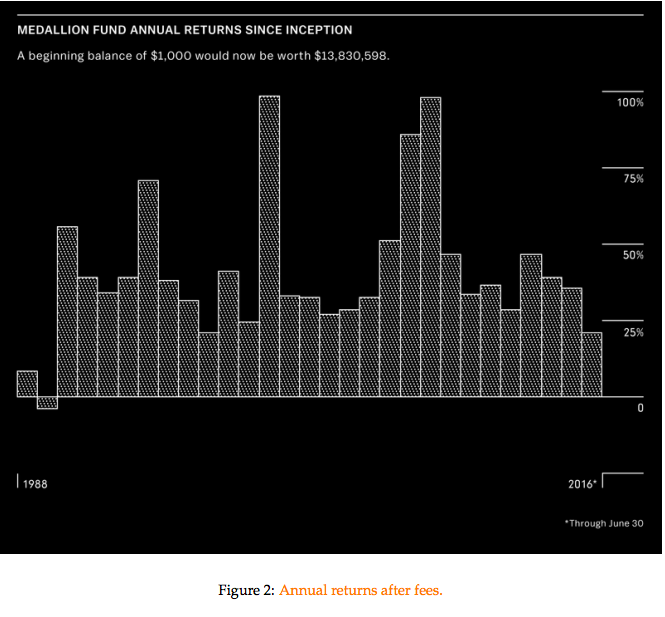

For those who are wondering whether such astronomical returns (see graph below) and such sustained returns over time are really possible, it is worth commenting here on the words of Simons, in his lecture last week at the Massachusetts Institute of Technology (MIT), when he was asked for the umpteenth time in his career whether he had ever been compared to the fraudster Madoff: «Of course, with our results and after what happened with Madoff, shortly after that the SEC (US regulator) looked at us and investigated us thoroughly. Of course they didn't find anything.». But this team of scientists who have been beating the markets for more than 30 years, with a fund closed exclusively to them, and 3 others with entry barriers of USD 5 million, really care little about the sceptics.

.

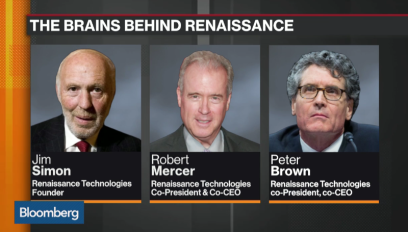

Renaissance is unique among hedge funds, institutional funds and closed-end funds. Its partners and managers are as cool as they are eccentric. Of the more than 300 employees, 90 are doctors (Ph.D) in disciplines such as mathematics and physics. Peter Brown, who co-heads the firm, used to sleep on a folding bed in his office. His counterpart, Robert Mercer, rarely speaks. And the identical twins, Stephen and Vincent Della Pietra, PhDs specialising in string theory, often argue loudly with each other. The rest of the staff can't be called typical office workers either. There is too much talent for vulgarity.

.

For the outsiders, the mystery is how Medallion has been able to win so close to the top of the table. an annual 80% before commissions, The fund, by the way, takes almost half of the return, although in reality almost all of it stays at home as it is a fund exclusively for members and employees. And the most surprising thing is that despite three decades of experience, they have not been able to copy them enough to come close to their results. The reasons are to be found in the power of its computational capacity, because the computers in their bunker basements are among the most advanced on the planet. Their talented employees have more and better data in which to find patterns and models that can be exploited. And they also fine-tune the costs of their transactions, of which there are many, while taking into account the consequences that their own trading generates in the markets.

.

But it should not be forgotten that the origins of most of its founders come from IBM back in the 1980s. There they used statistical analysis for the first linguistic challenges faced by mathematicians and computer scientists. Jim Simons, mathematical genius, professor at MIT and Harvard, winner of the Oswald Veblen Prize in Geometry and co-creator of the Chern-Simons Theory, was also a code breaker for the Institute for Defence Analyses (IDA).IDA) of the USA. (the current location of the Renaissance headquarters may not be coincidental, given that East Setauket was the area known as Culper Spy Ring, The birthplace of espionage, which enabled Goerge Washington to confront British troops with prior knowledge of their secret plans at the end of the 18th century). The aim of quantitative analysis is similar: to build models that find hidden signals in the «noise» of the markets.. Often they are just whispers, but some are able to predict how the price of a share, a bond or a barrel of oil will make a profitable move, however imperceptible it may be. The problem is complex. Prices depend on fundamentals and flows and the often irrational behaviour of the actors who are buying and selling. Despite (or because of) the fact that Simons lost his job at IDA after publicly denouncing the Vietnam War in a New York Times article, the cryptographic connections he researched helped him create Renaissance, and a few years later Medallion. On his way out, he sought out and surrounded himself with cryptographers and mathematicians such as Elwyn Berlekamp and Leonard Baum, former colleagues at IDA, Stony Brook and professors Henry Laufer and James Ax, for his initial project: Statistical price prediction.

.

The beginnings were bittersweet, and trend following and conversion to the mean caused them problems. Gradually they built models and more models. The initial results were mixed: +8.8% in 1988 and -4.1% in 1989. But in 1990, after explicitly focusing on short-term trading, Medallion achieved a profit of +56% net of commissions. The scientists went on to develop an internal programming language for their models. Today, Medallion uses dozens of «strategies» that run together as one. The computer code they use includes several million lines of code, which is soon to be said. Several teams are responsible for specific areas of research, but in practice everyone can work on everything. Every week there is a meeting where new ideas are tested and discussed to extreme limits by almost a hundred PhDs and other gifted minds.

.

In the early 1990s, spectacular yields became the norm at Renaissance: 39.4%; 34%; 39.1%. And customers began to flock to Medallion. The fund manager never bothered with marketing, in fact today its website still looks like a relic from 20 years ago. In 1993 Renaissance stopped accepting new customers. Fees were multiplied from 5% management + 20% success fee to 5% + 44%. Brutal, but even so, their net returns still stood out far above the rest. Not only that, but also In 2005, they had already expelled from the fund all former investors who were neither partners nor employees, leaving Medallion exclusively for them, and creating for the outsiders the first of the 3 institutional funds of which we will give details later: RIEF, RIDA and RIDGE.

.

Scientific background applied to markets:

The success encouraged Simons to hire more and more brilliant scientists. The next batch of gifted people to join the Renaissance family was a team of mathematicians from IBM's research centre in Yorktown Heights, NY, who were struggling at the time to get machines to recognise, emit and translate human speech. Let's just say that the parents of Siri, Alexa and Google Translate. At first mathematicians tried to rely on linguists to codify grammar, but they soon realised that the problems they faced were much better solved by mathematical probabilities than by language experts.. Mercer for example disappeared for months to type conjugations of French verbs into a computer. Processing his data allowed him to write an algorithm that found the most plausible translation for each sentence: «Le chien est battu par Jean» translated as «John does beat the dog», which was a dramatic improvement on the literal translation that systems without such algorithms were running up against. With every linguist they fired and mathematician they signed up, the system took a step forward. A similar thing happened with speech recognition: «Given an auditory signal x, the speaker probably said y«. «Recognition and translation are the intersection between mathematics and programming,» said Ernie Chan, who worked in the 1990s in IBM's research department and today manages QTS Capital Management.

.

Mercer and Brown then made a bold proposition to IBM: «Let us build a computer model to manage a part of your pension fund».». At the time IBM was managing a $28 billion fund for its employees. IBM rejected the proposal, thinking what would language programmers know about the investment world? But Mercer and Brown were already determined to apply their knowledge to making money in the financial markets. IBM was also at a low ebb, and it was easy for Simon, Mercer and Brown to recruit talent at the time. Renaissance was created by mathematicians who learned to program, not the other way around. They learned how to build large systems where many people were working at the same time. That was another competitive advantage of Renaissance.

.

Talented additions came and went, the Della Pietra twins (String Theory), Lalit Bahlt (responsible for human speech recognition algorithms), Mukund Padmanabhan (digital signal processing specialist). Almost all of them had worked together at IBM. They soon realised that tackling the market was much more demanding than the advances required at IBM. Either your algorithm was better than the rest - which were starting to flood the markets - and you made money, or it was worse and you went broke. High pressure was tremendously productive. Renaissance spent a lot of resources collecting, sorting and cleaning data, and making it accessible to its researchers. «If you have an idea, you want to test it quickly. And if you have to get the data you want to use right first, it slows the process down enormously,» said Patterson, another code breaker who worked for British intelligence and was part of Renaissance until 2001. But intellectual challenges are not the only incentives for this group of data-hungry brains. They also enjoy something more intangible: The feeling of a family of top-level scientists and the complicity and satisfaction that this brings them. Simons was like the benevolent father figure who added emotional intelligence to a group as diverse as they were geeky.

.

When the IBM scientists joined Renaissance, Medallion was already earning more than 30% net of commissions. And almost a third of that came from futures trading. In those early days, the inefficiencies of the market were more visible and exploitable than they are today. For example, one of their scientists noticed that there was a 15-minute gap between the close of options and futures, which allowed them to create a specific system to exploit that for a time. The market was full of aberrations, and the scientists investigated each one to death. The sum of all of them generated very large amounts of money for them. In the beginning it was millions, but after a few years it was in the billions. But as the financial system became more sophisticated with the proliferation of other quantitative funds, inefficiencies became scarce.

.

When Mercer and Brown came to Renaissance, they started working separately, but soon realised that they were more powerful working together. They fed off each other: Brown was the optimist and Mercer the sceptic. «Peter is very creative with a lot of ideas, and Bob says, I think we need to go deeper on this one,» Petterson said. They took over the group working on listed stocks, which were losing money. It took no less than 4 years to make the system work.. But Jim Simons was very patient. The investment paid off, and even Today, listed equity managers, through their derivatives and leverage (let's not forget that inefficiencies today are much more subtle) still generate the lion's share of Medallion's profit.

.

Simons explained in an interview in Institutional Investor back in 2000 that a winning [quantitative] system must be highly layered. «With every new idea you have to determine: Is it really new or is it somehow implicit in something we've already done? Once that's determined, the team has to figure out how much it should weigh in the mix.» He explained that signals can cool off at any given moment, but that vigilance must be maintained because they can emerge again at any time, or even withdrawing that vigilance can have an impact on the performance of the whole. The trade can be in any asset class and last for fractions of seconds or many months. In a lecture Brown gave in 2013 he explained an example that they shared with outside investors at the time, and was therefore public: By studying the weather in financial centres around the globe they found that local markets have a subtle tendency to rise more on sunny days than on cloudy ones. «It turned out that if it is cloudy in Paris, the French stock market is less likely to rise that day than if the sun shines during the opening hours of its market».» he said. It was not a big money maker, as that only happened slightly above the 50% of the time. But with the right tools and system in place, they are exploitable signals, along with many others. Brown continued: «The point is that there can no longer be obvious and powerful signals, because they would have been exploited by others as soon as they were incipient. What we do is look for huge amounts of signals, and for that we have 90 PhDs in mathematics and physics, who just have to sit there every day to distinguish them from the noise of the markets. We have over 10,000 processors (year 2013) down there who are constantly gutting very diverse data in search of those signals». Nowadays the methods of profiting from the market are as secret as they are difficult to imagine. A couple of years ago information was leaked that they were planning to use GPS (atomic) clocks to synchronise buy and sell orders in different markets, through nearby servers that manage to take massive positions without their purchases altering the market price and before even the HFT (High Frequency Trading) funds have time to react. We cannot even imagine what they will (or do) with quantum computers.

.

In addition to language specialists, Astrophysicists have been especially successful throughout history in deciphering systems. Such scientists shine above the rest when it comes to finding patterns in a sea of data. noisy. String theorists have also been particularly successful in filtering data. And the Della Pietra brothers, who along with others of their team at IBM were involved in the listed equity area at Renaissance, were among the first to shine in their field. These identical twins, now 58 years old, have never been apart from each other. Both attended an advanced honours programme at Columbia at the age of 16, graduated from Princeton with a degree in physics and received their PhDs from Harvard in 1986. They always sat next to each other, recalls his former professor of abstract algebra at Princeton. «Their conversations were full of argumentation. They were passionate mathematical discussions, and they were always correcting their professors». The fact that they are identical twins seems to take them to another dimension. «They are almost telepathic,» says Ernie Chan. At Renaissance, the Della Pietra's have always had adjoining offices with a large window for constant communication. «They are very creative and competitive with each other,» adds Patterson, to whom they reported directly for a few years.

.

The IBM team focused on constantly improving system efficiency and performance. As the Renaissance models were essentially short term, focused on fine-tuning transaction costs and how their own movements affected markets, both very difficult problems to solve, according to other fund managers. quants. They also ensured that trades and profits were in line with the system, since a bad price or any other crack could spoil the whole outcome of that particular operation.

.

Medallion reserved exclusively for members and employees:

The amount of money invested by an employee in Medallion depends on his or her overall contribution to the company. And collaboration with the environment is seen as key to having a bigger slice of the pie. Employees are allowed to buy a limited number of shares in the fund. In addition, a quarter of their salary is invested directly in the fund for at least 4 years. They all pay, of course, the tremendous 5% mgmt fee + 44% performance fee. Simons made it clear from the start that the size of the fund matters, and that too much money hurts performance. Renaissance currently limits the size of Medallion to 10-12 billion, which is double what it was a decade ago. It is therefore not uncommon for partners and employees to disinvest large sums of money to maintain a manageable fund size. Profits are also usually distributed on a semi-annual basis.

.

Thanks to Medallion, Simons, who still owns the company's 50%, amasses a fortune of 16 billion, according to the Bloomberg Billionaires Index. The other Renaissance heavyweights such as Laufer, Mercer and Brown have unquantified fortunes publicly, but have probably amassed many hundreds of millions each. But in a way, money, like the family atmosphere among the partners, keeps them together, with the exception of a few scientists who, already wealthy, have preferred to devote their intellect entirely to research or philanthropy. In general, few employees and partners leave Renaissance over the years. Why should they? The intellectual challenges are as attractive as they are constant, the colleagues are top-notch and the salaries are astronomical.. As all the employees have become wealthy, their lifestyles have changed. Trains to Manhattan have given way to private helicopters. Scientists have traded in their Hondas for Porsches, and expensive hobbies have become the norm. Simons' cousin Robert Lourie, who heads the futures research team, built stables and a riding arena for his daughter. State-of-the-art yachts are also the order of the day, and spending on company trips for team building activities is unmentionable. Simons, a heavy smoker, even took out a fire insurance policy with his favourite restaurant to allow him to continue smoking his beloved Merit after dinner. You will understand better now why the coast where the management company is located is known as the Renaissance Riviera.

.

However, the money has, of course, also brought them some displeasure. In 2001 they hired a Russian scientist, Alexander Belopolsky. Patterson was reluctant to hire him because Belopolsky had previously worked on Wall Street, where he had jumped from one job to another. His fears were well-founded. In 2003 Alexander and another Russian, Pavel Volfbeyn, announced that they were leaving to work at another hedge fund, Millennium Partners, where they would be working on a new project. had negotiated multi-million dollar bonuses in exchange for trying to copy Renaissance's know-how.. Of course, both the Russian scientists and Millennium were sued in court by Renaissance, and the matter was subsequently settled by a financial settlement of which no details are known.

.

However, not all Russians were unhappy at the company. Around that time, another scientist named Alexey Kononenko, who came out of the former USSR and received his PhD from Penn State in 1997, was promoted and moved up the Renaissance organisational chart with a bang, raising some eyebrows among the more senior staff. Kononenko was seen having dinner at Simons' house, and that was a sure sign that the Russian had a gift that made him more special than the rest of the company's gifted brains. Time proved him right, and Medallion achieved returns in excess of 40% per annum net after that dinner.

.

Building on the crash of 2007 and 2008, what is the secret of Renaissance?

When competitors or former investors are asked how Renaissance can continue to achieve such impressive results, the answer is unanimous: They run and evolve more than the rest.. Even so, they have not been without their scares. According to sources close to the fund manager, in August 2007 the mortgage market crashed, wiping out many hedge funds along the way, which literally disappeared from the map, including the 30 billion giant managed by Goldman Sachs. The disasters of so many trapped investors and leveraged quantitative and non-quantitative hedge funds flooded the markets with sell orders, making the situation much worse. Medallion suffered a loss of almost a billion in a matter of days, almost 20% of its size at the time.. This, which had never happened before in the fund's almost 30-year history, gave the team of scientists food for thought. They even considered whether they should reduce risk to ensure the fund's survival by selling off some positions. Fortunately, the scientists put their hearts aside and focused on their brains, letting the systems do their job. In the last four months of the year, they not only recovered their losses but closed the year with a brutal profit of +85.9% net. But it doesn't stop there. In 2008, the year of the stock market crash, profits were even higher, close to 100% net. The Renaissance partners reaffirmed their principles: «Don't mess with the models». And they also learned a lesson: the damage that large third-party bankruptcies can cause to the market must also be calculated.

.

Quantitative managers often say that there is no system that is effective forever. The variables are infinite and the markets as changeable and diverse as the human race and its globalisation. So one wonders how much longer Renaissance will be able to deliver these superior returns. The reality is that almost a decade after Simons' official retirement, the money-making machine is still running, and the old ex-IBM team is still between 50 and 65 years old.

.

The visit of Cluster Family Office to the Renaissance facilities:

We will now tell you our impressions of the visit we made a couple of years ago to the Renaissance bunker in Long Island (images below from google maps). We will start by saying that, once they passed their due diligence to be accepted as institutional investors, we had to insist that we were allowed to visit their headquarters., The majority of those selected are only shown their Manhattan offices, which are more «than the Manhattan offices".«commercial»but also spectacular. About 40 people work in Manhattan on a regular basis, but the offices are large enough to house the more than 300 employees who work at renaissance. Why is that? Well, because in Manhattan they have a backup and servers equivalent to the equipment they use in the bunker, and from time to time they practice a drill as if it had been rendered inoperative, moving all personnel for a day or two to Manhattan., in order to ensure that they continue to work perfectly in the event of an emergency in the bunker. That's how geeky and rigorous they are.

Why do we call the Renaissance headquarters on Long Island a bunker, if it appears to be a building (or several), large, yes, but just like any other? Well, because in addition to the access control on the road and the fact that it is surrounded by a lush forest that naturally conceals the facilities, inside there are a multitude of access controls, depending on the degree of restriction desired for each part of the building. Some doors were crossed when our companions swiped a simple magnetic strip through the reader, but others, closer to the heart of the company, required additional codes and even their fingerprints.. In addition to its two-storey height and its whimsical shape, which is slightly reminiscent of the Pentagon building, the main block also has two underground levels which house, among other secrets, the computer room. They agreed to show us around for a few minutes. It was a huge, white-walled, perfectly cooled space with a double-height ceiling. In the centre of the room, half a dozen 2-metre-high columns were lined with processors lined up on either side, forming long corridors between each column. The length of each column was impressive - we estimated at a rough guess that they must be between 50 and 60 metres long., The processors, as they allowed us to walk down those aisles from one end to the other. Obviously the figure of more than 10,000 processors that Brown talked about in 2013 was no exaggeration. Inside that room was another smaller room, to which we did not have access, which must have contained other mainframe computers. Interestingly, all the cooling machinery was outside that large room, so that even the air-conditioning maintenance technicians didn't have to enter the computer room at all. We had never seen anything like this before, and probably very few private companies have such a computer arsenal. We immediately understood what other big names in quantitative management were talking about when they said that «...the new system is a new way of doing business.«No one is at Renaissance's level in terms of data processing and analysis, not even close.»

.

During the visit to the rest of their facilities we could see that indeed all the individual offices are identical in size and decoration, following the guidelines of the partners. We did not see a single closed office door, everyone works with their door open to facilitate interaction and the exchange of ideas., as Simons states in an interview. They explained some of their internal processes, such as the challenges that rapporteurs of new proposals to be incorporated into the system have to overcome. Any new idea must overcome a huge number of Ph.Ds (PhDs in physics, mathematics, etc.) trying to smash it mercilessly. Y the proposal of the rapporteur(s) will only progress if it overcomes the criticism and convinces the eminent. The next step is to test the proposal with models for a period of time. If it continues to work, it is tested with operations and real money in small amounts for another period of time. And if finally all the results are positive and there is no affectation or interference with the rest of the systems, it is implemented. The process can take months or even years, It is not fully implemented until it is empirically well proven and tested. It was impressive to see the challenges, where these new proposals are debated to death. There was a large screen presiding over a huge oval table with about forty seats, and around it a second ring of chairs for a total audience of more than a hundred. Imagine that room full of Ph.Ds arguing vehemently and trying to find the cracks in any new proposal. Truly, nothing that does not certainly improve the existing system will make it through that first theoretical filter and subsequent practical implementations.

.

The comments and behaviour of the managers we met that day confirmed to us that indeed the motivation for scientists to stay at Renaissance is not primarily money - once they have become rich enough, what keeps them there is the attraction of an intellectually challenging environment and being surrounded by the best. And what better place than here, they said. They also told us that the intellectual challenge of working surrounded by 90 Ph.Ds of the scientific elite not only serves to retain the talent already working at Renaissance, but also to attract eminent people who are bored in their university research positions. These profiles, tired of no professor or university colleague daring to contradict them on anything, fit perfectly in the fun that an environment such as Renaissance offers them, where they can the challenges they constantly subject each other to are at a level they could never find in any university in the world.. The concentration of talent, not to mention the impressive semester cheques, acts as a real intellectual magnet to retain and attract the most prodigious minds.

.

Funds open to institutional investors: Renaissance Institutional Funds

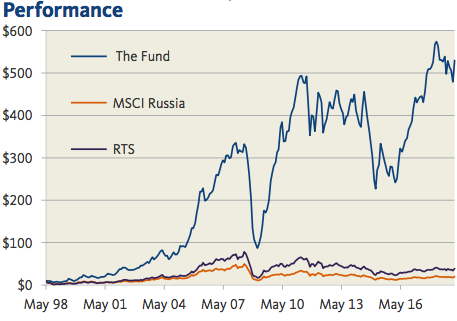

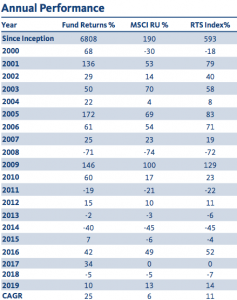

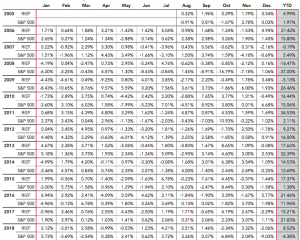

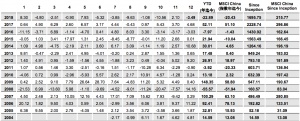

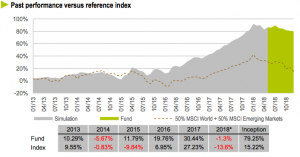

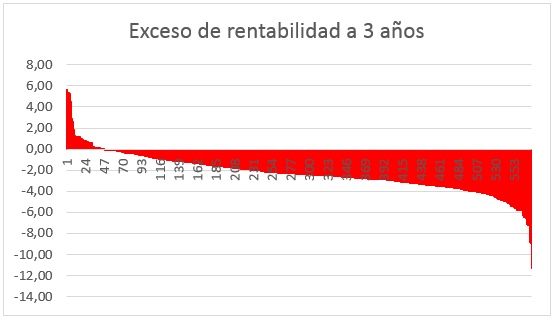

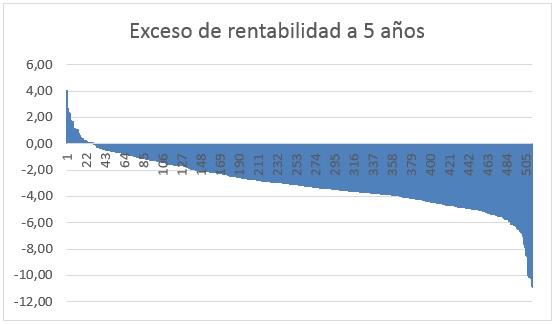

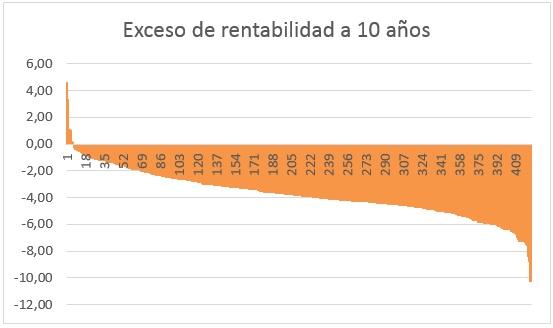

In addition to the legendary Medallion, which is reserved exclusively for members and employees, as mentioned above, the fund manager has 3 funds open to institutional investors with a minimum of 5 million to invest and who have passed the fund manager's internal due diligence: Renaissance Institutional Intitutional Equity Fund (RIEF), Renaissance Institutional Diversified Alpha Fund (RIDA) and Renaissance Institutional Diversified Global Equities Fund (RIDGE). They explained to us how they discriminate the management of Medallion compared to that of the RIEF fund, the oldest of the 3 funds that are still open to institutional investors (you can see its track record since 2005 in the table below). They readily admit that their «best ideas» are applied to the Medallion, and that their «second best ideas» are used in RIEF.. The other two institutional funds, RIDA and RIDGE, are different animals. The latter two are seen as tests or platforms where other (apparently more conservative) ideas are applied, they are perfect laboratories for their research, although for many other fund managers they would be their own funds. flagships or flagships, without a doubt. After analysing the 3 funds, from Cluster Family Office We decided to invest for the moment only in RIEF, which we could define as the most similar quantitative fund of the three to Medallion, essentially focused on equities from all over the world and long-biased. In the graph below you can see its performance since its launch in 2005, when -as we have already said- all external investors were definitively expelled from Medallion.

.

The good news for junior investors, as we mentioned at the beginning of this article, is that can access funds of funds that slice these combinations starting at 125,000 euros/dollars., although logically paying an additional commission, as we explain in «Funds that make inaccessible funds accessible«. Medallion will certainly remain reserved exclusively for Renaissance partners and employees forever. But investing in the substitute RIEF The minimum amount of 5 million and the due diligence carried out by Renaissance itself to decide whether or not to grant access to the aspiring institutional investor are insurmountable barriers for the vast majority. This is why being able to enter through the back door via a fund of funds is an extraordinary opportunity. The only one.

.

Disclaimer: This article does not represent an investment recommendation for the products mentioned. The funds referred to in the article are not registered for marketing in Spain and are only suitable for qualified investors, with minimums ranging from €125,000 to €5,000,000.