SEE ALL THE COSTS AND DETAILS OF THE PROCESS HERE

.

Every year it is becoming more and more common for Spanish families to consider sending their children to study at American universities. Despite this, many still have the misconception that it is a luxury reserved for an elite of millionaires and/or gifted eggheads. However, study at a university in the USA is not difficult at all, and the reasons for sending our children to universities in the USA are multiple and justified. For example, the international prestige of a degree from a university there is far superior to that of comparable alternatives in Spain. It should also be borne in mind that the likelihood of finding more and better jobs upon return, either in the USA itself or in any other country in the world, is much higher with a US degree. As for personal experience, no doubt, living inside of a university that is like a real city in its own right, with its own flats, restaurants, cinemas, concert halls, sports stadiums, shops, gyms, libraries, banks or police, has no comparison with simply attend classes at a Spanish university.

.SEE ALL THE COSTS AND DETAILS OF THE PROCESS HERE

.

The million-dollar question in the title of this article is: Can I really send my children to a university in the USA? Most families would think that only an elite group with extremely bright sons or daughters can get enough scholarships to study there, unless the parents are millionaires and can afford to pay huge sums. But they are wrong. The flexibility of the American university system allows foreign families to access academic scholarships that are relatively suitable for any good student.. This is a true policy of attracting universal talent. Let's say that with a remarkably high average of the last 4 years of studies in Spain, that is, from 3rd ESO to 2nd Bachillerato, with grades between 7 and 9 out of 10, you can find scholarships that cover a very substantial part of the cost of tuition fees. Obviously there is also the cost of room and board for the student, but this is comparable to the cost of any student from here attending a university in a Spanish city other than their own, which would require them to pay for a student flat and daily meals.

The million-dollar question in the title of this article is: Can I really send my children to a university in the USA? Most families would think that only an elite group with extremely bright sons or daughters can get enough scholarships to study there, unless the parents are millionaires and can afford to pay huge sums. But they are wrong. The flexibility of the American university system allows foreign families to access academic scholarships that are relatively suitable for any good student.. This is a true policy of attracting universal talent. Let's say that with a remarkably high average of the last 4 years of studies in Spain, that is, from 3rd ESO to 2nd Bachillerato, with grades between 7 and 9 out of 10, you can find scholarships that cover a very substantial part of the cost of tuition fees. Obviously there is also the cost of room and board for the student, but this is comparable to the cost of any student from here attending a university in a Spanish city other than their own, which would require them to pay for a student flat and daily meals.

.

.

As mentioned above, there is total flexibility, i.e. there are universities for all tastes and academic levels. For example, a family with a child who has a grade point average in the lower range of the above mentioned can choose to go to a less prestigious university with a higher scholarship, to a higher level university with a small scholarship, or to a top university without a scholarship. The same applies to sports scholarships: If the student's level in his or her sporting discipline is very high, he or she can opt for a less prestigious university practically free of charge or for a more prestigious university paying most of the cost out of pocket. Depending on the circumstances of each student and the willingness and financial capacity of the family, a tailor-made option will be chosen. And of course there are also options for those students who simply pass the baccalaureate with averages of 5-6 out of 10 and do not excel in any sport, but without scholarships, which will force parents to cover the full cost. In fact, studying at a university in the USA is an extraordinary opportunity for the brightest, for simply good students and even for less bright students, who would not be able to reach the cut-off mark to be able to study at a Spanish university the degree they like the most, but could do so at various American universities, thanks to the aforementioned flexibility.

.

.

.

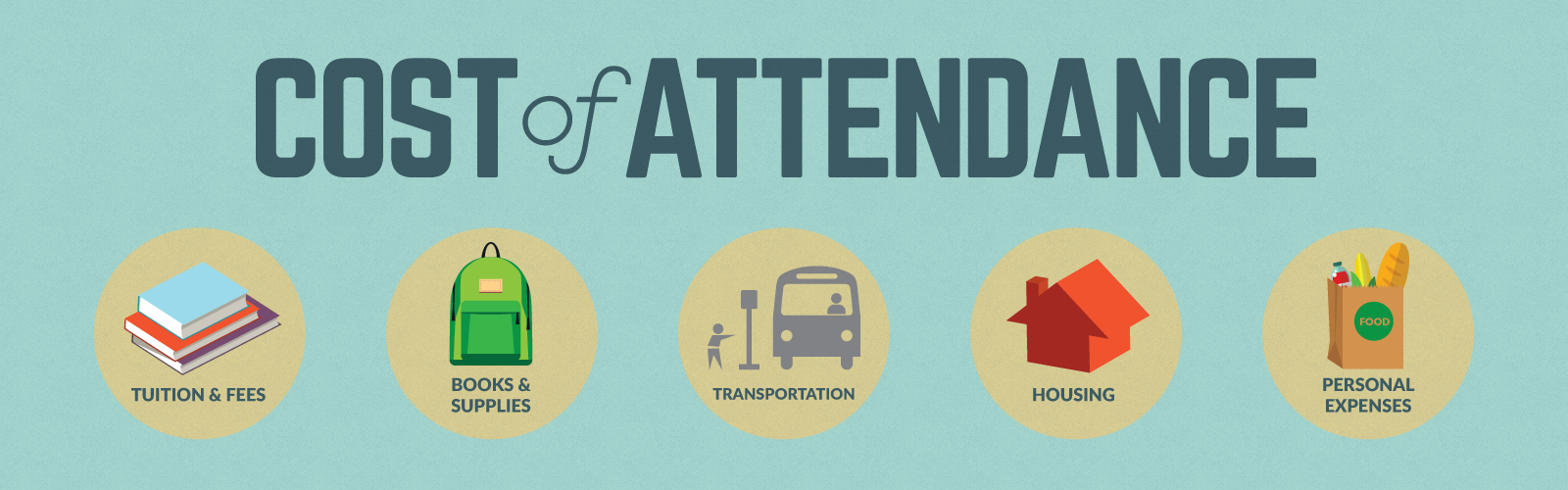

In order for readers to get a practical idea of the costs without grants The approximate costs that a Spanish student who decides to go to the USA to obtain a degree can assume, here are a few figures per year, The programme is based on a standard academic load, from mid-August to the beginning of May, with 24-30 credits per year and a 4-4.5 year expectation to graduate:

.

- Tuition fees:

- Between €10,000 and €55,000 depending on the prestige and quality of the university.

- Cost of room and board:

- Between 8 and 10 thousand euros

- Books, materials, travel and miscellaneous expenses:

- Between 2 and 3 thousand euros

- Health insurance for international students:

- Between €1,000 and €2,000

Therefore, if you want to send your child to an American university, you have to calculate logistical costs of between 11 and 15 thousand € per year, plus the annual tuition that depends entirely on the prestige and quality of the university, and all of this could come with a scholarship to a greater or lesser extent as we have already said. As you can see, the costs of room and board are the same as what it would cost to send our children to study in any city in Spain. And the annual tuition fees can be perfectly equivalent to the tuition fees in some private Spanish universities, even without access to any scholarship. SEE ALL THE COSTS AND DETAILS OF THE PROCESS HERE

.

Here you will find a example of housing where students from Arizona State University live. It is obvious that the atmosphere and quality of life is light years away from the student flats that university students usually rent during their studies in any city in Spain.

.

We have already seen in the price table above that with some scholarships, and even without any, the costs of sending our children to universities in the USA are affordable for many more families than we might think. However, it is undoubtedly an effort and financial sacrifice on the part of the family towards their children. But there is no better inheritance than to give them the best possible education during their lifetime so that they can defend themselves before the world with the best weapons and the most prestigious qualifications. Wouldn't it be infinitely more useful and profitable for them that we have paid for their studies at the best universities on the planet than to have left them a handful more money in our will? From our experience in the formation of heirs and the relationship of the new generations with the family heritage, we can assure you that this is the case. If our children are to make their way in the difficult world they will have to face, it will be of little use to them if we leave them only a basket full of fish as an inheritance. We must provide them with the best fishing rod, the best equipment and the best fishing instructors. And their training must enable them to find the most fish-filled international waters and to move in them with complete ease. That will be our greatest legacy.

.

One of the most important benefits of the whole application process is that, during the months of preparation, the pupils will give a huge qualitative leap in maturity and motivation. Their personality will mature due to the process of internal reflection that the pupils will go through as they work on their Essays with our coaches. They will have to explain in essays of only 500 to 600 words who they are and why the university should choose them over other candidates. What personal merits they have accumulated in their short life and what they want to make of it in their future. They will become aware of the high level of competition for admission to the university of their dreams (don't worry, the final list of universities to which they will apply will include options accessible to the student and no one will ever be left without at least one letter of admission). This whole process will make them appreciate much more and much better the financial effort made by their parents for them. For the first time in their lives, they will have to analyse who they are and present their best version of themselves to the world in order to be worthy of the prize of receiving an admission letter. Here we leave you a few videos with some of the emotional reactions of students when they receive the news that they have been admitted to the university of their choice. These videos which abound on YouTube, will give you an idea of what it means, for the teenagers who choose the American university path and for the whole family, to be rewarded at the end of the whole process of effort. You will not tire of watching them. When that time comes, we can guarantee that your children will have grown a great deal personally compared to when they started their journey 9, 12 or 18 months ago.

One of the most important benefits of the whole application process is that, during the months of preparation, the pupils will give a huge qualitative leap in maturity and motivation. Their personality will mature due to the process of internal reflection that the pupils will go through as they work on their Essays with our coaches. They will have to explain in essays of only 500 to 600 words who they are and why the university should choose them over other candidates. What personal merits they have accumulated in their short life and what they want to make of it in their future. They will become aware of the high level of competition for admission to the university of their dreams (don't worry, the final list of universities to which they will apply will include options accessible to the student and no one will ever be left without at least one letter of admission). This whole process will make them appreciate much more and much better the financial effort made by their parents for them. For the first time in their lives, they will have to analyse who they are and present their best version of themselves to the world in order to be worthy of the prize of receiving an admission letter. Here we leave you a few videos with some of the emotional reactions of students when they receive the news that they have been admitted to the university of their choice. These videos which abound on YouTube, will give you an idea of what it means, for the teenagers who choose the American university path and for the whole family, to be rewarded at the end of the whole process of effort. You will not tire of watching them. When that time comes, we can guarantee that your children will have grown a great deal personally compared to when they started their journey 9, 12 or 18 months ago.

.

Applying to American universities is the best personal growth process they can undergo, and it will come at the best time in their lives (between the ages of 15 and 18) to make the leap in maturity they need.

.

Finally, we leave you with the links to some of the universities where we have had the pleasure of placing boys and girls thanks to our advice service for graduating in the USA. Taking a look at their websites may be a good start for you to see the difference between the American university path and the domestic one: Brown University, Penn State University, Wesleyan University, Barrett Honors College at Arizona State University, Clark University, Tufts University, Northeastern University, Georgia Tech, Columbia University, UCLA, etc.

.

Request HERE the cost breakdown and your chances of admission.

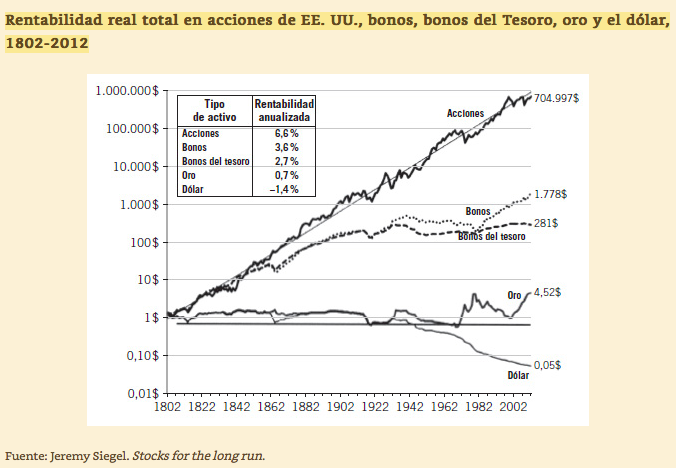

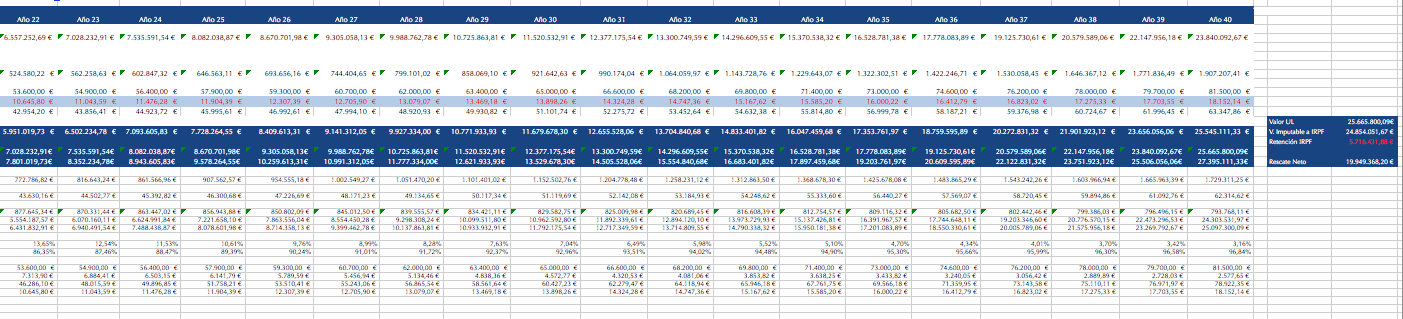

The medium to long term horizon for investors is very dark. A report by McKinsey Global Institute (

The medium to long term horizon for investors is very dark. A report by McKinsey Global Institute (