You will probably be familiar with this title, since only six months ago we published the article entitled «.«Chinese Queen's Gambit»in which we analysed the reasons why Xi Jinping had taken certain internal control measures. Well, now we are witnessing another chess game, this time on the European international geopolitical chessboard with Biden and Putin as opponents, under the watchful eye of Germany, the rest of the European countries and of course China, always waiting to take advantage of any resulting scenario.

.

It is worth noting that this conflict between NATO (Biden), Ukraine and Russia (Putin) coincides with the US's negotiations with Iran on the nuclear issue and the applicable sanctions. The background to the whole conflict is none other than the global energy flow in the coming years. We could call it the New World Energy Order.

.

How many images of NATO troops and heavy weapons in Ukraine have been seen on our Western television screens? And yet there are plenty of them, but only the menacing Russian troops appear again and again everywhere. In fact, the press conference held by the State Department spokesman on Thursday, February 3, was a very good example of this. Ned Price is not wasted. In it Price accused the veteran journalist Matt Lee of preferring the official Russian version to the US version of the alleged existence of the preparation of a false flag attack, while Lee only repeatedly asked the US State Department spokesman for proof, who said that the proof was simply the official statement he had just made. Here is the excerpt from the video with the tense moment from last Thursday's press conference. Incidentally, Ned Price has already has not appeared The icing on the western propaganda cake is the mistake of none other than Bloomberg publishing fleetingly the headline «Russia invades Ukraine» before the alleged false flag attack or any other move for which the headline is designed. These are all examples of the news bias that we also suffer from in the West, and not only in the Chinese- or Russian-controlled media in the East.

.

That is why it should be recalled time and again that the start of the conflict was caused by the threat of Ukraine's imminent NATO membership, insistently urged by the USA, in order to be able to place heavy weapons on the Russian borderline itself. That and no other was the opening of the chess game and the conflict, in which Biden made the first hostile move. And this threatening opening has generated a logical response from Russia, which, baring its teeth, has amassed troops around Ukraine in an attempt to get Biden and NATO to return to square one and leave the chessboard as it was. We are therefore facing a confrontation that would not have occurred if Biden had not actively pushed for Ukraine's inclusion in the Western military alliance, despite the Western media's insistence on selling the idea that it was Putin who started the conflict by threatening to invade Ukraine unilaterally, something the Kremlin has denied to no avail. So we are dealing with a US action and a Russian reaction, and not the other way around, as all the Western media are selling it without the slightest rigour or blushes.

.

Having made this necessary preamble, let us now turn to the conclusion itself. Let us start from the premise that any political-military conflict that does not lead to a classic open war, in disuse in the developed world since the Second World War, has relative winners and losers. And that often the most feasible outcome is the most plausible one, i.e. the one in which all parties involved suffer the least possible economic damage.

.

In this US-NATO-Ukraine-Russia conflict, the least hurtful outcome would be a commitment by Ukraine not to join the Atlantic Alliance club, at least for a decade, in exchange for Russia also renouncing the incorporation of new Russophile territories in Eastern Ukraine or even giving back some of the territories it already holds in the Donbass. That is, more or less, back to square one of just a few months ago. Logically, to get to that point, Putin «demands» the major, i.e. that the NATO line returns to the borders where it was in 1999, when Estonia, Latvia, Lithuania, Slovenia, Romania, Slovakia and Bulgaria joined the Atlantic alliance. A Western military goal to what was then a very weak Russia. And Putin's impossible demand is the chrome he will be more than willing to concede if he gets a few more decades of Ukrainian independence from the Western military alliance.

.

An agreement would make perfect sense for both parties, as explained by Gavekal in his report on Russia, as it would allow Ukraine's economic progression and the pacification of its endemic low-profile armed conflict with Russia in the east of the country, both of which are impossible to achieve if the conflict escalates. For Putin it would put out the fire on a new front of NATO's threatening rapprochement with Moscow for at least a few years. And for the EU it would be the lifeline it badly needs to avoid the energy suffocation it would face in the event that Russia decides to turn off the tap, not only on gas but also on oil.

.

.

On the other hand, if the conflict escalates with galloping sanctions against Russia, the logical response will be to turn off the tap to Europe, and with that we will see fuel prices rise to infinity and beyond and an outrageous inflationary spike. That in turn would generate a radical increase in interest rates in an anaemic economic environment, i.e. a textbook runaway stagflation, which would trigger all sorts of market dislocations, risk premiums and also economic costs that would take a long time to recover (especially in Southern Europe). Putin knows this and is therefore willing to use his power to get the chessboard reversed to the starting position, i.e. 2021. Energy self-sufficient Biden does not have as much to lose as Europe. But the destabilisation of an EU with already semi-ripped north-south seams would create a scenario in which the Western bloc would be at a distinct disadvantage vis-à-vis a China-Russia alliance that is going through one of its best moments. As shown by this button in the form of a new gas pipeline and a 30-year supply agreement between Putin and Xi, which to top it all off is denominated in Euros.

.

However, resolving the conflict via pact and de-escalation does not mean that there will not be some bombings and deaths, unfortunately. Negotiations are usually concluded in-extremis, both in time and in form, i.e. after skirmishes that seem to foreshadow imminent and inevitable military escalations. But let us remember that the economic cost of open war (read ground invasion and open NATO-Russia military confrontations) is unaffordable for Europe, high for Russia and extremely dangerous for the stability of the Western bloc USA-EU.

.

.

Therefore, an agreement seems the most likely outcome. But it is likely to be an unofficial agreement, i.e. without light and stenographers or photos of the leaders shaking hands in front of journalists, but an agreement nonetheless. The only ones who would clearly lose in a scenario of de-escalation and a pact between Russia and the West would be the Russophobic and ultra-nazionalist Ukrainian politicians (yes, with a «z» for Nazis), once nurtured by the West to perpetrate the 2013 coup d'état that was whitewashed under the name of the Euromaidan revolution. Which by the way was not such but a violent regime change orchestrated by the West, as Rafael Poch well explained in this prescient article in 2014, which had little media coverage as was to be expected. As we said, these Ukrainian ultranationalists are perfectly sacrificable, in exchange for Europe not being blown apart by the energy suffocation that could result from the culmination of Ukraine's NATO membership.

.

It is true, however, that a priori Biden has the least to lose if the conflict escalates, and that adds risk and uncertainty to the situation. Moreover, Putin knows that he will not get concessions if his military threat is not credible, and for that some bloodshed will probably be unavoidable. But, as we have already said, usually the options that end up being given in any conflict are the least costly economically for the parties, and in this case it is undoubtedly a temporary backtracking on Ukraine's inclusion in NATO and a return to square one in 2021 (not 1999 as Putin initially stated in his letter to the Three Wise Men). The Normandy Quartet knows that it is the four of them who have the most at stake in this conflict, and they are rushing to negotiate without the interference of those who have the least to lose, namely Biden and NATO.

.

In all this turmoil, the gains of fishermen investing in Russia at the height of the conflict will, as always, be obvious only after the event. And as always the Chinese, the smartest in the class, They are already benefiting strategically from the Russian-European turbulent river and continue unstoppably towards world hegemony.

After listening to and reading many Western and Eastern analyses of the Chinese government's move in its financial markets, and largely agreeing with the analysis of Gavekal, What is clear to us is that these are decisions that will benefit China's interests in the medium and long term, entrenching its imminent global dominance. As with gambits in chess, which sacrifice a pawn or other piece at the outset to gain an advantage later, Xi Jinping's government is sacrificing certain sectors and the size of certain companies in a surgical manner, although the collateral effects of such policy decisions may be noticeable in the short term, and especially amplified in the Western media.

.

The exact reasons why Xi has targeted sectors such as technology, online education and the financing of Chinese companies in the US market are known only to his closest and most loyal political circle. But we will now explain 7 reasons that could well be behind the Beijing government's moves.

An exhibition of power, a warning to all, anyone who moves will not be in the photo, a punch on the table or whatever we want to call it. In short, the government is marking its territory with these actions, demonstrating that Xi's pulse is not trembling to lead the flock towards more and better pastures for the common good (of the party and the state). Growth and global economic dominance, yes, but without the government letting go of the reins at all. An empirical demonstration that Capital will not weaken the foundations of the party.

Pre-emptive action in the face of escalating US measures against China. What better strategy than to sacrifice in advance companies dependent on US financing, thus discouraging the potential pressure that Washington could exert on Beijing if it threatened to turn off the tap on Wall Street. China will now be less dependent on US investment, knowing that investment in Chinese companies today already comes from many other countries that are increasingly allied with and dependent on China. There is life (investors) beyond Wall Street, and more and more of it every day.

As for the online education sector, which has been hammered in the markets by measures that would force its companies to become non-profit entities, they seem to be the scapegoats for the extraordinary rise in the cost of education in China. And private education, as widespread as online education can be, could easily escape government control and supervision. In other words, the move will lead to cheaper education (even at the risk of temporarily less access to education as a whole) and greater control, not only of educational content and systems but also of the shareholders in this sector of business.

Another sector crunched by the government's measures is the food and home delivery business. But despite the bombastic headlines warning of the sector's collapse, the measures taken by Xi's government seem entirely reasonable. The main measure he has ordered is none other than the obligation for the wage and working conditions of the riders or delivery drivers to be equal to those of any other wage-earner who reaches the legally established minimum. This is clearly also in the medium and long term interests of the Chinese economy.

Back to industry: The measures that are shrinking the size and influence of some technology and internet-related companies can be read as a return to industry. But that would probably be too simplistic a reading because China is not going to give up on technology companies that lead to progress in R&D - quite the contrary. What seems to be targeted are technology companies that only cater to sterile leisure, i.e. video games and social networks, for example. In other words, companies that encourage distraction and the dedication of hours by users to non-productive activities. That is nothing.

Derived from this concept of back to industry (& back to R+D) we can also sense an intention that reminds us of the Manhattan Project. In other words, China wants its technological talents to focus on research and development of new technologies, such as semiconductors, in order to alleviate the current and future shortages that we are going to have all over the world. They encourage the potential for technological growth to go in the strategic direction that suits China's future, rather than in other directions that would only distract the population from the collective productive objective that Xi has designed and that is leading China to global economic leadership.

Because at the moment China can not only afford to see outflows of foreign investment, but this outflow is also a perfect escape valve for the unwanted appreciation of the Renminbi (RMB). Let us not forget that China has a trade surplus of $50 billion per month and that its currency also supports flows of another $20 billion in the purchase of Chinese debt by investors from all over the world. And that puts upward pressure on the RMB that is difficult to manage. These controlled, surgically designed investment outflows therefore make perfect sense from the point of view of China's strategic interests.

Some will probably say that the radical movements in share prices in some cases, such as Tencent or BABA, generated by politburo decisions, are madness and undermine the confidence of international investors. Others will say that it is Xi Jinping himself who has gone mad, damaging his own companies and sectors, in a fit of anti-capitalist communism in the purest podemite style. But even if that were the case, let us not forget that in the West we are not very sane either, With the hangover from Hurricane Trump and central banks keeping more and more zombies (companies and states) too big to fail. But nothing could be further from the truth. Xi's modern China does not miss a beat, and always governs with horizons that go far beyond a measly Western democratic legislature.

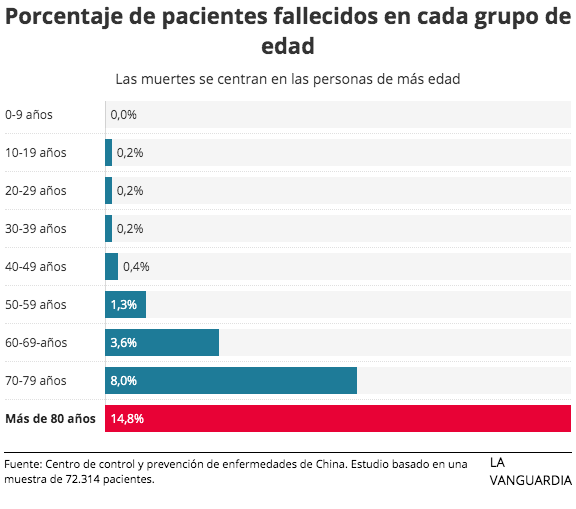

Some will say that the archive exposes the shame of everyone in this pandemic. But the reality is that it does not expose everyone equally, far from it. Today we think it is worth re-reading this article which we published 12 months ago, specifically on 5 March 2020. In it, you will see how some of us were already warning of the seriousness of what was coming, while our politicians continued with the mantra that the coronavirus was like normal flu but kills less. The most outrageous thing is that this disinformation did not only come from ignorant half-baked politicians, but from people like the very Minister of Finance and Government Spokesperson, Maria Jesús Montero. And with the aggravating factor that this lady was (and is) not only a double minister but also a doctor and surgeon, with a long history of hospitals under her direction such as the Virgen de Valme University Hospital or the Virgen del Rocío University Hospital. Or, for example, what was said at the time by the very popular and tireless Fernando Simón, a medical epidemiologist no less, who told us that masks did not protect us in any way and that we should not use them because people would make fun of us.

.

Given their medical training, we can hardly think that these reckless words of our leaders were the result of ignorance, but obviously of bad faith. As we ourselves have shown in this article, one did not need to be a doctor to see the pandemic coming at the beginning of 2020. Mere common sense and the information published by analysts and prestigious foreign epidemiologists was available to anyone who wanted to be informed beyond our TV news. It is worth re-reading this article from a year ago to recall the shameful statements made by the Spanish authorities. Because not all of us were living in the dark at the time, some of us were unequivocally warning of the seriousness of the situation and of the risk of not even having an economic recovery in the form of a U in Spain if we did not take immediate drastic measures. Rereading it a year later, with more than 100,000 The Spanish dead (68,000 according to official figures), is not to be sniffed at:

«The lies of the Spanish government and health authorities regarding the coronavirus.» (5 March 2020)

.

It is regrettable to see the differences in the handling of the emergency situation in the coronavirus pandemic between different countries around the world. But what is worrying is the attitude of the Spanish political and health authorities in the face of this crisis, as they strive time and again to distort the facts and data in order to minimise its stark reality. A mixture of cowardice and misunderstood paternalism that justifies, in the eyes of some, the absence of courageous decisions. The Spanish authorities' determination to deceive the public stands in sad contrast to the realistic and serious warnings of other governments and global health organisations.

.

The Minister Spokesperson of the Government, Maria Jesús Montero, has declared in different media, and without any blushes, that Covid-19 is nothing more than a “...a new and unacceptable project".“new flu, similar to normal flu and with an even lower mortality rate than normal flu”.” (for example in minute 10 of the following interview with him on RAC1 last week).

.

.

The unfortunate reality is that the lethality of this virus is much higher than that of seasonal flu. And any well-informed scientist, whose rigour is not contaminated by the political slogans of the government, will admit statistical figures of around 3 or 4 deaths per 100 infected. Some Spanish authorities use mortality figures for normal 2% flu, but for hospital admissions and not for those infected, thus inflating the mortality rate and making it incomparable with that of Covid-19. On the other hand, also maliciously, they proclaim that the mortality of the coronavirus is 0.7%, taking the death figures for those infected just at the beginning of the epidemic in Europe, which means that the sick who are going to die have not yet done so. To further embarrass the minister, here is the official comparison between the mortality rate of the common flu and the US CDC's Covid-19:

.

The most statistically reliable figures are found in China, where there are more and older cases of coronavirus. And those figures are now in the 3,75% mortality3012 deaths out of 80409 infected. Unfortunately, a fraction of those infected today will also die, while the number of new infections is already declining, so that this percentage is also tending to increase by about 0.04% per day, as it has done in the last few days. In other words, if the official figures in China are to be believed, mortality is indeed frighteningly close to 4%. And if we don't believe the official figures (I personally do) and think that the Chinese government is making up the mortality, then that's the end of the story. You can follow the daily evolution of the official figures in China at this page from Wikipedia, and the official figures for the rest of the world at this one.

.

However, some news which many people dismiss as being tremendist, infodemic or fake news, are in line with what is published in the majority of the world's media. international media with up-to-the-minute timelines of any new developments regarding the coronavirus,and spare no means or adjectives to keep the people of their respective countries on alert and on the lookout for health emergency. Because this state of alert and emergency does indeed punish the economy in the short term, but it saves lives. Thus, countries such as the US, where the spread of the virus is currently still proportionally lower than in Spain, are giving unequivocal instructions to their citizens to be prepared for imminent confinement o emergency situation This is because, mortality rate aside, what is clear is that this coronavirus is highly contagious, and its spread across the planet is unstoppable. Mortality rates aside, what is very clear is that this coronavirus is highly contagious, and its spread across the planet is unstoppable. That is why responsible governments are alerting and preparing their citizens for a massive infection. According to the calculations of Harvard Professor of Epidemiology Marc Lipsitch, Between 20 and 60% of the world's population will be infected by the coronavirus if we do not take drastic measures as China has done and/or an effective and viable drug does not emerge for everyone. And pending such a drug, our only option is to slow the pandemic. That means, even with optimistic mortality rates, millions and millions of deaths across the planet, at a brutal cost at all levels. What a contrast with the happy flowers statements of our ministers and health spokespersons who continue to talk about “new flu that kills less than normal flu”, right?

.

.

It is undeniable that a realistic warning about what is coming makes the population radically modify its usual activity, and with it consumption, productivity and therefore the economy plummets, as has happened in China. But courageous (albeit belated) measures, such as those taken and implemented with martial rigour by Xi Jinping, will save his country's economy in the medium and long term. Because an uncontrolled epidemic, with the mortality rate that this coronavirus entails, would have a far greater impact on the economy in the medium term than the short-term slump. Economically we could see a V-shaped economic downturn and recovery, but without bold measures by the already growth-anemic developed economies, we in the West will not even see a U-shaped recovery.

.

In Italy, the epidemic is just a few weeks ahead of us, and yesterday the decision was taken,The government's decision to close all schools and universities in the country, albeit belatedly, was a belated one. In Spain, on the other hand, despite recognise at least 3 infections in children school-age children, the closure of schools is not (yet) being considered. Not only that, but in one case it was the mother who insisted time and time again that her daughter be tested for the coronavirus, while the health authorities kept telling her to find a family member (as both parents had to stay at home because they were infected) to take her to school normally! What a botched job we are doing on such a serious issue in which we all have so much at stake! Because the fact that the vast majority of children and young people overcome the infection with mild or even asymptomatic symptoms does not in any way prevent these children and young people from infecting their parents, grandparents and teachers. These are all groups that will suffer serious consequences and whose mortality is very high, as we have seen above. Moreover, it is absurd to try to contain the epidemic by keeping infected parents at home and letting their children, who are also infected but many of them do not know it, move freely in the streets, buses and other environments with which they usually interact.

.

Another example: In Spain, the authorities have gone out of their way to emphasise that the existing infections were not from the EU (local infections) but imported, from Italy, China, etc. They insistently stressed that this was a very important detail, trying to convince the population that Spain was in a perfectly controlled situation since our infections were all imported, ignoring the fact that it is only a matter of time before there are, as there have been, community infections in Spain. However, when faced with infections whose origin is not imported, the Spanish authorities still describe them as of “unknown origin”, without yet recognising that they are already Community infections, i.e. local.

.

On the other hand, in the United Kingdom, despite having fewer people infected than in Spain today, there are already clearly warn The population should be made aware that community infections are an imminent reality and that the population needs to be aware of this in order to be better prepared.

.

Even in the American universities clearly warns that if students take advantage of spring break (similar to Easter holidays in Spain) to leave the country or visit areas with a high incidence of the virus, they will have problems to be readmitted back, unless they stay in the country for the rest of the year. two-week quarantine in a suitable location before returning to their rooms on campus. Just like here...

.

The situation is very serious, because unless a medication emerges within a few days that drastically reduces mortality and is feasible for mass administration, what is happening in Italy will only be the tip of the iceberg in the rest of Europe. And neither the health services (already overstretched in Italy) nor the logistics of essential supplies will be able to cope with a massive contagion. That is why it is vital to take courageous measures of blockade and isolation as China has done, even if it means a short-term economic collapse. However, the first decision the EU took was to take the option of closing intra-European borders off the table, thus paving the way for the free movement of Europeans and Covid-19 from Lisbon to Berlin. Yes, those same intra-European borders they did not hesitate to close instead, unilaterally suspending the agreement on Schengen, The refugees were arriving by the millions in the heart of Germany.

.

The paradox that China will now face is that it will have to continue to close its borders (to people, not goods) to prevent, once its domestic epidemic is under control, the virus from infecting them again, now coming from countries like the Europeans where the infection will be out of control due to late and cowardly political decisions. This is why we will see the recovery of the courageous Asian giant sooner than that of the old and cowardly Europe, which represents an extraordinary investment opportunity, as we have already advanced in “Realistic coronavirus figures and the opportunities of an unfortunate crisis“. China begins its path back to business. And it does so having acquired a priceless technological know-how to handle the next health crises, as we can read in this WeekInChina article.

.

In short, the handling of information and alerts to the public say a lot about each country. And unfortunately in Spain we have authorities who are more concerned with bread for today than with deaths and hunger for tomorrow. They focus the State's communication efforts on keeping the population in the dark, who consequently live without any foresight in the face of a health emergency, i.e. without stockpiling food and medicines or any family or personal contingency plan whatsoever. Even the Director of the Alerts and Emergencies Coordination Centre, Fernando Simon, has gone so far as to say that wearing a mask in the street is counterproductive because people would laugh at us or think we are infected, insisting over and over again that masks do not protect us from infection in any way.. And then admitting with a small mouth that if the population buys masks, health professionals will not have enough, showing that they are an efficient and necessary element of protection. Let us remember that in countries such as China they are compulsory masks for the entire population in risk areas and punish those who go out on the streets without them. Other governments, such as the French or German directly confiscate or prohibit the export of facemasks so that their health professionals can have them, without treating their citizens as imbeciles by telling them that they are no protection against infection and that they will make fools of themselves if they put one on.

.

It is true that some young and healthy readers may dismiss this article as being tremendist, but they should bear in mind that although they would overcome the infection with hardly any symptoms, they would probably fatally infect other less healthy and younger people in their family and professional environment, or simply strangers with whom they share, for example, a simple public transport. In the end, it is better to continue informing ourselves in international media and preparing ourselves for the worst, while we cross our fingers that we will soon have a medication available to everyone that will reduce the real mortality rate to the levels of a simple flu.

So much for what we wrote a year ago. Tremendous, isn't it?

Value Parters (VP) is a Hong Kong-based fund manager that we have known very well for many years. We have visited them personally on several occasions and have been investing in some of their funds for years. VP is the only Chinese fund manager listed on the Board of the Hong Kong Stock Exchange. We will now translate and comment on the reflections of its Co-Chairman, Louis So, The report on the economic effects of the pandemic in China a few months ago.

.

It would not be an exaggeration to say that the onset of the COVID-19 pandemic has led to the worst global economic crisis since the Great Depression of the 1930s. The combination of a demand shock, a supply-side shock, a financial shock and political upheaval has sent markets around the world reeling.

.

While no one can predict how the world's economies will emerge from the crisis, some experts are making educated guesses based on current economic data. Whatever happens, a post-COVID-19 environment is going to be very different from anything in the past. China will certainly outperform other markets, although it may not sufficiently boost the growth of the global economy.

,

Therefore, there will be a higher degree of government intervention, more money printing, very low interest rates and a much bigger asset bubble. This asset bubble will in turn widen the gap between rich and poor, and this will lead to social instability.

.

At some point, this system will collapse. In the future, politically speaking, left-wing politicians will gain popularity and gain support. Then we think that some redistribution of wealth will occur.

,

While the last 50-70 years have seen a period of global wealth accumulation, there were also periods when wealth was distributed. Such events occurred because of wars, or because governments allocated resources differently. That is something we can expect to happen in the world over the next five to ten years.

,

On the consumer side, there will be a contactless economy, consisting of a boom in e-commerce and online entertainment. VP has positioned its portfolios to benefit from this trend.

,

Companies will have to rethink their business models. In the past, just-in-time inventory management was the norm. But now companies will have to think about whether they need to build up cash reserves for inventory and supply chain management. That will also change the mindset of business leaders.

,

COVID-19 could escalate a potential crisis of capitalism and the free market. The challenges may cause capitalism to falter. Providing a much better social welfare system could be a potential solution. Although it may affect the economic growth of countries, it will create a much happier environment for society.

,

This pandemic has not changed VP's strategy much. The company is still tapping into what could eventually be the world's largest market: China. Savings are high in this country. We need to participate in this market as investors if we want good returns.

,

The relationship between China and the US will get worse before it gets better. China is not dependent on exports and does not rely on other countries to grow its economy as it used to. This will drive China into isolation for a while. But China and the United States will have no choice but to become friends, partners and allies again. Perhaps the Trump-Biden swap will bring this about.

,

China will come out ahead. And it will emerge from the pandemic ahead of other markets.. The predictions are based on recent economic data from China showing a V-shaped recovery trend at both the macro and consumer levels. It is highly likely that China will take advantage of the pandemic to accelerate its growth spurt and economic leadership of the world.

,

With data available just after the March crash, year-on-year figures showed that fixed asset investment fell 9.4 per cent in March, but increased to a 3.9 per cent positive gain in May. Retail sales were down 15.8 per cent in March, but only down 2.8 per cent in May.

,

Even a business like electricity production showed a year-on-year decline of 4.6 per cent for the month of March, but returned to 4.3 per cent growth in May. The same pattern can be seen on the consumer side. Products such as cosmetics, furniture, automobiles, tobacco and alcohol experienced a similar V-shaped recovery.

.

The data show an economy that is steadily recovering from the pandemic. So there is every reason to be optimistic. China is in a much better position to cope with this crisis than the West, and the FIFO rule is being met because of good virus control. China is benefiting from a large middle class that has one of the highest savings rates in the world. The country had a savings rate of 47% in 2017 and ranked third out of 170 countries monitored by the World Bank.

.

So China is now a fairly self-sufficient economy, and this has helped it to cope with the pandemic. China has innovation, production, distribution and also the end consumer within its borders. Therefore, the country is experiencing less supply-side trauma than other countries.

.

China also has a much more modest stimulus programme than other countries. While the US is pumping out a huge stimulus programme consisting of about 18 per cent of its GDP and rising, China's stimulus package is less than 5 per cent of its GDP.

.

We are quite optimistic about China. It is still on track to become the world's largest economy by 2030 or sooner. Therefore, several investment themes will be the main drivers of growth, including consumer upgrades, a growing number of high-net-worth individuals, technology and the explosion of 5G. There will also be more individuals seeking higher education, along with the development of online service platforms and a growing healthcare sector.

.

China is too big to ignore at the moment. It accounts for 16 per cent of global GDP, which means we can look at it as an asset class in its own right.

.

So do not expect China to slow down any time soon.. There are many factors to consider, such as the relationship between China and the US, and a possible resurgence of the virus. Only time will tell. But things looked much better in the second half of 2020 and so far also look much better for 2021 than in the other economic powers.

We have been saying it backwards and forwards, China is already the centre of the world and its leadership will dangerously relegate investors who remain focused on the West and fearful of the badly named emerging markets (since many are already emerging and most of the West has not yet realised it). Check if not the pre- and post-pandemic economic growth data and projections.

.

This time it is a scientific rather than an economic publication that alerts us to China's hegemony. Below we translate, summarise and comment on the magazine's article. Science by Jon Cohen, which analyses China's progress in the field of vaccination against Covid19 and the dreaded SARS-CoV-2 coronavirus. And above all, it highlights the bio-economic influence that China is achieving across the globe, as always in a stealthy, intelligent and unstoppable manner:

.

The first people in the world to receive the COVID-19 vaccine were not part of a clinical trial. No television networks or newspapers covered the historic event. No company issued a statement.

.

On 29 February 2020, less than 2 months after the world awoke to the threat of the new disease, virologist Chen Wei, a major general in the Chinese army, and six military scientists on her team squared themselves in front of a Chinese Communist Party flag and received injections of an experimental COVID-19 vaccine. Chen, a national hero for her work on Ebola vaccines, had come to the pandemic's ground zero, Wuhan, with her group from the Academy of Military Medical Sciences, in part to help create the candidate vaccine with a commercial company, CanSino Biologics. Commentators inside and outside China later questioned whether the event, which was widely reported on social media, was real. No less than the People's Daily, the Communist Party's main newspaper, labelled a photo of Chen receiving the vaccine as «#FAKENEWS». But Hou Li-Hua, a researcher at the academy working on the vaccine project, says it was «real news», an attempt to protect the hard-hit city's scientists.

.

In the US, the Trump administration's $10.8 billion Operation Warp Speed has accelerated vaccine research and development specifically for the US population, and is doing so faster than many researchers thought possible. But an equally massive effort is underway in China. CanSino and two other Chinese companies - one government-owned and the other working closely with its regulatory agency - are investing substantial resources, testing four candidates in tens of thousands of volunteers worldwide, and are likely to be just days or weeks away from announcing efficacy results from the trials, on the heels of encouraging results announced over the past month by Pfizer and BioNTech, Moderna, AstraZeneca and Oxford University, and Russia's Gamaleya Research Institute of Epidemiology and Microbiology.

.

But the low profile of those historic first injections, the military's collaboration with a «private» company and the ethically fraught decision to begin vaccinations outside of a clinical trial telegraphed that, apart from similar scale and speed, China's vaccine effort is following a very different course from that of the United States and Europe. Most major Western vaccines are based on attractive modern technologies such as genetically modified viral vectors, designer proteins and RNA fragments. By contrast, three of China's four leading vaccine candidates use a classic, tried and tested method: inactivated whole virus. An approach that dates back to the first successful influenza vaccine in the 1930s. And China's vaccine effort is weighed down by its radical success with aggressive public health measures to stop the spread of the SARS-CoV-2 coronavirus, as its measures have left China with virtually no virus on which to test vaccines, including forced isolation of cases and testing of entire cities. By contrast, the raging pandemic in the US has allowed trials there to quickly show signs of efficacy. «China crushed the coronavirus epidemic early, so they missed the opportunity to test the efficacy of their vaccines there,» says epidemiologist Ray Yip, who closely follows the development of the COVID-19 vaccine as an advisor to Bill Gates. «If they had had a lot of cases in China, they could have finished an efficacy trial earlier than other countries.

.

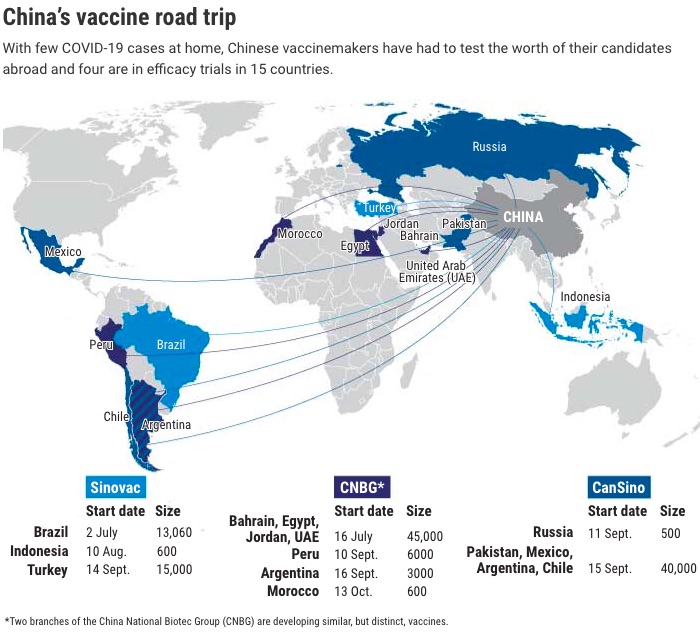

So China's vaccine developers have gone abroad. Although the US has excluded them from Operation Warp Speed, they have negotiated with 15 other countries on five continents. They have mounted massive trials in the Arab world - and given candidate vaccines to senior government officials there, and also conveniently cajoled the radical Bolsonaro in Brazil, where the pandemic is raging, to test a vaccine and explore its production there.

.

But China is not just looking for promising sites for clinical trials. It does not urgently need vaccines at home to combat a virus it has largely crushed, but is playing a global game by pledging to send any proven vaccines to countries that are conducting trials for its candidates, or to share the technologies behind them. «They know they don't need a vaccine to contain the epidemic in China,» says Yip. «They can take their time,» and take a much longer and more long-term view. strategic.

HUBEI, CHINA - APRIL 15: 220 volunteers from Wuhan are vaccinated during the phase II trial on 15 April 2020.

As seen in the photo above, Chinese company CanSino Biologics created the first COVID-19 vaccine to enter clinical trials, and by April it had advanced to a phase II study in Wuhan.

.

Yanzhong Huang, a global health specialist at both Seton Hall University and the Council on Foreign Relations, says the country is «actually using the vaccine to promote the diplomacy of foreign policy objectives». This «vaccine diplomacy», he says, contrasts sharply with Warp Speed's «vaccine nationalism» and aims to «fill the vacuum left by the US».

,

«It's a very carefully executed and thought-out strategy,» says Stephen Morrison, who directs the Center for Global Health Policy at the Center for Strategic and International Studies. «A strategic goal of the Chinese government is to achieve hegemonic influence in the next 10 years..»

.

At home, too, attitudes toward vaccines contrast with those in the United States and Europe, where distrust is high, Morrison says. To the dismay of vaccine experts abroad, hundreds of thousands of people in China have already lined up to receive experimental vaccines, even before their value and safety have been proven. «There has not been a collapse of faith and trust in science and the state,» says Morrison. «There is less fear about where this is all going.» Paradoxically, it is the Westerners, the die-hard freedom advocates who question isolation measures, restrictions on movement and the reliability of testing, who have lost the most freedom as a result of their radical confinements and perimeter closures.

.

In China, the speed with which Chen and his colleagues were able to get those first vaccines is all the more remarkable given that CanSino was arguably slow.

.

Although some COVID-19 vaccinators launched their projects the day after the SARS-CoV-2 sequence was made public on 10 January, CanSino CEO Yu Xuefeng had reservations. «We started looking into it in mid-January, but there was a hesitation,» he says. COVID-19, Yu was concerned, might be a bluff, The disease, such as severe acute respiratory syndrome (SARS), another disease caused by a coronavirus, alarmed the world in 2003 but disappeared a year later, after companies and governments had devoted many resources to developing vaccines.

.

Yu, who is originally from China, completed his PhD in microbiology at McGill University in Canada in 1997, and then stayed on, working on vaccines for almost 9 years at a Sanofi Pasteur branch there. He co-founded Canino in 2009. A team led by Chen in China helped develop his only previous product to receive approval: an Ebola vaccine based on a widespread and largely harmless virus known as adenovirus 5 (Ad5), into which they added a gene for the surface protein of the Ebola virus.

.

Yu and his team considered making an anti-COVID-19 vaccine with messenger RNA (mRNA) for the coronavirus« novel surface protein, called spike, the innovative approach taken by Pfizer and its partner BioNTech, the »winner« of the race to report preliminary efficacy data. But CanSino decided to go with what it knew, using the Ad5 vector to carry the spike gene. »I thought it was the fastest and most mature way to develop a new vaccine," says Yu.

.

Within a month, CanSino's candidate was ready for delivery to Chen and his team, and on 16 March the company launched the world's first COVID-19 vaccine trial in Wuhan to test its safety and ability to elicit immune responses. CanSino had beaten Moderna by eight hours, though a world paralysed by the vaccine race among Western companies paid little attention.

.

Several US and European contenders, including AstraZeneca, have also adopted adenoviruses to carry the target protein, with some opting for an Ad5 vector similar to CanSino's, despite several concerns about the approach. In 2007, two disastrous efficacy trials of an Ad5-based AIDS vaccine found that, for reasons still unclear, it actually increased the risk of HIV infection. The other concern is that pre-existing immunity to Ad5 may attack the vaccine vector, which may explain why, in early trials, the CanSino vaccine elicited a weaker-than-expected antibody response. «We see that there is some impact,» Yu acknowledges, «but it's not black and white.» (Preliminary efficacy data for the AstraZeneca/Oxford vaccine suggest that immunity against its adenovirus vector may have compromised that candidate's performance as well, at least in double-full-load dosing.).

The other two Chinese players, Sinovac Biotech and China National Biotec Group (CNBG) - a subsidiary of one of the world's largest vaccine manufacturers, state-owned Sinopharm - are taking a different approach: vaccinating people with the whole, «killed» virus. This does not require sophisticated protein or RNA design or genetic engineering: Scientists simply inactivate the virus with a chemical (beta propiolactone) and mix it with an adjuvant that effectively puts the immune system on full alert. In theory, these vaccines can produce broader antibody and T-cell responses, because they contain the full set of viral proteins, rather than just one. And unlike mRNA vaccines, which have to be stored at sub-zero temperatures, inactivated viruses require no more than the ordinary refrigeration of any household fridge.

.

But many scientists see inactivated virus vaccines as outdated, difficult to manufacture in large quantities and potentially dangerous. Warp Speed rejected the approach outright. «I don't think the inactivated vaccine is a good idea,» says Moncef Slaoui, chief scientist at Warp Speed.

.

A major concern is that inactivated SARS-CoV-2 vaccines could trigger a more severe disease, known as «enhanced respiratory disease», in immunised people who do become infected. Basically, if a vaccine triggers ineffective antibodies, they can form immune complexes that clog the lungs. This happened with a respiratory syncytial virus vaccine given to children in the 1960s, and in animal experiments with vaccines against SARS and another coronavirus disease, Middle East respiratory syndrome. The prospect of growing large batches of virus before killing them also poses problems; twice in the last five years, live poliovirus has escaped from European plants making inactivated poliovirus vaccines. Yes, yes, what some conspiracy theorists claim happened in the «mysterious» virology lab in Wuhan has happened before in Europe itself, without the western media or any crazy president pointing an accusing finger at us.

.

But inactivated SARS-CoV-2 vaccines, unlike mRNA and other technologies widely supported by Operation Warp Speed, have a strong track record. «There are many different ways to make vaccines, and it's great that innovation is happening alongside proven approaches,» says Nicole Lurie, strategic advisor to the Coalition for Epidemic Preparedness Innovation (CEPI), who previously served as US assistant secretary for preparedness and response. «Inactivated vaccines are one of several proven approaches.» Meng Weining, senior director of Sinovac, says they compared the inactivated approach - which they already use to make six vaccines - with two other strategies in animal models. «The inactivated whole virus vaccine gave a much, much better result,» says Meng.

.

Although it is theoretically easier to produce mRNA in large quantities than to grow the virus on a similar scale, vaccine experts say the production of inactivated virus vaccines is unlikely to be an obstacle. CNBG, for example, has «enormous resources»: 10,000 employees and scientists, huge manufacturing capacity,» says Nicholas Jackson, who heads CEPI's China office and formerly worked in vaccine R&D at Pfizer. «They are a very competent beast.» And, crucially for Chinese vaccine diplomacy, many other countries have manufacturers that have been producing inactivated virus vaccines for decades.

.

If China's COVID-19 vaccines work, manufacturers say they could produce 1.5 billion doses in total next year. And countries that cannot access Warp Speed-funded vaccines, especially those that have hosted Chinese efficacy trials, could have a more assured vaccine supply.

.

Sheikh Mohammed Bin Rashid Al Maktoum, prime minister of the United Arab Emirates (UAE), on 3 November tweeted a photo of himself in Dubai with the right sleeve of his kandura rolled up high, being injected with a CNBG COVID-19 vaccine. «We wish everyone safety and great health, and we are proud of our teams who have worked tirelessly to make the vaccine available in the UAE,» Al Maktoum wrote. Two of the country's top ministers had received the vaccine three weeks earlier.

Pictured above is Mohammed bin Rashid Al Maktoum (left), Prime Minister of the United Arab Emirates, shortly after receiving a COVID-19 vaccine from CanSino Biologics on 3 November under his country's emergency use authorisation.

.

The UAE has become the cornerstone of the NBSC efficacy trials and is following China's controversial lead in allowing people to receive the vaccine outside of clinical trials.

.

At a 23 June videoconference linking Abu Dhabi, Beijing and Wuhan, health officials, ambassadors and CNBG executives sat at long tables in rooms decorated with the flags of each country and celebrated their decision to conduct a trial together to assess efficacy. The trial has since expanded to Bahrain, Egypt and Jordan and is expected to recruit 45,000 people. CNBG says it came to the UAE to test its two whole-virus vaccines - similar inactivated preparations made by two independent, and even competing, laboratories, one in Wuhan and the other in Beijing - because the high rate of SARS-CoV-2 infection there should hasten a sign of efficacy. But diplomacy and trade also drove the decision. The UAE's huge foreign workforce means that trial participants come from 125 different countries. «If you can prove that these vaccines work in the UAE,» says Huang, «that means everyone would think the vaccine would work in their countries too.».

.

China may be hoping for a public relations (PR) benefit as well: The United Arab Emirates and many of the other partner countries have large Muslim populations, which Huang says could help mitigate human rights complaints about China's treatment of Uighur Muslims in Xinjiang province. «They certainly don't want to have more enemies abroad,» he says.

.

Huang adds that through its series of overseas trials, China hopes to create goodwill for its Silk Belt and Road Initiative (BRI), massive infrastructure investment in more than 100 countries to increase trade. Critics have accused the BRI of being «debt trap» diplomacy that is a form of neo-colonialism. «China wants to work with these countries and prioritise them to have the vaccine because I think this will facilitate the implementation of the BRI,» he says.

.

China's vaccine diplomacy has not always worked well. On 9 November, after Brazil suspended a Sinovac vaccine trial following the death of a participant, President Jair Bolsonaro took to Facebook. «Death, disability, anomalia,» he wrote, quoting a Brazilian health agency that had listed the possible reasons for the suspension: death, disability, genetic anomalies. Bolsonaro's message was clear: This Chinese vaccine, called CoronaVac, was dangerous.

.

«A lot of people were very surprised by that post,» says Esper Kallas, who runs the vaccine trial centre at the University of São Paulo that the participant had joined. «He was celebrating the failure of a vaccine.» For Bolsonaro, it was a public relations victory over his political archenemy, the governor of São Paulo, who supported the CoronaVac trial. The president was also reveling in a setback for China, which Bolsonaro, like his ally, US President Donald Trump, has relentlessly criticised.

.

It turned out that the participant died of a drug overdose. His death had nothing to do with the CoronaVac, and the trial was quickly resumed.

.

China chose to navigate Brazil's daunting politics because with an out-of-control pandemic - it is third in the world in total infections, with more than 100,000 new cases every week - the country is a magnet for vaccine trials and is desperate for vaccines. The state of São Paulo in September committed $90 million to Sinovac for 46 million doses (this is 10 times cheaper than what the US government is paying for mRNA vaccines from Pfizer/BioNTech and Moderna). And Brazil could increase supply by manufacturing the vaccine on site under licence. Sinovac says it could transfer its technology to Instituto Butantan, a major vaccine manufacturer in Sao Paulo, a collaboration Meng describes as «win-win».

.

China has had warmer receptions in other countries. In September, Turkey launched a 13,000-person efficacy trial of Sinovac's vaccine. Serhat Ünal, who heads Hacettepe University's Vaccine Institute - which is similar to Butantan's in Brazil - and sits on the health ministry's scientific board, says Turkey has «a good infrastructure for phase III studies» and, unlike the US and much of Europe, hosted a Chinese vaccine manufacturer.

.

The three Chinese manufacturers also have large efficacy trials planned or underway in Indonesia, Pakistan, Saudi Arabia, Mexico and Chile (see map above). It's a good strategy, says Ünal. «When you do phase III in different countries, it's more transparent, it's more reliable,» he says.

.

As much as vaccine diplomacy influences the deals Chinese vaccine manufacturers make for efficacy trials, they are also driven by capitalism, says Yip, who for four years headed the China office of the US Centers for Disease Control and Prevention (CDC). «Everyone is clamouring for a COVID vaccine,» he says. «Everyone wants to tell their people that we've got some vaccine for you.» Y Chinese companies will make profits when supplying it.

.

It is a safe bet that one or more of China's overseas trials will announce efficacy data any day now. Results so far from other vaccines have fuelled a growing sense that many vaccines will crush, what is, from a vaccine's point of view, a somewhat weak virus. But China is not waiting for phase III results before using vaccines widely at home. Its regulators appear to be satisfied with the animal studies combined with minimal safety and immune response data from phase I and II trials. In June, CanSino received an emergency use authorisation to vaccinate the military, and since then both Sinovac and CNBG have been given the green light to vaccinate large populations outside of clinical trials. Unconfessable but presumably very significant numbers.

A refrigerated container with a batch of 120,000 doses of Sinovac's Chinese COVID-19 vaccine arrived at São Paulo international airport on 19 November. The vaccine will be used if ongoing efficacy trials show it to be safe and effective.

.

With the pandemic defeated at home, China is vaccinating its people as insurance, often against a dangerously infected world.. CanSino's Yu says «thousands» of troops on peacekeeping missions have received his company's vaccine before travelling to places with a high burden of COVID-19. CNBG says «hundreds of thousands» of people in China have received their vaccines. «By doing this, we are able to build an immunological barrier among specific groups of people such as health care workers, pandemic prevention personnel and border inspection personnel,» the company explained in its written responses to Science. Vaccination is «completely voluntary with informed consent,» CNBG stresses. Moreover, «We did not receive a single case report of a severe adverse reaction, and no infections were reported for vaccinees working in high-risk areas».

.

Sinovac's Meng says that «more than 90%» of the company's employees have received their vaccination because they are considered a high-risk group; he received it because he travels abroad. (According to China's Ministry of Culture and Tourism, 155 million Chinese travelled abroad in 2019, including thousands of students university students who are continuing their education in the best American universities). In October, the company began selling its vaccine -$60 for two doses - in Yiwu, a city in Zhejiang province. And Yip says the government was even considering vaccinating all of Beijing after an outbreak of COVID-19 there in June. Yip says officials «had already written the guidelines»; if more than 500 cases had come to light, «they would inject everyone in Beijing with the vaccine». In the end, contact tracing, testing and isolation of infected people limited the outbreak to 335 cases.

.

In the end, contact tracing, testing and isolation of infected persons limited the outbreak to 335 cases.

.

Morrison says that the Chinese government has «clearly decided at the highest level» that it is worth betting on creating «facts on the ground»and gain a global commercialisation advantage by having the first COVID-19 vaccines in wide use. «It's a risk but it's also potentially a big win,» he says.

.

But what happens if damage is done? «You shouldn't apply peacetime rules during war. Our lives are turned upside down,» says Yip, who lives part-time in Beijing.

.

If its range of vaccines is successful, China's image will gain a boost both at home and abroad. «They have reputational problems, internally and externally,» says Morrison.

.

In May, China's President Xi Jinping told the World Health Assembly, which governs the World Health Organisation (WHO), that the country would make its COVID-19 vaccines «a global public good», a somewhat vague statement that left many China watchers scratching their heads. However, China fulfilled this commitment in October by joining the COVID-19 Global Vaccine Access Service (COVAX)., The WHO and UNECE are leading an effort in part to ensure that any product that is proven safe and effective reaches rich and poor countries alike quickly.

.

This is primarily a diplomatic move. COVAX has not received support from the US or Russia, and China sees that it «could have a controlling influence over an important international mechanism». Moreover, says Alexandra Phelan, a lawyer at Georgetown University's Center for Global Health Science and Security who specialises in China, «It is a good act of a global citizen to support this effort».

.

If a vaccine made in China proves safe and effective, it could help people forget the pandemic that started there and how poorly the government responded at first, says Morrison. And at home, it could absolutely clean up the image of China's vaccine manufacturers. Chinese citizens have recovered from a series of scandals over the past decade that include the use of ineffective vaccines against diphtheria, pertussis and tetanus; inadequate registrations of a rabies vaccine; and sales of an expired polio vaccine.

.

A successful Chinese-made COVID-19 vaccine that has been vetted by external regulators would reassure the domestic market, says Phelan. «There is a lot of domestic ground to make up.».

.

In Brazil, Kallas says a similar dilemma could arise if Butantan, as expected, starts manufacturing Sinovac's CoronaVac. «There is a saying here that the neighbour's chicken is always the tastiest,» says Kallas. «We have a perception that everything we make is not as good as the imported stuff.»

.

But for now, Brazil is embracing the Chinese vaccine. With cases on the rise, the arrival of just 120,000 doses of CoronaVac on 19 November became big news. The bias against China is little more than a far-right political «contamination», says Kallas, and most Brazilians see CoronaVac as «a viable option».

.

In short, China is managing its vaccine supply trials around the world intelligently and strategically, with no epidemiological fires to put out within its borders. As always, the Chinese are the smartest in the class. And to their economic clout they are now adding biological and diplomatic clout. Soon no country in the world will be able to afford to be China's enemy. And its businesses of all kinds are there, freely quoted and available to any investor.

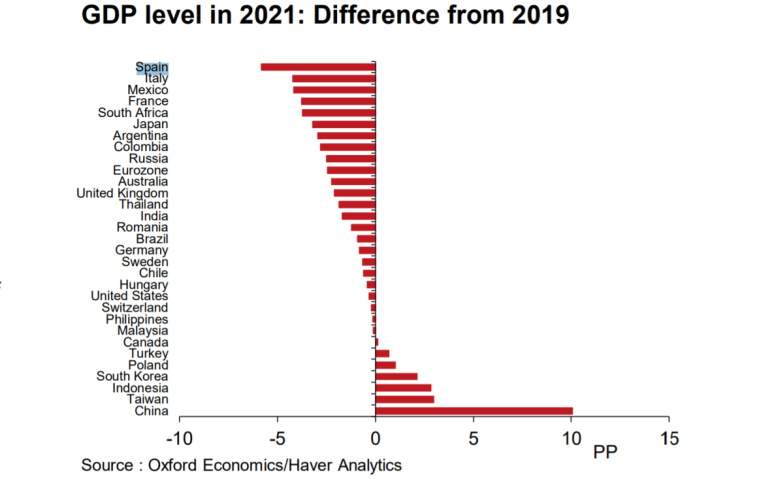

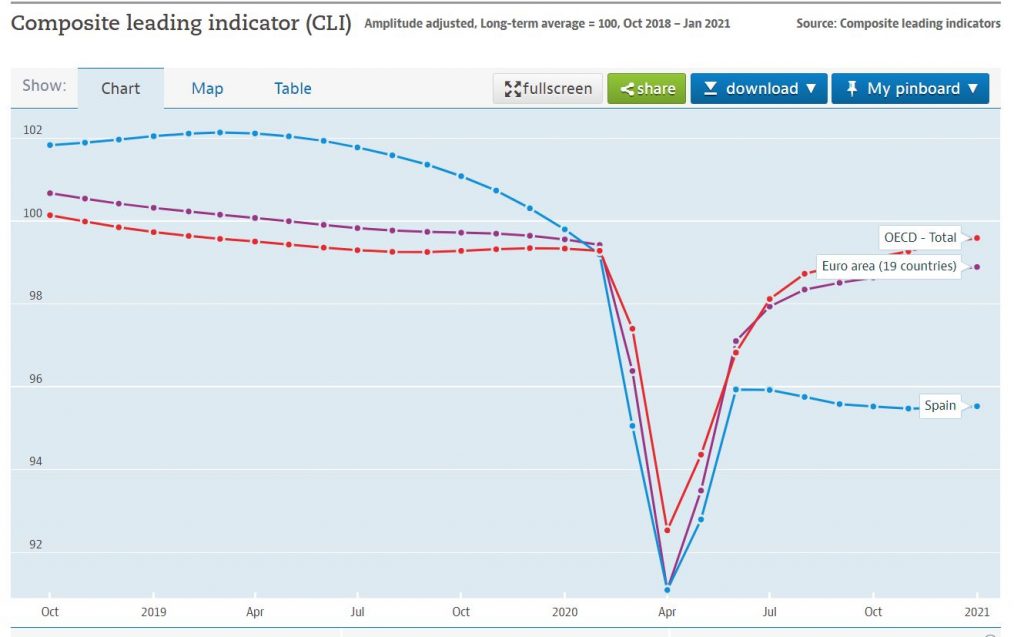

The latest data published by Funcas The forecasts for the fall in GDP in Spain are devastating. Moreover, although the adjustment of the forecast in the rest of Europe has been slightly upward, meaning that the final fall will probably be somewhat less than the expected hit at the start of the pandemic, the economic disaster throughout Europe is bleeding. Worse still, the scarcity of production, ageing demographics, rising social spending, over-indebtedness of states and extractive taxation stretched beyond its limits make the Old Continent's economic recovery a desert that many Europeans are facing with hardly any water. Let's see the magnitude of the tragedy in the following graphs by ElEconomista:

Nor does the US economy have much brighter prospects, despite the fact that its economic growth and taxation is enviable from a European point of view. Nevertheless, its business and innovative fabric is already allowing for a slow but much more feasible recovery than in Europe and the burden that we Latin and Greek Europeans are carrying.

The global economic centre, which has been shifting inexorably towards Asia for more than a decade now, is therefore being further boosted by the pandemic. This health crisis, which is crushing Western economic expectations as no other debacle has ever done, is creating an even more serious threat to the global economy. tremendous and silent acceleration of the process of relocation of the economic and financial centre towards China and its area of influence.. In this area of influence we must include such powerful economies as India, Australia, Japan, Korea and Russia itself, as well as, of course, the more orbital ones such as Vietnam, Thailand, Myanmar, Taiwan, the Philippines, Indonesia and Malaysia, to name just the largest.

It is true that some Asian economies are also suffering relatively large GDP declines during the pandemic. But the fact that they are orbiting a gigantic locomotive like China, whose growth forecast despite the pandemic is not only positive but overwhelming, means that their medium- and long-term prospects are radically different from the desert that awaits us Westerners in general and Europeans in particular, not to mention Spain's dramatic outlook, of course.

As can be seen in the graph above, the winners in this pandemic are as clear and distant as the losers. In view of what lies ahead, we would do well to follow the compass of economic growth for our investments in the coming years. In other words, the outlook for our investments in Spain is one of insomnia, since you can already imagine the fiscal reaction that our government will perpetrate in the face of such a debacle... In other words, a confiscatory taxation never seen before (with great evils great «remedies»...), in which any solution imaginative will also be blessed by the northern countries of the EU, since every euro confiscated from ordinary Spaniards will be one euro less that the Germans and the Dutch will have to finance/give us. Therefore, legal insecurity in Spain is going to be record-breaking in the times to come, and we would do well to replacing Spanish bank accounts and isins with Luxembourgish ones. No one in the EU will watch over our legal certainty in the face of confiscatory governments of one colour or another. No one.

We must therefore avoid investments in countries where the pandemic's scourge will result in an economic axe with very little capacity for recovery. Therefore, investments in countries such as Spain will have - and are already having - devastating prospects, or at least with very high opportunity costs compared to other investments in China or other countries with infinitely better conditions. And we are not only referring to the fact that investments in the Spanish stock market are going to be a disaster, but also to domestic real estate investments, whose demand for rents or buyers will be greatly reduced by the general impoverishment of the population and the business fabric. And we all know what happens when demand falls below supply, don't we? Well, to this we will have to add even more extractive taxation for property owners, since we are facing a State that is agonisingly tax-collecting due to the fall in GDP. A fall that goes straight into the vein of the public deficit, cuts and the more than likely desperate confiscation of everything that moves and does not move, that is, movable and immovable assets.

Therefore, in the coming years we will see stock markets with the wind at the back and stock markets with the wind at the front. And these headwinds and tailwinds are of course also applicable to real estate investments. But since buying real estate in distant and unfamiliar markets is foolhardy without a local team to look after your interests, ordinary investors should focus on equity investments in listed companies in countries with the best economic, demographic, production and financial prospects. And this obviously brings us to certain Asian markets as a priority, such as Mark Mobius already predicted a year and a half ago. Let us not forget that there are companies in the world that own an infinite number of properties that form part of their fixed assets, and therefore when we buy their shares we are also buying them. bricks.

The question is where to find good Asian funds, managed by strong local teams, that far outperform their respective benchmarks, and of course also the funds owned by multinational managers, who invest «by hearsay» in Asia from their Western offices in London or New York. For there are already excellent Luxembourg-domiciled funds (125,000) that overweight the fastest-growing Asian markets and are therefore accessible from just 125,000 euros. give access to a portfolio of top-tier funds for professional investors and hedge funds in Asia..

It is true that most advisors and other analysts continue with the old-fashioned approach of promoting Western investments as virtually the only investable universe, regarding all other options as obscure and risky «emerging markets». Nothing could be further from the truth, since the real risk lies in the European «declining markets» and not in the Asian emerging markets, most of which are already rather emerging and form the present and future economic and financial centre, with or without Wall Street's permission.

At this point in the pandemic and with the markets having recovered so rapidly since the lows of 23 March, we would like to offer some thoughts for investors from the latest report from Oaktree Capital. Let us start by listing some of the obvious reasons why investors should not be so optimistic about market prices. For example, the risk of virulent resurgence posed by the fact that economic activity has resumed in most Western countries. It is true that not having resumed economic activity would generate more economic and social crisis, but the health crisis that may be generated by strong resurgences could certainly be a drag on the share prices of many companies.

.

Another reason for pessimism is that the slow recovery of consumption and social interaction habits, so necessary for free economic exchange, may extinguish many businesses and enterprises that simply will not make it alive to the full reopening of economies when it occurs.

.

Some scientists also warn that a fully effective and safe vaccine may not be available until well into 2021, which would slow down the return to economic normality more than expected.

.

Other economists warn of the large number of private corporate bankruptcies and the irreparable damage that can be done to public accounts by the policy of almost infinite monetary risk to avoid collapse. Not to mention the uncertain changes in business models in sectors such as travel, retail sales, offices or any activity that has traditionally been carried out by concentrating many people in closed environments or high population density.

.

For all these reasons and many more, there is no shortage of reasons for those who prefer to keep their money where it is and see the glass of this pandemic as half empty, even though prices are already near record highs. Perhaps some of them got out of the market in the middle of the fall and are still losing money in 2020. But as we said recently, whoever is still in the negative today could have done better.. So let us look at some of the reasons why it is very dangerous, or at least unprofitable, to underestimate the power of the tailwind of coordinated monetary policies of all the world's central banks.

.

Most investors believe that, although we will not see a radical recovery in the economy, the decisions of the central banks are going in the right direction. And that they will be determinant in that recovery which, although with uncertain ups and downs, will come in the medium term. Confidence in central banks is a self-fulfilling prophecy.

There is growing optimism about advances in potential vaccines that are already in production around the globe. And there have been promising near-term advances in a variety of treatments. All of this contributes to the sense that the worst is over and that there is much good immunological and pharmacological news imminent.

After such sharp falls in economic figures (unemployment, GDP, international trade, wages, etc.), the recovery of these figures will also be spectacular in Asia and the US (not so much in Southern Europe or Latam, of course), which, quarter after quarter, will contribute to investor optimism.

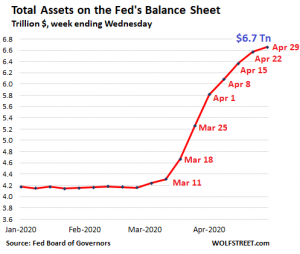

The US Fed and Treasury have acted swiftly and forcefully, but not the ECB, which is much more politically bound. This is why confidence is recovering more in the US than in Old Europe. Fed Chairman Jay Powell proclaimed from the outset that they were not going to run out of ammunition, which has clearly had an effect.

The Fed also said on the record that they would continue to buy assets for as long as necessary, regardless of the massive increase in the size of the Fed's balance sheet that this entails.

This purchase of assets means putting a huge amount of money in the hands of debtors. This capital is in turn reinvested by them in various ways, also by buying other assets and thus making them more expensive. This process further compresses the rates and yields to be expected.

Some expected the Fed to discriminate between good and bad debtors to lend to, but that has never been its objective. Central banks are now simply providing liquidity to anyone who needs it, regardless of their respective financial or accounting realities.

Investors, at least in the West, are anticipating a long era of low, very low rates, which leads to a scenario with multiple consequences, all of them favourable to the rise of the markets:

Low rates in turn lower the discount rates that investors use - or should use - and thereby increase the net present values of future cash flows. This is one of the ways in which rate compression generates an increase in stock market valuations.

Low rates also compress the risk-free rate, in turn crushing all yields demanded by investors. This leads to insolvent debt placements at laughable yields, for example. Or high share prices of dubious businesses in exchange for a meagre dividend.

All asset prices are interconnected by these relationships. That is, even if central banks buy asset A and not asset B, asset B will also tend to rise comparatively, since in the face of the expected yield compression of A due to the demand generated with public money, the demand with private money for B will increase, compressing its yield relatively as well. And vice versa, of course. So whether central banks focus their massive purchases on solvent assets (investment grade) or insolvent assets (junk bonds), they will all rise in price comparatively, reducing yields to ridiculous levels.

Such low yields discourage many investors who prefer the volatility of equities in exchange for higher future returns. Again the self-fulfilling prophecy.

Obviously human behaviour also plays a role in this market recovery which is clearly ahead of the economic recovery (isn't that what stock markets used to do, to stay ahead of the economy). More and more investor education generates a certain amount of demand when panics occur, thus reducing the depth and/or durability of crashes. But not all of the demand generated is a product of better financial education, unfortunately. We also see the FOMO (fear of missing out) factor, i.e. watching your neighbours recover their losses in the middle of a pandemic and missing out on the party. On the other hand, ETFs and index funds make sure that no stock is left behind, whether it deserves to recover its price or not.

.

In fact, we have already seen an almost sustained rally since the Fed turned on the tap 12 years ago. And we saw in 2018 what happened to prices as soon as there was a slight hint of shutting down or reducing the flow of water. So for a decade now, many investors have been learning not to row against the central banks' wind but with it.

.

In addition, the popularisation of platforms such as Robinhood in the US has led millions of young people to allocate their savings to an attractive market with a much more respectable patina than sports betting or online casinos. It has democratised investment in the stock market without even having to be a retail investor in any bank. Obviously this carries with it the danger of turning investment into gambling, but in any case those savings, which previously did not end up in the markets, now generate demand and contribute to price increases. Today, immediacy is king, and patience seems an obsolete value for most of the young money entering the stock market. For this investor niche, a pandemic/crash with record volatilities such as those experienced in recent months is the best lure to accelerate the desired process of enrichment -or ruin-.

.

The rise of such young profiles in search of immediate profit, together with indiscriminate infers such as ETFs and index funds, are driving zombie companies and chicharros to infinity and beyond, making fundamental business data relatively irrelevant. Does that mean we should throw our money into the arms of any listed stock? Obviously not. For, while it is true that with any sailboat any investor can seemingly sail with the wind at the back of the central banks' sails, we need to have a good engine to reach a safe harbour when a storm comes or the wind dies down.

And that engine that will save our lives is only provided by the shares of good businesses in growing economies bought at a good price. The rest of the sailboats without engines will fall by the wayside, although as long as the wind is blowing they all think they are sea dogs.

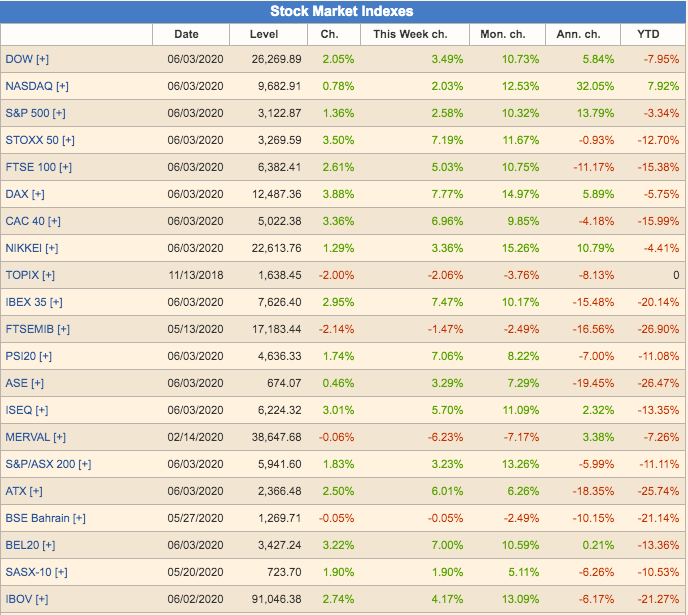

It is true that as of 3 June 2020 the S&P 500 is at -4% from the start of the year, the Dow Jones is at -9%, the German DAX is at -7% and the Hong Kong stock exchange is still at -15% YTD. It is also true that the stock markets of other countries are even further behind, such as those of Brazil, India, Russia, Indonesia or European countries like France, the UK, Italy or Spain. However, there are others which, to the surprise of many, are already at -2% levels, such as Japan or clearly in positive territory, such as Denmark.

.

And not all investment possibilities are limited to matching the general reference indices of the countries, which as you can see on any website like this one, are still quite red in general. We can find some sectoral indices such as the Healthcare, Biotech or the very same Nasdaq with positive returns, despite the travails of this fateful year.

.

But of course, having a portfolio full of international index funds or etfs, replicating only consistently winning sector indices, is almost as difficult as choosing a portfolio of world stocks that outperforms the market year after year.

Another possibility for the investor is to choose good actively managed funds that have managed to outperform their respective benchmarks for many years and are therefore already making money, net of fees, for their investors. The problem is that for the vast majority of retail investors (according to the unfortunate nomenclature used by Spanish regulation), finding funds that achieve substantial alpha and outperform their indices on a consistent and sustained basis over time is often as difficult, if not more so, than getting winning stocks or sector indices right.

.

Here it is worth recalling what we explained in «Why big international investors don't invest in the same funds as you do»The "outperformance" of funds that consistently outperform their benchmark indices. There are some, but investors must have a portfolio size of several million to exceed the minimum requirements of these funds for professional or institutional investors.

.