In the EU more and more alternative investment fund managers are becoming more and more -are governed by the AIFMD (Alternative Investment Fund Managers Directive). The alternative investment nomenclature includes all European investment vehicles that do not meet the requirements to be considered UCITS (Undertakings for Collectible Investment in Transferable Securities). If, in addition to being non-UCITS, their managers comply with the above-mentioned directive, they will be considered AIFMD funds. UCITS funds are those usually sold by Spanish banks to their retail and private banking clients. However, it should not escape anyone's attention that on the other hand alternative investment funds are the funds of choice for major investors worldwide. In other words, although for the vast majority of Spanish retail and private banking investors their investment universe is limited to the 10,000 or so UCITS funds marketed by banks in Spain, for professional investors and the world's wealthiest individuals, alternative investment funds and hedge funds make up the vast majority of their portfolios. In other words, most of the world's best funds in history (some even closed to new investors as they do not accept any more money) are not UCITS and are not marketed in Spain, but alternative management funds, which can be invested in jurisdictions that are much less restrictive than Spain.

.

Let us remember that there are more than 100,000 investment funds in the world. And the million-dollar question is, how can a Spanish retail investor access this universe of 90,000 non-UCITS funds that are not marketed in Spain? The answer is not so simple, as it is not enough to open an account in a bank abroad. There are additional difficulties The most common problems encountered by the ordinary Spanish investor, such as taxation, which is linked to the jurisdiction where the fund is domiciled, are as follows. As we will see below, funds do not necessarily have to be domiciled in the same country as the management company. Most of the world's alternative investment management companies, domiciled in the USA, Asia, etc., have their headquarters in the same country as the fund management company. have local funds for investors in their own country, but they also have replicas of these funds in offshore jurisdictions for large international investors.

.

The reason why fund managers create these mirror funds or feeder funds for international investors in offshore jurisdictions, where taxation for the investor is zero, is not so much so that they do not pay taxes, but so that they are not harmed by the taxation of the country where the fund manager is located in addition to their own taxation. In other words, if they invest directly in local funds, they would be subject to double taxation: That of the country of origin of the fund manager and that of their own country where the investors reside. It is true that in some cases such double taxation could be fully or partially recovered if there is a treaty between the two countries to avoid it, but not in all cases. Moreover, even in those cases where such treaties would be beneficial, it is still an inconvenience that adds to the investor's fiscal discomfort and uncertainty.

.

This is why large international investors often use offshore and non-EU mirror funds, mirror funds or feeder funds domiciled offshore and in non-EU countries. OECD to invest in funds from American, Asian, etc. fund managers. In this way a Spanish investor who invests in a US hedge fund, for example, should not be taxed in both the USA and Spain, but only in Spain, without the need to resort to bilateral treaties to avoid double taxation.. The problem is that Spanish taxation penalises investors resident in Spain who invest in funds domiciled in these offshore countries, where the aforementioned replicas aimed at international investors are usually located (we will explain later how this penalty can be avoided).

.

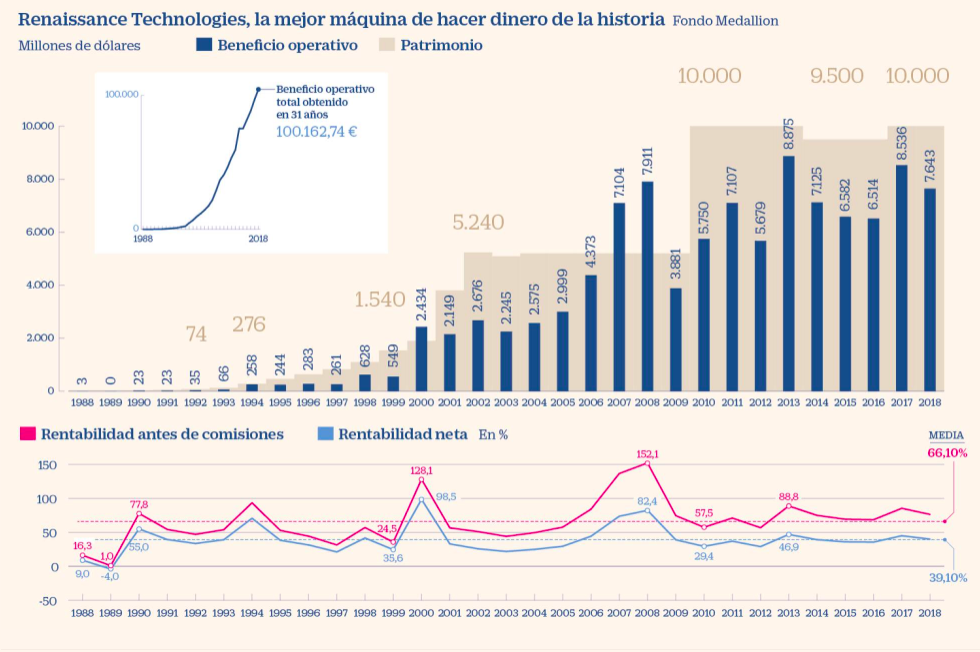

Let us look at an example of a benchmark fund manager with the aforementioned duplicity of funds, aimed at investors according to their country of origin: The manager of the legendary fund Medallion (already closed to new investors since 1993) is the prestigious Renaissance, of which we have already we spoke at length and explained our visit to their bunker in this article. Well, this fund manager, like so many other world leaders in management, has funds for domestic institutional investors (US-investor), domiciled in the USA; and funds domiciled in Bermuda for foreign investors (non-US investors). As we have already said, the distinction is made so that the international investor does not suffer the taxation of the funds domiciled in the USA and so that they only have the effects of the taxation of the respective countries where each investor resides.

.

However, there are also other reasons for fund managers to domicile their funds for large international investors in non-OECD/offshore jurisdictions. In addition to avoiding double taxation for the international investor and saving taxes for the fund manager itself, those jurisdictions do not entail any restrictions in terms of trading platforms or geopolitical vetoes when it comes to underwriting funds. For example, most international investors would find it very difficult to subscribe to funds in countries such as China, Korea, Indonesia, the Philippines, Vietnam, Russia, etc. In some cases because of political/economic sanctions imposed by certain countries, and in others simply because the markets are still technically, politically and/or regulatory unwilling to allow international money into their domestic funds.

The fact is that, whether by hook or by crook, large international investors use these channels created ad hoc for them. And either they are not penalised fiscally by their respective countries if they invest in these jurisdictions, or they have investment vehicles and structures that legally exempt them from these penalties. The loser, as always, is the ordinary Spanish investor, who is condemned to invest in the UCITS environment and the few retail hedge funds domiciled in Spain, in short, condemned to the fish that our banking system sells them.

.

It is true that some American or Asian fund managers, eager to attract retail funds from the European market, set up their own UCITS vehicles in Ireland or Luxembourg and register them for marketing in various EU countries. But unfortunately they are often not the brightest but the most voracious.. And they do not seem to mind giving up much of their alternative know-how and assuming the restrictions on portfolio concentration, liquidity, restriction of hedging and/or restriction of operational freedom in general that the UCITS label entails, in exchange for inflows of money from small European investors. The result is that these UCITS funds are very different from the original ones and with much lower returns.

.

Therefore, we are going to focus on the solutions so that a smaller Spanish investor can access the best American and Asian hedge funds on the planet without suffering, on the one hand, double taxation for investing in their funds aimed at local investors, and on the other hand, the tax penalty for investing in their feeders or offshore mirror funds aimed at international investors. There are two absolutely legal and transparent ways of doing this:

.

- By having a european investment vehicle, within which these funds can be subscribed for foreign investors (we explain this in The advantages of investing from Luxembourg).

- Investing through a AIFMD fund of funds which in turn contains those offshore funds (we explain in Funds that make inaccessible funds accessible).

.

This second option solves in one fell swoop the 3 problems encountered by the ordinary Spanish investor:

.

First of all, the first insurmountable problem for most investors is the minimum investment requirement. And the fact is that The best funds in the world often lack retail classes and require prohibitive minimums of $500,000, $1 million or even $5 or $10 million or euro equivalent. Moreover, without going any further, funds such as those of the aforementioned Renaissance not only require a minimum investment of 5 million, but they also select the institutional investors they like the most, and can be rejected even if they exceed this minimum investment (Cluster Family Office had to pass this filter to be approved as investors in Renaissance, considered the best fund manager in the world for several decades). Well, these AIFMD funds of funds that contain large institutional funds 125,000 minimums are usually as low as 125,000 eur.

.

Secondly, it avoids the tax penalty that offshore investments suffer from, as explained above, as they are funds domiciled in Luxembourg and under the AIFMD label. Therefore, Spanish regulation and legislation considers their capital gains to be as deferrable over time as those of any Banco Santander or La Caixa fund.

.

And thirdly, by investing in them from accounts in Luxembourg banks, it avoids the restrictive reading of the Spanish regulator to qualify as a professional investor, This makes it de facto impossible for ordinary investors to subscribe to these funds from Spain. These Luxembourg funds are marketed exclusively to well-informed investors (or qualified or professional investors, depending on the nomenclature of each jurisdiction). In other words, a Spanish retail investor cannot invest in them from a bank in Spain, as alternative management is considered a complex product, even though it bears the European AIFMD stamp. Therefore, according to Spanish regulations, these AIFMD funds can only be marketed in Spain for professional investors, which implies very restrictive requirements that are impossible for ordinary investors to comply with. Moreover, the only way for a retail investor to explicitly request to renounce his status and be allowed to invest in these funds from Spain as a professional is to comply with the following requirements at least two of the following requirements according to Spanish regulations:

.

- That the client has undertaken transactions of significant size in the relevant market in the financial instrument in question or similar financial instruments, with an average frequency of 10 per quarter over the previous four quarters.

- The size of the customer's portfolio of financial instruments, consisting of cash deposits and financial instruments, exceeds EUR 500,000.

- The customer holds or has held for at least one year a professional position in the financial sector that requires knowledge of the operations or services envisaged.

.

It should also be noted that it is the Spanish marketer or bank itself that must check and demonstrate to the regulator that these requirements are met, and that it will obviously prefer to sell this client its usual catalogue of own and external retail funds with its juicy implicit or explicit fees, rather than consider him eligible to buy alternative funds that are outside its marketing agreements. It is obviously de facto impossible for most Spanish investors to access such funds from accounts in Spain.

.

By contrast, Luxembourg's regulation is much less restrictive and much more friendly with alternative investment funds for junior investors, as it is sufficient to be considered as a «well-informed» investor. The regulation reads as follows:

.

To qualify as a «well informed» investor you must be either:

- An Institutional Investor

- A Professional Investor

- Any other investor who has confirmed in writing that they adhere to the status of a «well informed» investor and who:

- Either invests a minimum of EURO 125,000 in the specialised investment fund;

- Or who has an appraisal from an EU bank, an investment firm or a management company certifying that they have the appropriate expertise, experience and knowledge to adequately understand the investment made in the fund.

.

In other words, that 125,000 is sufficient for any investor to apply to be considered as an investor in Luxembourg. well-informed and therefore eligible to invest in an AIFMD fund. It is therefore advisable to open accounts with Luxembourg banks in order to be able to invest in these funds. Another thing is that banks require a minimum amount to open accounts for new clients, which is unfortunately often the case. That is why it is also essential to work with a professional who has a sufficient number of clients with these banks, i.e. who has influence on them to persuade them to accept new clients with accounts as small as 125,000 euros.

.

In short, thanks to Luxembourg's less restrictive legislation, any Spanish investor with a minimum of 125,000 euros can invest in a completely legal and transparent manner in AIFMD alternative funds that contain the best alternative funds and hedge funds in the world, despite having very high minimums and being domiciled in jurisdictions only suitable for large institutional investors with complex investment structures and vehicles.

.

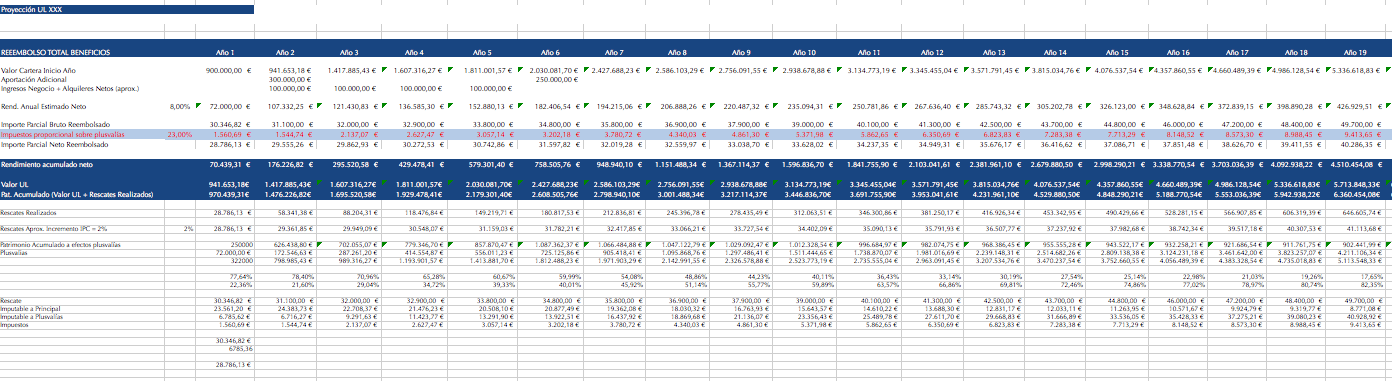

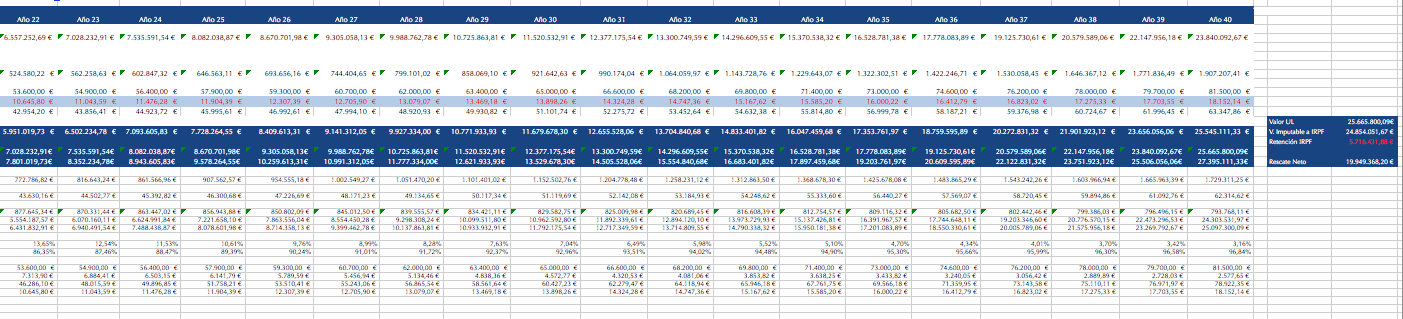

The drawback obviously is that a fund of funds is commission on commission. It is therefore necessary to look very carefully at the historical NET returns obtained by the fund, and whether or not these are clearly higher than those obtained by each individual in their UCITS investment portfolio and Spanish banking universe..

.

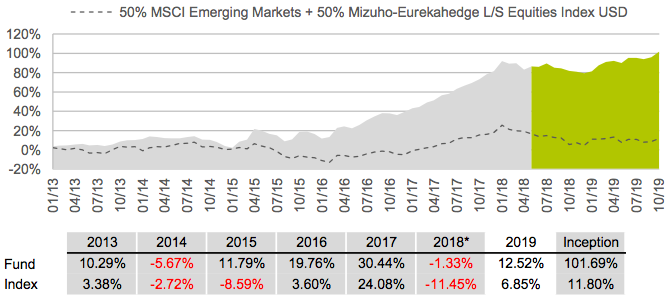

.

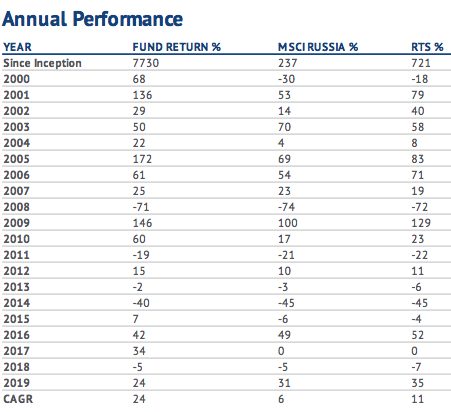

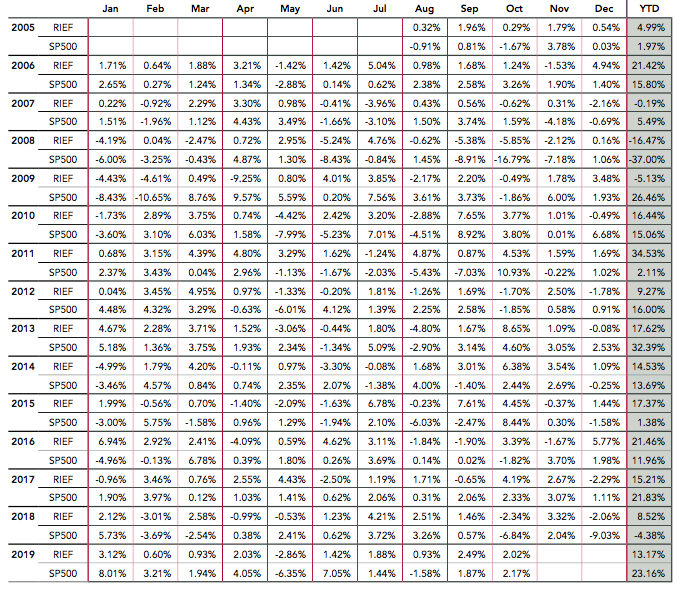

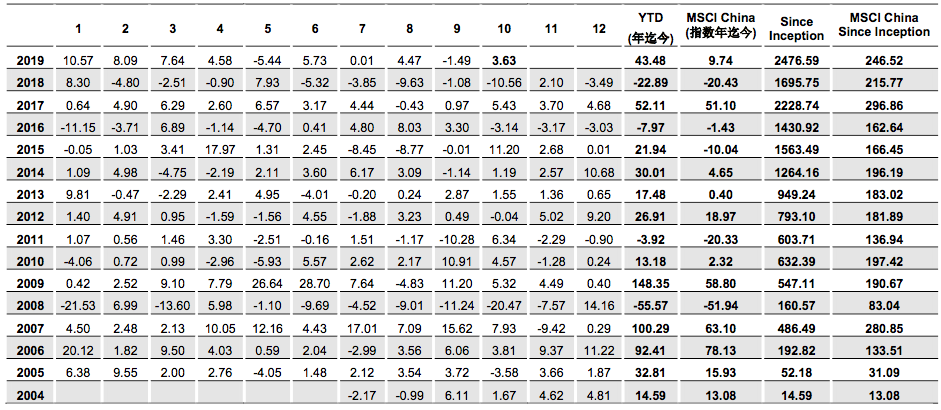

In the tables above you will see the historical performance of 3 world-renowned hedge funds - which some of you may recognise - with minimum investment levels of half a million, one million and 5 million. And finally, below these lines, the performance of a Luxembourg fund of funds AIFMD, therefore accessible to any investor. well-informed with an account in Luxembourg from $125,000, containing a dozen international funds (including the 3 above) plus a few listed stocks (Berkshire Hathaway...), so that you can compare it over the long term with your own portfolios.

.

.

And finally, for those who still think that the limitations of the UCITS environment are worth it because of the possibility of investing only in transferable funds, here is an article entitled «Is it worth holding on to an upgradeable investment in exchange for further deferring accumulated capital gains?«. The results of the calculations you will find in that article are devastating, as just by improving the return by 0.21% per annum, the benefits of 20 years of capital gains deferral are outweighed by the average return of the last quarter of a century. More importantly, once the sold portfolio has been taxed, in addition to being free to invest at a higher yield in any hedge fund in the world, you can also defer taxation forever, either with your own investment vehicle or through a fund of funds AIFMD, as explained in points 1 and 2 above.

.

Having said all this, for those who do not have that €125,000/$ minimum, there are honourable exceptions in the limited and mediocre UCITS environment. World-renowned Spanish value managers such as AZ Valor, Magallanes or Paramés himself (although his COBAS has yet to make headway) may be the best way to invest a small portfolio in an easy and simple way.

According to

According to

Perhaps for those of us who are professionally engaged in it, the answer may seem obvious. Especially for those of us who have suffered for decades in our own flesh the miseries and shortcomings of private banking. It is no coincidence that, in addition to being advisors, we were, are and will continue to be essentially investors, and as such, our interests are still, unfortunately, at the antipodes of those of the banks and their misnamed advice. Having said that, let us now analyse the transcendental decisions that every investor should take to advise on the correct management of their assets.

Perhaps for those of us who are professionally engaged in it, the answer may seem obvious. Especially for those of us who have suffered for decades in our own flesh the miseries and shortcomings of private banking. It is no coincidence that, in addition to being advisors, we were, are and will continue to be essentially investors, and as such, our interests are still, unfortunately, at the antipodes of those of the banks and their misnamed advice. Having said that, let us now analyse the transcendental decisions that every investor should take to advise on the correct management of their assets.