For those of you for whom the trees of panic and volatility prevent you from seeing the forest of opportunities and returns that lie in the palm of your hands, let us explain Nick Maggiulli's simple, mathematical analysis of Ritholtz Wealth, which we fully endorse.

.

The crux of the matter is to shed light on asset purchases during times of panic. But first let us put the current crash in context.

.

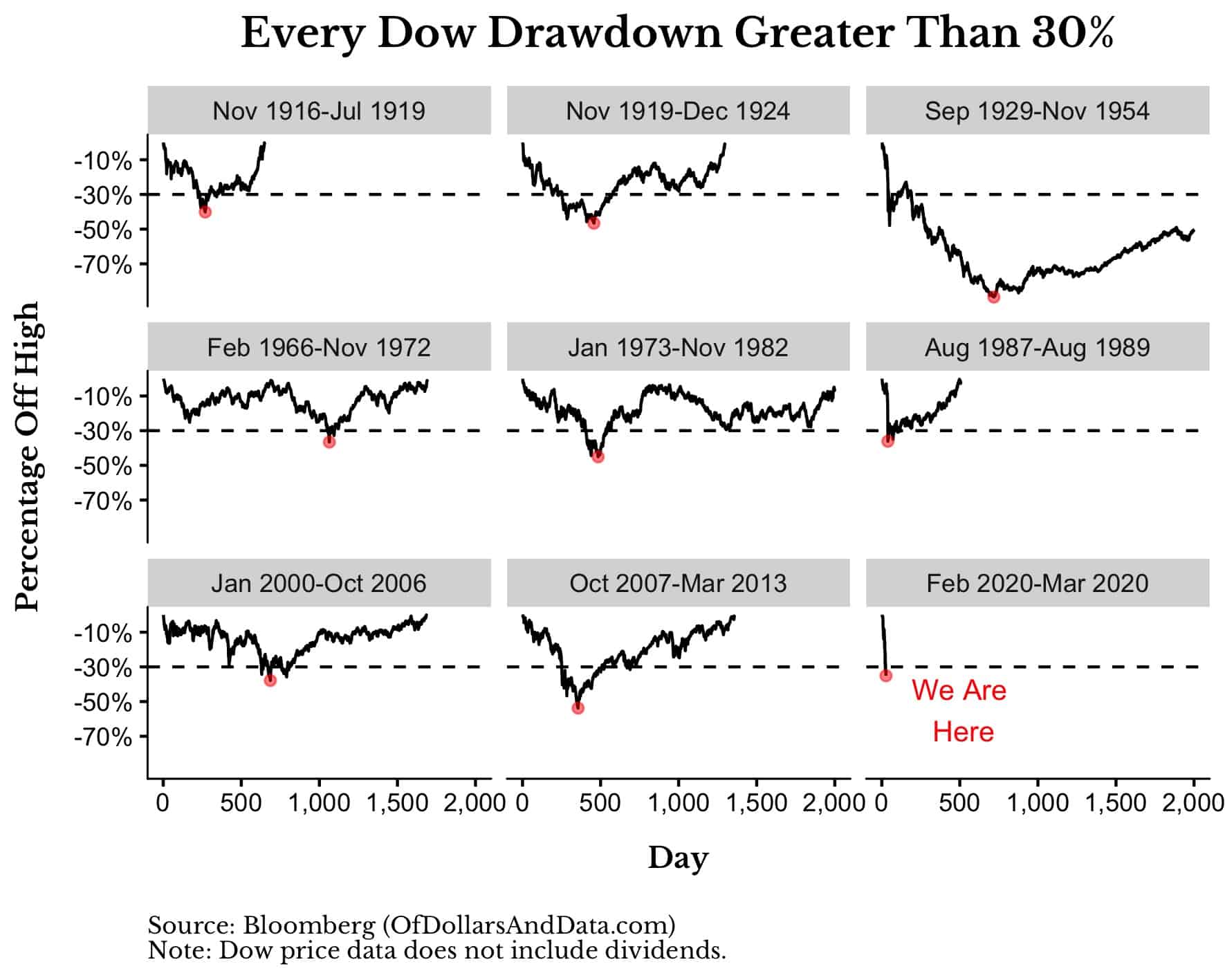

As of today, the low for the Dow Jones has occurred on 23 March 2020 and has been 35% from its highs, making it one of the worst months in the history of the US stock market.

.

If we analyse all the crashes above 30% since 1915, we see that this crash is one of the fastest and fastest we have ever had.

Moreover, while in the past we see the little red dot that signals the floor, at this moment we still do not know if we have already seen the low of last week or if it is still to come in this coronavirus crash.

.

Nevertheless, there is no doubt that these are golden times for investors buying equities now. Every euro or dollar we invest in today's markets will grow much more than those invested in previous months as soon as the markets recover. Because we all assume that sooner or later the markets will recover and humanity as a whole will eventually beat this virus as it has beaten other health crises before, right?

.

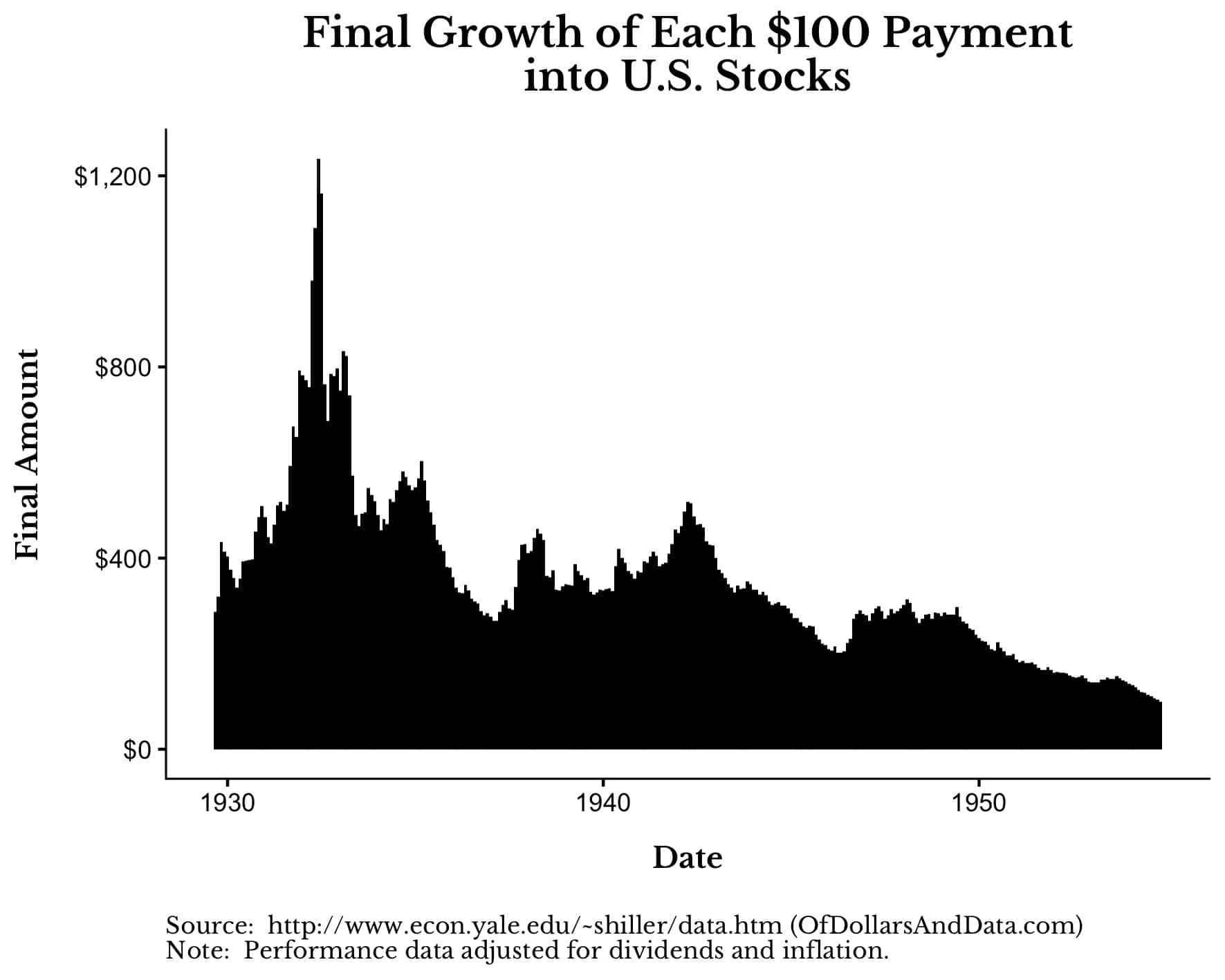

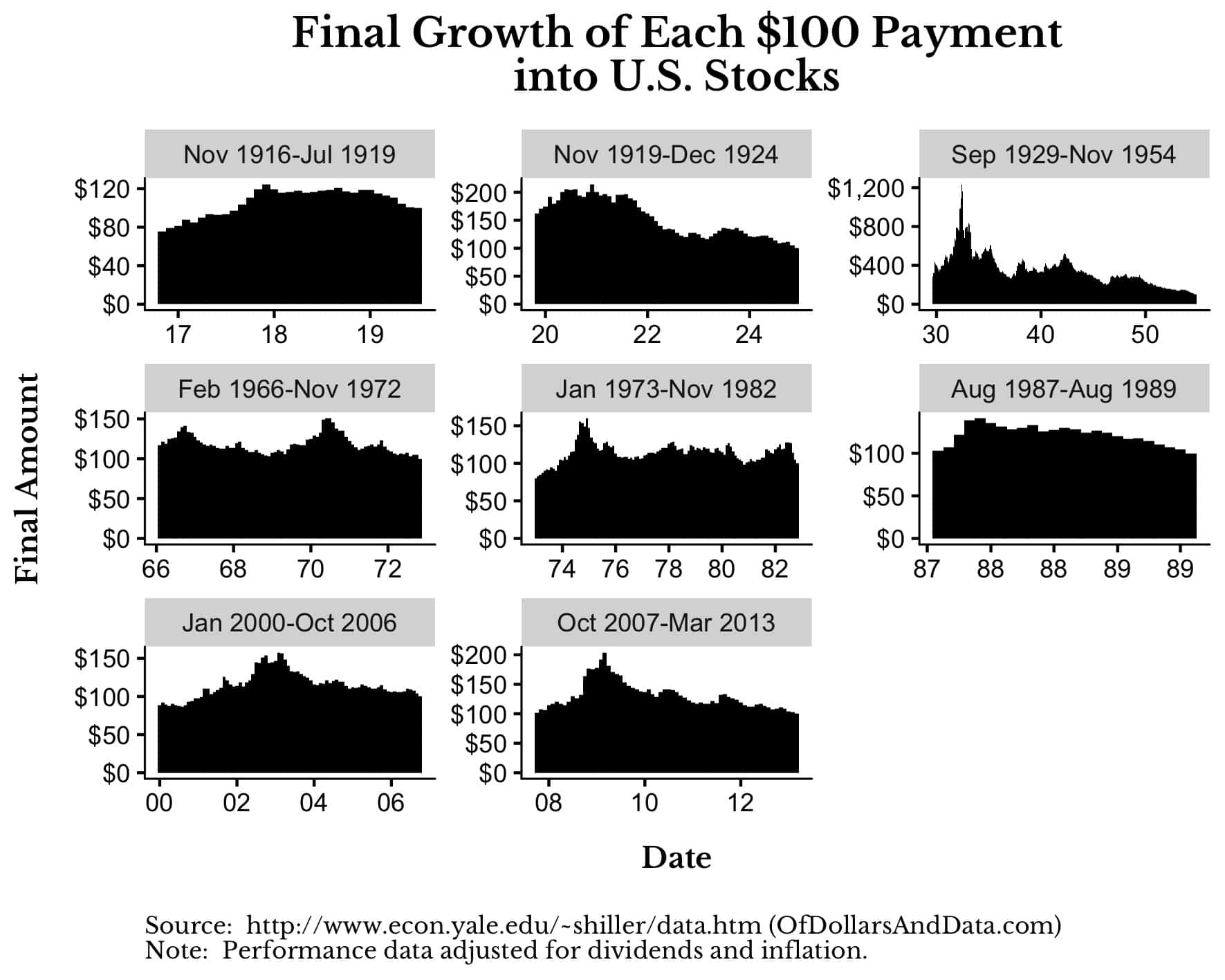

To demonstrate that every dollar invested today will yield much more than those invested before the crash, let us imagine that we decide to invest $100 every month in the US stock market from September 1929 to November 1954 (crash of 1929 and its subsequent long recovery).

.

If we had followed this strategy, this is what each $100 packet would have earned (including dividends and adjusted for inflation) until the recovery was completed in November 1954:

As you can see, the closer we bought to the low in the summer of 1932, the greater the long term benefit of that purchase. Each $100 invested at those lows grew $1200, which is three times as much as the $100 packs bought in 1930 ($400).

.

However, even if we look at the other falls above 30% shown in the first chart, we still see much higher profits if we buy during times of major panic and market declines:

This chart shows that buying near crashes (even if we don't hit their lows exactly) provides between 50 and 100% more profit compared to an investment at other times. That means that your $100 will grow $150 or $200 more (adjusted for inflation) when the market has recovered again.

.

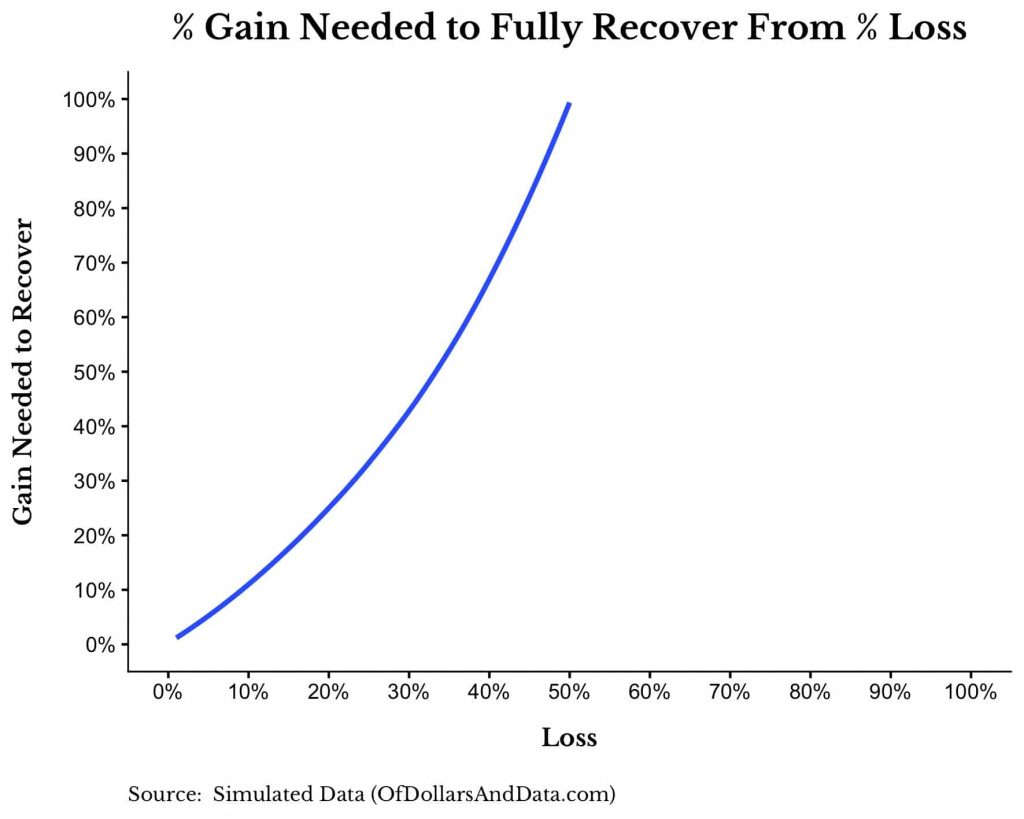

But where does such a spectacular increase come from? Well, besides being intuitive, its origin lies in simple mathematics: Every percentage loss requires a higher percentage gain to compensate for it. At this point in the film, it should not escape anyone's attention that a 10% fall requires an 11,11% rise to recover that loss. In the same way that a 20% loss requires a 25% rise and a 50% fall requires a 100% rise. You can see this exponential relationship very clearly in the graph below:

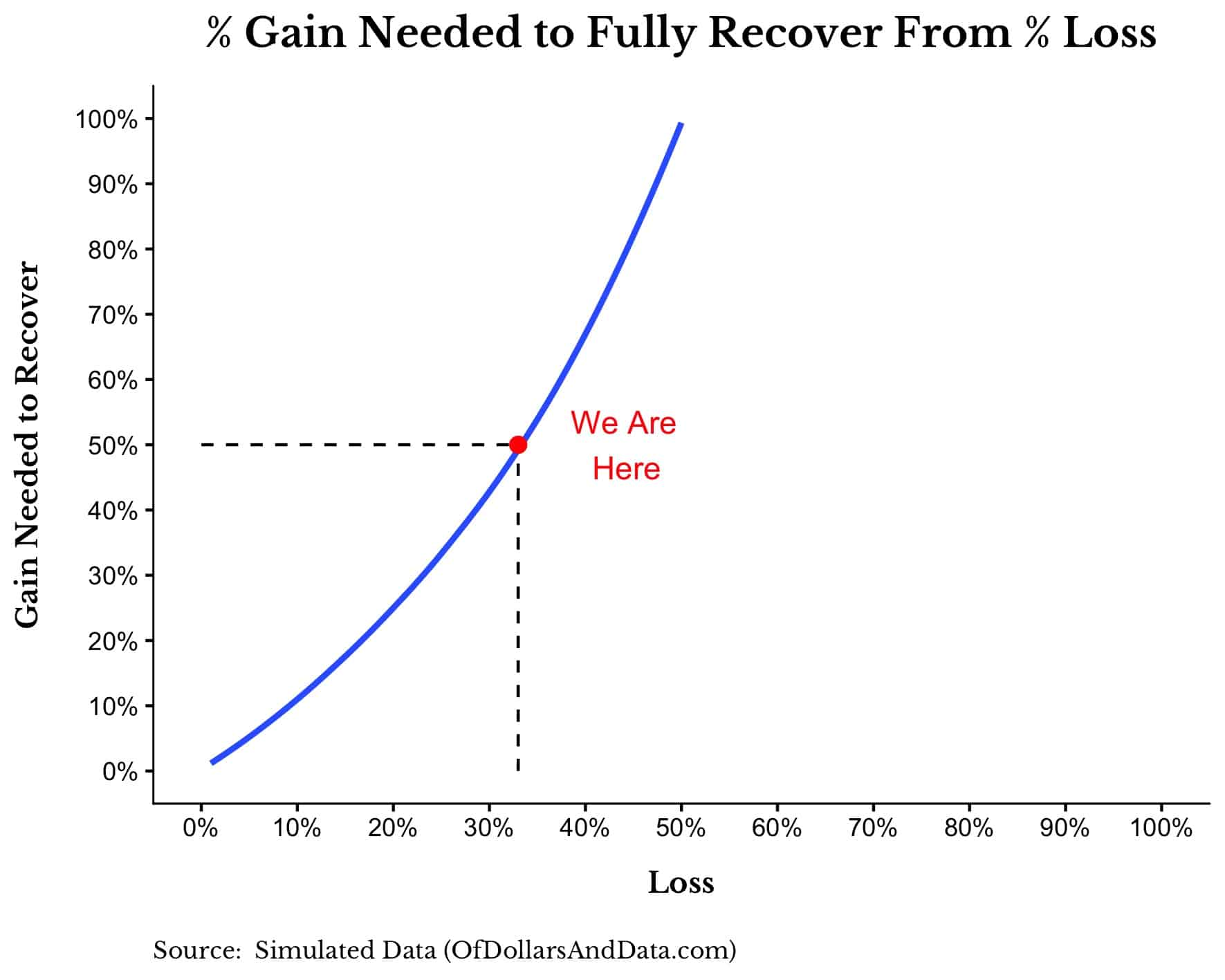

Let us now see what the chart would look like adapting it to the fall in the markets up to last week (-33%) and see the profit that would be needed to recover it:

If we do not see new lows, the recovery needed is 50%. And what a coincidence, for every $100 invested now they will generate $150 (a further 50%) when the recovery materialises.

.

But despite the obvious benefit of buying during the current panic, most investors are not doing so at all. Including those who have a lot of cash, either because they had it in other assets or because they sold during the crash in panic. And thank goodness they don't, because if they did, the crashes would no longer be crashes, and therefore the opportunities for good investors would vanish before they materialised. Excuses for not doing so can be diverse and very convincing for less good investors. Among them are «this time it's different» or «we don't know if it will fall further». As if a good investor is only one who is lucky enough to buy just on the day when the markets quote what will be the historic low of that crash. Remember that in graph 2 we talk about buying "as close as possible" to the low, without aiming to buy right on the bull's eye.

.

Let us now honestly answer the following question: How long do you think it will take for the markets to recover to the pre-pandemic highs? A month, a year, a decade? How long will it take for the indices to recover from that 33% decline? Answer yourselves.

.

Based on that answer, let us return again to the expected annual return in the future for our current investment. The equation is as follows:

Expected annual return = (1 + % Gain needed to recover)^(1/Number of years to recovery) - 1

But since we know that the percentage gain needed to recover is 50%, we can simplify it as follows:

Expected annual return = (1.5)^(1/Number of years to recovery) - 1

Therefore, if you think that the market will take time to recover:

1 year, then your expected annual return = 50%

2 years, then your expected annual return = 22%

3 years, then your expected annual return = 14%

4 years, then your expected annual return = 11%

5 years, then your expected annual return = 8%

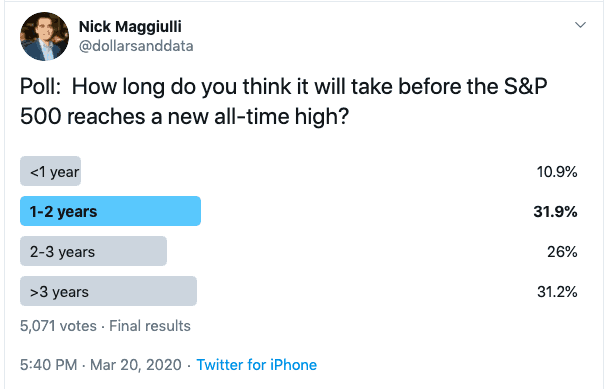

Even taking 5 years for a full recovery, the market would be offering you the same return as the US stock market has historically yielded. Nick Maggiulli asked this same question on twitter and found that two out of three of his poll participants believe that the recovery will come within 3 years.

That means that if the majority of respondents are correct, any investment made now, is going to yield between 14% and 50% annualised until the market recovers. Think about what this means. Investors who choose not to buy at this time are either giving up an annualised return in excess of 14% for the next 3 years, or they believe that the market will take more than 5 years to recover and despise annualised returns of less than 8%. In short, the only reasonable reason not to do so is if you already have all your money invested and have no more at the moment (time to sell grandma to invest more in the stock market, as he said...).

.

Of course, new black swans may occur on the planet, delaying the recovery of markets, as has been the case for decades in Japan, for example. But it seems unlikely, especially in efficient economies such as the US and growing economies such as China and the other Asian economic orbit. Moreover, note that throughout the article we are referring to the market, i.e. the indices. But imagine the figures that will be achieved by those who also have the possibility of investing in actively managed funds that significantly outperform the benchmark indices. In other words, those who invest in portfolios where the management team selects the companies with the greatest potential for recovery at this time (Healthcare sector in China, for example). And we will not tire of repeating that, although the vast majority of actively managed funds do not outperform their benchmarks, especially within the limited universe of funds marketed in Spain, there are world-renowned managers who have been doing so for decades. Unfortunately, however, they are not easily accessible to the average Spanish investor, as we explain in detail in «Why don't large international investors invest in the same funds as you?«.

.

As he once said Jim O'Shaughnesy, Many people confuse possibility with probability, and the two are almost opposites. Keep this in mind as you face new challenges that will come in these days.

.

One of the things that still surprises me is to see how simple mathematics can help us to clarify the thickets in which our own minds entangle us. Our fears and passions are our worst ally in the face of the crash caused by the covid19 virus. Objective figures are certainly a glimmer of sanity to handle Mr. Market's schizophrenia. And the numbers show us that, assuming the market (and even more so our well selected stocks by the world's best managers) will recover in the coming quarters or semesters, the returns we will get are very, very attractive. And therefore, any hypothetical new low in the stock markets would be nothing more than an additional buying opportunity and even higher profits. Fortunately for a minority, the majority do not see it this way and are still waiting to see the floor, like those who are permanently waiting to catch the next train, which will probably be an AVE train that does not stop at their particular station.

After the much read and commented in networks «The lies of the Spanish government and health authorities about the coronavirus«In the third instalment of articles dedicated to the global crisis caused by the SARS-Cov-2 coronavirus and Covid-19 disease. In our first article entitled «Realistic coronavirus figures and the opportunities of an unfortunate crisis»We were already anticipating this: The effects on the entire world economy are devastating in the short term. But only in the short term since the infection has a clear expiry date, Unlike other geopolitical, military or social conflicts, which also generate panic in the markets. Y It is this temporality that should awaken the good investor in us and change our fear for the famous greed that Buffett and other investment greats recommend when the rest of us panic.

.

In this pandemic, which is now beginning to sweep the West, the investment opportunity is one of those that are often called once in a life time, This is one of those rare occasions in the course of a lifetime of investing. This is because, although there is always room for doubt due to imponderables that can complicate scenarios, business activity will probably recover to pre-pandemic levels in the medium term at best. Obviously these imponderables include, for example, a mutation that makes the virus more resistant and/or deadly, war conflicts that add more instability to the world order, or other health crises that could arise and coincide in time with the current pandemic. But if none of these things happen, the recovery in the tone of the economy will be no more than a few months. a couple of quarters, And what should a few quarters mean on the horizon for a good investor? Nothing.

.

Therefore, it's time to go shopping (or hunting, as Buffett would say) and take advantage of the fact that the results of countless good companies around the world are going to be temporarily and exceptionally bad. Because the fall in profits and turnover will not be due to poor business performance but to a lull in global economic activity that is as exceptional as it is temporary. If we talk about airlines, we will find some at half the price of last year. If we look at the energy transport sector, the falls and fluctuations have been insane. And what can we say about the China's health sector, The winning horses, for example, have an exceptional horizon ahead of them because they will be the almost exclusive providers of pandemic and post-pandemic material on a planetary level.

.

But how to find these pearls with such a promising future? Decades ago we learned that it is much more efficient to select the best international fund managers than trying to analyse the best companies on the planet. The knowledge that good local management teams will have of the best companies in their respective countries (Vietnam, India, Brazil, China, etc.) will always be infinitely superior to ours or to that of any multinational management company that tries to make its selection through a manager located in London or New York, even if its forefathers were originally from those countries. We would therefore be well advised to invest our money now in those investment funds who have local and comprehensive knowledge of China (or the specific health sector as mentioned above) or any other country.

.

And those good local managers will not only choose good businesses, but also cheap ones, with bright prospects for recovery. Because if we think that a company may be losing a whole quarter of its turnover due to the pandemic, for example, and we buy it now at a panic price, its growth prospects in terms of turnover over the next 4 or 6 quarters will be spectacular. In other words, we will be investing with Value criteria but with a Growth potential that is as exceptional as it is profitable. If we add to this the fact that we will be selecting companies whose business is based on taking advantage of growing economies and demographics such as those in Asia, the tailwind will further boost our future profits.

.

As the image on the left hand side of the Cobas March Newsletter, It is now, when our neighbours in the 3rd 5th are beginning to realise that perhaps the coronavirus is not just a simple flu, that we should invest without fear and give free rein to our good investor's greed. Now, when our less informed friends and acquaintances are alarmed by the market crashes that are all over the TV news. Just like the lift man who recommended shares to Groucho Marx. in this essential book, or Rockefeller's shoeshine boy invested in the stock market. In other words, when the less informed panic about the coronavirus epidemic and the markets go into a tailspin, it is the most appropriate time to invest in the quality assets that have been exaggeratedly depreciated in recent days. It is perfectly possible, as we have already said, that things will get even more complicated, and that the investments we make today will temporarily lose an additional 20% or 30%. But if they do, and our investments are of quality and made with the good judgement of the best fund managers on the planet, it will be for a very short time. On the other hand, if we remain fearful out of the market, it is likely that we will not see that additional 20-30% fall but a sharp recovery and miss out on much of the upside, having blown this one. «once in a life time».» opportunity.

.

We know that many will read this article but will not follow the recommendation, as it is easy to understand that you have to buy when everyone else is selling, but it is difficult to dare to put it into practice. And thanks to the majority who won't dare and those who don't even agree with our arguments, a few of us will be able to make substantial profits in the coming years.

It is not a question of being tremendists but simply of having a minimum of critical sense in the face of the barbarities that media, politicians and other official agencies in many Western countries proclaim according to their own interests and/or ignorance. For example, the 2% coronavirus mortality figure that is being bandied about is simply not realistic. And to realise this you just need to know how to multiply and divide as well as to know the reality.

.

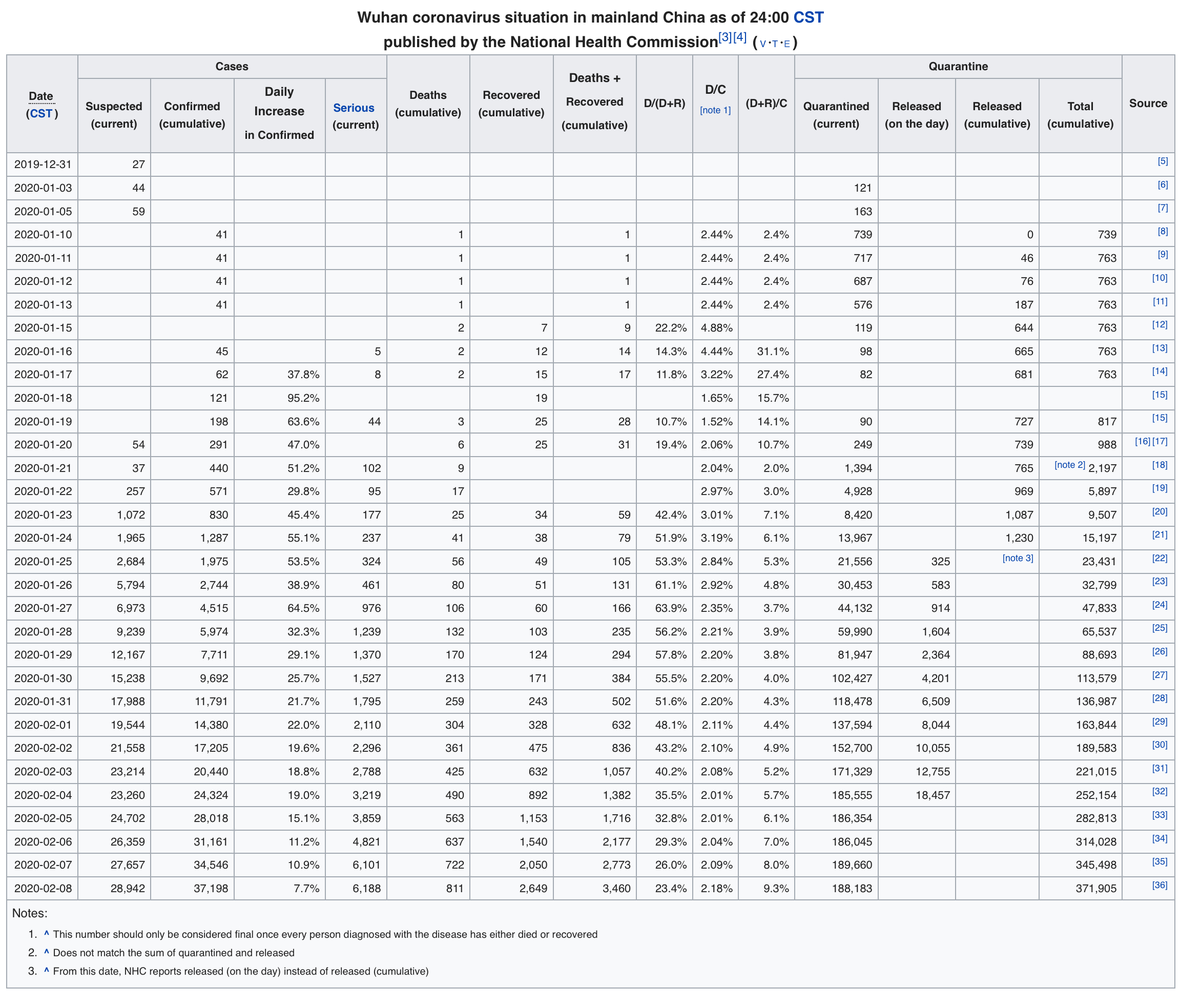

Although it may come as a surprise to many, the Wikipedia (graph below) is one of the sources with the most up-to-date and up-to-date data on the progression of the pandemic. We will take for granted the figures officially published by China to see that the mortality rate is probably much higher than the 2% mentioned, because if we think that the real figures are even worse (what other reason would the Chinese authorities have to manipulate them), the situation and the outlook would be even more terrifying. In the daily updates of those infected by the new or novel coronavirus we see a significant slowdown in the last few days, with the percentage going from over 30% to 7.7% in the last 10 days.

The same is true for the number of deaths, whose increase is also seen to slow down from levels above 35% to the current 12%. Obviously the mortality of an epidemic should be calculated as the number of deaths relative to the total number of infected, and this is what those who claim that the mortality rate of the new coronavirus (2019-nCoV) is around 2% are miscalculating. But it should not escape anyone's attention that they are making a gross error in calculating deaths to date with those infected to date, since many of those infected counted today will, unfortunately, die in the next few days. In other words, the mortality rate should be calculated when the epidemic has already passed, because if we do so during the (current) expansion period, we will be assuming that none of those currently alive will die. Such a basic error can hardly be attributed to the ignorance of those who use the 2% mortality rate as an argument for the inhabitants of the planet to remain unconcerned and live a normal life. The death toll today already exceeds the death toll from SARS. This epidemic only infected 8,000 people in 9 months, while in China alone there are already more than 37,000 officially infected in barely 2 months, and with a real mortality rate that we will now try to guess.

.

It is obviously very difficult to guess how many of those infected today will die in the next few days, and even more difficult to guess how many days they will survive. But just thinking that a fifth of the seriously ill (with altered vitals, i.e. really very sick), who currently account for almost 17% of those infected today, may end up dying in the next 4 days, let's say, and adding those who have already died, the calculation of the mortality rate shoots up to levels above 4%. And that is not counting the fact that none of those infected during the next 4 days will die in the following 4 days... We are therefore facing a pandemic whose mortality rate can only be calculated in retrospect, but which all indications are that it will probably double the 2% proclaimed by most of the media. Remember that the death rate from influenza is much lower than 1%, there is a relatively effective vaccine, and yet it still causes hundreds of thousands of deaths each year worldwide. If we add to this realistic mortality rate of this new coronavirus the chilling ease of contagion it is demonstrating and the fact that the vaccine has yet to arrive, the explosive cocktail is served. Moreover, imagine how this infection will behave in societies adjacent to China such as, for example Vietnam, Myanmar, Laos, Thailand, Philippines, India, Indonesia, Malaysia, etc., with 1.5 billion inhabitants whose hygiene, sanitation and epidemiological control systems are far more precarious than those of today's China. There, the proliferation of the virus cannot be controlled, as it is happening in China according to the official figures of the last few days, but only an accessible and timely medication or vaccine would prevent extravagant mortality.

.

It is worth reading the very interesting analysis by Tyler Durden on Zerohedge, The report rightly points out that in a country like the US itself, the situation could also become very complicated due to the high cost of the health system for the population that cannot afford good private insurance. This would lead the infected Americans to avoid using health services, with the consequent lack of control of the epidemic, despite being one of the societies with the highest per capita income on the planet. Moreover, in most Western democracies, governments would be far more reluctant than the Chinese government to harm their domestic economies to try to control the epidemic. By definition and unfortunately, most Western democracies would be more concerned about bowing to their lobbies and taking populist measures that would not jeopardise their re-election, the economy, or their partisan interests, than they would be about ordering courageous but unpopular measures. We see daily examples of health ministers and mayors downplaying the risks and calling for business as usual so that nothing disturbs the fragile economic balance in southern Europe. Without going any further, it is shameful that it is the companies themselves who have to suspend their participation in the Mobile World Congress in Barcelona, while the local authorities continue to insist on convincing them not to cancel their reservations for hotels, restaurants, chauffeurs and other unmentionable expenses.

.

That said, we should obviously not pin our hopes on controlling the pandemic globally, but on effective treatments and subsequent vaccines that can be made available to the world's population in the coming weeks. Because if we do not have those drugs for several months, the pandemic could reach our own neighbourhoods and claim millions of victims, especially in Asia. But it is not enough to discover an effective drug or vaccine; we must also be able to produce it on a mass scale and at a cost that is affordable for the vast majority of the world's population and/or states.

.

Health sector companies such as Inovio, China, a leader in research into viruses such as Ebola, MERS and Zika, is already testing potential vaccines for 2019-nCoV in animals. And probably the criticised «shortcuts» in international clinical trial protocols that China is surely taking will accelerate the achievement of an effective treatment that will save millions of lives around the world. Because given the extremely high rate of spread and mortality of this coronavirus, time is more than gold, it is Life.

.

But how is this pandemic affecting the global economy? Well, we are just seeing the tip of the iceberg of the destructive effects on economic growth. Obviously the first on the list to be affected is China's economy. But the cascading effect can be devastating because of the interconnectedness between Chinese products and those of the rest of the world. Just look at the Chinese components (often internal and invisible parts) around you, and think that they are already materially temporarily no longer being produced.

.

That word, the temporality, is the key to turning an unfortunate global health crisis into an opportunity. Because even if the treatment or vaccine arrives in time to prevent the global epidemic, the crisis in China is already an inevitable fact. But the fact that a large part of the country has already collapsed, with businesses closed, transport blocked and people locked in their homes, does not mean that this situation cannot be reversed in the coming quarters, but precisely means that China's resurgence is closer. Because, unlike other crises such as a trade war, an economic embargo, a military war or any other geopolitical conflict, this epidemic is not a crisis that can be reversed in the coming quarters. has an expiry date. This is not only because the infection will generate a natural peak and will eventually control itself, but also because any vaccination or medication will drastically shorten this period and the mortality it entails, minimising its effects and invigorating recovery.

.

Assuming that such medication or vaccine arrives in time to prevent a pandemic severely affecting Europe and America, what will be the post-epidemic scenario in Asia? Natural epidemiological timing indicates that a return to normalcy in China may come much sooner than in its neighbours. Moreover, China has far more resources, discipline and health structure to effectively medicate its population when the time comes. The Chinese state's strong political will and economic capacity to recover its economy through financial stimulus, which may even dwarf the QE carried out by Western central banks, will also be decisive. We should therefore expect a massive post-epidemic response from Xi Jinping's government. No effort will be spared to help the Chinese economy make up for lost time, which, let us remember, will not last more than a couple of quarters, given that the treatments (Chinese or Western) will not take long to appear and will be available to whoever pays for them. It is therefore foreseeable that during the second half of 2020 (or even earlier) the recovery of the Chinese economy will be underway, and it will be a matter of state and national pride to return to the path of dominance of the world economy to which the Chinese seem to be destined. Moreover, the trade war with the US has not spilled blood into the river, as we have already predicted almost a year ago, so there is even less reason for pessimism about China's economic recovery.

.

Therefore, in addition to preparing ourselves and our environment for the worst-case scenario of the pandemic (remember that the more than likely current mortality rate is much higher than 2% as we have seen), we would do well to position our investments to take the best advantage of this textbook black swan called the coronavirus. We should therefore take advantage of possible falls in the Asian markets - especially the sectorhealthcareChinese- to buy shares in companies that will rise from the ashes of this epidemic with a strength and pride that we are unlikely to see in the West. Significantly, however, share price falls to date have been surprisingly modest, perhaps in anticipation of such a stunning economic recovery, or perhaps the result of Mr. Market's chronic schizophrenia, who knows.

.

We have long seen Asia's growing economies as the only robust economic growth niche on the planet, and so we are now looking to Asia's growing economies as the world's only economic growth niche. we have said it repeatedly. Only there are the two indispensable factors for economic growth: high productivity; and a demography with a majority of productive young people and a minority of extractive retirees. It is no coincidence that a good number of funds in which we invest are managed in Asia and by local managers. That is why this unfortunate black swan comes, like all of them, accompanied by an opportunity that is rare in the course of an investment life. For the moment the Asian markets seem oblivious to the blockade in the making, and if the pharmacological solution arrives before the stock markets fall, so much the better. But if we see significant price declines in the coming weeks, it will certainly be an opportunity to buy and overweight Asian companies, especially in China, with huge potential in the coming semesters and years.

Paula Leyes achieved a grade 10 in her A-levels and is studying a dual degree in Mathematics and Computer Science at the University of Harvard. She is 18 years old and is one of four Spanish students who have enrolled at Harvard this academic year. This is a record, as never before have so many Spaniards been accepted to begin their degrees at this prestigious American university, which admits only around 1,600 new students from around the world each year. Only 4% per cent of applicants are ultimately admitted, and believe me when I say that the remaining 96% per cent are also outstanding and exceptional students, the majority of whom also achieve top marks during the extremely rigorous selection process. What’s more, Paula has also received offers of admission from no fewer than 14 other highly prestigious US universities, including Stanford, Princeton, Columbia and Georgetown.

.

Paula is clearly an exceptional success story, but Does this mean that only boys and girls with excellent grades and/or plenty of money can go and study at American universities? NO, not at all. Just one step below those elite universities lies a range of hundreds of magnificent universities where any student with grades of 6, 7 or 8 and a reasonable budget can gain access, provided they are genuinely committed and have the right guidance to to study in the United States.

.

This guidance will support interested families every step of the way through the university application process. It is a long process that must begin between 15 and 18 months before the end of the second year of Bachillerato; in other words, we must start preparing the student for US university entrance exams during the first half of the first year of Bachillerato.

.

But what if we’ve missed the boat and are already in our second year of sixth form? Well, that doesn’t mean our hopes of studying in the US are over. We’ll just have to work a bit harder, and we’ll probably need to apply to start university in the Spring Term and not in the Autumn Term. In other words, there is still time, and they won’t miss a whole academic year; they will simply start a term later. This is because, at American universities, new students arrive every term to begin their degrees. There is enormous flexibility within the US university system, both in terms of the academic calendar and when it comes to switching from one degree programme to another and transferring credits.

.

Nowadays, more and more Spanish primary and secondary schools are offering the opportunity to study for terms or entire academic years at public and private schools in the USA. It has become fashionable to send our children to American schools, where they are hosted by local families. And in many cases, this system results in a rather unpleasant personal experience. It is a personal sacrifice for the whole family, which leads most pupils to have absolutely no desire to return to the US to pursue their university studies, as they admit off the record some companies specialise in selling these courses. In other words, this leads to the exact opposite of what was intended, which is integration and acclimatisation to an American academic and social environment, so that students will subsequently wish to graduate from US universities. That is why our recommendation is to save the money for when they start university, as the academic standard of high school in the US is lower than ours. On the other hand, the academic education, university life and financial resources available to universities in the USA is far superior to our university system, whether we like to admit it or not.

But how are we supposed to «acclimatise» our children to an American environment if we haven’t previously taken them to study there? Without that initial experience or temporary immersion, it is unlikely that a 16- or 17-year-old would suddenly want to leave their familiar surroundings in Spain to go to an American university. Based on our experience as consultants (and as parents of students who have gone through this process and are currently studying at American universities), our recommendation is clear: use a few summers during their pre-teen years to send them to camps lasting 2, 3 or even 7 weeks in the USA. These summer camps, as well as being settings of lush natural beauty, healthy and hugely enjoyable (photo below), they offer the ideal immersion in a perfect American environment, where sport and leisure activities form part of the daily routine, and which will make them long with all their might to be admitted to American universities in the future. Furthermore, these summer programmes cost considerably less than the secondary school courses at American high schools currently offered by so many Spanish schools.

So, our children are now settled in, integrated and keen to study for their university degrees in the US. Now is the time to ask the million-dollar question:

Between €10,000 and €55,000 depending on the prestige and quality of the university.

Cost of room and board:

Between 8 and 15 thousand €.

Books, materials, travel and miscellaneous expenses:

Between 2 and 3 thousand euros

Health insurance for international students:

Between €1,000 and €2,000

Bear in mind that the costs of accommodation and meals on the university campuses themselves are comparable to what it would cost us to send our children to study at any Spanish university far from our own city. In other words, it costs the same as living expenses in Madrid, Barcelona or any other European city (or even less).

.

As for tuition fees, as you can see above, they vary considerably depending on the university’s reputation, location, etc. But to give you an idea, prices start at roughly the same level as any private Spanish university, although most high-quality universities charge around 18,000–20,000 euros per year.

.

Can you to secure a scholarship to study at university in the US? The range of scholarships and grants is vast, so depending on the student’s academic and/or sporting ability, these total costs can very easily be reduced. Obviously, to achieve this, the student must stand out from the majority of their fellow students at the university. There are also other forms of financial support that do not depend on either sporting or academic ability, and which can only be fully utilised with the help of expert advisers. For example, some universities offer scholarships simply because the student’s family lives in a town twinned with the university’s, or because the student meets a variety of personal criteria and requirements.

.

However, even without any sort of scholarship or financial aid, and with a fairly average academic record (an average of 6 out of 10, for example), it is possible to find American universities costing from 20,000 to 25,000 euros a year, including EVERYTHING (tuition fees, accommodation, meals, books, insurance, etc.).

Now that we’ve clarified the costs, let’s talk about why it’s a good idea to send our children to study at American universities. And please allow me to speak to you now, not just as US university admissions consultant, but also from the perspective of a father of two children who are currently studying at two different American universities.

.

In the US, it is common for children to leave home to live at university at the age of 17 and only return home during their Christmas and summer holidays. In fact, most American students tend to choose universities far enough away from home so that they don’t have to go home every Friday and thus miss out on the campus atmosphere at the weekends. Furthermore, as – unlike in Spain – unemployment is practically non-existent there, it is common for graduates to move straight from their studies into their professional (and romantic) lives and never return to live permanently with their parents again. That is why it is very unusual there to see university-age and post-graduate children who have not yet left the nest, as is sadly the case in Spain, where young people aged 30, 35 and even older are unable (and in some cases unwilling) to become independent.

.

The experience of a 17-year-old leaving home to immerse themselves in a 100% university environment 24 hours a day, 7 days a week in the USA makes a world of difference to a person’s maturity as they transition from adolescence to young adulthood. As parents, we will not only be giving our children the chance to graduate with university degrees that will open doors for them wherever they go (far more so than Spanish qualifications), but we will also be offering them the best way to learn to spread their wings and fly out into the world, to become independent not only physically but also mentally. In short, we’ll be preparing them to navigate a globalised world like we’ve never seen before with ease.

.

In any job interview, there is usually a huge difference between candidates who have studied at a university in their own city whilst still living with mum and dad, and those who have studied at universities abroad, living amongst other students and far from their parents. In most cases, the former are less likely to secure the job, as the job interview itself takes them out of their comfort zone – something they are completely unaccustomed to – and it all feels overwhelming to them. And that’s not to mention if the role they’re applying for will require them to travel frequently or live abroad. However, for those who have been away from home since the age of 17 and have graduated from top universities such as those in the USA, a job interview is simply another of the many challenges they have had to overcome over the past several years. The difference is vast and obvious to any HR manager or employer.

.

It is true that sending children to the best American universities It comes at a cost that not all families can afford (although, as we have seen, it is much more affordable than many people thought). But giving them an inheritance like that, in kind, will prove infinitely more useful to their success in life than, for example, inheriting a small flat in a village, or half a flat in the capital, or enough money to buy one. However, many parents still think of giving their savings to their children in the form of property, which they will struggle to maintain if their CV does not help them secure a good job. Or they give it to them in cash, at the risk of them squandering it on whatever whims they or their partners might have (holidays, cars, etc.), rather than using it a few years earlier on training that will determine their future success.

.

As the economist Gay de Liébana said in the article referred to above: Given the current economic climate for young people in Spain, families who are able to send their children to study at prestigious universities in countries that attract talent will be doing them a huge favour, as they will have far more resources and contacts to help them excel in their future careers. Conversely, talented individuals who remain within the Spanish university system will, unfortunately, find it much more difficult and are likely to fade into the background, becoming part of the multitude of young people who end up in jobs far below what they deserve given their highly comprehensive university qualifications.

Following on from our article entitled «The shortcomings and dirty secrets of ETFs and index funds«, in which we explained that not all that glitters is gold when it comes to passive management – which is so fashionable these days – we’re going to summarise and discuss the an interesting study carried out by Alexey Panchekha, CFA, on the blog CFA Institute’s Enterprising Investor. In this study, this specialist and researcher in mathematical applications for risk management – who has worked for Goldman Sachs and Bloomberg, amongst others – explains what he has termed the The Active Manager’s Paradox. Let’s see what he is referring to and how the findings of his study might be useful to the average investor.

.

The million-dollar question is: Is the reason why active management has lost ground to passive management over the last decade down to the high fees they charge, the fund managers’ lack of skill, or some other factor?

.

What is needed to answer this question rigorously is not a thoughtless, speculative or emotionally charged response from fans of one management style or another. That is why this study is based on facts regarding the decisions made by active fund managers. As the saying goes, you can hardly manage what you cannot measure.

.

Panchekha has analysed how active managers generate alpha with their selection of companies. They have carried out a multi-year study covering 114 US investment funds belonging to 57 different fund families, and have evaluated more than 400,000 one-year periods of returns (details of the methodology used in the study can be found at the end of this article). Taken together, the study’s sample represents 2 trillion (US trillions) in assets under management.

.

The key lies in the managers’ level of conviction. In other words, the level of certainty that fund managers have regarding each sub-group of companies in their portfolios. To determine this, the study distinguishes between overweight and underweight positions rather than simply the absolute volume, which could be distorted by the mandatory weightings in their respective benchmarks. The study therefore distinguishes between three types of shares in portfolios:

Those with a higher weighting or where there is greater conviction

Those that are underweighted or where conviction is lower

The neutrals

The components of these three categories are identified by measuring their portfolios and weightings on a daily basis, with each group being rebalanced every 14 days. The data was obtained from the Hercules database, provided by Turing Technology Associates. The results, shown in the chart below, illustrate the success rate of each category compared with its respective benchmark indices over successive one-year periods, as well as the annual alphas achieved during those periods.

The Impact of High-Conviction Overweights, Excluding Fees

The Impact of High-Conviction Overweights, Net of 85 basis points’ Fees

As can be clearly seen, overweight or high-conviction positions – comprising the fund managers’ best ideas – are the only category that actually generates alpha in excess of the indices. In 84% of cases when looking at gross returns, and in 74% of them when considering net returns with an average of 85 basis points in fees paid. By comparison, both underweight (lower-conviction) and neutral positions generated a gross success rate of 50% (pure beta), which would fall below that threshold after paying those same fees.

Warren Buffett, Letter to Shareholders, 1966.

.

High-conviction overweight positions – that is, those in which fund managers have the greatest confidence and certainty – are the only parts of their portfolios that generate returns in excess of their benchmark indices. Therein lies the paradox: although active fund managers demonstrate an ability to outperform the indices when selecting their preferred shares, they lose that ability when designing the rest of their portfolios in their eagerness to round them off, diversify them, balance them or reduce their «risk», once again confusing risk with volatility. In some cases, it is a lack of courage, a lack of conviction, or simply that many of them have their hands tied by the ratios and indices which, according to their prospectuses, they are required to follow in a certain way. The reason doesn’t matter. What the study shows is that only overweight holdings and those with high conviction manage to outperform the market. Any other asset allocation will reduce returns.

.

But that’s not all. Furthermore, according to the study, the average fund manager self-sabotages their returns by reducing their high-conviction positions to a meagre 55% of their portfolios. The corresponding allocation to underweight and neutral assets, accounting for almost half of their portfolios, therefore amounts to a beta ballast unbeatable. To illustrate this, Panchekha gives an example from American football, but the equivalent here would be as if the Barça manager only fielded Messi for 55% of the 90 minutes of play.

Of course, there is a reason why fund managers choose to carry this beta burden. For example, adding a market-neutral component reduces the fund’s tracking error relative to its benchmark – something that is surprisingly valued by the sector and some investors. It also reduces the likelihood that the fund’s performance will be exposed to the competition, which is out to poach clients from one another. But in any case, the study shows that all these «risk management» measures – which are of such concern to the industry and to poorly advised investors – inevitably come at the expense of returns, and are acts of cowardice or, at best, of insecurity.

.

The result of this combination of a lack of conviction (in the quality of their analysis) on the part of active fund managers, their lack of courage to set themselves apart from other fund managers, and the regulatory and corporate constraints they face, leads them to manage «risk» in a way that is – paradoxically – risky which causes them to lose everything they have gained and more. The following graph illustrates the harsh reality, Most active fund managers do not deserve the fees that investors pay them to outperform the market, since almost half of their portfolios fail to do so, and the costs do the rest. The problem is that the statistics do not distinguish between diversified and concentrated portfolios. In other words, portfolios in which 90 or 100% of the shares are high-conviction picks, compared with portfolios where, according to the statistics, only 55% of the shares are high-conviction picks.

Actively Managed Large-Cap Mixed-Asset Mutual Funds vs. the S&P 500

Whilst it is common practice in the financial industry to blame high fees for the poor performance of most actively managed funds, Panchekha’s study reveals that fees are only a secondary factor. In other words, Diluting the sole source of alpha in portfolios to levels of 55% has a far more devastating effect on returns than the fees paid. Returning to the football analogy, whilst Barça fans are blaming the team’s mediocre form on the exorbitant bonuses the manager receives (or on the condition of the pitches, or the weather, or injuries, or the referees, etc.), they should instead be criticising him for systematically leaving Messi on the bench for almost half of the matches. Panchekha states, and I quote:

«Whilst it is standard practice in the industry to attribute these outcomes to higher fees, our research suggests that fees are only a secondary factor. Diluting the sole source of stock-selection alpha to a minority component of a portfolio has a far greater structural impact than higher fees.»

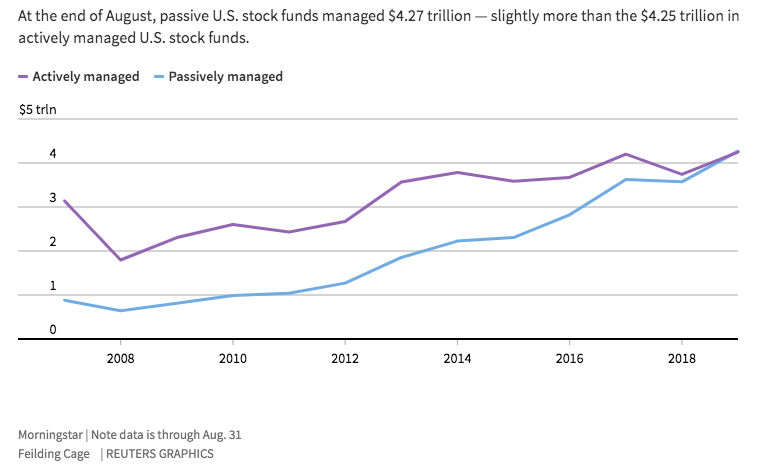

The now legendary underperformance of most actively managed investment funds relative to their benchmark indices has led US investors to withdraw $1.3 trillion (US trillions) from these funds and invest it in the growing passive fund and ETF sector, according to data from Morningstar.

.

The study presents averages and samples of funds without distinguishing between concentrated and diversified portfolio managers. If we separate the wheat from the chaff, that is to say, if we select managers of small portfolios, composed entirely of shares in which they have a very high degree of certainty and conviction, we will find a great deal of alpha and very little drawdown, despite their fees which, as we mentioned in the previous article, tend to be quite high. The NET returns of these star-manager funds, with boldly concentrated portfolios and an in-depth understanding of the businesses in which they invest, clearly and consistently outperform their respective benchmark indices over time, regardless of their TER. Or does any Berkshire Hathaway shareholder really care about Buffett’s salary or that of any of its current executives? And if, at any point, the returns on that holding company were to decline alarmingly, shareholders should be looking more closely at whether its management is beginning to compromise the quality of the holding company – for the first time in decades – rather than at whether Buffett or his successors are receiving high or low salaries.

.

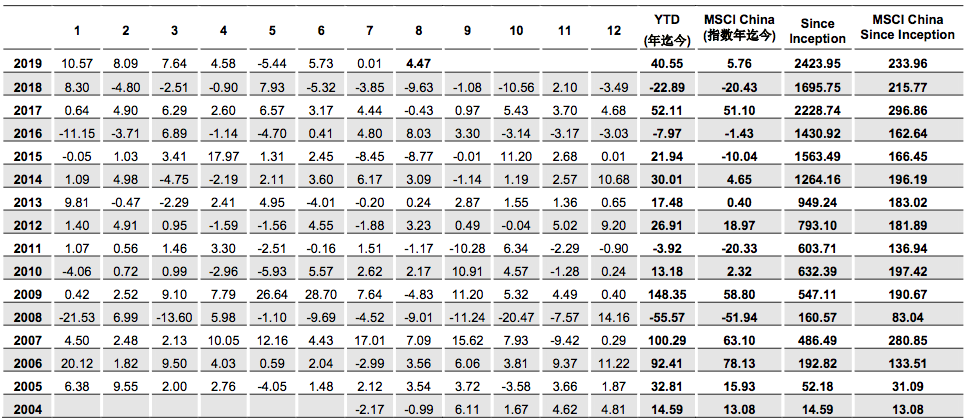

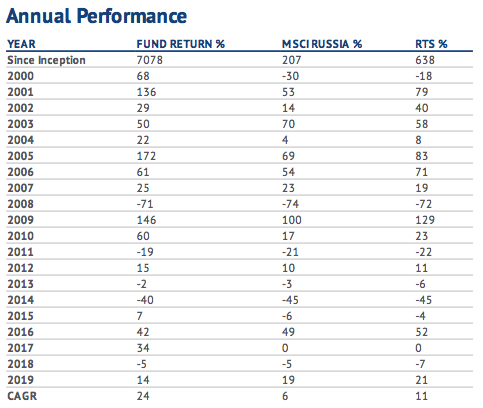

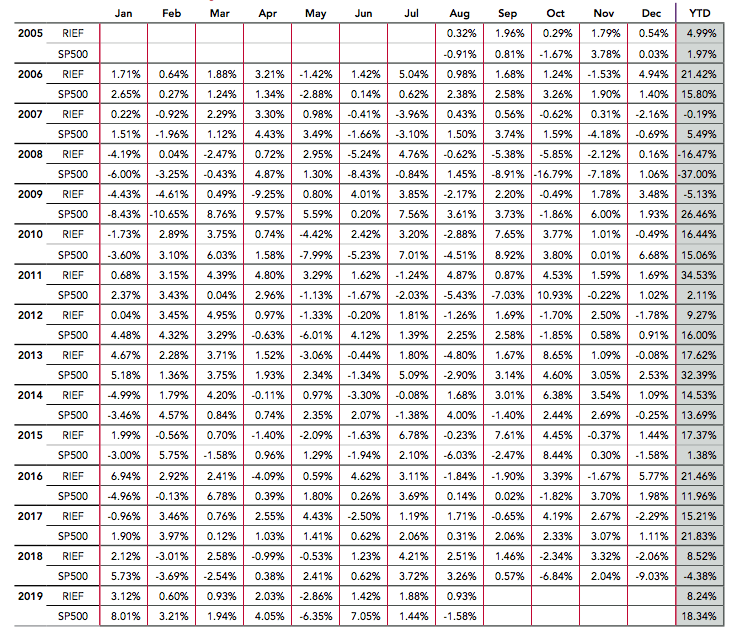

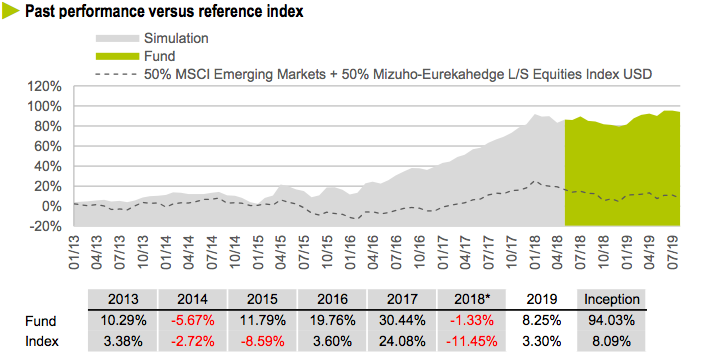

For the sceptics and others groupies When it comes to passive funds and ETFs, the study carried out by Panchekha should be the litmus test: The main reason for the mediocrity of active fund managers is their limited ability and/or lack of courage to concentrate their portfolios 100% on their «best ideas» or high-conviction companies. And this is, after all, an open secret that the world’s best value investors have always proclaimed: Why would you invest in your twentieth-best idea when you can invest in your first, second and third? The only answer is a lack of conviction, a fear of making a mistake, or corporate or regulatory obligations. High management fees are merely the final nail in the coffin for portfolios that are overly diversified and lack conviction and quality. How else could one explain the fact that active funds with the best NET returns on the planet (many of which are already closed to new investors) have fees significantly higher than the average of 85 basis points cited in the study? Let’s look at some examples of spectacular alphas in terms of NET returns in US dollars over the last few decades, the first against the MSCI China Index, the second against the Russian RTS Index and the third against the S&P 500 itself:

Finding funds that overcome the Active Manager’s Paradox is key for investors. But it is also crucial for the active fund industry that more and more managers overcome their fear of standing out from their competitors, that they overcome the self-imposed limitations in their prospectuses, and that they stop viewing concentration and volatility as risk factors. The real risk faced by most active managers who are content merely with not being the worst in their class is that they will eventually become extinct. And their extinction, whilst well-deserved, will increasingly favour the growth of index funds with portfolios that select companies in a far simpler and more superficial manner. Passive funds that behave as if a flat buyer were to decide to go to the solicitor simply by taking a few superficial ratios into account, without fully understanding the property’s condition, its energy efficiency, its building specifications or the neighbourhood, to give just a few examples. Obviously, it is better to buy a flat by taking a few superficial ratios into account than simply buying on a friend’s recommendation or at random, of course. But that is not the way in which our investments will perform adequately in the long term.

.

In short, the good news is that active fund managers as a whole create value. The bad news is that the vast majority of them lose it before it reaches their investors. Investors therefore have two options: To do sufficient research to be able to identify the fund managers with the greatest conviction and concentration in their portfolios; or simply to blame the mediocre performance of active fund managers on the fees paid, and throw themselves into the arms of even more diversified portfolios with less conviction but with low-cost fees. For those who choose to select the active funds they feel most strongly about for their portfolios, it is almost essential that expand their investment universe to include 100% of the world’s existing funds and don’t just settle for the 10% model sold in Spain.

.

Below are the details of the study’s methodology:

Research Design and Methodology

This analysis is based on a proprietary database of daily fund positions and portfolio weights compiled and maintained by Turing Technology Associates Inc. The specific funds included in the research dataset comprise 114 unique US equity mutual funds, from 57 fund families, representing $1.996 trillion in assets under management (AUM).

Fund Selection Process

The funds selected for use in the research were drawn from the set of mutual funds included within a series of investment portfolios known as Ensemble Active Management (EAM) Portfolios. Turing licences a series of proprietary technologies to clients to support their creation of such EAM Portfolios. Each EAM Portfolio is typically constructed from a set of 10 to 15 underlying mutual funds with a corresponding industry benchmark. As of early August 2019, Turing had 24 client-designed EAM Portfolios in live production.

All 114 funds used in the study were selected by Turing’s clients or prospective clients in connection with the design of an EAM portfolio. As Turing’s clients selected the underlying funds and the corresponding benchmark, the fund selection process remained independent of the researchers.

Each pair of a fund and a benchmark is the subject of the analysis. The benchmarks included the S&P 500, Russell 1000, Russell 2000, Russell 1000 Value and Russell 1000 Growth. The time periods used were either January 2014 to July 2019, or January 2016 to July 2019, depending on the data available.

Source of Daily Fund Positions

To access daily fund holdings, Turing applied its proprietary fund-replication technology known as the Hercules System. Hercules is a machine learning-based platform that processes a vast amount of publicly available data, with the core concepts behind the approach having been in use and under development for more than a decade. Hercules is not a regression-based approach. Daily estimated positions are generated by the Hercules System, with the out-of-sample portfolios rebalanced every 14 days.

For reference, the Hercules estimates of fund holdings and weights for the funds used in this study typically generated a tracking error of less than 1%, and a correlation with actual fund returns of more than 99.7%.

Isolating the Manager’s Conviction

The aim of this research was to analyse the impact of manager's conviction in security selection, and so we incorporated two key design elements into the study. Firstly, securities were categorised and evaluated on the basis of their portfolio weights relative to the benchmark. Rather than focusing on actual portfolio weights – which are heavily influenced by benchmark weights – the emphasis was placed on a manager’s decisions to overweight or underweight securities and the scale of those overweight or underweight positions. Second, we divided each fund into multiple, non-overlapping sub-portfolios determined by the level of manager conviction involved, and evaluated their performance separately. Each sub-portfolio was rebalanced every 14 days and treated as a distinct model portfolio. The three sub-portfolios analysed were:

High-Conviction Overweights: A sub-portfolio comprising the fund’s largest overweight positions in equities. The sub-portfolio was selected to cumulatively represent 80% of the portfolio’s aggregate overweight positions relative to the benchmark.

Underweights: A sub-portfolio comprising the fund’s largest underweight positions in shares. The sub-portfolio was selected to cumulatively represent 80% of the portfolio’s aggregate underweights relative to the benchmark.

Neutral Weights: A sub-portfolio comprising overweight securities that are not included in the Overweight sub-portfolio and underweight positions that are not included in the Underweight sub-portfolio.

All sub-portfolios reflect distinct choices made by a fund manager. The dynamic portfolio weights for each sub-portfolio are proportional to the original fund weights, normalised to 100%. Securities not included in the benchmark were excluded as they cannot be properly assessed against a benchmark. All performance data was calculated both gross of any fees and after factoring in a hypothetical 85 bps fee. Neither result reflected transaction costs.

The performance data presented consists of rolling one-year data (daily intervals), which was analysed to determine the percentage of rolling periods in which each sub-portfolio outperformed the corresponding benchmark (Success Rate), and the average excess (or negative) relative return.

A sub-portfolio comprising securities included in the benchmark but not held by the mutual fund (i.e., zero weights) was constructed and analysed. This fourth subgroup was not included in the research results because the only way to capture any potential alpha would be through a 100% short portfolio, which is not permitted in a traditional mutual fund. For reference, the Zero Weight portfolio underperformed the benchmark by 78 basis points, on average. Unfortunately, even a frictionless short portfolio of Zero Weight securities would not be able to generate enough returns to cover the fees of even a standard long-only mutual fund.

Index funds now account for more than 50% of the US equity fund market. And in Europe and the rest of the world, they are also gaining more and more followers. The main culprits for this are undoubtedly those pulling the strings of actively managed funds, whose mediocre net returns are driving disillusioned investors into the arms of passively managed funds. The reasoning of these disillusioned investors is simple: if we’re going to earn little, at least let’s pay low fees for it. But the fact that the majority of actively managed funds (between 8 and 9 out of 10) are mediocre and fail to outperform their respective indices does not mean that investors should settle for this and stop looking for that minority that outperforms them by a wide margin, as we explained in our article published on the COBAS website a couple of years ago. Here’s an example of the alpha in NET returns achieved by certain star fund managers, outperforming any index fund and with lower volatility:

Obviously, for investors who look beyond the products peddled by banks in Spain, there are gems like the one in the chart above, which outperform ETFs and other index funds by a mile. But what’s more, the comparisons are even more damning if we analyse in depth what is happening in the index fund and ETF industry. Let’s look at some of its shortcomings:

.

Just as a junk food manufacturer is a far cry from a good chef, those in charge of massive index funds such as those from BlackRock, Vanguard Group o State Street Corp They have nothing in common with good value fund managers. The former are only concerned with filling millions of cardboard boxes with something that looks like food, is cheap and appeals to shoppers. They couldn’t care less whether their customers end up with obesity, high blood pressure or any other health problems. All they care about is selling more and more volume every day at low cost. Similarly, index funds focus exclusively on pouring more and more millions into their portfolios, without caring in the slightest whether what they are buying are good or bad businesses, well or poorly managed, without caring about their fair value, let alone the long-term returns they will offer their shareholders. After all, why should they care, when more and more investors are turning away from expensive restaurants and resigning themselves to satisfying their hunger with cheap junk food?

What many people don’t realise is that these three giants of the index fund and ETF industry are responsible for keeping inefficient managers in the companies in which they invest. On reflection, the reasons may well be down to sheer carelessness, but if we scratch beneath the surface a little, hidden motives emerge, as we shall explain later. The fact is that its size is becoming such that their votes on the boards of directors are decisive to retain or replace management teams. The result is that not only do they invest indiscriminately in both good and bad companies (something inherent in passive or index-based management), but their votes also serve to keep poor managers in their posts. The million-dollar question is what interest these index fund owners could possibly have in retaining and paying out million-pound bonuses to inept managers. As always, the devil is in the detail.

.

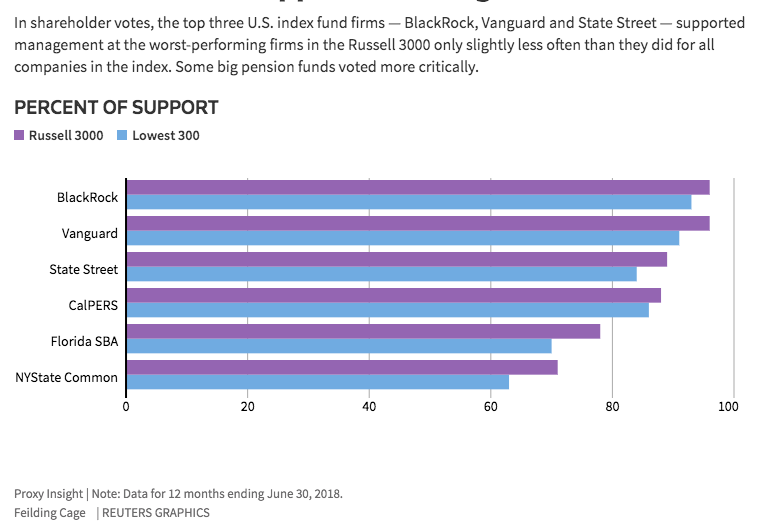

A study carried out by Reuters through the company Proxy Insight (lower graph) shows that in the 300 worst Among companies in the Russell 3000 index where proxy votes were cast, BlackRock voted in favour of management in 931 out of 1,000 cases, Vanguard in 911 out of 1,000, and State Street in 841 out of 1,000. The study concludes that these three giants supported the management of the worst-performing companies only slightly less than that of the other companies in the index, in other words, without caring in the slightest whether or not the management was harming the profits and performance of their companies.

The litmus test is that the percentage of support given by large pension funds to management teams at poorly performing companies is falling significantly. Of course, pension funds do care about returns for their future pensioners.

.

Some might argue that active fund managers do not usually go against the management in place either, but the reality is that active managers no longer invest in companies whose management is performing poorly or with whom they disagree. In fact, that is the essence of active management: identifying good businesses run by good managers, whilst also taking into account their price relative to their intrinsic value, in the case of value investing (Compare these returns with those of any passive fund). What’s more, even if a mediocre, lazy or ill-informed active manager were to invest in a poor-performing company and, through their proxy vote, support a poor management team, the influence they would have on the vote would be infinitely less significant than that of a massive index fund or ETF.

.

Consequently, there is a very real risk that mediocre companies with mediocre management will continue to exist indefinitely, due to the proxy votes cast by giant shareholders such as ETFs and index funds. Why would those passive funds care about the performance of the companies in their portfolios if their aim is not to outperform the index but simply to track it? Why would they confront their incompetent managers, replace them or deny them a huge bonus, if their sole incentive is to grow the fund rather than maximise returns for investors?

.

Another reason – this one more Machiavellian and immoral – for not going against the bad managers of large corporations is that it is those very same executives who are promoting these passive investment funds to their thousands upon thousands of employees. How else can one explain the fact that Vanguard, State Street and BlackRock all voted in favour of doubling the salary of the CEO of the energy company PG&E Corp, just after its shares plummeted following indications that the company was liable for the California wildfires? Or that they approved astronomical bonuses for executives at the cosmetics company Coty Inc – including half a million dollars to pay for their children’s school fees– after the company had been reeling from its reckless acquisition of Procter & Gamble’s beauty division. They have also unanimously vetoed an attempt by the other shareholders to separate the executive powers of the CEO and Chairman of the Board of General Electric Co, following a decade of poor results, etc., etc., etc… Even in the few cases in the Russell 3000 study where shareholders managed to veto executive bonuses, in 601 of those cases BlackRock attempted to award them bonuses through its vote.

.

Bear in mind that the largest holdings in index funds and ETFs, just like the indices they track, are in very large companies – that is, those with the highest number of employees worldwide. This is a vicious circle, as those executives are, after all, fund managers in return for fund owners voting in favour of their million-pound bonuses at board meetings. A win-win for them, but a lose-lose for investors in ETFs and index funds, and for the economy as a whole.

.

As it is the investors in these funds themselves who are most affected by the poor quality of the portfolios, it might seem that this circle is finally closing with a certain sense of justice. But we must not underestimate the damage being done to the global economy, because every day the markets are channelling more and more millions into mediocre companies and teams, with no one seeming to care about this inefficient allocation of capital. Furthermore, Western central banks continue with their free-for-all of cheap money, and with these trillion-dollar injections, alongside those from passive investment funds, We are undermining Darwin's theory of evolution. In other words, propping up zombie companies and executives with money created out of thin air and from investors more concerned with saving on fees than with investing their money wisely.

As Mark Mobius, former executive chairman of Templeton and founder of Mobius Capital Partners, said in an article from March: We need to invest in the stock markets of what are still known as emerging economies. And this time it’s the financial think-tank Gavekal Research who has published a report entitled «Wealth transfer to emerging markets» which is well worth reading. It states that the Keynesian era, that is to say, an era of financial repression and quantitative easing (QE) – or, in short, the era in which the world’s major central banks (the Fed, the ECB, the BoJ, etc.) have been lowering the cost of borrowing to revive the anaemic growth of Western economies across the globe, They are like shots of economic growth straight into the veins of emerging economies.

.

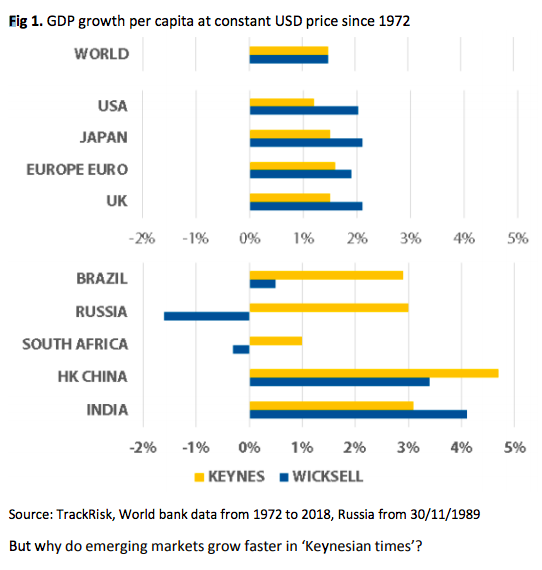

When the performance of gold outstrips that of the world’s major developed currencies, the world enters what is known as a Keynesian era. If we add to this coordinated action by the central banks of developed economies, the current policies of quantitative easing and rock-bottom interest rates amount to the death knell for rentiers. The question is, who stands to benefit from this inevitable demise? Emerging markets, without a doubt. And we can see this clear transfer of money from developed to emerging markets in Chart 1:

.

The lower axis shows the growth in GDP per capita (at constant US dollar prices) since the end of the gold standard. We can see that, in both Keynesian and Wicksellian periods (named after Knut Wicksell, who advocated interest rates that followed the trend of economic growth rather than acting as a corrective tool), growth is the same when we consider the world as a whole. But note that if we distinguish between emerging and developed countries, the picture changes radically. Here, the growth of emerging economies is clearly favoured by Keynesian periods, in stark contrast to what happens in developed countries. And also contrary to what Keynesian policy is, in principle, intended to achieve.

.

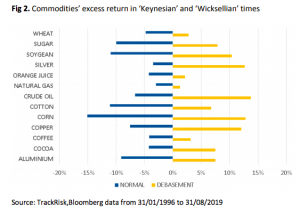

Why is this happening, when intuitively it would seem that loose monetary policies in Western currencies should favour the recovery of developed economies rather than those of emerging economies? The first reason is that emerging economies, many of which are commodity exporters, see their profits rise due to higher export prices. This is because commodities tend to become more expensive when Western currencies depreciate against other assets and currencies, which is what happens during Keynesian eras of low interest rates.

.

This is clearly illustrated in Figure 2, where, by contrast, Wicksellian cycles spell nothing short of ruin for commodity exporters.

.

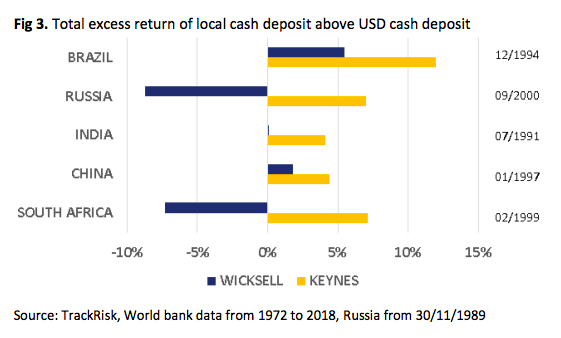

The second reason is that the external debt in US dollars held by companies in emerging economies becomes cheaper under the low interest rates of Keynesian eras, which generates additional profits for these companies. This is particularly true of those based in countries with sound, low-debt and highly productive economies, where their currencies remain stable or even appreciate.

.

Chart No. 3 measures the premium paid on local-currency deposits relative to the US dollar. In other words, it shows the savings in funding costs for these companies compared with the costs they would have incurred in local currency during Keynesian periods. Specifically, the additional cost of local currency financing ranges from 4% to 12% per annum in the BRICS countries. The savings are very significant for emerging markets, just as the reverse is true for developed markets, which in turn will benefit from this Keynesian era by investing their capital in emerging economies whilst assuming the local currency risk. In other words, capital is flowing into emerging economies through various channels in these times of ‘free money’ in the West. Among other reasons, this is because it is ‘free money’ for which there is nowhere in the West itself to invest it so that it yields even the slightest return.

.

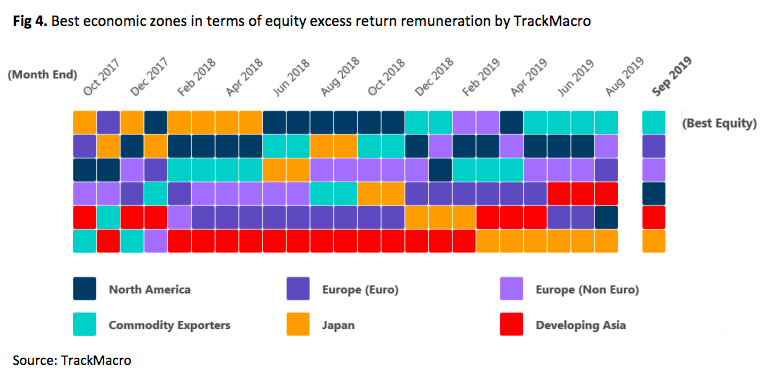

Furthermore, TrackMacro confirms that, as of September 2019, the ranking of the risks associated with holding shares in companies across the world’s various economies is as shown in Chart 4. In other words, commodity-exporting countries have been enjoying a boom since last August, topping the chart for the past five months. Note that the «Developing Asia» group excludes Asian commodity exporters, which are classified as «Commodity exporters». Therefore, it is clear that not all emerging markets are benefiting from these cash flows, just as we cannot place the German and Greek economies on the same level, even though both are «developed European» economies.

.

To further reinforce the case for investing in certain emerging markets, TrackMacro also reports that, according to key macroeconomic indicators, major commodity exporters such as Russia and Brazil offer an attractive risk-reward ratio. If we add to this the positive measures being taken by various emerging-market governments – such as the cut in corporation tax in India, made possible by the country’s low debt levels and a productive demographic – the case for investment becomes even stronger. We should invest in emerging economies with the same natural confidence and the best prospects as developed markets once had. But, of course, we must do so through the best local investment fund managers, who have a thorough understanding not only of companies in their own country but also of their legislative, accounting, tax and even cultural intricacies.

Investing whilst emerging markets have the wind in their sails and avoiding headwinds (debt, demographic trends, recession, low productivity, etc.) will be key in the coming years. For holders of typical Spanish share portfolios, here is a damning statistic: today, the Ibex 35 stands at the same level as in 1998, whilst the German stock market has risen 2.5-fold over the same period, the US market 2.7-fold and the Indian market 10.5-fold. But what is the worst for some and the best for others is yet to come.

.

Conclusion: Keynesian policies in the major developed economies should, in theory, combat deflationary pressures, stimulate domestic growth and strengthen Western companies in the face of competition from emerging markets. However, the outcome of such a policy of quantitative easing and sub-zero interest rates may be exactly the opposite. The depreciation of Western currencies leads to a massive influx of capital into emerging economies (which, incidentally, are natural magnets for investment in their own right, even without such desperate measures in the West). Investors today find themselves in an asymmetrical situation, where their major currencies have ceased to be safe-haven assets due to low interest rates. This ‘Age of Central Banks’ favours, in principle, gold, real assets and shares in emerging-market companies, to the detriment of developed economies, sovereign debt and shares in Western companies.

.

As Mark Mobius rightly pointed out in the article cited, in the late 1980s emerging economies accounted for just 5% of the global market, but now they account for more than 40%, and the figure is rising rapidly. Back then, investors could only invest in no more than half a dozen stock exchanges; yet now we have more than 70 markets open to growing foreign investment, fully equipped with state-of-the-art technical facilities and supervised by highly professional regulators. This now allows for enormous diversification and security, and shows us the way forward: now is the time to invest in certain economies emerging - or already emerging where there is a tremendous economic recovery and growth. Furthermore, the US-China trade war is nothing more than a golden opportunity to do so at reasonable prices. And anyone who continues to peddle fears about investing in emerging markets is either misinformed and out of touch, or is simply following orders from their superiors to peddle a deflationary, recessionary product that has smelled rather foul ever since central banks turned on the tap to keep zombie economies and companies afloat.

Although most investors have never looked beyond the Solvency Standard, we must not forget that it is now 48 years since the US monetary authorities decided to abandon the Gold Standard – that is, the pegging of the dollar’s value to that of the precious metal. The practice of pegging money to a commodity that conferred intrinsic value upon it was widespread not only in ancient times but also throughout the 19th and 20th centuries, and so its abolition in the early 1970s caused considerable unease amongst US savers, who were accustomed to sleeping soundly in the knowledge that they could exchange their bank notes for a proportion of gold. The difficulties faced by issuers in maintaining the value backing for their currencies were in crescendo, with the result that the proportion of intrinsic value in the money issued gradually decreased, thereby allowing the money in circulation to increase beyond the limit originally set by material wealth (commodity) itself.

.

From that point onwards, intrinsic value began to be gradually and more or less subtly replaced by confidence (fiat) in the issuer. In fact, in some countries such as China, parts of what is now Canada, and other European countries and kingdoms, this path of no return towards fiat money began centuries ago. The new fiat money standard quickly took hold in the West during the 20th century, driven by the economic pressures resulting from the world wars, thereby placing the value of money entirely in the hands of (fiat) in the states, which were, unsurprisingly, delighted by the opportunities for political manipulation of money that this afforded them. With the end of the Bretton Woods Agreement in 1971, the US definitively buried the intrinsic value of its currency, and fiat money became the global standard – in case anyone still had any doubts. From then on, obviously, some states fared better than others – take, for example, the US versus Argentina, Venezuela or the ‘banana republics’ and their hyperinflation. But even for the top performers, the confidence of most savers in their respective governments has not been enough to prevent a loss of purchasing power over the years.

.

The fiat money system is here to stay, clearly, and we will never again see our money pegged to any real asset. It is simply too tempting for governments to have the power to create an infinite supply of electronic (formerly printed) money. But despite this endless possibility, which hyperinflationary ‘banana republics’ have been abusing, That Fiat standard was self-imposed, based on a criterion that has been key for almost 50 years: solvency. In this way, by linking the ability to create an infinite amount of money to the limits of solvency for repaying debts, Fiat money has, in fact, been the replacement of the gold standard with the solvency standard. In other words, trust in the state had a limit, which was none other than its actual ability to repay its debts and balance its books between public spending and tax revenue from the population without causing inflation to spiral out of control. For this reason, for decades there have been countries whose currencies depreciated against others due to mismanagement, forcing those states to cover their budgetary excesses with new money or public debt, which in turn fuelled inflation. This public debt had to be considered attractive enough for private capital from domestic and foreign investors to finance it. Investors who, consequently, demanded in return an interest rate commensurate with the risk that that state would be unable to pay its debts without printing banknotes, and that inflation would therefore erode its purchasing power. In other words, interest rates which in turn placed a price on the currency issued by each state, based on its ability to balance its books and its inflation rate, that is to say its Solvency.

.

We therefore had a system whose insolvency was self-regulating, since anyone caught in an unstoppable spiral of debt at rising interest rates and galloping inflation would default within a few years, dragging their economy and that of their ill-advised fellow citizens into ruin. But as politicians have never known how to steer the economy, the abuse of debt – even in countries that kept their inflation under control – began to bubble up. Until the debt crisis of 2007 struck, followed by the crash of 2008. By then, excessive debt was so widespread and insolvency so high that the risk of default by insolvent parties was systemic, starting with the entire Western banking system. Solution: Draghi’s famous phrase, «whatever it takes«In other words, central banks will generate as much money as is needed to turn the insolvent into the solvent and thus save the system. Because with infinite liquidity, the insolvent party never goes bankrupt; they simply extend and roll over their debts to infinity and beyond, allowing creditors to avoid having to set aside provisions for bad debts beyond what their balance sheets can bear. It’s a bit like the ostrich that buries its head in the sand.

.

The new standard is therefore that of fiat money, but for the past decade it has also been infinite by decision of the world’s most powerful central banks. In other words, The money needed to keep banks, large systemic companies and the states themselves afloat is being created and will continue to be created, as is the case in the southern part of the eurozone, by adding zeros to its debt and with negative interest rates (we already discussed this 6 years ago in financial repression). Some of the obvious drawbacks are that we are allowing zombie companies – inefficient and up to their ears in debt – to survive, as they repay their maturing debts with new money created by central banks in exchange for their worthless IOUs. Another fatal drawback is that sub-zero interest rates not only keep insolvent public and private entities afloat but also provide even greater incentives for private borrowing. For all these reasons Solvency is no longer a ratio to be taken into account. It will also be chaotic that all these ultra-low-yield instruments are sweeping aside anyone who has made income their modus vivendi or modus operandi – that is to say, private rentiers, pension funds, insurance companies, sovereign wealth funds and other sources of capital seeking to avoid stock market volatility. To date, we have only A decade of zero interest rates, but the damage that quantitative easing will cause in the medium and long term is devastating for the sustainability of funded pension schemes (just as the ageing population we are also experiencing is for pay-as-you-go pension schemes).

.