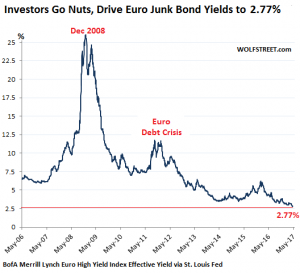

At the end of last week something unheard of happened, something absurd even among the absurdities of this New Normal that Central Banks have put us in: The average yield on junk bonds (the riskiest and most insolvent of corporate bonds) denominated in Euros fell to record lows of 2.77% per annum.

.

Already on 26 April, the absurdity of the ECB's negative yields policy hit a milestone, with yields on the most insolvent debt falling below 3% for the first time in history.

.

Comparatively, the most liquid and safe debt in the world, the 10-year US Treasury bond, yields 2.33% per annum, and the 30-year Treasury yields around 3%.

.

The following chart of the BofA Merrill Lynch Euro High Yield Index shows the madness in the Eurozone:

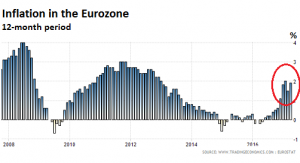

And it is not that these ridiculously low yields are the result of rampant deflation, despite the alarmism created in the last few months, no. The official annual inflation rate has been at 1.91 PPP3T and, as we can see in the following chart, it does not seem to be going away any time soon. Official annual inflation has been running at 1.9% and as we can see in the graph below, it does not look like it is going to disappear in the short term.

In other words, the real average yield on junk bonds, net of officially recognised inflation, as seen in the two indices above is now only 0.87% per annum! That is the return that bond buyers/investors get for lending their money to companies with junk ratings and manifest insolvencies for years, with risks of defaults (recognised by Fitch, Moody's and S&P) on the horizon more than considerable.

.

Against this backdrop, of course, it is not only European companies that want to raise fresh money. Like flies to honey, American companies are also flocking to the euro in search of euros from unsuspecting European investors in exchange for ridiculous interest rates. These are the so-called «Reverse Yankees», or issues by American companies in euros, eager for almost free credit. But why are European investors offering their money to insolvent debtors in exchange for so little? Have European investors gone mad? I'd better not answer you...

.

The answer lies in Draghi's efforts to implement his now reduced QE of 60 billion euros per year, which includes sovereign bonds, covered bonds, investment grade (IG) bonds and ABS. In addition, Draghi cut rates to negative -0.40%, thus intensifying the rise in debt prices and compressing yields on all debt, both sovereign and corporate (financial repression). What the ECB does not buy directly are junk bonds, but that does not mean that it does not end up with them in its cabinets (balance sheets), as it has bought and will buy paper that has become junk over time. And no one will be able to say that this was a misfortune that no one could have suspected, since much of this debt was already junk before it was bought and was given a rating upgrade by hammer and tongs to fit in with the politically correct requirements of the ECB.

.

As a result of this QE and NIRP (Negative Interest Rate Policy), many corporate bonds are now trading at yields below zero. For example the German 5-year bond is at -0.33%, which subjects investors to a very deep -2.23% after deducting official inflation! Obviously investors who want to achieve positive net (inflation-beating) returns, must either jump into the arms of much more insolvent and risky junk debt. Or they must fly into other currencies, such as USD debt. These are the NIRP Refugees, who «migrate» elsewhere to avoid the devastating effects of their indigenous debt.

.

The million-dollar question is why those affected by NIRP are risking so much for so little. Many are institutional investors who are obliged to buy euro bonds, such as insurance companies and euro fixed income funds. Moreover, with rising US rates, it is no longer even almost free to hedge EUR/USD currencies, as it was a couple of years ago. As a result, these institutional investors are condemned to buy wet paper at exorbitant prices and in exchange for ridiculous yields. Nor should we forget that these institutions are managing other people's money and not their own, what we will call DDO (Other People's Money), making it easier to take on bread for today and hunger for tomorrow, when this debt defaults or its price returns to more reasonable prices and generates huge losses for the unwary investors. The fact is that the managers of these institutions are paid to place these gigantic flows of DDOs, and they do so in line with the rest of the institutions. Because when collapse and losses, They will not be alone, as the rest of the institutions will suffer just like them. DDO that will blow up in everyone's face, in a very distributed and not very inculpatory way.

.

The more debt the ECB buys, the lower yields are in a perfect fish-bite, as well as other damage of incalculable consequences. Flooding the bond market with money is the perfect flight forward, satisfying the yields and capital gains needed by those who bought yesterday or last year. Play the game while the music is still playing, and no institution is going to stop before disaster strikes.

.

In addition to institutional investors, junk bonds are also sold at the price of gold to retail savers, unsuspecting investors who put their money in the «safe» and «guaranteed» funds sold to them by their corseted, sympathetic and trustworthy bankers (sic). And what has happened in the last few years, in which the music has continued to play non-stop, proves them right! Who hasn't made money buying this wet paper (sovereign or corporate) in the last 5 years? Why can't it continue to be like this for the next 5 years? Something like this thought the turkey the day before Christmas...

.

But the reality is that more and more issuers are turning to the European open bar. From runaway Spanish banks to the Mexican oil company Pemex, which placed 4.3 billion euros just a couple of months ago.

.

But bonds are not like shares. Bonds pay off (if you hold them long enough) at par. If you come to maturity, with these compressed rates, you can only make money if you have previously bought them at a discount. But in the current scenario, far from that, bonds are being bought in the secondary market above par! So what is the hope of all holders, traders and hedge funds of overpriced euro bonds? To get them out of the way early enough to gain a few pips before it is too late. But for institutional investors who have to hold them to maturity because their business model demands it, there will be no happy ending. Unless some clever institutionalist passes the hot potato in time to other, less experienced and more innocent hands, in the form of banking products that offer three times as much as a deposit, «with total security».

.

Via wolfstreet.com