More than a decade ago, shortly before the crash of 2008, the manager of the Hedge Funds Mark Sellers of Sellers Capital gave a great speech to a group of Harvard MBA students entitled «So you want to be the next Warren Buffett? What does your writing look like?» Sellers pulled no punches when he talked about the difficulty of becoming a great investor who can earn returns at 20% compounded annually saying: «I know everyone in this room is extremely smart and has worked hard to get to where they are. They are the brightest of the bright. However, there is one thing you should remember from my talk: You have almost no chance of being a great investor. You have a very, very low chance, like 2% or less».

.

Here is an extract from that speech:

.

One thing I will tell you up front: I am not here to teach you how to be a great investor. On the contrary, I am here to tell you why very few of you can expect to achieve this status.

.

If you spend enough time studying investors like Charlie Munger, Warren Buffett, Bill Miller, Eddie Lampert, Bill Ackman and others who have had similar success in the investment world, you will understand what I mean.

.

I know that everyone in this room is extremely intelligent and has worked hard to get to where you are. You are the brightest of the bright. And yet, there is one thing you should remember if you remember nothing else from my talk: You have almost no chance of being a great investor. You have a very, very low chance, like 2% or less.

.

And I'm pondering the fact that you all have high IQs and are hard workers and will soon have an MBA from one of the best business schools in the country. If this audience were a random sample of the general population, the probability of anyone here becoming a great investor later on would be even lower, like 1/50th of 1% or something. You all have a lot of advantages over Joe Investor (the everyday investor), yet you have almost no chance of standing out from the crowd in the long run.

.

And the reason is that it doesn't matter much what your IQ is, or how many books or magazines or newspapers you have read, or how much experience you have, or will have later in your career. These are things that a lot of people have, and yet almost none of them end up making 20% or 25% in the course of their career.

.

I know this is controversial and I don't want to offend anyone in the public. I'm not pointing to anyone in particular and saying: «You have almost no chance of making it big». There are probably one or two people in this room who will end up making money at 20% during their career, but it's impossible to know in advance who they will be without knowing each of you personally.

.

On the bright side, although most of you will not be able to compound money at 20% for your entire career, many of you will turn out to be good, above-average investors, because you are a biased sample, Harvard MBAs. A person can learn to be an above average investor. He can learn to do well enough, if he is smart, hard-working and educated, to keep a good, well-paying job in the investment business throughout his career.

.

You can make millions without being a great investor. You can learn to beat the averages by a couple of points a year through hard work and an above-average IQ and a lot of study. So there is no reason to be discouraged by what I am saying today. You can have a really successful and lucrative career even if you are not the next Warren Buffett.

But you can't accumulate money at 20% forever, unless you have it engraved in your brain from the age of 10, 11 or 12. I'm not sure if it's by nature or by education, but when you're a teenager, if you don't have it, you can't get it anymore. By the time your brain is developed, you either have the ability to run circles around other investors, or you don't.

.

Going to Harvard or other high-level public and private universities will not change that and reading all the books that have been written about investing will not change that either. Neither will years of experience. All these things are necessary if you want to become a great investor, but in themselves are not enough because they can all be copied by competitors.

.

7 traits of highly successful investors:

.

In my view, there are at least seven traits that great investors share that are true competitive advantages because once a person reaches adulthood they can no longer be learned. In fact, some of these traits cannot be learned at all; you are either born with them or you don't have them.

.

1. The ability to buy shares while others panic and sell shares while others are euphoric. Very easy to say but almost impossible to apply when the time comes when the world is sinking and there are a thousand reasons to think that this time it is different.

.

2. The second character trait of a great investor is that he is obsessive. They get up in the morning and go to bed at night thinking about companies, share prices, economic and financial data, and they want to win and win.

.

3. A third trait is the willingness to learn from past mistakes. There is little point in not doing so as it will not inoculate us from making the same or similar mistakes in the future.

.

4. A fourth trait is an inherent sense of risk based on common sense. It is as simple as that. No matter what the computers and calculations of probability of success say. Common sense must never be abandoned, and it will become our best ally and protector from disaster.

.

5. Great investors are confident in their own convictions and stick to them, even when faced with criticism. This is also easy to say but very difficult to do, when you see that everyone around you thinks just the opposite.

.

6. It is important to have both sides of the brain working, not just the left (the one that is good at mathematics and organisation). This is why many great investors are also able to write very well. The right side of the brain is able to detect subtleties that are very important for investment success, such as the character or behaviour of managers, and not just the business figures that their teams publish.

.

7. And finally, the most important, and rarest, trait of all: The ability to live through volatility without changing your investment thought process. This is almost impossible for most people; when the going gets tough, they have a hard time not selling their stocks at a loss. You have to distinguish between volatility and risk, and this is something that much of the industry - not just ordinary investors - confuse and condemns them to mediocrity at best (I recommend reading «Why do they call it Risk when they mean Volatility? The Fable of the 3 Neighbours«)

.

I would argue that none of these traits can be learned once a person reaches adulthood. At that point, their potential to be an outstanding investor in the future is already determined. It can be honed, but it cannot be developed from scratch because it has to do mostly with the way your brain is wired and the experiences you have as a child. That doesn't mean that financial education and experience in reading and investing are not important. They are fundamental to getting into the game and staying in the game. But those things can be copied by anyone. The seven traits above cannot be.

Value Parters (VP) is a Hong Kong-based fund manager that we have known very well for many years. We have visited them personally on several occasions and have been investing in some of their funds for years. VP is the only Chinese fund manager listed on the Board of the Hong Kong Stock Exchange. We will now translate and comment on the reflections of its Co-Chairman, Louis So, The report on the economic effects of the pandemic in China a few months ago.

.

It would not be an exaggeration to say that the onset of the COVID-19 pandemic has led to the worst global economic crisis since the Great Depression of the 1930s. The combination of a demand shock, a supply-side shock, a financial shock and political upheaval has sent markets around the world reeling.

.

While no one can predict how the world's economies will emerge from the crisis, some experts are making educated guesses based on current economic data. Whatever happens, a post-COVID-19 environment is going to be very different from anything in the past. China will certainly outperform other markets, although it may not sufficiently boost the growth of the global economy.

,

Therefore, there will be a higher degree of government intervention, more money printing, very low interest rates and a much bigger asset bubble. This asset bubble will in turn widen the gap between rich and poor, and this will lead to social instability.

.

At some point, this system will collapse. In the future, politically speaking, left-wing politicians will gain popularity and gain support. Then we think that some redistribution of wealth will occur.

,

While the last 50-70 years have seen a period of global wealth accumulation, there were also periods when wealth was distributed. Such events occurred because of wars, or because governments allocated resources differently. That is something we can expect to happen in the world over the next five to ten years.

,

On the consumer side, there will be a contactless economy, consisting of a boom in e-commerce and online entertainment. VP has positioned its portfolios to benefit from this trend.

,

Companies will have to rethink their business models. In the past, just-in-time inventory management was the norm. But now companies will have to think about whether they need to build up cash reserves for inventory and supply chain management. That will also change the mindset of business leaders.

,

COVID-19 could escalate a potential crisis of capitalism and the free market. The challenges may cause capitalism to falter. Providing a much better social welfare system could be a potential solution. Although it may affect the economic growth of countries, it will create a much happier environment for society.

,

This pandemic has not changed VP's strategy much. The company is still tapping into what could eventually be the world's largest market: China. Savings are high in this country. We need to participate in this market as investors if we want good returns.

,

The relationship between China and the US will get worse before it gets better. China is not dependent on exports and does not rely on other countries to grow its economy as it used to. This will drive China into isolation for a while. But China and the United States will have no choice but to become friends, partners and allies again. Perhaps the Trump-Biden swap will bring this about.

,

China will come out ahead. And it will emerge from the pandemic ahead of other markets.. The predictions are based on recent economic data from China showing a V-shaped recovery trend at both the macro and consumer levels. It is highly likely that China will take advantage of the pandemic to accelerate its growth spurt and economic leadership of the world.

,

With data available just after the March crash, year-on-year figures showed that fixed asset investment fell 9.4 per cent in March, but increased to a 3.9 per cent positive gain in May. Retail sales were down 15.8 per cent in March, but only down 2.8 per cent in May.

,

Even a business like electricity production showed a year-on-year decline of 4.6 per cent for the month of March, but returned to 4.3 per cent growth in May. The same pattern can be seen on the consumer side. Products such as cosmetics, furniture, automobiles, tobacco and alcohol experienced a similar V-shaped recovery.

.

The data show an economy that is steadily recovering from the pandemic. So there is every reason to be optimistic. China is in a much better position to cope with this crisis than the West, and the FIFO rule is being met because of good virus control. China is benefiting from a large middle class that has one of the highest savings rates in the world. The country had a savings rate of 47% in 2017 and ranked third out of 170 countries monitored by the World Bank.

.

So China is now a fairly self-sufficient economy, and this has helped it to cope with the pandemic. China has innovation, production, distribution and also the end consumer within its borders. Therefore, the country is experiencing less supply-side trauma than other countries.

.

China also has a much more modest stimulus programme than other countries. While the US is pumping out a huge stimulus programme consisting of about 18 per cent of its GDP and rising, China's stimulus package is less than 5 per cent of its GDP.

.

We are quite optimistic about China. It is still on track to become the world's largest economy by 2030 or sooner. Therefore, several investment themes will be the main drivers of growth, including consumer upgrades, a growing number of high-net-worth individuals, technology and the explosion of 5G. There will also be more individuals seeking higher education, along with the development of online service platforms and a growing healthcare sector.

.

China is too big to ignore at the moment. It accounts for 16 per cent of global GDP, which means we can look at it as an asset class in its own right.

.

So do not expect China to slow down any time soon.. There are many factors to consider, such as the relationship between China and the US, and a possible resurgence of the virus. Only time will tell. But things looked much better in the second half of 2020 and so far also look much better for 2021 than in the other economic powers.

Film buffs will have recognised the famous line from the title of the article. In one of the most difficult moments of the Apollo 13 odyssey, the Chief Engineer in the control room acknowledges aloud that they are facing what will be the toughest moments in NASA's history, to which the engineer played by the great Ed Harris replies: «...the crew will have to face the toughest moments in the history of NASA.«With all due respect Sir, I think this is going to be our finest hour.«one of the most legendary lines of the film, along with the well-known «Houston, we have a problem».

.

You may be wondering what this film has to do with investments and financial markets. Well, as you may know, it is common for fund and managed account managers to write newsletters and notes to investors in the worst moments of the markets. In them they usually report their view of the crisis situation, try to justify the losses, reason their strategies by reaffirming them or by giving a change of direction, etc. All this in an attempt to reassure investors, thus trying to prevent them from withdrawing their trust - and money - from their fund managers. Such communications abound and are almost obligatory for any self-respecting manager, since it is in difficult times that the relationship between managers and investors needs to be strengthened.

.

This time, however, our attention has been drawn to the letter written by one of the fund managers that form part of the group of funds and asset managers whose due diligence we are currently carrying out at Cluster Family Office, the identity of which you will allow us to reserve for our Clients. The curious thing about this letter, the title of which is the aforementioned phrase from Apollo 13, is that is not addressed to its investors, as would be expected, butto the managers of the companies in which they are invested. We consider this to be extraordinary, as it is not at all usual to address them publicly in times of stock market crisis, let alone in the terms we translate below from the original letter:

«With all due respect Sir, I think this is going to be our finest hour.»

Dear Partner,

We are all going through very difficult times, both in the health, social and economic areas. It is true that we are not «inside your company» and we are aware of our limitations, but we believe that our vision and perception of the situation can bring you something. Our company manages assets for long investors from all continents, with a high sense of fiduciary service and excellence. We have held 483 online meetings in the past few weeks with domestic and foreign companies, always seeking a better understanding of their business prospects in the current environment. If you in your company need any contact with any of the companies we have relationships with, please do not hesitate to let us know, we will be happy to help. At this time, perhaps a view from 30,000 feet, from a team that is studying various international cases and businesses, may be useful to you. In addition, as investors and partners in your business, we would like to tell you the following:

.

The number one priority at this time is to ensure the health of your professional teams and family members. The emotional stress you are all under is enormous, and being there for your staff and their families at this time is extremely important. Be transparent, empathy goes a long way and reinforces the meaning and mission of each employee.

Regarding the coming quarters, all company managers, owners and investors have uncertainties and questions. You are not alone. Visibility for this year is very low. Liquidity is king. We all know that the economy will weaken due to rising unemployment. However, we do not think that everything will be different. There will always be demand for good services and products at good prices. The main needs of consumers will remain the same. There is no need to panic or make ill-considered decisions.

Major crises often precipitate innovation. Trends that already existed will accelerate. We are seeing some companies adapting more nimbly to online commerce and creating digital tools for their businesses. We are excited by the adaptive and innovative capacity of companies and entrepreneurs in our country. We can offer you practical examples from inside and outside our borders.

These are times when it is interesting to rethink structural costs. But do not forget that people are your main asset. We don't want to be proselytising, but remember the time and effort it took you to find and train your professionals. If possible, don't lose your high potential and don't cut the pay of the key players in your company. And if you do, remember that the same cuts should also be applied proportionally to the top management.

In difficult times like these, social, environmental and corporate governance (ESG) marketing and practices may seem superfluous. This is understandable, of course, for companies struggling to stay afloat. However, we believe that ESG practices are even more important now. Consumers, investors and professionals will place an even higher priority on companies that take care of environmental, social and corporate governance practices. So don't forget your shareholders. The way you treat your suppliers, customers, employees, the environment and the community around you will be remembered for a long time to come. The old saying «treat others as you would like to be treated» has never been more relevant.

If possible, you should not only focus on a defensive business position, but it is also time to go on the offensive, as there may be excellent opportunities out there. That company you have always wanted to acquire, or that professional you have always wanted to recruit, may now be more open to talk and listen to your offers.

Stay focused. In times like these, anxiety makes us want to act hastily. Listen to everyone, but don't change too much or burden your team with new and unnecessary requests. Board members tend to ask for a lot and offer few suggestions at times like these. Maintain rigour.

Finally, we would like to emphasise our long-term vision. Do not sacrifice the long term to satisfy short-term investors.

There is a scene in the film Apollo 13 that is worth remembering. The mission is going through a very difficult moment. The «boss» says to his engineers: «This will be Nasa's worst moment”, and one of the engineers (Ed Harris) responds: “With all due respect sir, I believe this will be our finest hour! Moments like this define great leaders.

Good luck! Take good care of yourselves and remember the instructions given in case of emergency on all flights: Put on your oxygen mask first and then help the people sitting next to you to do so. If you are not well, it will be more difficult for you to take care of your families and your equipment.

.

You can count on us. Best regards.

https://youtu.be/OlR17RaMVmM

Not bad, is it? Unfortunately, not all fund managers take such a long-term, protective view of good business. Most of them are just trying to avoid being embarrassed by their benchmarks, a task in which they fail more than 90%. You can find plenty of articles and statistical studies on the ineffectiveness of most active managers by googling (here, here o here). But it is not impossible to find active managers who justify their fees by outperforming their indices in a convincing and sustained manner over time, especially if we eliminate the barrier of 10% of funds marketable in Spain and we can invest freely in the 100% of funds existing all over the world, as we have explained above. here o here.

.

Whether we are entrepreneurs, self-employed or employees, we can all be good investors in difficult times like these. All it takes is a few simple tips, which are otherwise very difficult to follow. Buy when others sell, sell when others buy. And to do so best possible way, outperforming the rates, as the managers who have written this note have been doing for more than 14 years.

,

Now, and for a couple of months now, So it is time to buy and not sell, at least until the shoeshine boy, the lift operator and the neighbour in the 5th floor 2nd floor come back to boast about their investments in the stock market and, of course, are vaccinated.

After the much read and commented in networks «The lies of the Spanish government and health authorities about the coronavirus«In the third instalment of articles dedicated to the global crisis caused by the SARS-Cov-2 coronavirus and Covid-19 disease. In our first article entitled «Realistic coronavirus figures and the opportunities of an unfortunate crisis»We were already anticipating this: The effects on the entire world economy are devastating in the short term. But only in the short term since the infection has a clear expiry date, Unlike other geopolitical, military or social conflicts, which also generate panic in the markets. Y It is this temporality that should awaken the good investor in us and change our fear for the famous greed that Buffett and other investment greats recommend when the rest of us panic.

.

In this pandemic, which is now beginning to sweep the West, the investment opportunity is one of those that are often called once in a life time, This is one of those rare occasions in the course of a lifetime of investing. This is because, although there is always room for doubt due to imponderables that can complicate scenarios, business activity will probably recover to pre-pandemic levels in the medium term at best. Obviously these imponderables include, for example, a mutation that makes the virus more resistant and/or deadly, war conflicts that add more instability to the world order, or other health crises that could arise and coincide in time with the current pandemic. But if none of these things happen, the recovery in the tone of the economy will be no more than a few months. a couple of quarters, And what should a few quarters mean on the horizon for a good investor? Nothing.

.

Therefore, it's time to go shopping (or hunting, as Buffett would say) and take advantage of the fact that the results of countless good companies around the world are going to be temporarily and exceptionally bad. Because the fall in profits and turnover will not be due to poor business performance but to a lull in global economic activity that is as exceptional as it is temporary. If we talk about airlines, we will find some at half the price of last year. If we look at the energy transport sector, the falls and fluctuations have been insane. And what can we say about the China's health sector, The winning horses, for example, have an exceptional horizon ahead of them because they will be the almost exclusive providers of pandemic and post-pandemic material on a planetary level.

.

But how to find these pearls with such a promising future? Decades ago we learned that it is much more efficient to select the best international fund managers than trying to analyse the best companies on the planet. The knowledge that good local management teams will have of the best companies in their respective countries (Vietnam, India, Brazil, China, etc.) will always be infinitely superior to ours or to that of any multinational management company that tries to make its selection through a manager located in London or New York, even if its forefathers were originally from those countries. We would therefore be well advised to invest our money now in those investment funds who have local and comprehensive knowledge of China (or the specific health sector as mentioned above) or any other country.

.

And those good local managers will not only choose good businesses, but also cheap ones, with bright prospects for recovery. Because if we think that a company may be losing a whole quarter of its turnover due to the pandemic, for example, and we buy it now at a panic price, its growth prospects in terms of turnover over the next 4 or 6 quarters will be spectacular. In other words, we will be investing with Value criteria but with a Growth potential that is as exceptional as it is profitable. If we add to this the fact that we will be selecting companies whose business is based on taking advantage of growing economies and demographics such as those in Asia, the tailwind will further boost our future profits.

.

As the image on the left hand side of the Cobas March Newsletter, It is now, when our neighbours in the 3rd 5th are beginning to realise that perhaps the coronavirus is not just a simple flu, that we should invest without fear and give free rein to our good investor's greed. Now, when our less informed friends and acquaintances are alarmed by the market crashes that are all over the TV news. Just like the lift man who recommended shares to Groucho Marx. in this essential book, or Rockefeller's shoeshine boy invested in the stock market. In other words, when the less informed panic about the coronavirus epidemic and the markets go into a tailspin, it is the most appropriate time to invest in the quality assets that have been exaggeratedly depreciated in recent days. It is perfectly possible, as we have already said, that things will get even more complicated, and that the investments we make today will temporarily lose an additional 20% or 30%. But if they do, and our investments are of quality and made with the good judgement of the best fund managers on the planet, it will be for a very short time. On the other hand, if we remain fearful out of the market, it is likely that we will not see that additional 20-30% fall but a sharp recovery and miss out on much of the upside, having blown this one. «once in a life time».» opportunity.

.

We know that many will read this article but will not follow the recommendation, as it is easy to understand that you have to buy when everyone else is selling, but it is difficult to dare to put it into practice. And thanks to the majority who won't dare and those who don't even agree with our arguments, a few of us will be able to make substantial profits in the coming years.

Financial analyst and writer John Mauldin has christened the beginning of 2020 as the decade in which we will live dangerously. In this article we will translate and comment on the arguments and analyses published by this author under the same title. Readers will be able to see the coincidence in some aspects with respect to what we have been saying in the past. publishing on this blog for more than 4 years.

.

Hyman Minsky taught us that stability, perhaps because of the abuse we tend to make of it, sooner or later leads to instability. But that abuse is as unconscious as it is harmful, and we humans like to dabble in concepts like «reasonable», «manageable», «conservative» or «prudent». That's why we feel safe seeking more and more performance until we go too far to avoid disaster.

.

To think that somehow central banks are capable of eliminating recessions and risk is crazy, despite the fact that most investors fall into this trap time and again. Yes, it is true that, as we have said many times before, with infinite liquidity no one is insolvent and therefore their debt is virtually devoid of default risk. But at some point gravity will do its work again and the insolvent will collapse as God -or the elementary fundamentals of economics- commands.

.

Debt seems harmless at first. And with sufficient cash flow, capital repayments are not a problem, let alone ridiculous interest rates. Besides, debt will be used wisely and profitably to increase growth, won't it? Well, it won't, because human nature always leads us to denaturalise goodness, and lenders will insist ad nauseam that we get into debt far beyond what is necessary for economic growth, and we start getting into debt simply to consume today what we should be consuming tomorrow. So the goodness of indebtedness is corrupted along the way.

.

Personal debt, though often excessive, is not the most serious problem. Corporate and public debt are the main challenge for which Mauldin predicts a dangerous decade ahead. And let us not forget that all this public and corporate debt ends up as personal debt, since most of us are after all taxpayers, shareholders or both.

.

The calm on the markets, however, may last a few more years (2020, 2021, 2022, 2023...). But beneath the surface of the central banks' cheerful free bar, the pressure is increasing every year. Slowly, almost imperceptibly, but at some point it will explode.

Ben Hunt, a personal friend of Mauldin's, has developed the concept of the «The Long Now«. Something like an endless today that swallows up the income of the future. Or as Hunt defines it: «Everything we bring to the present of our future and that of our children».». The Long Now is the realisation of the stark reality of Fiat money or fiat money, without anchorage to any tangible and finite value. In other words, trust in an abused and uncontrolled system is what makes us choose bread for today. And that system is the one that tells us that inflation is virtually zero, that wealth inequality, low productivity and negative savings rates are just a circumstantial fact of life. We are also told that we must vote for ridiculous candidates to be a good and politically moderate citizen, that we must buy ridiculous funds and stocks to be a good investor, or that we must take ridiculously unpayable loans to be a good parent or child.

.

Debt is future consumption brought into the present. But to pay that money back we or our heirs will have to consume less in the future, unless our economy grows sufficiently. And that is the problem, that today's debt is not being used to gain growth but we live in a world where the economy is driven by consumption. Furthermore, Ben Hunt observes that society tends to procrastinate in solving problems. We tend, with surprising skill, to postpone the inevitable (rather than avoid it indefinitely). And when it comes to over-indebtedness, it is also a three-way game, as neither debtors, creditors nor regulators are in the mood to end the game. It is in the interest of none of them to recognise that the debt is a dead letter and unpayable and to write off the losses on their balance sheets. The traumatic consequences of recognising insolvency and the resulting bankruptcies.

.

A game of Monopoly would never end if the bank refinances the debts of the players infinitely.. The million-dollar question is, as a spectator of this distorted game of Monopoly, to which player should we lend our money in exchange for reasonable returns? To the players who owe astronomical amounts to the banks, but who nevertheless continue to play and play? Or to the few players who owe nothing and are meritoriously sustaining themselves in the game by their own means? An infinite game would make no sense at all and would call into question the very market system we have known since the beginning of civilisations. Therefore, at some point not necessarily far away, the game will end and there will have to be losers. Many of them.

.

That said, Mauldin predicts that we will be comfortable and relatively safe along the way. That at any given moment, analysts will look at the data and think we have avoided the worst. We will have some passing recessions and some financial crises, but they will seem «manageable» when we get into them. And we will indeed come out of them. But what we will not see is the magnitude of the expansion that the system will need to continue to finance our debt, which will continue to grow and grow throughout this Long Now. So the debt burden will become heavier, and there will come a time when it will be unsustainable even for this trust-based system of infinite money.. Then the fan will blow more than just air in everyone's face.

.

Mauldin defined the inevitable process in 3 phases: An initial seemingly manageable instability, perhaps initially caused by high yield debt, but easily contagious to other parts of the system that are also unstable. Secondly, a drying up of liquidity that will force banks to reduce lending, thereby reducing the capital available to productive businesses and thus reducing economic growth, leading to recession. This second episode may be recurrent, with drying up of funding and intermittent renewed flows based on emergency measures by central banks, but increasingly unmanageable. And finally, a third phase of global political instability, where artificial intelligence - among other factors - will make a lot of intermediate jobs redundant. The shrinking voter will vote for governments that promise to maintain a welfare state that provides for his or her needs and comfort as in past decades, and those governments will of course raise taxes (remember that infinite liquidity dried up in phase two) to the point of economic suffocation, deepening the recession. Mauldin does not expect to see the start of this process until the second half of the new 20s.

.

Perhaps the whim of fate is leading us into another decade of the Roaring Twenties like 100 years ago. But a new Great Depression will hardly be mitigated by central banks with depleted ammunition.

In the EU more and more alternative investment fund managers are becoming more and more -are governed by the AIFMD (Alternative Investment Fund Managers Directive). The alternative investment nomenclature includes all European investment vehicles that do not meet the requirements to be considered UCITS (Undertakings for Collectible Investment in Transferable Securities). If, in addition to being non-UCITS, their managers comply with the above-mentioned directive, they will be considered AIFMD funds. UCITS funds are those usually sold by Spanish banks to their retail and private banking clients. However, it should not escape anyone's attention that on the other hand alternative investment funds are the funds of choice for major investors worldwide. In other words, although for the vast majority of Spanish retail and private banking investors their investment universe is limited to the 10,000 or so UCITS funds marketed by banks in Spain, for professional investors and the world's wealthiest individuals, alternative investment funds and hedge funds make up the vast majority of their portfolios. In other words, most of the world's best funds in history (some even closed to new investors as they do not accept any more money) are not UCITS and are not marketed in Spain, but alternative management funds, which can be invested in jurisdictions that are much less restrictive than Spain.

.

Let us remember that there are more than 100,000 investment funds in the world. And the million-dollar question is, how can a Spanish retail investor access this universe of 90,000 non-UCITS funds that are not marketed in Spain? The answer is not so simple, as it is not enough to open an account in a bank abroad. There are additional difficulties The most common problems encountered by the ordinary Spanish investor, such as taxation, which is linked to the jurisdiction where the fund is domiciled, are as follows. As we will see below, funds do not necessarily have to be domiciled in the same country as the management company. Most of the world's alternative investment management companies, domiciled in the USA, Asia, etc., have their headquarters in the same country as the fund management company. have local funds for investors in their own country, but they also have replicas of these funds in offshore jurisdictions for large international investors.

.

The reason why fund managers create these mirror funds or feeder funds for international investors in offshore jurisdictions, where taxation for the investor is zero, is not so much so that they do not pay taxes, but so that they are not harmed by the taxation of the country where the fund manager is located in addition to their own taxation. In other words, if they invest directly in local funds, they would be subject to double taxation: That of the country of origin of the fund manager and that of their own country where the investors reside. It is true that in some cases such double taxation could be fully or partially recovered if there is a treaty between the two countries to avoid it, but not in all cases. Moreover, even in those cases where such treaties would be beneficial, it is still an inconvenience that adds to the investor's fiscal discomfort and uncertainty.

.

This is why large international investors often use offshore and non-EU mirror funds, mirror funds or feeder funds domiciled offshore and in non-EU countries. OECD to invest in funds from American, Asian, etc. fund managers. In this way a Spanish investor who invests in a US hedge fund, for example, should not be taxed in both the USA and Spain, but only in Spain, without the need to resort to bilateral treaties to avoid double taxation.. The problem is that Spanish taxation penalises investors resident in Spain who invest in funds domiciled in these offshore countries, where the aforementioned replicas aimed at international investors are usually located (we will explain later how this penalty can be avoided).

.

Let us look at an example of a benchmark fund manager with the aforementioned duplicity of funds, aimed at investors according to their country of origin: The manager of the legendary fund Medallion (already closed to new investors since 1993) is the prestigious Renaissance, of which we have already we spoke at length and explained our visit to their bunker in this article. Well, this fund manager, like so many other world leaders in management, has funds for domestic institutional investors (US-investor), domiciled in the USA; and funds domiciled in Bermuda for foreign investors (non-US investors). As we have already said, the distinction is made so that the international investor does not suffer the taxation of the funds domiciled in the USA and so that they only have the effects of the taxation of the respective countries where each investor resides.

.

However, there are also other reasons for fund managers to domicile their funds for large international investors in non-OECD/offshore jurisdictions. In addition to avoiding double taxation for the international investor and saving taxes for the fund manager itself, those jurisdictions do not entail any restrictions in terms of trading platforms or geopolitical vetoes when it comes to underwriting funds. For example, most international investors would find it very difficult to subscribe to funds in countries such as China, Korea, Indonesia, the Philippines, Vietnam, Russia, etc. In some cases because of political/economic sanctions imposed by certain countries, and in others simply because the markets are still technically, politically and/or regulatory unwilling to allow international money into their domestic funds.

The fact is that, whether by hook or by crook, large international investors use these channels created ad hoc for them. And either they are not penalised fiscally by their respective countries if they invest in these jurisdictions, or they have investment vehicles and structures that legally exempt them from these penalties. The loser, as always, is the ordinary Spanish investor, who is condemned to invest in the UCITS environment and the few retail hedge funds domiciled in Spain, in short, condemned to the fish that our banking system sells them.

.

It is true that some American or Asian fund managers, eager to attract retail funds from the European market, set up their own UCITS vehicles in Ireland or Luxembourg and register them for marketing in various EU countries. But unfortunately they are often not the brightest but the most voracious.. And they do not seem to mind giving up much of their alternative know-how and assuming the restrictions on portfolio concentration, liquidity, restriction of hedging and/or restriction of operational freedom in general that the UCITS label entails, in exchange for inflows of money from small European investors. The result is that these UCITS funds are very different from the original ones and with much lower returns.

.

Therefore, we are going to focus on the solutions so that a smaller Spanish investor can access the best American and Asian hedge funds on the planet without suffering, on the one hand, double taxation for investing in their funds aimed at local investors, and on the other hand, the tax penalty for investing in their feeders or offshore mirror funds aimed at international investors. There are two absolutely legal and transparent ways of doing this:

This second option solves in one fell swoop the 3 problems encountered by the ordinary Spanish investor:

.

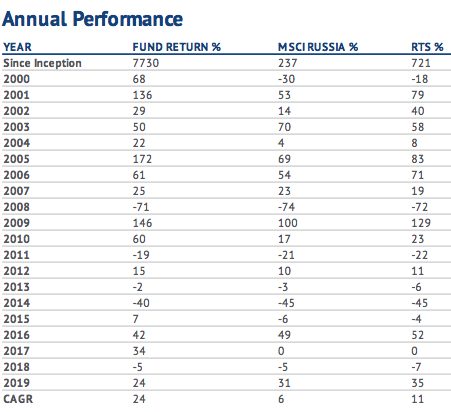

First of all, the first insurmountable problem for most investors is the minimum investment requirement. And the fact is that The best funds in the world often lack retail classes and require prohibitive minimums of $500,000, $1 million or even $5 or $10 million or euro equivalent. Moreover, without going any further, funds such as those of the aforementioned Renaissance not only require a minimum investment of 5 million, but they also select the institutional investors they like the most, and can be rejected even if they exceed this minimum investment (Cluster Family Office had to pass this filter to be approved as investors in Renaissance, considered the best fund manager in the world for several decades). Well, these AIFMD funds of funds that contain large institutional funds 125,000 minimums are usually as low as 125,000 eur.

.

Secondly, it avoids the tax penalty that offshore investments suffer from, as explained above, as they are funds domiciled in Luxembourg and under the AIFMD label. Therefore, Spanish regulation and legislation considers their capital gains to be as deferrable over time as those of any Banco Santander or La Caixa fund.

.

And thirdly, by investing in them from accounts in Luxembourg banks, it avoids the restrictive reading of the Spanish regulator to qualify as a professional investor, This makes it de facto impossible for ordinary investors to subscribe to these funds from Spain. These Luxembourg funds are marketed exclusively to well-informed investors (or qualified or professional investors, depending on the nomenclature of each jurisdiction). In other words, a Spanish retail investor cannot invest in them from a bank in Spain, as alternative management is considered a complex product, even though it bears the European AIFMD stamp. Therefore, according to Spanish regulations, these AIFMD funds can only be marketed in Spain for professional investors, which implies very restrictive requirements that are impossible for ordinary investors to comply with. Moreover, the only way for a retail investor to explicitly request to renounce his status and be allowed to invest in these funds from Spain as a professional is to comply with the following requirements at least two of the following requirements according to Spanish regulations:

.

That the client has undertaken transactions of significant size in the relevant market in the financial instrument in question or similar financial instruments, with an average frequency of 10 per quarter over the previous four quarters.

The size of the customer's portfolio of financial instruments, consisting of cash deposits and financial instruments, exceeds EUR 500,000.

The customer holds or has held for at least one year a professional position in the financial sector that requires knowledge of the operations or services envisaged.

.

It should also be noted that it is the Spanish marketer or bank itself that must check and demonstrate to the regulator that these requirements are met, and that it will obviously prefer to sell this client its usual catalogue of own and external retail funds with its juicy implicit or explicit fees, rather than consider him eligible to buy alternative funds that are outside its marketing agreements. It is obviously de facto impossible for most Spanish investors to access such funds from accounts in Spain.

.

By contrast, Luxembourg's regulation is much less restrictive and much more friendly with alternative investment funds for junior investors, as it is sufficient to be considered as a «well-informed» investor. The regulation reads as follows:

.

To qualify as a «well informed» investor you must be either:

An Institutional Investor

A Professional Investor

Any other investor who has confirmed in writing that they adhere to the status of a «well informed» investor and who:

Either invests a minimum of EURO 125,000 in the specialised investment fund;

Or who has an appraisal from an EU bank, an investment firm or a management company certifying that they have the appropriate expertise, experience and knowledge to adequately understand the investment made in the fund.

.

In other words, that 125,000 is sufficient for any investor to apply to be considered as an investor in Luxembourg. well-informed and therefore eligible to invest in an AIFMD fund. It is therefore advisable to open accounts with Luxembourg banks in order to be able to invest in these funds. Another thing is that banks require a minimum amount to open accounts for new clients, which is unfortunately often the case. That is why it is also essential to work with a professional who has a sufficient number of clients with these banks, i.e. who has influence on them to persuade them to accept new clients with accounts as small as 125,000 euros.

.

In short, thanks to Luxembourg's less restrictive legislation, any Spanish investor with a minimum of 125,000 euros can invest in a completely legal and transparent manner in AIFMD alternative funds that contain the best alternative funds and hedge funds in the world, despite having very high minimums and being domiciled in jurisdictions only suitable for large institutional investors with complex investment structures and vehicles.

.

The drawback obviously is that a fund of funds is commission on commission. It is therefore necessary to look very carefully at the historical NET returns obtained by the fund, and whether or not these are clearly higher than those obtained by each individual in their UCITS investment portfolio and Spanish banking universe..

.

.

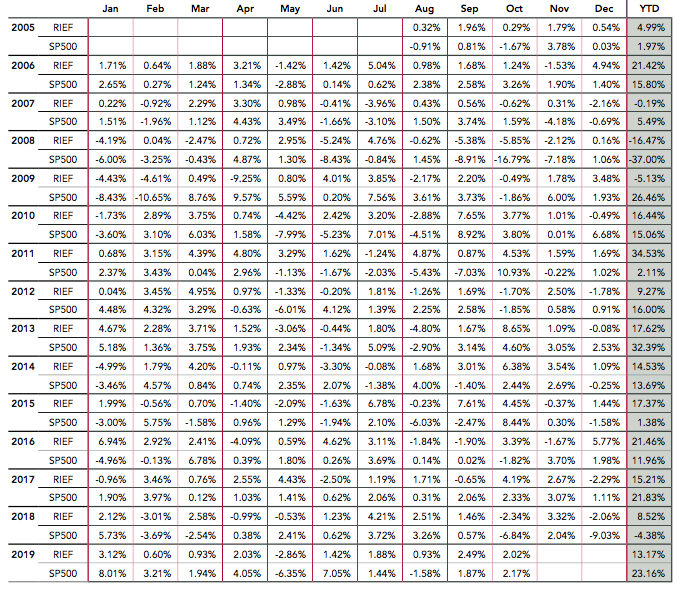

In the tables above you will see the historical performance of 3 world-renowned hedge funds - which some of you may recognise - with minimum investment levels of half a million, one million and 5 million. And finally, below these lines, the performance of a Luxembourg fund of funds AIFMD, therefore accessible to any investor. well-informed with an account in Luxembourg from $125,000, containing a dozen international funds (including the 3 above) plus a few listed stocks (Berkshire Hathaway...), so that you can compare it over the long term with your own portfolios.

.

.

And finally, for those who still think that the limitations of the UCITS environment are worth it because of the possibility of investing only in transferable funds, here is an article entitled «Is it worth holding on to an upgradeable investment in exchange for further deferring accumulated capital gains?«. The results of the calculations you will find in that article are devastating, as just by improving the return by 0.21% per annum, the benefits of 20 years of capital gains deferral are outweighed by the average return of the last quarter of a century. More importantly, once the sold portfolio has been taxed, in addition to being free to invest at a higher yield in any hedge fund in the world, you can also defer taxation forever, either with your own investment vehicle or through a fund of funds AIFMD, as explained in points 1 and 2 above.

.

Having said all this, for those who do not have that €125,000/$ minimum, there are honourable exceptions in the limited and mediocre UCITS environment. World-renowned Spanish value managers such as AZ Valor, Magallanes or Paramés himself (although his COBAS has yet to make headway) may be the best way to invest a small portfolio in an easy and simple way.

Recently the newspaper Public has interviewed several Spanish sportsmen and women who decided to study at universities in the USA to perfect their careers, both academic and sporting. This drain of talent is not only being suffered by our country at a sporting level but also at an academic level, as any student of medium or medium-high level has a place in the American university system.

.

Let's look at the motivations that lead sportsmen and women and «simple» students to pursue their careers at American universities. For sportsmen and sportswomen, the fact of studying there means obtaining a university degree that they would most probably not get here, as it would be very difficult for them to combine their sporting career, training and tournaments with classes and exams. The result is that very few Spanish athletes have a university degree when they finish their more or less successful sporting careers. In the USA, sporting success is not only compatible with, but necessarily goes hand in hand with the university world. The compatibility of training and competitions that will lead them to professional sport with classes, studies and exams is total and absolute. In addition, the facilities, sporting level and quality of coaches in the sports areas of the university system in the USA is a dream, as their budgets are light years ahead of those of any sports club in Spain, unfortunately.

.

In short, a 16-18 year old athlete who decides to stay in Spain has only one card at stake for his or her future: whether to be sufficiently successful as a sports professional or to be relegated to being, for example, a mere coach without a university degree. In the best case scenario, they will have to retrain academically when they throw in the towel on their professional career, late and badly, in order to get a job. On the other hand, an athlete who goes to an American university, even if he or she is not successful enough as a professional, will at least have a university degree (often linked to the world of sport) that will allow him or her to make his or her way in the post-sport world with the same possibilities as any other graduate. In addition, you can even obtain your masters or postgraduate degrees while continuing your sporting career.

.

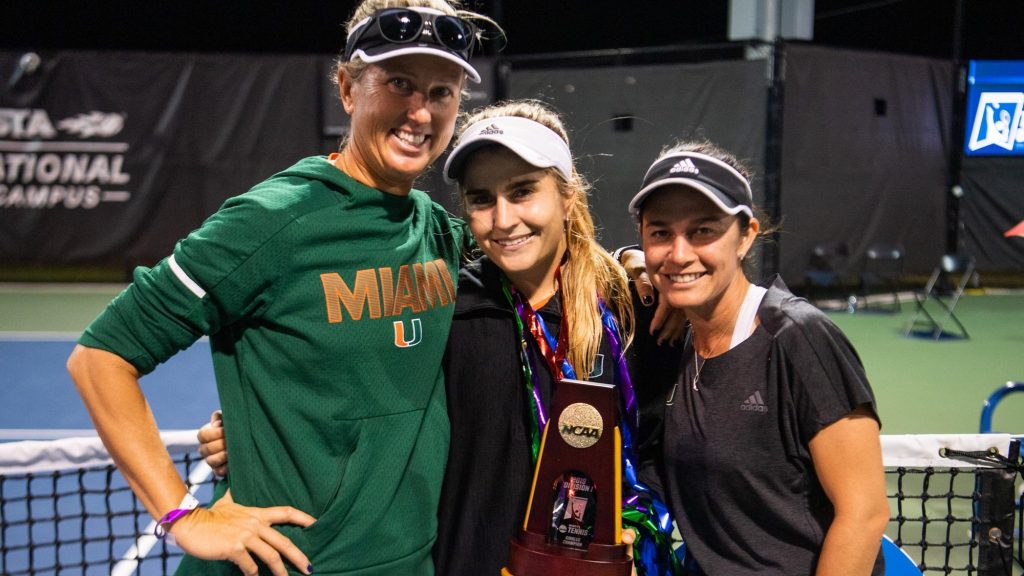

Estela Pérez-Somarriba from Madrid, a student at the University of Miami, and NCAA champion (the most competitive college tennis league in the world), explains it perfectly in the interview:

.

“I was right to look at the long term. I wanted to play tennis professionally, it had always been my dream and it still is. But when I finished high school, I started to weigh up the academic, tennis, economic and personal aspects. I didn't know if I wanted to live in Madrid all my life, I needed to mature, I couldn't afford to travel and pay a coach to take the professional leap, and in the United States I could combine sport with a career”.

Estela is studying Economics and Sports Management, and she couldn't be happier with her decision. Her goal now is to jump to the women's professional circuit (WTA) as soon as she graduates, which she will also do on a scholarship from start to finish by the university itself:

“The physical and medical resources, the facilities, the advisors and teachers help you a lot. My day-to-day life is tough, but we are top-level athletes and if you want to be the best in your sport and get a degree, it is always going to be a challenge. But here I have a lot of facilities that I didn't have before.

But it is not only athletes who have their way open to the university world in the USA. Every day, more and more students who do not play any sport are studying at the more than 2,000 universities across the country. And the fact is that prices are not so abusive as a priori many families might think. Nor do theythe academic standards required are so high.

Any student of average level has a place in an American university. The prices do not have to be higher than the costs of a private Spanish university. And living expenses, i.e. flat and meals, within the university campus itself cost the same as sending our children to study in Madrid, Barcelona, Seville, Bilbao or any other Spanish city. You can see the details of the costs and price ranges in our article: «Can I send my children to study at a university in the USA?«

.

Furthermore, let's not fool ourselves, a degree from an American university will open more professional and employment opportunities for our children than a Spanish degree. Whether they return to Spain to look for work, stay in the USA or go to live in any country in the world, having a university degree from any American university under their arm will make a difference for life. What better inheritance can we leave them than that?

.

Although it may come as a surprise to many, the process of preparing for admission to an American university must be done at least one and a half years in advance. and appropriate expert advice. In other words, as we have already explained here, The time to start the process is between the end of the 4th year of ESO and the first half of the 1st year of Bachillerato.

In this Público article you can find other stories of Spanish sportsmen and women who cleverly decided to develop their careers in the USA.

.

In short, families with children aged 15-17, whether or not they are athletes, whether or not they are bright students, explore the academic and scholarship possibilities offered by the American university world. It will make a difference in their lives, and yours.

Our developed society seems to be frolicking in the sand by the seashore, totally oblivious to the tsunami that is crashing over us. This great wave that will sweep away everything we know is none other than the disruptive change that is already being generated by new technologies, and especially by advances in artificial intelligence (AI). The changes in society that we saw during the industrial revolution or the global implementation of the internet were child's play compared to what is coming our way. Technological and personal adaptation skills with constant training are already what our parents' and grandparents' literacy was. Without such skills and training, our old age, and more seriously, the lives of our children, are condemned to a marginalisation comparable to that of the illiterate of yesteryear.

.

The latest OECD study (Skills Outlook 2019) is devastating. It warns that the percentage of the population in Spain with the capacity to adapt to technological progress and the digitalisation of tasks is only 23%. These figures include people aged between 16 and 65, so if we think beyond the age of (pre)retirement, the scenario is even more terrifying. More than 3/4 of our society will be marginalised in the face of the technological advances that are already being implemented in the workplace. The figures improve slightly in countries with more advanced educational and social systems, such as Norway, Sweden, Finland, New Zealand, etc. But imagine the figures that could come out of less advanced societies such as those in Africa or deep Asia or South America. The extinction of jobs analogue is already and will be overwhelming.

.

But that is only the tip of the iceberg, since the artificial intelligence (AI) is a disruptive breakthrough as momentous as possibly the mastery of fire by early hominids. The AI revolution will eliminate not only the remnants of analogue jobs in the less developed corners of the globe, but also a good part of the digital ones. Until our generation, society and the global economy have been able to cope with, adapt to and take advantage of technological advances despite initial fears. We remember the trade union protests in the industrial revolution, when machines began to replace workers, who had to readapt to other work tasks. Another example would be digital photography, which overnight wiped out giants such as Kodak and their film developers. Or streaming content such as Netflix, HBO, Prime Video, etc., which are forcing the Hollywood empire itself to reinvent itself or die. The same will soon happen with other disruptive changes such as mobility in self-driving cars and a host of imminent changes that will make our society unrecognisable when our children try to enter the world of work. It is true that civilisation has been sufficiently assimilating these advances and more jobs have been created than destroyed, as economies have grown even faster than the population. But the speed of technological advances is exponential, and especially artificial intelligence will overwhelm society without having enough time to react and readapt as it has done in the past.

.

There is no antidote to the incoming tsunami. We continue to fiddle absentmindedly in the sand, wondering whether our children should learn English, Chinese or German, while they go to the university around the corner to get a degree in a subject for which we delusionally think they will have no shortage of work. Unfortunately this will not be the case. Experts warn that our children will have to adapt to work in professions that do not yet exist today and that no less than 75% of today's professions will cease to exist. The million-dollar question is what we can do to be as well prepared as possible for these radical changes. But the honest answer is that the disruptive advances of AI are so brutal and imminent, there is seemingly nowhere to take cover. The tsunami is already upon us, and all we can do is stop fiddling absentmindedly on the shore and face it head on and try to survive occupationally and socially.

.

To this end, we must educate our children at leading universities and in subjects whose employment opportunities will not be cannon fodder in the face of the global deployment of artificial intelligence. There is little else we can do. Professions such as teachers, doctors or manufacturing that can be replaced by 3D printing, to give just a few examples, will have to adapt radically to the new AI rules of the game if they are to survive. Others, such as those involving typing, telephone answering, etc. will probably become hopelessly extinct in the face of virtual assistants, of which Alexa, Siri, etc. are only primitive and crude versions. As the speaker in the video we link to at the end of this article says, they would be what we call «virtual assistants".«narrow AI«.

.

The prestigious MIT University in the US has created a project, 1 billion, no less, to train multidisciplinary students to adopt and combine their education of any degree, even if it is not technological, with artificial intelligence, very present in all their careers. As Gay de Liébana said in his lecture last month in Barcelona, parents must do everything possible to give their children the best training and qualifications for the global world they will face. That is what he did with his own son, who now lives and works in Los Angeles, and sent him to study at an American university. By the way, here you can read the costs and scholarship possibilities for Spanish students at universities in the USA, You will see that you don't have to have brilliant grades or be rich to send your children to the best university education system on the planet. Another of the virtues of the university system in the USA - key in the current and future environment - is the flexibility to transfer and validate credits from one degree to another without losing courses or money. In fact, it is so easy to reorient your studies throughout your college years that 70% of students graduate with a different degree than the one they started with, making decisions and adapting their study programme to their preferences each term. This flexibility, together with the technological edge of American universities, will be a feature of the American university system. It is vital for our children's educational process to be able to adapt more easily to the changes that will also occur during their university years.

.

In short, the machine revolution is already here, and our children will have to cope in a changing world, very different from the one we know. To do so, they will have to train and adapt throughout their lives, since the professional tasks they perform will be as ephemeral as the customs of the society in which they will live. They must avoid professions that will become extinct, and at the same time train constantly to adapt to new professions that will emerge from nowhere at breakneck speed and that we cannot even imagine today. We will experience this too, although it will probably affect us somewhat less as we will be close to retirement or already fully engaged in a contemplative but overwhelming life.

.

Finally, we leave you with this very interesting speech 8-minute film made last year by Michael Harrison, a graduate in Theoretical Physics at the MIT and with a Master's degree in Aerospace Systems Architecture from the USC. Artificial intelligence not only puts many of the present professions at risk at its levels of narrow AI y strong AI, but also the civilisation itself when it reaches the level of super-strong AI. But hopefully our children won't see that... but our grandchildren will.

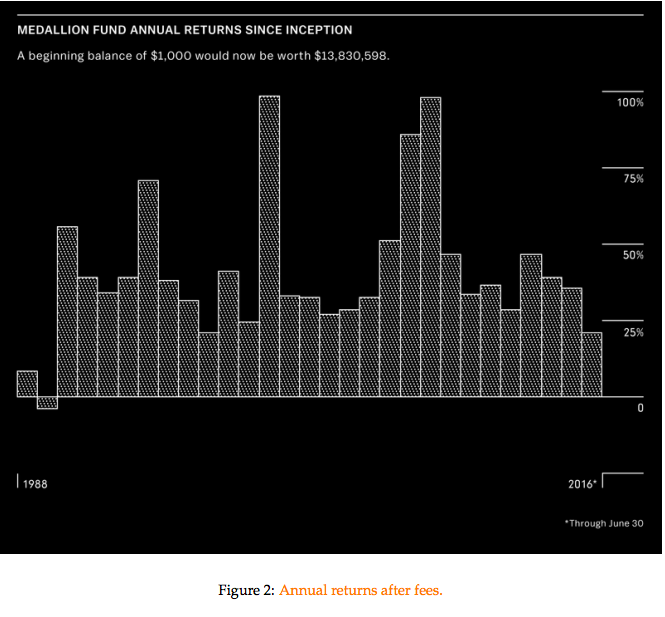

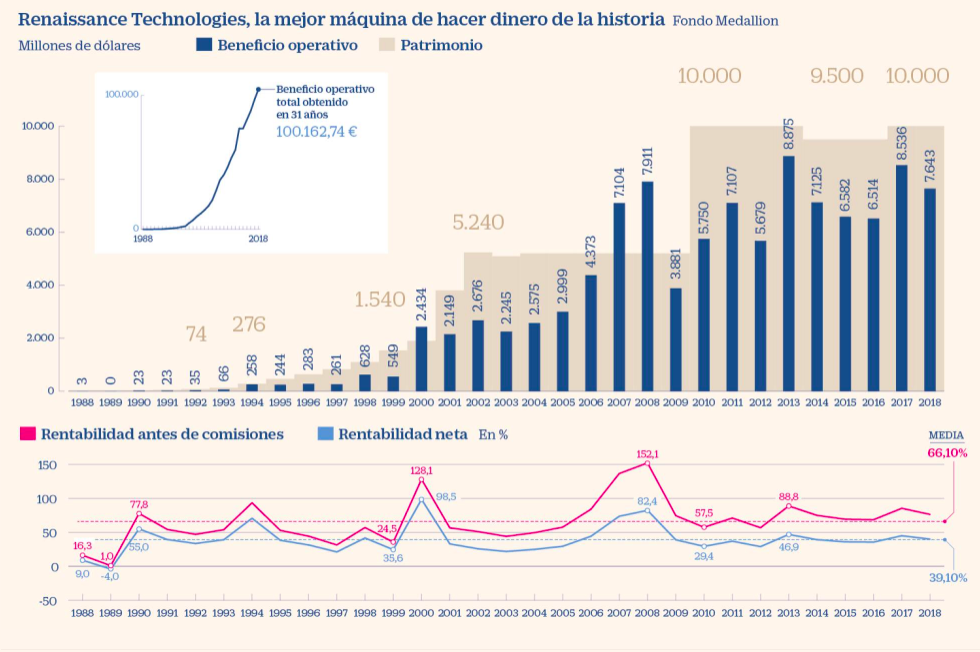

Most investors know little or nothing about the inner workings of what is considered the best investment fund in the world, due to its stratospheric performance over more than 30 years, the Medallion Fund. We have therefore decided to write this article unveiling the information we have gathered and the ins and outs we learned when we visited its management,Renaissance Technologies, a couple of years ago. Despite the length of the article, we believe it will be very interesting for readers to learn about the background, inner workings, curiosities and eccentricities of this great group of scientists, who have been recognised as the best managers in the world for their ability to beat the market for decades.

.

The first piece of bad news is that since 1993, Medallion has only managed money for its just over 300 employees and, of course, the owners of the management company. The good news is that Medallion's fund manager Renaissance, has 3 funds open to some institutional clients. But the second piece of bad news is that to invest in these institutional funds you have to have a minimum of $5 million, and also pass the due diligence that the fund manager performs on new investors. Yes, you read that correctly, to access Renaissance's institutional funds it is not enough to have a minimum investment of 5 million dollars, but the managers reserve their right of admission. But do not be discouraged, read on because At the end of the article we will explain how an investor with a minimum of 125,000 euros/dollars can access these funds.

.

According to Bloomberg, the size of the Medallion, which is the fund set aside for «...", has been reduced to the size of the Medallion.«friends & family».» The current owner's fund size is approximately $11 billion, which together with the other funds that Renaissance manages for an elite group of institutional clients, make up the $62 billion under management in total (figures as of January 2019).

.

We will now explain the origins and evolution of the world's best fund manager, and at the end of the article we will tell you about our personal visit to the Renaissance Technologies facilities, after passing both their due diligence and ours and thus becoming institutional clients of their funds.

.

The origin and evolution of Medallion and Renaissance performance:

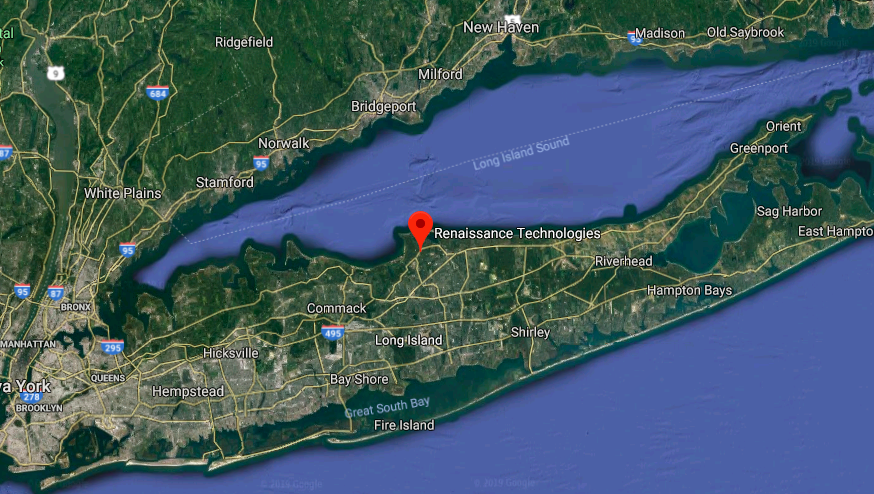

On the north shore of the luxurious Long Island, just a couple of hours' drive from Manhattan, lies the area popularly known as the Renaissance Riviera. Not for nothing are the biggest billionaires in the area scientists working for Renaissance Technologies in neighbouring East Setauket. This elite group created in 1988 what has been the biggest money-making machine in the financial world, the Medallion Fund. A quantitative fund that has far exceeded the returns of other legendary managers such as Ray Dalio or George Soros. And what is even more spectacular is that it has done so in less time and from a smaller size.

.

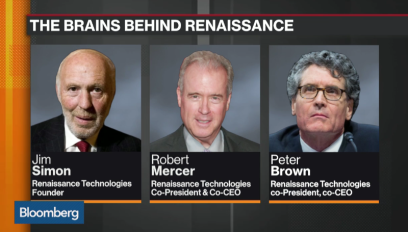

This fund almost never loses money. Its worst 5-year performance has been -0.5%. According to Andrew Lo, professor of finance at MIT and chairman of AlphaSimplex, another quantitative fund manager, «Renaissance is the financial and commercial version of the Manhattan Project«. Andrew Lo praises Jim Simons, the mathematician who founded Renaissance in 1982, for bringing so many scientists and intelligence together in a single enterprise. «They are the pinnacle of quantitative investing. No one is even close to their level.». Very few companies generate so much fascination, buzz and speculation. Everyone has heard of Renaissance and the mythical Medallion but hardly anyone knows what goes on in there. Apart from Simons, a somewhat more public figure who retired in 2009 with a personal fortune estimated at more than $16 billion, little is known about the rest of its small group of founding scientists, whose wealth exceeds the GDP of several countries.

.

For those who are wondering whether such astronomical returns (see graph below) and such sustained returns over time are really possible, it is worth commenting here on the words of Simons, in his lecture last week at the Massachusetts Institute of Technology (MIT), when he was asked for the umpteenth time in his career whether he had ever been compared to the fraudster Madoff: «Of course, with our results and after what happened with Madoff, shortly after that the SEC (US regulator) looked at us and investigated us thoroughly. Of course they didn't find anything.». But this team of scientists who have been beating the markets for more than 30 years, with a fund closed exclusively to them, and 3 others with entry barriers of USD 5 million, really care little about the sceptics.

.

Renaissance is unique among hedge funds, institutional funds and closed-end funds. Its partners and managers are as cool as they are eccentric. Of the more than 300 employees, 90 are doctors (Ph.D) in disciplines such as mathematics and physics. Peter Brown, who co-heads the firm, used to sleep on a folding bed in his office. His counterpart, Robert Mercer, rarely speaks. And the identical twins, Stephen and Vincent Della Pietra, PhDs specialising in string theory, often argue loudly with each other. The rest of the staff can't be called typical office workers either. There is too much talent for vulgarity.

.

For the outsiders, the mystery is how Medallion has been able to win so close to the top of the table. an annual 80% before commissions, The fund, by the way, takes almost half of the return, although in reality almost all of it stays at home as it is a fund exclusively for members and employees. And the most surprising thing is that despite three decades of experience, they have not been able to copy them enough to come close to their results. The reasons are to be found in the power of its computational capacity, because the computers in their bunker basements are among the most advanced on the planet. Their talented employees have more and better data in which to find patterns and models that can be exploited. And they also fine-tune the costs of their transactions, of which there are many, while taking into account the consequences that their own trading generates in the markets.

.

But it should not be forgotten that the origins of most of its founders come from IBM back in the 1980s. There they used statistical analysis for the first linguistic challenges faced by mathematicians and computer scientists. Jim Simons, mathematical genius, professor at MIT and Harvard, winner of the Oswald Veblen Prize in Geometry and co-creator of the Chern-Simons Theory, was also a code breaker for the Institute for Defence Analyses (IDA).IDA) of the USA. (the current location of the Renaissance headquarters may not be coincidental, given that East Setauket was the area known as Culper Spy Ring, The birthplace of espionage, which enabled Goerge Washington to confront British troops with prior knowledge of their secret plans at the end of the 18th century). The aim of quantitative analysis is similar: to build models that find hidden signals in the «noise» of the markets.. Often they are just whispers, but some are able to predict how the price of a share, a bond or a barrel of oil will make a profitable move, however imperceptible it may be. The problem is complex. Prices depend on fundamentals and flows and the often irrational behaviour of the actors who are buying and selling. Despite (or because of) the fact that Simons lost his job at IDA after publicly denouncing the Vietnam War in a New York Times article, the cryptographic connections he researched helped him create Renaissance, and a few years later Medallion. On his way out, he sought out and surrounded himself with cryptographers and mathematicians such as Elwyn Berlekamp and Leonard Baum, former colleagues at IDA, Stony Brook and professors Henry Laufer and James Ax, for his initial project: Statistical price prediction.

.

The beginnings were bittersweet, and trend following and conversion to the mean caused them problems. Gradually they built models and more models. The initial results were mixed: +8.8% in 1988 and -4.1% in 1989. But in 1990, after explicitly focusing on short-term trading, Medallion achieved a profit of +56% net of commissions. The scientists went on to develop an internal programming language for their models. Today, Medallion uses dozens of «strategies» that run together as one. The computer code they use includes several million lines of code, which is soon to be said. Several teams are responsible for specific areas of research, but in practice everyone can work on everything. Every week there is a meeting where new ideas are tested and discussed to extreme limits by almost a hundred PhDs and other gifted minds.

.

In the early 1990s, spectacular yields became the norm at Renaissance: 39.4%; 34%; 39.1%. And customers began to flock to Medallion. The fund manager never bothered with marketing, in fact today its website still looks like a relic from 20 years ago. In 1993 Renaissance stopped accepting new customers. Fees were multiplied from 5% management + 20% success fee to 5% + 44%. Brutal, but even so, their net returns still stood out far above the rest. Not only that, but also In 2005, they had already expelled from the fund all former investors who were neither partners nor employees, leaving Medallion exclusively for them, and creating for the outsiders the first of the 3 institutional funds of which we will give details later: RIEF, RIDA and RIDGE.

.

Scientific background applied to markets:

The success encouraged Simons to hire more and more brilliant scientists. The next batch of gifted people to join the Renaissance family was a team of mathematicians from IBM's research centre in Yorktown Heights, NY, who were struggling at the time to get machines to recognise, emit and translate human speech. Let's just say that the parents of Siri, Alexa and Google Translate.At first mathematicians tried to rely on linguists to codify grammar, but they soon realised that the problems they faced were much better solved by mathematical probabilities than by language experts.. Mercer for example disappeared for months to type conjugations of French verbs into a computer. Processing his data allowed him to write an algorithm that found the most plausible translation for each sentence: «Le chien est battu par Jean» translated as «John does beat the dog», which was a dramatic improvement on the literal translation that systems without such algorithms were running up against. With every linguist they fired and mathematician they signed up, the system took a step forward. A similar thing happened with speech recognition: «Given an auditory signal x, the speaker probably said y«. «Recognition and translation are the intersection between mathematics and programming,» said Ernie Chan, who worked in the 1990s in IBM's research department and today manages QTS Capital Management.

.

Mercer and Brown then made a bold proposition to IBM: «Let us build a computer model to manage a part of your pension fund».». At the time IBM was managing a $28 billion fund for its employees. IBM rejected the proposal, thinking what would language programmers know about the investment world? But Mercer and Brown were already determined to apply their knowledge to making money in the financial markets. IBM was also at a low ebb, and it was easy for Simon, Mercer and Brown to recruit talent at the time. Renaissance was created by mathematicians who learned to program, not the other way around. They learned how to build large systems where many people were working at the same time. That was another competitive advantage of Renaissance.

.

Talented additions came and went, the Della Pietra twins (String Theory), Lalit Bahlt (responsible for human speech recognition algorithms), Mukund Padmanabhan (digital signal processing specialist). Almost all of them had worked together at IBM. They soon realised that tackling the market was much more demanding than the advances required at IBM. Either your algorithm was better than the rest - which were starting to flood the markets - and you made money, or it was worse and you went broke. High pressure was tremendously productive. Renaissance spent a lot of resources collecting, sorting and cleaning data, and making it accessible to its researchers. «If you have an idea, you want to test it quickly. And if you have to get the data you want to use right first, it slows the process down enormously,» said Patterson, another code breaker who worked for British intelligence and was part of Renaissance until 2001. But intellectual challenges are not the only incentives for this group of data-hungry brains. They also enjoy something more intangible: The feeling of a family of top-level scientists and the complicity and satisfaction that this brings them. Simons was like the benevolent father figure who added emotional intelligence to a group as diverse as they were geeky.

.

When the IBM scientists joined Renaissance, Medallion was already earning more than 30% net of commissions. And almost a third of that came from futures trading. In those early days, the inefficiencies of the market were more visible and exploitable than they are today. For example, one of their scientists noticed that there was a 15-minute gap between the close of options and futures, which allowed them to create a specific system to exploit that for a time. The market was full of aberrations, and the scientists investigated each one to death. The sum of all of them generated very large amounts of money for them. In the beginning it was millions, but after a few years it was in the billions. But as the financial system became more sophisticated with the proliferation of other quantitative funds, inefficiencies became scarce.

.

When Mercer and Brown came to Renaissance, they started working separately, but soon realised that they were more powerful working together. They fed off each other: Brown was the optimist and Mercer the sceptic. «Peter is very creative with a lot of ideas, and Bob says, I think we need to go deeper on this one,» Petterson said. They took over the group working on listed stocks, which were losing money. It took no less than 4 years to make the system work.. But Jim Simons was very patient. The investment paid off, and even Today, listed equity managers, through their derivatives and leverage (let's not forget that inefficiencies today are much more subtle) still generate the lion's share of Medallion's profit.

.