Interesting reflections in this article from ValueWalk on how tourism-dependent economies are affected by this pandemic. Below we summarise and comment on the dark prospects that the author explains in this article.

.

Before the pandemic, the global tourism industry was a major contributor to the world economy, accounting for 10% of global GDP and more than 320 million jobs worldwide. But the pandemic has put at least 100 million jobs at risk, most of which are in micro, small and medium-sized tourism enterprises. That is 1 in 3 tourism-related jobs.

.

How have countries that are particularly dependent on tourism been affected by the pandemic?

These countries are likely to be affected by the pandemic for much longer than others that are not solely dependent on their tourist economy. The reason is simple and obvious. Contact-intensive services are part of the internal fabric of the tourism and travel sector, which unfortunately for tourism-dependent countries, had to be suspended due to the nature of the pandemic and will most likely continue until people feel safe to travel en masse again. There is no way to do tourism without personal, physical contact. And the virtual tourism that has emerged, via visits with professional guides who live-stream their tours via zoom and the like, is not and will not be a meaningful substitute or palliative for economic disaster.

.

In the first half of 2020, global travel and tourism fell by almost 80% and lost US$1.2 billion in revenue. The consequences for tourism-dependent countries, including several African countries, countries in the Caribbean, the Mediterranean and some Pacific Island nations, are severe, as their economies and GDP continue to shrink as the pandemic unfolds.

.

How do tourism-dependent countries plan to recover?

A number of tourism-dependent countries are trying to finance various policy measures to mitigate the effects of plummeting tourism revenues on households and businesses. Cash transfers, subsidies, tax breaks and loan guarantees have been part of these government policy measures. However, in countries such as Spain, which is used to receiving 84 million foreigners each year, such measures are clearly proving insufficient and ineffective.

.

Other tourism-dependent countries have opted for very specific approaches. The Seychelles, for example, benefited from an increase in tuna exports during the pandemic to compensate for tourism losses, while in Barbados the government is seeking to reduce social spending and reprioritise capital spending to create jobs in non-tourism sectors. Small economies, if their rulers are nimble and imaginative, can make decisions that have a substantial offsetting effect.

.

With the slow lifting of global travel restrictions, many tourism-dependent countries have also begun to reopen their borders. Some have drafted and approved very specific travel admission programmes that would admit tourists from low-risk countries with special quarantine requirements or allow admission on condition that tourists can provide proof of a negative COVID-19 test. However, others such as Spain cannot do so because their levels of contagion and ICU bed occupancy and daily deaths do not allow it.

.

What will happen to hidden tourist destinations?

While many tourism-dependent countries are implementing recovery strategies to boost travel and tourism, there are many tourist destinations, with somewhat more diversified economies due to their larger size such as Spain, that need tourism to survive the pandemic.

.

There are hidden parts of Europe where tourism is also key and represents between 10% and 15% of their GDP, for example Spain or Croatia. Or even more, such as in the Fiji Islands or others in the Asia-Pacific region.

.

Destinations such as Fiji for example are isolated tourist destinations that did not experience an influx of tourists on a regular basis even before the pandemic. However, now, given people's hesitancy to travel to popular holiday destinations, these destinations may be the perfect places for people to go now that countries are lifting travel restrictions.

.

What is the future for tourism-dependent countries like Spain?

It is very difficult to predict the future of the tourism industry and how tourism-dependent countries will fare during and after the pandemic. But slowly, with countries lifting travel restrictions and opening their borders, tourism-dependent countries may recover after the pandemic, but with so many people still hesitant about mass travel, such as flying, it is likely that global tourism will not return to pre-pandemic levels in the near future. And when it does return, the Hunger Games will decide which countries get the biggest slice of the sector's comeback, since tourism distribution need not return to the same countries - far from it. The key question is whether or not the economic damage caused in countries such as Spain will be reversible before the next generation is spoiled. And the macro data we explain in «We must plan for misery»The «tourism crisis" does not bode well for the optimism of our children. Our governments, present and future, will have much to say in the potential recovery and exploitation of tourism. But, as we warned in "The sinister future of our children in Spain»Parents must also make it easier for our children to make a living in less hostile economic environments.

The well-known Bloomberg editor Tracy Alloway explains in an article published this week what has happened in the markets with the price of the famous company GameStop and its chain of -obsolete?- physical videogame shops. Below we summarise Alloway's reflections and add some more from our point of view.

.

It seems inevitable that the democratisation or populisation brought about by technology will also reach the financial markets. But the impact of trading by small speculators through platforms such as Robinhood Markets is causing a real earthquake in which the strong hands of the markets are immersed without knowing or being able to do anything about it. Organised through various social networks, amateur investors/speculators have been able to make the share prices of meme stocks such as GameStop take off, while large hedge funds are suffering the consequences of having analysed these companies in more depth and betting against them.

.

Some fear that this war of money flows between small amateurs and big professionals, which generates infinite and further increases in the share prices of mediocre businesses, will collapse the system at some point. It may not go that far, but what is undeniable is that it takes away one of the basic premises of capital markets: the efficient allocation of capital.

.

What happened to GameStop and how did it all start? The online broker RobinhoodMarkets, along with other similar platforms, have flooded the market with new amateurs. Many of them from their own homes, some of them unemployed, some of them studying and all with a lot of time on their hands because of the pandemic. It seems as if financial investment has become just another video game for this already gigantic niche. Tremendously crowded forums have sprung up, such as Reddit's WallStreetBets, whose slogan reads something like «Making money and having fun while doing it». These forums have made it their goal to exploit a financial system they have historically been unable to access. And the traditional market players, the establishment, are horrified at how they are managing to bend the system in their favour.

How are they changing the way the market works? Traditionally Value investing has looked for undervalued companies to buy at a relatively cheap price in the expectation that it will go up. For the new amateur traders on such platforms, Value is not nearly as important. Some of the stocks these traders have their eye on are far from profitable or attractive to a traditional investor. But once the price starts to rise, the collective magnet is activated and the attraction of more and more interconnected traders on r/wallstreetbets begins. So far so good, since traditionally a company's share price can rise to a point where, relative to its earnings multiple, book value, etc., it is no longer attractive to investors. As a result, demand begins to be outstripped by supply and the share price moderates to more or less reasonable levels. But with the massive irruption of these new small speculators, prices can go far beyond what pseudo-fundamental or even technical analysis has historically tolerated.

Why? Because flows dominate over professionals. The flows of money in and out are more important in this segment than the fundamentals themselves. And small traders have more capacity to detect and take advantage of the flows in and out of shares, with tools such as forums and the detection of the majority opinion of their colleagues in the purest social network style, than the professionals trying to properly delimit the value of these businesses. Paradoxically, professionals, at least in the stock segments targeted by these crowded platforms, are being relegated to the crumbs that retail investors used to have, and are sailing small boats at the mercy of the storms and big swells generated by the huge mass of amateur traders. The world upside down (finally?).

Who were the professionals in the GameStop case? Short sellers, i.e. funds that borrow shares to sell them, hoping that their price will fall before they have to buy them back and return them to those who lent them to them for a small rental fee. These funds used to publicise their bearish bets and negative fundamental analysis on a company in order to convince the rest of the market that it is bad business to hold the stock and generate sales to drive the price down. But that strategy of professional investors going public with a short sale may now be history, because these days what this news generates is unbridled bullish interest from the unconditional mass of r/wallstreetbets. It is like a red alert that throws amateur traders into buying options on these stocks en masse, turning the traditional predators, the big funds and hedge funds, into prey.

What is the strategy? The guys at r/wallstreetbets usually pick stocks that have weaknesses they can exploit. For example, some have taken to buying options on stocks to force their prices up. As many of you already know, options are contracts that give the holder the right to buy or sell the underlying stock at a certain price within a certain period of time. And new commission-free trading platforms, such as Robinhood, have made options trading much easier. The key idea is that buying options en masse forces market-makers to hedge their own exposures by buying shares of the underlying company. That dynamic can be enough to drive the price up, which generates more buy orders, feeding back more and more of the dynamic: The stock goes up, the short sellers give up and have to buy back the shares they need to return, and those forced purchases drive the price even higher.

Can the small speculators really beat the big whales of Wall Street? What we should be looking at is not the amount of money retail speculators spend, but the amount of leverage inherent in those bets. Let's take an example:

Pol has a Robinhood account. He bought a call option strike $3,250 on Amazon on 14 August for $1,500. That option is crossed by a market-maker, let's say her name is Lola, who works at a large bank. But Lola does not want to take on the risk as Pol's counterparty; she wants to be merely a neutral facilitator. Her job is to facilitate trades in the market, not to bet on it, so she wants to hedge her position. She does this by buying Amazon shares, calculating what is called the delta of her position. The delta is how much the value of the option will change based on the price of the underlying stock. In this case she calculates that she must buy $66,100 worth of Amazon stock to maintain her neutral position. If Amazon's share price rises, she would have to pay for the option sold to Pol, but at least she would be compensated by the profit she would make on her Amazon shares.

A few days later, Amazon shares do indeed rise, and do so by 5%, so Lola needs to rebalance her books to maintain her neutral position. This time, because Lola's delta has increased, she will need to buy even more underlying shares. In fact, she will need to buy $230,000 worth of Amazon shares already. Et voilà! Pol's small bet has resulted in a purchase of $230,000 worth of Amazon shares.

By targeting broker exposure in a coordinated and massive way, retail traders are taking advantage of what is known as the «gamma squeeze». That is, as Amazon's share price approaches the strike price of the option, brokers and counterparties who want to remain neutral must buy more and more of the company's shares.

What about hedge fund shorts? Gamma squeezes can be most effective when short squeezes of the company's shares are added. Traders at r/wallstreetbets have often identified companies with a lot of short interest and a small number of shares listed on the market. This further complicates matters when short sellers must buy back shares to close out their short positions. This dynamic also contributes to the rising price of outstanding shares as supply is scarce and demand, although forced, is more and more increasing. Hedge fund Melvin Capital announced on 25 January that it had accepted a $2.74 billion injection from competitors Citadel and Point72 Asset Management after its short positions generated a 30% loss for the year.

Is this phenomenon a simple game? We might call it a simple gambling game were it not for the fact that these dynamics affect real companies, with real managers and real employees. Shares in GameStop, after all a retail software business, have soared exponentially this year. And the current price is such a cash injection that ideas have begun to emerge of what GameStop's management could do with all that capital raining down from the sky. Think of the strategic acquisitions, expansions and diversification of the business that are now within their reach. So these arbitrary flows also end up affecting the fundamentals of companies. AMC Entertainment Holdings, another meme stock whose main business is cinemas and theatres, avoided the bankruptcy to which the pandemic seemed to have condemned them at the end of January, by capitalising on the rise in its shares promoted mainly by retail traders. And in turn, some hedge funds may be selling some clearly bullish stocks to cover their losses, which will work against their returns.

How long can this last? No one knows. It is difficult for the US regulator to fight comments on forums that generate such large movements because it is difficult to prove that such posts are part of an illegal orchestration to manipulate the market. In December the Massachusetts regulator made a formal complaint against Robinhood alleging that they had aggressively advertised their platform to attract novice investors and had not taken sufficient safeguards to protect them. Not very consistent, but that's all the regulator could do.

.

Big market squeezes tend to end abruptly and dramatically, and that will probably be GameStop's ultimate fate. But when that time comes, most fans of r/wallstreetbets will take their huge cash flows to their next target.

.

But we must not forget that amateur traders, most of them young people with or without university careers, who are causing these financial earthquakes are merely playing by the same rules of the game as the other players. The consequences of their flows are as morally reprehensible or irreproachable as the consequences of the flows of traditional strong hands. They have not invented anything, except that their strategic decisions do not stem from an investment committee or the Machiavellian complicity of several of them, but from investment trends or fashions that are transmitted through what we might call socio-economic networks, and whose execution is as atomised as it is massive and disciplined.

.

The big loser in this game is the efficient allocation of capital. Because although the rise in share prices can save companies from bankruptcy or provide businesses with money that, if well used, can make them take off in profits and improve their fundamentals, let us not forget that capital is being showered on those who do not deserve it. Companies that over the years have not been able to attract the capital of investors seeking value do not know how to generate it. And probably, the fact of providing them with capital that does not seek Value but rather to take advantage of inefficiencies in the system (not in the market), will not only perpetuate mediocre managers in their posts but will also give them, at least temporarily, more power.

An INefficient allocation of capital that comes on top of what we have been suffering since 2008, with state interventions to keep zombie companies and managers alive with free debt at negative rates, and against which it is very difficult to navigate. Therefore, although it is perhaps fairer that not only the strong hands take advantage of the failures of the system (don't miss the video-analysis by Tucker Carlson above), the market must increasingly handle more and more players who do not seek efficiency in the placement of their capital but other things. And that makes the market more inefficient and for longer, which is not necessarily as bad as it seems for those who navigate it with the search for value as their only compass.

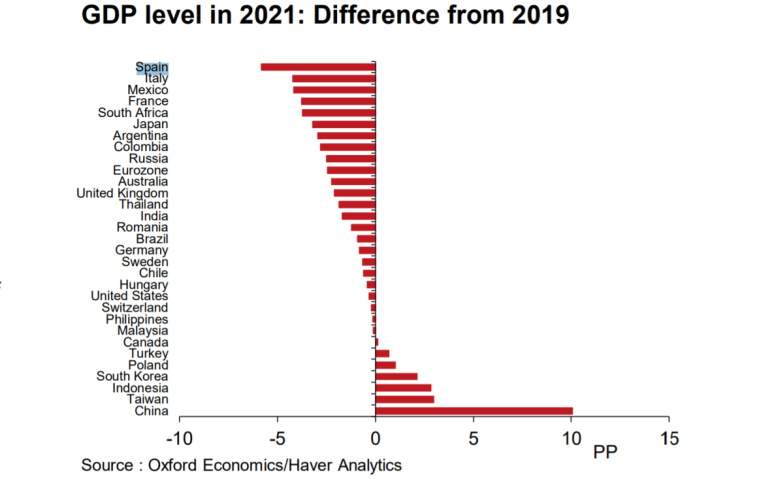

The latest data published by Funcas The forecasts for the fall in GDP in Spain are devastating. Moreover, although the adjustment of the forecast in the rest of Europe has been slightly upward, meaning that the final fall will probably be somewhat less than the expected hit at the start of the pandemic, the economic disaster throughout Europe is bleeding. Worse still, the scarcity of production, ageing demographics, rising social spending, over-indebtedness of states and extractive taxation stretched beyond its limits make the Old Continent's economic recovery a desert that many Europeans are facing with hardly any water. Let's see the magnitude of the tragedy in the following graphs by ElEconomista:

Nor does the US economy have much brighter prospects, despite the fact that its economic growth and taxation is enviable from a European point of view. Nevertheless, its business and innovative fabric is already allowing for a slow but much more feasible recovery than in Europe and the burden that we Latin and Greek Europeans are carrying.

The global economic centre, which has been shifting inexorably towards Asia for more than a decade now, is therefore being further boosted by the pandemic. This health crisis, which is crushing Western economic expectations as no other debacle has ever done, is creating an even more serious threat to the global economy. tremendous and silent acceleration of the process of relocation of the economic and financial centre towards China and its area of influence.. In this area of influence we must include such powerful economies as India, Australia, Japan, Korea and Russia itself, as well as, of course, the more orbital ones such as Vietnam, Thailand, Myanmar, Taiwan, the Philippines, Indonesia and Malaysia, to name just the largest.

It is true that some Asian economies are also suffering relatively large GDP declines during the pandemic. But the fact that they are orbiting a gigantic locomotive like China, whose growth forecast despite the pandemic is not only positive but overwhelming, means that their medium- and long-term prospects are radically different from the desert that awaits us Westerners in general and Europeans in particular, not to mention Spain's dramatic outlook, of course.

As can be seen in the graph above, the winners in this pandemic are as clear and distant as the losers. In view of what lies ahead, we would do well to follow the compass of economic growth for our investments in the coming years. In other words, the outlook for our investments in Spain is one of insomnia, since you can already imagine the fiscal reaction that our government will perpetrate in the face of such a debacle... In other words, a confiscatory taxation never seen before (with great evils great «remedies»...), in which any solution imaginative will also be blessed by the northern countries of the EU, since every euro confiscated from ordinary Spaniards will be one euro less that the Germans and the Dutch will have to finance/give us. Therefore, legal insecurity in Spain is going to be record-breaking in the times to come, and we would do well to replacing Spanish bank accounts and isins with Luxembourgish ones. No one in the EU will watch over our legal certainty in the face of confiscatory governments of one colour or another. No one.

We must therefore avoid investments in countries where the pandemic's scourge will result in an economic axe with very little capacity for recovery. Therefore, investments in countries such as Spain will have - and are already having - devastating prospects, or at least with very high opportunity costs compared to other investments in China or other countries with infinitely better conditions. And we are not only referring to the fact that investments in the Spanish stock market are going to be a disaster, but also to domestic real estate investments, whose demand for rents or buyers will be greatly reduced by the general impoverishment of the population and the business fabric. And we all know what happens when demand falls below supply, don't we? Well, to this we will have to add even more extractive taxation for property owners, since we are facing a State that is agonisingly tax-collecting due to the fall in GDP. A fall that goes straight into the vein of the public deficit, cuts and the more than likely desperate confiscation of everything that moves and does not move, that is, movable and immovable assets.

Therefore, in the coming years we will see stock markets with the wind at the back and stock markets with the wind at the front. And these headwinds and tailwinds are of course also applicable to real estate investments. But since buying real estate in distant and unfamiliar markets is foolhardy without a local team to look after your interests, ordinary investors should focus on equity investments in listed companies in countries with the best economic, demographic, production and financial prospects. And this obviously brings us to certain Asian markets as a priority, such as Mark Mobius already predicted a year and a half ago. Let us not forget that there are companies in the world that own an infinite number of properties that form part of their fixed assets, and therefore when we buy their shares we are also buying them. bricks.

The question is where to find good Asian funds, managed by strong local teams, that far outperform their respective benchmarks, and of course also the funds owned by multinational managers, who invest «by hearsay» in Asia from their Western offices in London or New York. For there are already excellent Luxembourg-domiciled funds (125,000) that overweight the fastest-growing Asian markets and are therefore accessible from just 125,000 euros. give access to a portfolio of top-tier funds for professional investors and hedge funds in Asia..

It is true that most advisors and other analysts continue with the old-fashioned approach of promoting Western investments as virtually the only investable universe, regarding all other options as obscure and risky «emerging markets». Nothing could be further from the truth, since the real risk lies in the European «declining markets» and not in the Asian emerging markets, most of which are already rather emerging and form the present and future economic and financial centre, with or without Wall Street's permission.

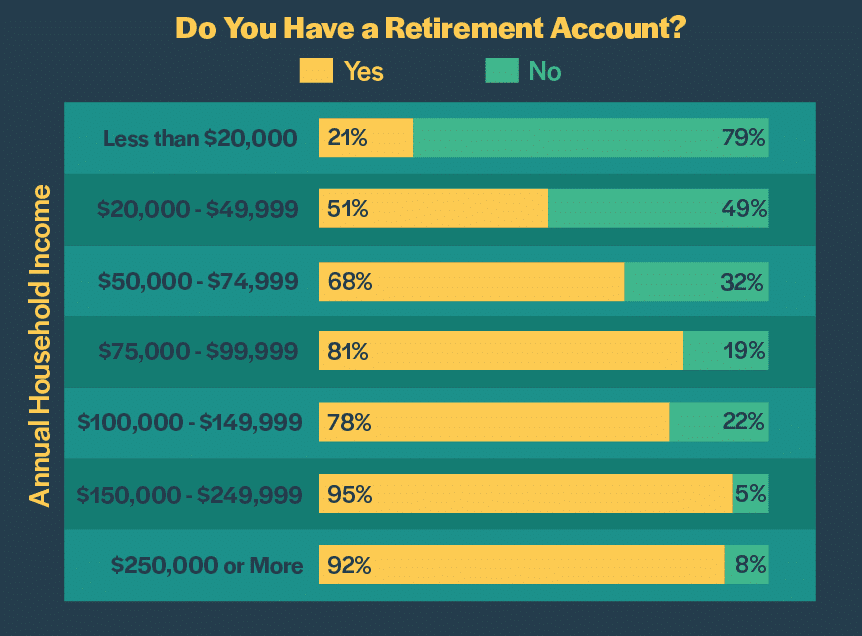

According to a recent study published by ValueWalk, Those families who would most need the long-term returns generated by investing in the stock market are the most reluctant to invest in it. In contrast, those with the highest wealth and income are precisely those who have the highest proportion of company shares in their portfolios. And those additional returns that the wealthier generate over the long term through the stock market further widen the gap between the rich and the poor over the years. The conclusion is that the poorest have an even worse financial outlook in retirement, not only because of their low lifetime earnings, but also because of their aversion to the stock market.

.

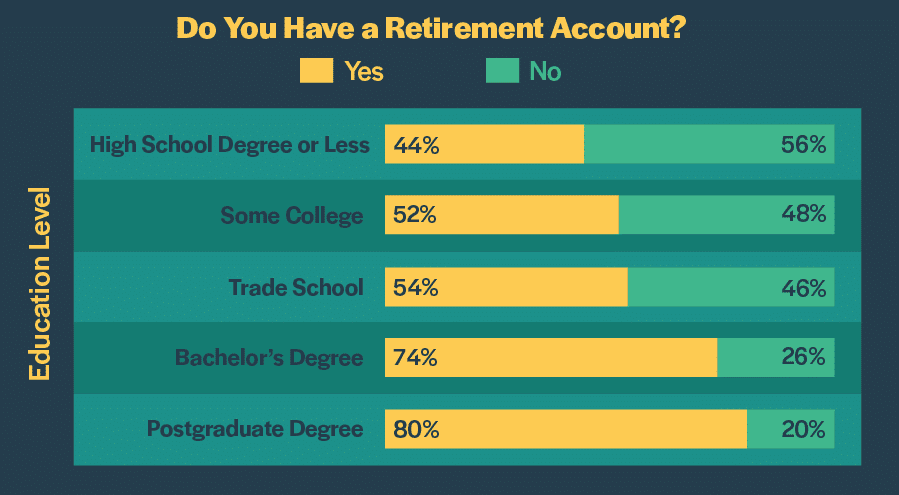

But not only the poorest invest less in the stock market. According to the data from this survey of the US population, also less educated citizens are more fearful of investing in company shares. As many of you already know, the culture of investing for the long term in an equity portfolio is widespread in the US. And it is common for employees to give up a portion of their salary so that their employers can deposit it in investment portfolios on their behalf (the famous 401(k)). Most American retirement plans are based on equity portfolios in which both the owners of the portfolios and their employers on behalf of their employees add to them over the course of their working lives, thus leaving the financial future of retirees with a less precarious working life in the hands of the growth of corporate profits rather than the state.

In the graph above we see the percentage of US workers who have a retirement plan and therefore a growing equity portfolio over their working lives, according to their income level. As you can see, it would seem that the difference between rich and poor is absolutely determined by their ability to invest to secure their future. But in the graph below we see that not only economic capacity is a differential factor but also academic training, influencing the decision to sacrifice current consumption in exchange for future consumption or financial security in old age.

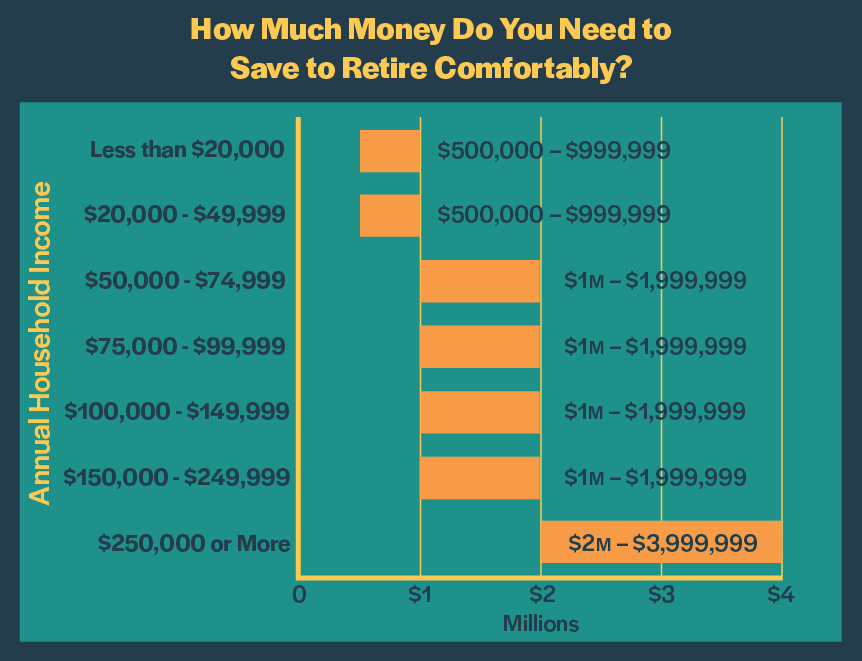

Thus, the higher the education, the higher the percentage of the population that invests in companies and does so in the long term. It is also true that the more educated we are, the more likely we are to earn a higher income, and therefore the easier it is for us to invest part of our money. But the perception that stock markets favour the richest and therefore cannot improve the lives of the poorest also suffers from a clear bias between different income levels, as we can see in the following graph. 66% of those earning less than $20,000 per year think that stock markets are unfair because they favour the rich and insiders.. In contrast, only 32% of those earning $250,000 or more per year are of the same opinion.

.

This is a particularly damaging bias, since investing in company shares should be a long-term income levelling practice. Yet the stock market aversion of people with lower incomes and educational backgrounds condemns them to dependence on failing states and a precarious retirement.

Another interesting insight is people's perception of the money they will need to retire comfortably. As you can see below, those earning less than $50,000 a year think they will have enough with an investment portfolio worth between half a million and a million dollars when they retire. On the other hand, those earning between 50 and 250,000 a year think they will need between 1 and 2 million to retire comfortably. And for those accustomed to incomes in excess of $250,000 per annum, the figure already rises to between $2 million and $4 million.

The conclusions we can draw are therefore, among others, that investment in company shares over the years of our working lives is determined not only by our level of income but also by our level of education and financial training. And that less educated citizens regard stock market investments not as their lifeline but as a practice for the wealthy elite. Financial literacy is therefore more necessary than ever, especially for those on the lowest incomes. Imagine how the incomes of the poorest people would improve if they were to take advantage of moments like this and continue to do so for decades(Incidentally, since last March when we wrote these articles recommending that we put all our eggs in the basket, the markets have risen by 25-30%, which is an understatement to say the least).

After the much read and commented in networks «The lies of the Spanish government and health authorities about the coronavirus«In the third instalment of articles dedicated to the global crisis caused by the SARS-Cov-2 coronavirus and Covid-19 disease. In our first article entitled «Realistic coronavirus figures and the opportunities of an unfortunate crisis»We were already anticipating this: The effects on the entire world economy are devastating in the short term. But only in the short term since the infection has a clear expiry date, Unlike other geopolitical, military or social conflicts, which also generate panic in the markets. Y It is this temporality that should awaken the good investor in us and change our fear for the famous greed that Buffett and other investment greats recommend when the rest of us panic.

.

In this pandemic, which is now beginning to sweep the West, the investment opportunity is one of those that are often called once in a life time, This is one of those rare occasions in the course of a lifetime of investing. This is because, although there is always room for doubt due to imponderables that can complicate scenarios, business activity will probably recover to pre-pandemic levels in the medium term at best. Obviously these imponderables include, for example, a mutation that makes the virus more resistant and/or deadly, war conflicts that add more instability to the world order, or other health crises that could arise and coincide in time with the current pandemic. But if none of these things happen, the recovery in the tone of the economy will be no more than a few months. a couple of quarters, And what should a few quarters mean on the horizon for a good investor? Nothing.

.

Therefore, it's time to go shopping (or hunting, as Buffett would say) and take advantage of the fact that the results of countless good companies around the world are going to be temporarily and exceptionally bad. Because the fall in profits and turnover will not be due to poor business performance but to a lull in global economic activity that is as exceptional as it is temporary. If we talk about airlines, we will find some at half the price of last year. If we look at the energy transport sector, the falls and fluctuations have been insane. And what can we say about the China's health sector, The winning horses, for example, have an exceptional horizon ahead of them because they will be the almost exclusive providers of pandemic and post-pandemic material on a planetary level.

.

But how to find these pearls with such a promising future? Decades ago we learned that it is much more efficient to select the best international fund managers than trying to analyse the best companies on the planet. The knowledge that good local management teams will have of the best companies in their respective countries (Vietnam, India, Brazil, China, etc.) will always be infinitely superior to ours or to that of any multinational management company that tries to make its selection through a manager located in London or New York, even if its forefathers were originally from those countries. We would therefore be well advised to invest our money now in those investment funds who have local and comprehensive knowledge of China (or the specific health sector as mentioned above) or any other country.

.

And those good local managers will not only choose good businesses, but also cheap ones, with bright prospects for recovery. Because if we think that a company may be losing a whole quarter of its turnover due to the pandemic, for example, and we buy it now at a panic price, its growth prospects in terms of turnover over the next 4 or 6 quarters will be spectacular. In other words, we will be investing with Value criteria but with a Growth potential that is as exceptional as it is profitable. If we add to this the fact that we will be selecting companies whose business is based on taking advantage of growing economies and demographics such as those in Asia, the tailwind will further boost our future profits.

.

As the image on the left hand side of the Cobas March Newsletter, It is now, when our neighbours in the 3rd 5th are beginning to realise that perhaps the coronavirus is not just a simple flu, that we should invest without fear and give free rein to our good investor's greed. Now, when our less informed friends and acquaintances are alarmed by the market crashes that are all over the TV news. Just like the lift man who recommended shares to Groucho Marx. in this essential book, or Rockefeller's shoeshine boy invested in the stock market. In other words, when the less informed panic about the coronavirus epidemic and the markets go into a tailspin, it is the most appropriate time to invest in the quality assets that have been exaggeratedly depreciated in recent days. It is perfectly possible, as we have already said, that things will get even more complicated, and that the investments we make today will temporarily lose an additional 20% or 30%. But if they do, and our investments are of quality and made with the good judgement of the best fund managers on the planet, it will be for a very short time. On the other hand, if we remain fearful out of the market, it is likely that we will not see that additional 20-30% fall but a sharp recovery and miss out on much of the upside, having blown this one. «once in a life time».» opportunity.

.

We know that many will read this article but will not follow the recommendation, as it is easy to understand that you have to buy when everyone else is selling, but it is difficult to dare to put it into practice. And thanks to the majority who won't dare and those who don't even agree with our arguments, a few of us will be able to make substantial profits in the coming years.

Financial analyst and writer John Mauldin has christened the beginning of 2020 as the decade in which we will live dangerously. In this article we will translate and comment on the arguments and analyses published by this author under the same title. Readers will be able to see the coincidence in some aspects with respect to what we have been saying in the past. publishing on this blog for more than 4 years.

.

Hyman Minsky taught us that stability, perhaps because of the abuse we tend to make of it, sooner or later leads to instability. But that abuse is as unconscious as it is harmful, and we humans like to dabble in concepts like «reasonable», «manageable», «conservative» or «prudent». That's why we feel safe seeking more and more performance until we go too far to avoid disaster.

.

To think that somehow central banks are capable of eliminating recessions and risk is crazy, despite the fact that most investors fall into this trap time and again. Yes, it is true that, as we have said many times before, with infinite liquidity no one is insolvent and therefore their debt is virtually devoid of default risk. But at some point gravity will do its work again and the insolvent will collapse as God -or the elementary fundamentals of economics- commands.

.

Debt seems harmless at first. And with sufficient cash flow, capital repayments are not a problem, let alone ridiculous interest rates. Besides, debt will be used wisely and profitably to increase growth, won't it? Well, it won't, because human nature always leads us to denaturalise goodness, and lenders will insist ad nauseam that we get into debt far beyond what is necessary for economic growth, and we start getting into debt simply to consume today what we should be consuming tomorrow. So the goodness of indebtedness is corrupted along the way.

.

Personal debt, though often excessive, is not the most serious problem. Corporate and public debt are the main challenge for which Mauldin predicts a dangerous decade ahead. And let us not forget that all this public and corporate debt ends up as personal debt, since most of us are after all taxpayers, shareholders or both.

.

The calm on the markets, however, may last a few more years (2020, 2021, 2022, 2023...). But beneath the surface of the central banks' cheerful free bar, the pressure is increasing every year. Slowly, almost imperceptibly, but at some point it will explode.

Ben Hunt, a personal friend of Mauldin's, has developed the concept of the «The Long Now«. Something like an endless today that swallows up the income of the future. Or as Hunt defines it: «Everything we bring to the present of our future and that of our children».». The Long Now is the realisation of the stark reality of Fiat money or fiat money, without anchorage to any tangible and finite value. In other words, trust in an abused and uncontrolled system is what makes us choose bread for today. And that system is the one that tells us that inflation is virtually zero, that wealth inequality, low productivity and negative savings rates are just a circumstantial fact of life. We are also told that we must vote for ridiculous candidates to be a good and politically moderate citizen, that we must buy ridiculous funds and stocks to be a good investor, or that we must take ridiculously unpayable loans to be a good parent or child.

.

Debt is future consumption brought into the present. But to pay that money back we or our heirs will have to consume less in the future, unless our economy grows sufficiently. And that is the problem, that today's debt is not being used to gain growth but we live in a world where the economy is driven by consumption. Furthermore, Ben Hunt observes that society tends to procrastinate in solving problems. We tend, with surprising skill, to postpone the inevitable (rather than avoid it indefinitely). And when it comes to over-indebtedness, it is also a three-way game, as neither debtors, creditors nor regulators are in the mood to end the game. It is in the interest of none of them to recognise that the debt is a dead letter and unpayable and to write off the losses on their balance sheets. The traumatic consequences of recognising insolvency and the resulting bankruptcies.

.

A game of Monopoly would never end if the bank refinances the debts of the players infinitely.. The million-dollar question is, as a spectator of this distorted game of Monopoly, to which player should we lend our money in exchange for reasonable returns? To the players who owe astronomical amounts to the banks, but who nevertheless continue to play and play? Or to the few players who owe nothing and are meritoriously sustaining themselves in the game by their own means? An infinite game would make no sense at all and would call into question the very market system we have known since the beginning of civilisations. Therefore, at some point not necessarily far away, the game will end and there will have to be losers. Many of them.

.

That said, Mauldin predicts that we will be comfortable and relatively safe along the way. That at any given moment, analysts will look at the data and think we have avoided the worst. We will have some passing recessions and some financial crises, but they will seem «manageable» when we get into them. And we will indeed come out of them. But what we will not see is the magnitude of the expansion that the system will need to continue to finance our debt, which will continue to grow and grow throughout this Long Now. So the debt burden will become heavier, and there will come a time when it will be unsustainable even for this trust-based system of infinite money.. Then the fan will blow more than just air in everyone's face.

.

Mauldin defined the inevitable process in 3 phases: An initial seemingly manageable instability, perhaps initially caused by high yield debt, but easily contagious to other parts of the system that are also unstable. Secondly, a drying up of liquidity that will force banks to reduce lending, thereby reducing the capital available to productive businesses and thus reducing economic growth, leading to recession. This second episode may be recurrent, with drying up of funding and intermittent renewed flows based on emergency measures by central banks, but increasingly unmanageable. And finally, a third phase of global political instability, where artificial intelligence - among other factors - will make a lot of intermediate jobs redundant. The shrinking voter will vote for governments that promise to maintain a welfare state that provides for his or her needs and comfort as in past decades, and those governments will of course raise taxes (remember that infinite liquidity dried up in phase two) to the point of economic suffocation, deepening the recession. Mauldin does not expect to see the start of this process until the second half of the new 20s.

.

Perhaps the whim of fate is leading us into another decade of the Roaring Twenties like 100 years ago. But a new Great Depression will hardly be mitigated by central banks with depleted ammunition.

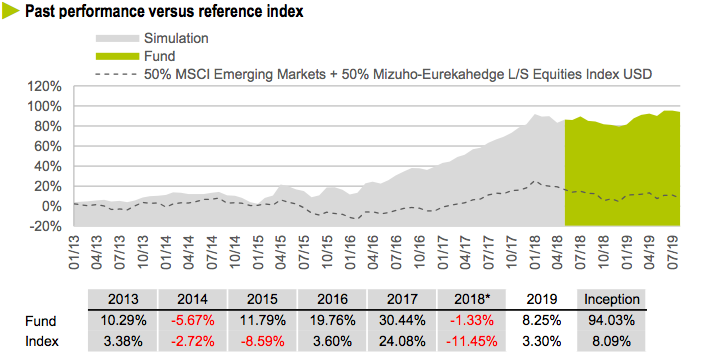

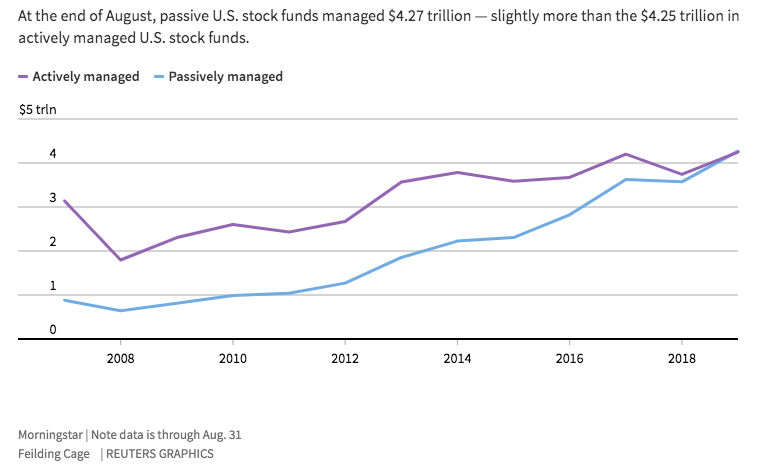

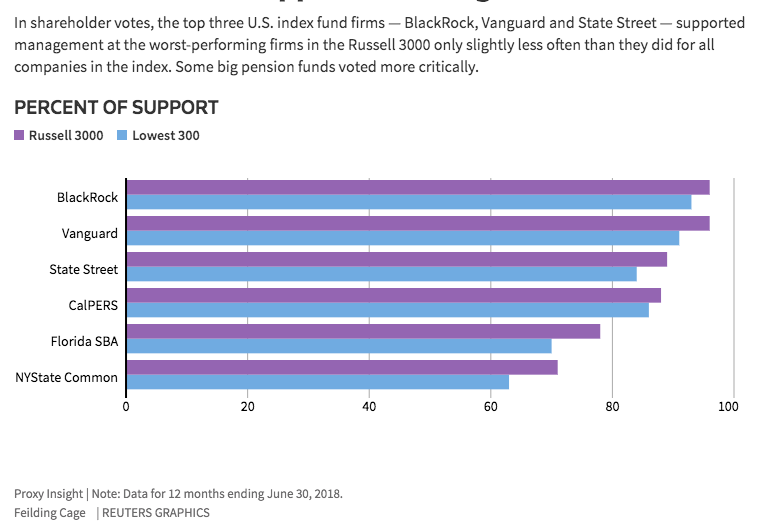

Index funds now account for more than 50% of the US equity fund market. And in Europe and the rest of the world, they are also gaining more and more followers. The main culprits for this are undoubtedly those pulling the strings of actively managed funds, whose mediocre net returns are driving disillusioned investors into the arms of passively managed funds. The reasoning of these disillusioned investors is simple: if we’re going to earn little, at least let’s pay low fees for it. But the fact that the majority of actively managed funds (between 8 and 9 out of 10) are mediocre and fail to outperform their respective indices does not mean that investors should settle for this and stop looking for that minority that outperforms them by a wide margin, as we explained in our article published on the COBAS website a couple of years ago. Here’s an example of the alpha in NET returns achieved by certain star fund managers, outperforming any index fund and with lower volatility:

Obviously, for investors who look beyond the products peddled by banks in Spain, there are gems like the one in the chart above, which outperform ETFs and other index funds by a mile. But what’s more, the comparisons are even more damning if we analyse in depth what is happening in the index fund and ETF industry. Let’s look at some of its shortcomings:

.

Just as a junk food manufacturer is a far cry from a good chef, those in charge of massive index funds such as those from BlackRock, Vanguard Group o State Street Corp They have nothing in common with good value fund managers. The former are only concerned with filling millions of cardboard boxes with something that looks like food, is cheap and appeals to shoppers. They couldn’t care less whether their customers end up with obesity, high blood pressure or any other health problems. All they care about is selling more and more volume every day at low cost. Similarly, index funds focus exclusively on pouring more and more millions into their portfolios, without caring in the slightest whether what they are buying are good or bad businesses, well or poorly managed, without caring about their fair value, let alone the long-term returns they will offer their shareholders. After all, why should they care, when more and more investors are turning away from expensive restaurants and resigning themselves to satisfying their hunger with cheap junk food?

What many people don’t realise is that these three giants of the index fund and ETF industry are responsible for keeping inefficient managers in the companies in which they invest. On reflection, the reasons may well be down to sheer carelessness, but if we scratch beneath the surface a little, hidden motives emerge, as we shall explain later. The fact is that its size is becoming such that their votes on the boards of directors are decisive to retain or replace management teams. The result is that not only do they invest indiscriminately in both good and bad companies (something inherent in passive or index-based management), but their votes also serve to keep poor managers in their posts. The million-dollar question is what interest these index fund owners could possibly have in retaining and paying out million-pound bonuses to inept managers. As always, the devil is in the detail.

.

A study carried out by Reuters through the company Proxy Insight (lower graph) shows that in the 300 worst Among companies in the Russell 3000 index where proxy votes were cast, BlackRock voted in favour of management in 931 out of 1,000 cases, Vanguard in 911 out of 1,000, and State Street in 841 out of 1,000. The study concludes that these three giants supported the management of the worst-performing companies only slightly less than that of the other companies in the index, in other words, without caring in the slightest whether or not the management was harming the profits and performance of their companies.

The litmus test is that the percentage of support given by large pension funds to management teams at poorly performing companies is falling significantly. Of course, pension funds do care about returns for their future pensioners.

.

Some might argue that active fund managers do not usually go against the management in place either, but the reality is that active managers no longer invest in companies whose management is performing poorly or with whom they disagree. In fact, that is the essence of active management: identifying good businesses run by good managers, whilst also taking into account their price relative to their intrinsic value, in the case of value investing (Compare these returns with those of any passive fund). What’s more, even if a mediocre, lazy or ill-informed active manager were to invest in a poor-performing company and, through their proxy vote, support a poor management team, the influence they would have on the vote would be infinitely less significant than that of a massive index fund or ETF.

.

Consequently, there is a very real risk that mediocre companies with mediocre management will continue to exist indefinitely, due to the proxy votes cast by giant shareholders such as ETFs and index funds. Why would those passive funds care about the performance of the companies in their portfolios if their aim is not to outperform the index but simply to track it? Why would they confront their incompetent managers, replace them or deny them a huge bonus, if their sole incentive is to grow the fund rather than maximise returns for investors?

.

Another reason – this one more Machiavellian and immoral – for not going against the bad managers of large corporations is that it is those very same executives who are promoting these passive investment funds to their thousands upon thousands of employees. How else can one explain the fact that Vanguard, State Street and BlackRock all voted in favour of doubling the salary of the CEO of the energy company PG&E Corp, just after its shares plummeted following indications that the company was liable for the California wildfires? Or that they approved astronomical bonuses for executives at the cosmetics company Coty Inc – including half a million dollars to pay for their children’s school fees– after the company had been reeling from its reckless acquisition of Procter & Gamble’s beauty division. They have also unanimously vetoed an attempt by the other shareholders to separate the executive powers of the CEO and Chairman of the Board of General Electric Co, following a decade of poor results, etc., etc., etc… Even in the few cases in the Russell 3000 study where shareholders managed to veto executive bonuses, in 601 of those cases BlackRock attempted to award them bonuses through its vote.

.

Bear in mind that the largest holdings in index funds and ETFs, just like the indices they track, are in very large companies – that is, those with the highest number of employees worldwide. This is a vicious circle, as those executives are, after all, fund managers in return for fund owners voting in favour of their million-pound bonuses at board meetings. A win-win for them, but a lose-lose for investors in ETFs and index funds, and for the economy as a whole.

.

As it is the investors in these funds themselves who are most affected by the poor quality of the portfolios, it might seem that this circle is finally closing with a certain sense of justice. But we must not underestimate the damage being done to the global economy, because every day the markets are channelling more and more millions into mediocre companies and teams, with no one seeming to care about this inefficient allocation of capital. Furthermore, Western central banks continue with their free-for-all of cheap money, and with these trillion-dollar injections, alongside those from passive investment funds, We are undermining Darwin's theory of evolution. In other words, propping up zombie companies and executives with money created out of thin air and from investors more concerned with saving on fees than with investing their money wisely.

Although most investors have never looked beyond the Solvency Standard, we must not forget that it is now 48 years since the US monetary authorities decided to abandon the Gold Standard – that is, the pegging of the dollar’s value to that of the precious metal. The practice of pegging money to a commodity that conferred intrinsic value upon it was widespread not only in ancient times but also throughout the 19th and 20th centuries, and so its abolition in the early 1970s caused considerable unease amongst US savers, who were accustomed to sleeping soundly in the knowledge that they could exchange their bank notes for a proportion of gold. The difficulties faced by issuers in maintaining the value backing for their currencies were in crescendo, with the result that the proportion of intrinsic value in the money issued gradually decreased, thereby allowing the money in circulation to increase beyond the limit originally set by material wealth (commodity) itself.

.

From that point onwards, intrinsic value began to be gradually and more or less subtly replaced by confidence (fiat) in the issuer. In fact, in some countries such as China, parts of what is now Canada, and other European countries and kingdoms, this path of no return towards fiat money began centuries ago. The new fiat money standard quickly took hold in the West during the 20th century, driven by the economic pressures resulting from the world wars, thereby placing the value of money entirely in the hands of (fiat) in the states, which were, unsurprisingly, delighted by the opportunities for political manipulation of money that this afforded them. With the end of the Bretton Woods Agreement in 1971, the US definitively buried the intrinsic value of its currency, and fiat money became the global standard – in case anyone still had any doubts. From then on, obviously, some states fared better than others – take, for example, the US versus Argentina, Venezuela or the ‘banana republics’ and their hyperinflation. But even for the top performers, the confidence of most savers in their respective governments has not been enough to prevent a loss of purchasing power over the years.

.

The fiat money system is here to stay, clearly, and we will never again see our money pegged to any real asset. It is simply too tempting for governments to have the power to create an infinite supply of electronic (formerly printed) money. But despite this endless possibility, which hyperinflationary ‘banana republics’ have been abusing, That Fiat standard was self-imposed, based on a criterion that has been key for almost 50 years: solvency. In this way, by linking the ability to create an infinite amount of money to the limits of solvency for repaying debts, Fiat money has, in fact, been the replacement of the gold standard with the solvency standard. In other words, trust in the state had a limit, which was none other than its actual ability to repay its debts and balance its books between public spending and tax revenue from the population without causing inflation to spiral out of control. For this reason, for decades there have been countries whose currencies depreciated against others due to mismanagement, forcing those states to cover their budgetary excesses with new money or public debt, which in turn fuelled inflation. This public debt had to be considered attractive enough for private capital from domestic and foreign investors to finance it. Investors who, consequently, demanded in return an interest rate commensurate with the risk that that state would be unable to pay its debts without printing banknotes, and that inflation would therefore erode its purchasing power. In other words, interest rates which in turn placed a price on the currency issued by each state, based on its ability to balance its books and its inflation rate, that is to say its Solvency.

.

We therefore had a system whose insolvency was self-regulating, since anyone caught in an unstoppable spiral of debt at rising interest rates and galloping inflation would default within a few years, dragging their economy and that of their ill-advised fellow citizens into ruin. But as politicians have never known how to steer the economy, the abuse of debt – even in countries that kept their inflation under control – began to bubble up. Until the debt crisis of 2007 struck, followed by the crash of 2008. By then, excessive debt was so widespread and insolvency so high that the risk of default by insolvent parties was systemic, starting with the entire Western banking system. Solution: Draghi’s famous phrase, «whatever it takes«In other words, central banks will generate as much money as is needed to turn the insolvent into the solvent and thus save the system. Because with infinite liquidity, the insolvent party never goes bankrupt; they simply extend and roll over their debts to infinity and beyond, allowing creditors to avoid having to set aside provisions for bad debts beyond what their balance sheets can bear. It’s a bit like the ostrich that buries its head in the sand.

.

The new standard is therefore that of fiat money, but for the past decade it has also been infinite by decision of the world’s most powerful central banks. In other words, The money needed to keep banks, large systemic companies and the states themselves afloat is being created and will continue to be created, as is the case in the southern part of the eurozone, by adding zeros to its debt and with negative interest rates (we already discussed this 6 years ago in financial repression). Some of the obvious drawbacks are that we are allowing zombie companies – inefficient and up to their ears in debt – to survive, as they repay their maturing debts with new money created by central banks in exchange for their worthless IOUs. Another fatal drawback is that sub-zero interest rates not only keep insolvent public and private entities afloat but also provide even greater incentives for private borrowing. For all these reasons Solvency is no longer a ratio to be taken into account. It will also be chaotic that all these ultra-low-yield instruments are sweeping aside anyone who has made income their modus vivendi or modus operandi – that is to say, private rentiers, pension funds, insurance companies, sovereign wealth funds and other sources of capital seeking to avoid stock market volatility. To date, we have only A decade of zero interest rates, but the damage that quantitative easing will cause in the medium and long term is devastating for the sustainability of funded pension schemes (just as the ageing population we are also experiencing is for pay-as-you-go pension schemes).

.

However, the most curious thing about the current situation is that it may be surprisingly sustainable, as it has advantages such as the fact that we can kick the can down the road when it comes to mass bankruptcies for decades – who knows, perhaps even for generations. We simply need to get used to the idea (and we’re already doing so) that sovereign debt, for example, far exceeds 100% or even 200% of GDP. After all, what does the debt-to-GDP ratio matter if solvency is a problem that central banks have left behind with their new «Infinite Money Standard»? Thus, we see how states keep themselves and their banks solvent by creating money without it entering significant circulation, since the vast majority of these flows do not leave the debt circuit perpetuated between central banks, private banks and state-owned, quasi-state-owned or systemic companies. In a word, we are living in the paradise of ‘too big to fail’. Under this new system of infinite liquidity, the effects of the dreaded ‘austericide’ – championed by the German hawks – can be mitigated, as it fosters inefficient and anaemic economic growth whilst keeping inflation at rock-bottom levels and also warding off the dreaded deflation. But the short-sighted benefits do not end there; in this vicious cycle, politicians can secure re-election without having to make bold decisions or think beyond one or two parliamentary terms – which is their usual intellectual horizon.

.

So what are the risks of this infinite liquidity? Well, as well as providing the perfect breeding ground for the inefficient allocation of money whose price is close to zero, hyperinflation would be another factor that could ultimately cause this new system to implode. But as we saw 10 years ago in «The illusion of wealth and the Quantitative Theory«An increase in the money supply without a corresponding increase in the velocity of circulation is not sufficient to drive up prices. And the tap controlling the speed at which money flows through the veins of the population – that is, the so-called real economy – is entirely controlled by central banks, governments and private banks.”.

We are therefore entering a profound era in which the Solvency Standard has become obsolete, and in which infinite liquidity will keep zombie companies, banks, states and governments afloat, whilst also giving them an air of normality to which we are already becoming scandalously accustomed. So let’s put the low volatility aside and the comfortable life of the rentiers of yesteryear, the natural selection of the insolvent and inefficient, and a reasonable cost of capital.

.

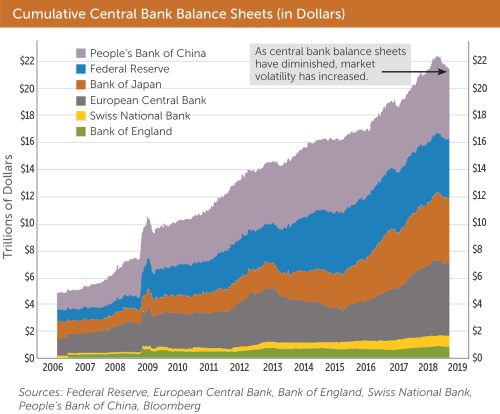

Infinite Money is the New Standard, and we must learning how to make ends meet in this new era that is set to last for several decades (we’re already a decade into it). Just look at the chaos that ensued as soon as attempts were made to turn off the tap in 2018 (chart at the top of the article). As a result of the market turmoil, central banks have begun to backtrack, reopening the tap in 2019 and 2020. Rentier investors and conservative investors (sic) who still believe they can beat inflation with low volatility are being misled by their financial advisers and/or bankers. In this environment of zero interest rates and excessive debt, neither today nor for many years to come will it be possible to generate solid, sustainable returns that outpace inflation without taking on enormous risk. And that risk is none other than lending our money to issuers of debt and structured products – whether guaranteed or otherwise – and other forms of financial engineering, which are effectively ‘zombies’ kept afloat only by an endless supply of money.

.

The million-dollar question is whether we can throw the savings of the most conservative investors into the arms of virtually zombie banking products, trusting that the era of infinite money is here to stay. The answer is that many have been doing so for a decade and it has worked out relatively well for them (although they have hardly kept pace with real inflation), given that no deposit, guaranteed product or fixed-income portfolio has gone bust under the leadership of Draghi, Yellen or Bernanke. But the fact that a political decision has been taken to keep insolvency afloat does not make those investments solvent. Therefore, barring a very few exceptions involving alternative income-generating assets – such as life settlements or certain segments of the US mortgage market, which exhibit moderate volatility but offer quarterly liquidity and selective access – the most conservative investors would do well to accept the volatility of the stock markets countries whose economies are still growing and will continue to grow for at least a decade. And to invest in those growing assets and markets, they must look for the best funds in the world, without the huge restrictions imposed by minimum investment amounts or marketing regulations in Spain.

.

In this era of infinite money, which is here to stay – as the famous soap opera used to say – one could say that without volatility, there is no paradise.

For the investor, the definition of risk linked to volatility is not only misleading but also totally counterproductive. However, a large part of the financial sector and practically the entire banking sector determine - legally and in practice - the risk of investments through their volatility: The higher the volatility, the higher the risk (sic) and vice versa. But the worst thing is that this is how they qualify the risk profile of their clients, a profile that will determine the assets in which they will be able to invest, according to this volatility. As a result, we find aberrations such as considering an insolvent and expensive fixed income portfolio as a proposal suitable for conservative profiles. And we see how many investors are deprived of buying stocks simply because valuations are volatile in the short or medium term. And it does not matter to them that over the medium to long term the certainty of stock market returns is much, much higher than the likelihood that the bonds in the insolvent and expensive fixed income portfolio will return principal and interest without anycredit event (unless bailouts with public money, which we will pay back in the future in the form of taxes, avoid permanent losses, as we have seen in the last decade).

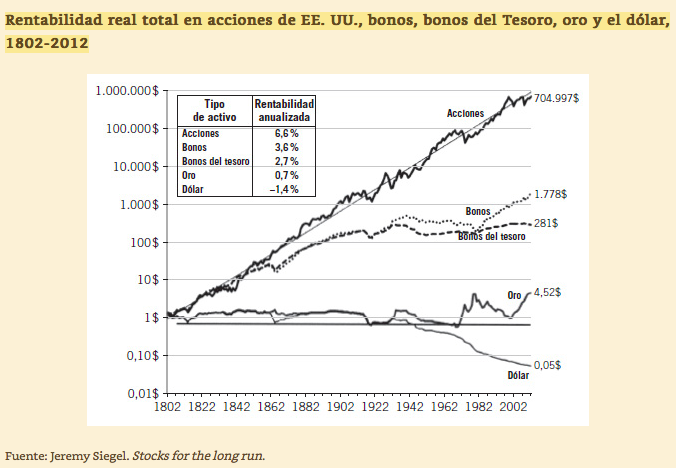

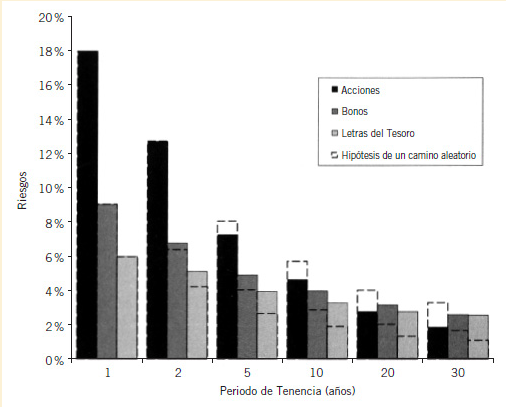

Francisco García Paramés explains it perfectly in his book «...".«Investing for the long term«From it we have extracted the graphs, which are devastating in terms of the fallacies instilled in investors by a large part of the banking and financial sector. As you can see in the graph above, the risk of long-term stock market losses is nil, while the risk of permanent losses in fixed income persists. Moreover, even volatility is lower over the long term in equities! In other words, by investing passively in listed equities, we will not only achieve higher returns over the long term, but we will do so with lower volatility and no downside risk. If we also do so actively through managers of bright backgrounds that outperform benchmarks on a consistent and sustained basis over time, we conclude that this is our best option as investors who want to preserve and grow our investments over the long term.

.

This is and should be the investment criterion: to preserve and increase our financial capital while avoiding permanent losses. What is a permanent loss? It is a loss from which we will not be able to recover before the opportunity cost, currency devaluation and inflation eat us to death.. In other words, a loss that will reduce the progression of our wealth so decisively that only inflation, devaluation and the passage of many years will allow us to recover it in nominal terms, but which will have crippled our purchasing power over a large part of our investment life. For example, a permanent loss is a credit event on a bond or debt asset, or the purchase of a property or share in the middle of a price bubble. In other words, paying far more for an asset than it is worth and will be worth for many years to come. Although obvious, it is worth remembering that a permanent loss is not a temporary short-term loss. Short-term temporary loss is simply volatility that affects us momentarily in an apparently negative way, but which will be recovered with greater or lesser speed depending on the intrinsic value of the asset relative to the fall in price.. And we say «apparently negative» because, as we shall see below, such a permanent loss provides us with golden opportunities.

Here are a few examples of the difference in risk that the same volatility can have, taken from the reflections of Didier Darcet about it. Let's say three neighbouring homeowners in the same neighbourhood, with three identical houses, suffer a major fire in the neighbourhood that completely destroys their properties. They thus have the same initial volatility, since their assets have depreciated identically in value and time:

.

The former has no insurance to compensate him for the losses, so he will suffer them permanently. It is true that over time inflation and the devaluation of your currency can make your empty plot of land worth nominally the same as your house was worth before the fire. But that inflation/devaluation and the opportunity cost squandered over a good part of his investment life will mean that his losses will have been permanent despite recovering the same nominal amount of money over time. For this first neighbour, suffering a fire was a real risk. And after the trauma he will probably decide to sell his plot of land unthinkingly or out of necessity, to move to another cheaper neighbourhood or to a rented house, where he believes he is safer from future risks.

The second neighbour does have fire insurance equivalent to the cost of building the house, so, say in the medium term, he can replace the asset and recover the loss suffered in the short term. Therefore, although he has the same short and medium-term volatility as the first neighbour, his risk would be virtually nullified by insurance. Some would say that he is a homeowner with no medium/long-term risk, but with undeniable volatility if a loss occurs. Would such a homeowner consider that he is at risk of losing part of his equity? In the short term yes, but no one in their right mind should consider them to be a risky owner or risk taker, if they are insured and will be recoverable with full certainty in the medium to long term.

The third owner also has insurance that covers the cost of construction and will allow him to replace his house. But he will also want and be able to take advantage of the current circumstances, and will buy his uninsured neighbour's plot at a good price, taking advantage of the need and/or fear that the latter may have because of the fire (temporary loss or volatility) suffered in the neighbourhood. Therefore, he will convert his temporary loss into a higher profit in the medium and long term. And the most curious thing is that the volatility of this third case will be even higher in the short and medium term than that of the two previous cases, while maintaining practically zero risk. In the case of a financial investor, buying the neighbour's house would be the equivalent of buying back more shares of good Value funds or shares of extraordinarily cheap companies, i.e. taking advantage of the fear and/or need of others to buy assets with high Value at a low price.

Here it is worth remembering that the first graph is based on investors (owners) as the second neighbour, i.e. they will recover their temporary losses in the medium and long term. But imagine now what this same graph would look like if the investor is also able to take advantage of moments of volatility (of fire) to invest more and additionally buy assets at unusually low prices. Obviously, recoveries from temporary losses would be much faster, dramatically shortening short-term loss periods and very substantially increasing long-term returns. This is easy to say but difficult to do, as the natural primitive impulse is to flee from loss-making assets, like the first neighbour flees the neighbourhood where there has been a fire.

.

Readers should therefore consider their financial investments in the same way as the third neighbour, provided they are able to invest in actively managed funds that consistently and permanently outperform indices. If they do so, their volatility and returns will be high, while maintaining zero risk of permanent losses. And if investors are unable to find such funds, they can always emulate the second neighbour through passively managed funds, assuming short to medium-term volatility in exchange for zero risk of permanent losses.

.

Fortunately for neighbours like the third, most behave like the first. Without these obfuscated and/or needy investors there would not be a massive supply that would plummet prices after the fires. That is why the big managers pray and put candles to Saint Volatility, so that Mr. Market's schizophrenia will bring them opportunities. The higher the short-term volatility (fires), the more investment opportunities will occur and the higher the long-term returns with less risk of permanent losses, which are the only losses investors should care about. These are concepts that are radically opposed to the slogans of most professionals in the sector, who remain obstinate in placing their more conservative clients in assets with low volatility and, paradoxically, a greater real risk of permanent losses. Perhaps this is because for banks, as for politicians, the long term is science fiction. Some with the end of the legislature, and others with the collection of the variable or the obligatory sales figure at the end of the year, but both with a galloping myopia. And because when they talk about risk, they are referring to the risk they themselves have of losing their clients as soon as their portfolios, without the fire insurance of a good Value stock market fund, start to smoke.

Here is the newsletter sent out this week by Louis V. Gavel, from the prestigious research team at Gavekal, in which he talks about the effect of ETFs and the shift of the centre of the world from traditionally developed to emerging countries. A translated version of this article is proof of this:

.

«Another clear symptom that the investment world environment has changed is that the underperformance of emerging markets, which prevailed between 2011 and 2016 (when oil fell, the USD rose and yields remained low), is now clearly history. We are now living in a world where bond yields will tend to rise, the USD will tend to fall, and oil prices could show upward pressure. In such a world, exposure to emerging markets is once again rewarding. Indeed, an interesting feature of the recent falls is to see how volatility in US equity markets has actually been much higher than in most emerging markets. Even after this week's fall, Asian markets are significantly outperforming global equities.»

.

It is curious to see how, little by little, the centre of the investment world is shifting from the US and Europe to Asia, and with it, volatility is taking the opposite path. In other words, while development reaches the emerging countries, volatility travels to countries where development is weighed down by over-indebtedness. And the unfortunate thing is that for most advisors and private banking managers, investment proposals towards countries where there is economic and demographic growth with decreasing volatility (emerging countries), are of greater «risk» than traditional European and American funds, where anaemia and volatility take over their growth. The difficulty of finding good emerging funds that can be marketed in Spain, without having a suitable investment vehicle (where any fund, hedge fund or private equity in the world can fit, deferring taxation as if it were any fund sold to you by the bank on the corner) helps portfolios to continue to be filled with the usual funds. But reality is stubborn and the centre of the world is inexorably shifting towards Asia, where there are impressive managers who achieve spectacular alphas.

.

Here is the newsletter of Louis-Vincent Gave The complete, which is virtually unmissable:

In Agatha Christie's Murder on the Orient Express, the victim is stabbed by twelve different individuals.

The same is often true of bull markets; when they die, one finds many a finger-print on the murder weapon.

With that in mind, one could pin the death of the bond bull market on accelerating inflation, or on the globally synchronized global growth surge, or on the lack of investments in new capacity over the past decade (see A Brave New New World, attached), or even on the demographic shift unfolding in the Western World (see The Savings Glut's Long Life and Slow Death), or simply on the realisation that fiscal policies all around the world are bound to stay extraordinarily loose for far too long (see US Budget Deficits, attached)... But whichever reason one wants to hang one's hat on, the bond bear market is likely here to stay. After all, if bonds can't even rally by a few basis points as equity markets meltdown, then we must have a structural bond bear market on our hands.

And at the risk of stating the obvious, this structural bond bear market is now clearly a headwind for equities.

It also marks a profound shift in the investment environment.

In a piece written close to the market top (see A Once in a Generation Shift - attached), we highlighted that OECD bonds had been the perfect counterweight to equity positions for decades. However, it wasn't always so. In periods when inflation picks up, OECD bonds do not protect portfolios against downside risk. Instead, they add to the downside risk. We also showed that one way to know whether we were in an ‘inflationary’ environment or a ‘deflationary’ environment was to look at the relative performance of long dated US Treasuries to Gold as both had asset classes tend to ‘trend’ over long periods of time. And when the ratio ‘gold to bonds’ moves ABOVE its 4 year moving average, that is typically a confirmation that we are moving into an inflationary environment. As the chart below highlights, following this week's rise in yields, such a move has now just occurred:

So if OECD bonds are no longer a sound hedge for equity risk, what is an investor looking to reduce the overall volatility of his portfolio, to do?

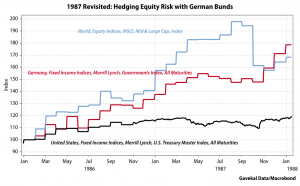

In the 1970s, and again in the 1987 crash, one of the best hedges (aside from gold), were German (and Swiss) bunds. Back then, the DM was slowly but surely establishing itself as Europe's trading and reserve currency; a genuine alternative to a US$ weighed down by too many years of US ‘guns and butter’ policies. Take 1987 as an example: US interest rates rose until they broke the back of the (then) roaring equity bull market. But as equities cracked and the fed slashed rates, investors sought out the safe haven of the inflation-fighting Bundesbank. So much so that, by the end of 1987, for an investor looking back at January 1986, German bunds had actually outperformed not only US Treasuries (that wasn't even close), but global equities as well:

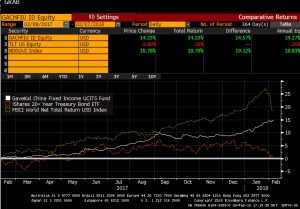

So, as Yogi Berra once said, is it ‘deja-vu all over again’? After all, in the US today, we not only have guns and butter; we should also soon have bridges, and tunnels, and hip replacements and student loan write-offs etc... (see The US Budget Deficits, attached). At the same time, we have China making a concerted push to turn the RMB into Asia's DeutscheMark, a currency that will increasingly fund Asia's trade and Asia's capital spending. And sure enough, just as global equities (World MSCI in the chart below) and US Treasuries (TLT US in the chart below) have started to roll over, Chinese bonds (represented below by the Gavekal China Fixed Income UCITS fun) have held their own. In fact, like German bunds in the fall of 1987, the Gavekal China Fixed Income UCITS fund has returned over 14% in US$ terms which handily beats the flat return of long dated US Treasuries, and could approach the return of global equities should global equities repeat the past week in the near future!

Another clear sign that the investment environment has changed is that the underperformance of emerging markets, which prevailed between 2011 and 2016 (as oil fell, the US$ rose and bond yields stayed low) is now clearly over. We are now living in a world where bond yields will trend higher, the US$ is trending lower, and oil prices could show upside pressures. In such a world, exposure to emerging markets once again becomes rewarding. In fact, one of the interesting feature of the current pullback is how volatility on US equities has actually been much worse than that of most emerging markets. Even after this week's pullback, Asian markets are significantly outperforming global equities. For example, our Asian Value UCITS fund (which focuses on developing Asia) is up +31.12% over the past 12 months, while our Asian Opportunities (which includes Japan, Australia and Asian bonds) is up +23.61% over the past 12 months. This compares favourably to the +19.4% gain in the World MSCI for the past year.

Still, the question at hand is whether we are now confronting a correction? The start of a crash? Or the unfolding of a genuine bear market?

ARGUMENTS FOR A CORRECTION:

We were due: record RSI indicators, record stretch without a 5% correction, first year without a down month etc...

As mentioned above, the investment environment is changing. Deflation should no longer be a concern. Central banks will no longer be as supportive of asset prices. The US$ is done rising. Oil is done adding liquidity to the system. Interest rates are moving higher... Any one of these forces would be a lot for the market to digest. But all together, they may be like Diderot's proverbial apricot, or Monty Python's wafer-thin mint: a little too much to chew on.

However, fundamentally, interest rates remain low, global growth is solid and so investors are likely to keep chasing returns?

“It's not a crash, it's a correction”.”

ARGUMENTS FOR A CRASH

Old card-sharks will always say that “if you sit down at a poker table and after 30 minutes, you have not figured out who the fish is, then you are the fish”.