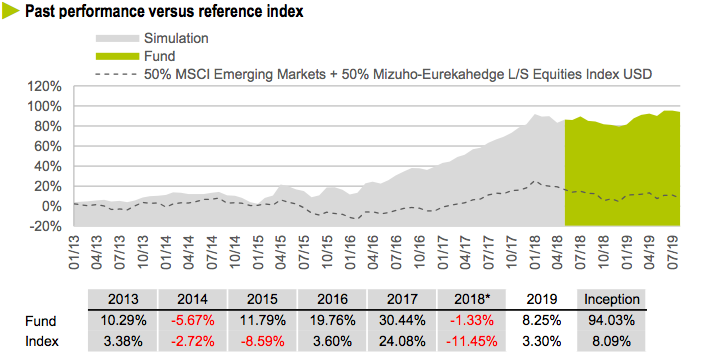

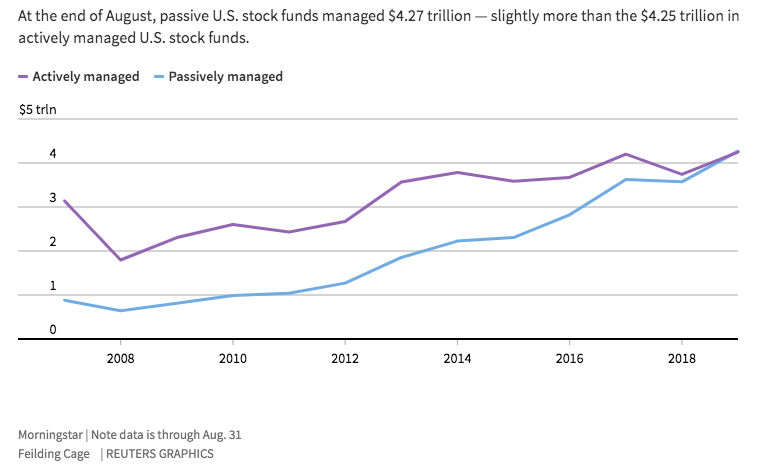

Index funds now account for more than 50% of the US equity fund market. And in Europe and the rest of the world, they are also gaining more and more followers. The main culprits for this are undoubtedly those pulling the strings of actively managed funds, whose mediocre net returns are driving disillusioned investors into the arms of passively managed funds. The reasoning of these disillusioned investors is simple: if we’re going to earn little, at least let’s pay low fees for it. But the fact that the majority of actively managed funds (between 8 and 9 out of 10) are mediocre and fail to outperform their respective indices does not mean that investors should settle for this and stop looking for that minority that outperforms them by a wide margin, as we explained in our article published on the COBAS website a couple of years ago. Here’s an example of the alpha in NET returns achieved by certain star fund managers, outperforming any index fund and with lower volatility:

Obviously, for investors who look beyond the products peddled by banks in Spain, there are gems like the one in the chart above, which outperform ETFs and other index funds by a mile. But what’s more, the comparisons are even more damning if we analyse in depth what is happening in the index fund and ETF industry. Let’s look at some of its shortcomings:

.

Just as a junk food manufacturer is a far cry from a good chef, those in charge of massive index funds such as those from BlackRock, Vanguard Group o State Street Corp They have nothing in common with good value fund managers. The former are only concerned with filling millions of cardboard boxes with something that looks like food, is cheap and appeals to shoppers. They couldn’t care less whether their customers end up with obesity, high blood pressure or any other health problems. All they care about is selling more and more volume every day at low cost. Similarly, index funds focus exclusively on pouring more and more millions into their portfolios, without caring in the slightest whether what they are buying are good or bad businesses, well or poorly managed, without caring about their fair value, let alone the long-term returns they will offer their shareholders. After all, why should they care, when more and more investors are turning away from expensive restaurants and resigning themselves to satisfying their hunger with cheap junk food?

What many people don’t realise is that these three giants of the index fund and ETF industry are responsible for keeping inefficient managers in the companies in which they invest. On reflection, the reasons may well be down to sheer carelessness, but if we scratch beneath the surface a little, hidden motives emerge, as we shall explain later. The fact is that its size is becoming such that their votes on the boards of directors are decisive to retain or replace management teams. The result is that not only do they invest indiscriminately in both good and bad companies (something inherent in passive or index-based management), but their votes also serve to keep poor managers in their posts. The million-dollar question is what interest these index fund owners could possibly have in retaining and paying out million-pound bonuses to inept managers. As always, the devil is in the detail.

.

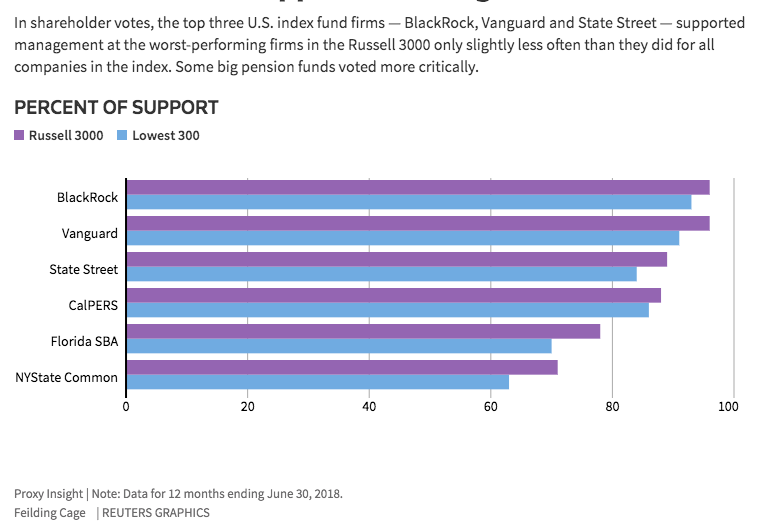

A study carried out by Reuters through the company Proxy Insight (lower graph) shows that in the 300 worst Among companies in the Russell 3000 index where proxy votes were cast, BlackRock voted in favour of management in 931 out of 1,000 cases, Vanguard in 911 out of 1,000, and State Street in 841 out of 1,000. The study concludes that these three giants supported the management of the worst-performing companies only slightly less than that of the other companies in the index, in other words, without caring in the slightest whether or not the management was harming the profits and performance of their companies.

The litmus test is that the percentage of support given by large pension funds to management teams at poorly performing companies is falling significantly. Of course, pension funds do care about returns for their future pensioners.

.

Some might argue that active fund managers do not usually go against the management in place either, but the reality is that active managers no longer invest in companies whose management is performing poorly or with whom they disagree. In fact, that is the essence of active management: identifying good businesses run by good managers, whilst also taking into account their price relative to their intrinsic value, in the case of value investing (Compare these returns with those of any passive fund). What’s more, even if a mediocre, lazy or ill-informed active manager were to invest in a poor-performing company and, through their proxy vote, support a poor management team, the influence they would have on the vote would be infinitely less significant than that of a massive index fund or ETF.

.

Consequently, there is a very real risk that mediocre companies with mediocre management will continue to exist indefinitely, due to the proxy votes cast by giant shareholders such as ETFs and index funds. Why would those passive funds care about the performance of the companies in their portfolios if their aim is not to outperform the index but simply to track it? Why would they confront their incompetent managers, replace them or deny them a huge bonus, if their sole incentive is to grow the fund rather than maximise returns for investors?

.

Another reason – this one more Machiavellian and immoral – for not going against the bad managers of large corporations is that it is those very same executives who are promoting these passive investment funds to their thousands upon thousands of employees. How else can one explain the fact that Vanguard, State Street and BlackRock all voted in favour of doubling the salary of the CEO of the energy company PG&E Corp, just after its shares plummeted following indications that the company was liable for the California wildfires? Or that they approved astronomical bonuses for executives at the cosmetics company Coty Inc – including half a million dollars to pay for their children’s school fees– after the company had been reeling from its reckless acquisition of Procter & Gamble’s beauty division. They have also unanimously vetoed an attempt by the other shareholders to separate the executive powers of the CEO and Chairman of the Board of General Electric Co, following a decade of poor results, etc., etc., etc… Even in the few cases in the Russell 3000 study where shareholders managed to veto executive bonuses, in 601 of those cases BlackRock attempted to award them bonuses through its vote.

.

Bear in mind that the largest holdings in index funds and ETFs, just like the indices they track, are in very large companies – that is, those with the highest number of employees worldwide. This is a vicious circle, as those executives are, after all, fund managers in return for fund owners voting in favour of their million-pound bonuses at board meetings. A win-win for them, but a lose-lose for investors in ETFs and index funds, and for the economy as a whole.

.

As it is the investors in these funds themselves who are most affected by the poor quality of the portfolios, it might seem that this circle is finally closing with a certain sense of justice. But we must not underestimate the damage being done to the global economy, because every day the markets are channelling more and more millions into mediocre companies and teams, with no one seeming to care about this inefficient allocation of capital. Furthermore, Western central banks continue with their free-for-all of cheap money, and with these trillion-dollar injections, alongside those from passive investment funds, We are undermining Darwin's theory of evolution. In other words, propping up zombie companies and executives with money created out of thin air and from investors more concerned with saving on fees than with investing their money wisely.

As Mark Mobius, former executive chairman of Templeton and founder of Mobius Capital Partners, said in an article from March: We need to invest in the stock markets of what are still known as emerging economies. And this time it’s the financial think-tank Gavekal Research who has published a report entitled «Wealth transfer to emerging markets» which is well worth reading. It states that the Keynesian era, that is to say, an era of financial repression and quantitative easing (QE) – or, in short, the era in which the world’s major central banks (the Fed, the ECB, the BoJ, etc.) have been lowering the cost of borrowing to revive the anaemic growth of Western economies across the globe, They are like shots of economic growth straight into the veins of emerging economies.

.

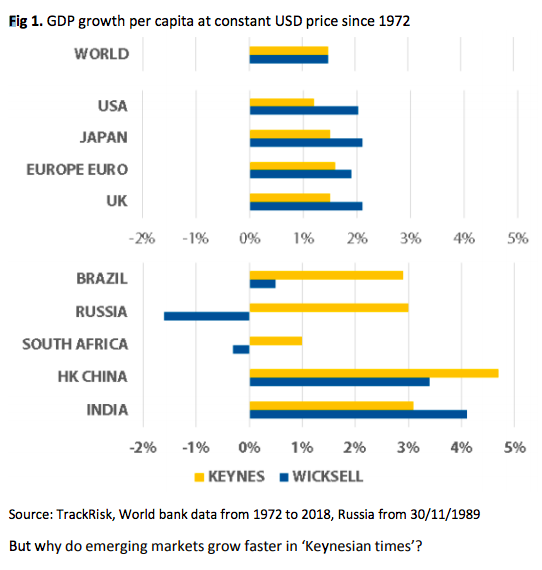

When the performance of gold outstrips that of the world’s major developed currencies, the world enters what is known as a Keynesian era. If we add to this coordinated action by the central banks of developed economies, the current policies of quantitative easing and rock-bottom interest rates amount to the death knell for rentiers. The question is, who stands to benefit from this inevitable demise? Emerging markets, without a doubt. And we can see this clear transfer of money from developed to emerging markets in Chart 1:

.

The lower axis shows the growth in GDP per capita (at constant US dollar prices) since the end of the gold standard. We can see that, in both Keynesian and Wicksellian periods (named after Knut Wicksell, who advocated interest rates that followed the trend of economic growth rather than acting as a corrective tool), growth is the same when we consider the world as a whole. But note that if we distinguish between emerging and developed countries, the picture changes radically. Here, the growth of emerging economies is clearly favoured by Keynesian periods, in stark contrast to what happens in developed countries. And also contrary to what Keynesian policy is, in principle, intended to achieve.

.

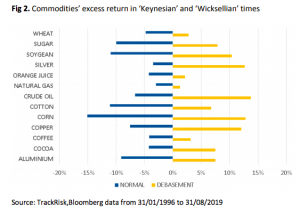

Why is this happening, when intuitively it would seem that loose monetary policies in Western currencies should favour the recovery of developed economies rather than those of emerging economies? The first reason is that emerging economies, many of which are commodity exporters, see their profits rise due to higher export prices. This is because commodities tend to become more expensive when Western currencies depreciate against other assets and currencies, which is what happens during Keynesian eras of low interest rates.

.

This is clearly illustrated in Figure 2, where, by contrast, Wicksellian cycles spell nothing short of ruin for commodity exporters.

.

The second reason is that the external debt in US dollars held by companies in emerging economies becomes cheaper under the low interest rates of Keynesian eras, which generates additional profits for these companies. This is particularly true of those based in countries with sound, low-debt and highly productive economies, where their currencies remain stable or even appreciate.

.

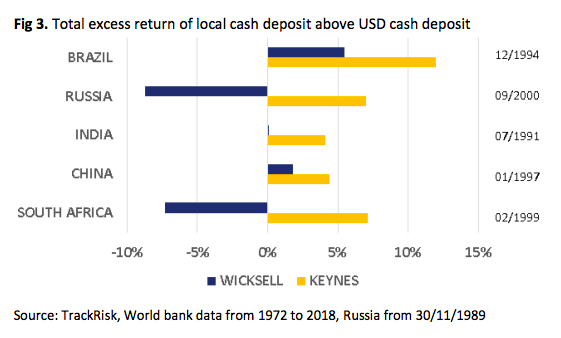

Chart No. 3 measures the premium paid on local-currency deposits relative to the US dollar. In other words, it shows the savings in funding costs for these companies compared with the costs they would have incurred in local currency during Keynesian periods. Specifically, the additional cost of local currency financing ranges from 4% to 12% per annum in the BRICS countries. The savings are very significant for emerging markets, just as the reverse is true for developed markets, which in turn will benefit from this Keynesian era by investing their capital in emerging economies whilst assuming the local currency risk. In other words, capital is flowing into emerging economies through various channels in these times of ‘free money’ in the West. Among other reasons, this is because it is ‘free money’ for which there is nowhere in the West itself to invest it so that it yields even the slightest return.

.

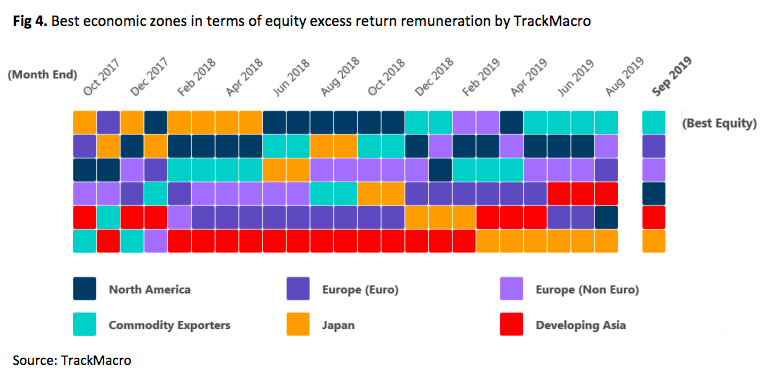

Furthermore, TrackMacro confirms that, as of September 2019, the ranking of the risks associated with holding shares in companies across the world’s various economies is as shown in Chart 4. In other words, commodity-exporting countries have been enjoying a boom since last August, topping the chart for the past five months. Note that the «Developing Asia» group excludes Asian commodity exporters, which are classified as «Commodity exporters». Therefore, it is clear that not all emerging markets are benefiting from these cash flows, just as we cannot place the German and Greek economies on the same level, even though both are «developed European» economies.

.

To further reinforce the case for investing in certain emerging markets, TrackMacro also reports that, according to key macroeconomic indicators, major commodity exporters such as Russia and Brazil offer an attractive risk-reward ratio. If we add to this the positive measures being taken by various emerging-market governments – such as the cut in corporation tax in India, made possible by the country’s low debt levels and a productive demographic – the case for investment becomes even stronger. We should invest in emerging economies with the same natural confidence and the best prospects as developed markets once had. But, of course, we must do so through the best local investment fund managers, who have a thorough understanding not only of companies in their own country but also of their legislative, accounting, tax and even cultural intricacies.

Investing whilst emerging markets have the wind in their sails and avoiding headwinds (debt, demographic trends, recession, low productivity, etc.) will be key in the coming years. For holders of typical Spanish share portfolios, here is a damning statistic: today, the Ibex 35 stands at the same level as in 1998, whilst the German stock market has risen 2.5-fold over the same period, the US market 2.7-fold and the Indian market 10.5-fold. But what is the worst for some and the best for others is yet to come.

.

Conclusion: Keynesian policies in the major developed economies should, in theory, combat deflationary pressures, stimulate domestic growth and strengthen Western companies in the face of competition from emerging markets. However, the outcome of such a policy of quantitative easing and sub-zero interest rates may be exactly the opposite. The depreciation of Western currencies leads to a massive influx of capital into emerging economies (which, incidentally, are natural magnets for investment in their own right, even without such desperate measures in the West). Investors today find themselves in an asymmetrical situation, where their major currencies have ceased to be safe-haven assets due to low interest rates. This ‘Age of Central Banks’ favours, in principle, gold, real assets and shares in emerging-market companies, to the detriment of developed economies, sovereign debt and shares in Western companies.

.

As Mark Mobius rightly pointed out in the article cited, in the late 1980s emerging economies accounted for just 5% of the global market, but now they account for more than 40%, and the figure is rising rapidly. Back then, investors could only invest in no more than half a dozen stock exchanges; yet now we have more than 70 markets open to growing foreign investment, fully equipped with state-of-the-art technical facilities and supervised by highly professional regulators. This now allows for enormous diversification and security, and shows us the way forward: now is the time to invest in certain economies emerging - or already emerging where there is a tremendous economic recovery and growth. Furthermore, the US-China trade war is nothing more than a golden opportunity to do so at reasonable prices. And anyone who continues to peddle fears about investing in emerging markets is either misinformed and out of touch, or is simply following orders from their superiors to peddle a deflationary, recessionary product that has smelled rather foul ever since central banks turned on the tap to keep zombie economies and companies afloat.

Recently the newspaper Public has interviewed several Spanish sportsmen and women who decided to study at universities in the USA to perfect their careers, both academic and sporting. This drain of talent is not only being suffered by our country at a sporting level but also at an academic level, as any student of medium or medium-high level has a place in the American university system.

.

Let's look at the motivations that lead sportsmen and women and «simple» students to pursue their careers at American universities. For sportsmen and sportswomen, the fact of studying there means obtaining a university degree that they would most probably not get here, as it would be very difficult for them to combine their sporting career, training and tournaments with classes and exams. The result is that very few Spanish athletes have a university degree when they finish their more or less successful sporting careers. In the USA, sporting success is not only compatible with, but necessarily goes hand in hand with the university world. The compatibility of training and competitions that will lead them to professional sport with classes, studies and exams is total and absolute. In addition, the facilities, sporting level and quality of coaches in the sports areas of the university system in the USA is a dream, as their budgets are light years ahead of those of any sports club in Spain, unfortunately.

.

In short, a 16-18 year old athlete who decides to stay in Spain has only one card at stake for his or her future: whether to be sufficiently successful as a sports professional or to be relegated to being, for example, a mere coach without a university degree. In the best case scenario, they will have to retrain academically when they throw in the towel on their professional career, late and badly, in order to get a job. On the other hand, an athlete who goes to an American university, even if he or she is not successful enough as a professional, will at least have a university degree (often linked to the world of sport) that will allow him or her to make his or her way in the post-sport world with the same possibilities as any other graduate. In addition, you can even obtain your masters or postgraduate degrees while continuing your sporting career.

.

Estela Pérez-Somarriba from Madrid, a student at the University of Miami, and NCAA champion (the most competitive college tennis league in the world), explains it perfectly in the interview:

.

“I was right to look at the long term. I wanted to play tennis professionally, it had always been my dream and it still is. But when I finished high school, I started to weigh up the academic, tennis, economic and personal aspects. I didn't know if I wanted to live in Madrid all my life, I needed to mature, I couldn't afford to travel and pay a coach to take the professional leap, and in the United States I could combine sport with a career”.

Estela is studying Economics and Sports Management, and she couldn't be happier with her decision. Her goal now is to jump to the women's professional circuit (WTA) as soon as she graduates, which she will also do on a scholarship from start to finish by the university itself:

“The physical and medical resources, the facilities, the advisors and teachers help you a lot. My day-to-day life is tough, but we are top-level athletes and if you want to be the best in your sport and get a degree, it is always going to be a challenge. But here I have a lot of facilities that I didn't have before.

But it is not only athletes who have their way open to the university world in the USA. Every day, more and more students who do not play any sport are studying at the more than 2,000 universities across the country. And the fact is that prices are not so abusive as a priori many families might think. Nor do theythe academic standards required are so high.

Any student of average level has a place in an American university. The prices do not have to be higher than the costs of a private Spanish university. And living expenses, i.e. flat and meals, within the university campus itself cost the same as sending our children to study in Madrid, Barcelona, Seville, Bilbao or any other Spanish city. You can see the details of the costs and price ranges in our article: «Can I send my children to study at a university in the USA?«

.

Furthermore, let's not fool ourselves, a degree from an American university will open more professional and employment opportunities for our children than a Spanish degree. Whether they return to Spain to look for work, stay in the USA or go to live in any country in the world, having a university degree from any American university under their arm will make a difference for life. What better inheritance can we leave them than that?

.

Although it may come as a surprise to many, the process of preparing for admission to an American university must be done at least one and a half years in advance. and appropriate expert advice. In other words, as we have already explained here, The time to start the process is between the end of the 4th year of ESO and the first half of the 1st year of Bachillerato.

In this Público article you can find other stories of Spanish sportsmen and women who cleverly decided to develop their careers in the USA.

.

In short, families with children aged 15-17, whether or not they are athletes, whether or not they are bright students, explore the academic and scholarship possibilities offered by the American university world. It will make a difference in their lives, and yours.

Most parents are surprised to find out that if they want their children to be able to study at an American university They have to start the process a couple of years before finishing their baccalaureate. Therefore, in many cases, by the time they make the family decision to explore the possibilities of their children studying in the best university system on the planet, it is already too late. The correct timing is to start the process at this time, when they have finished the 4th year of ESO or at the beginning of the 1st year of Bachillerato. That way, you can take advantage of the summer and the academic year to do some extracurricular activities that will substantially improve your transcript and CV for the university application process. Yes, it is true that it is also possible to start the path to an American university at the end of the 1st year of Bachillerato, but if we do so then all the steps will have to be taken with greater haste, which will be more stressful, and above all it will allow us fewer attempts to achieve good grades in the various exams that must be taken in the official centres designated in various Spanish cities. However, even in the 2nd year of Bachillerato, we have already achieved make express applications, However, the best thing to do is to apply for the following year, taking advantage of one or two sabbatical semesters to improve your English or to attend a Spanish university without any pressure.

It surprises most families to learn that it is not necessary to have excellent grades, although of course it helps to get into better universities, but any student with an average of 6 also has a chance if he or she does well in the entrance exams. Many parents are also surprised to learn that The costs may be much more affordable than they thought, and very similar to what any family sending their children to study at a private university in any Spanish or European city would have to pay. Below are the annual costs we published in our previous article: «Can I send my children to study at a university in the USA?«. As you will see, there are excellent university options with costs equivalent to those of private Spanish universities. In addition, there are possible scholarships and grants that substantially reduce costs, especially in the more expensive ones, depending on the student's academic merits and family economic needs. The following annual costs are gross, i.e. possible scholarships and grants should be deducted:

Tuition fees:

Between €10,000 and €55,000 depending on the prestige and quality of the university.

Cost of room and board:

Between 8 and 15 thousand €.

Books, materials, travel and miscellaneous expenses:

Between 2 and 3 thousand euros

Health insurance for international students:

Between €1,000 and €2,000

The process of gaining admission to US universities is long and complex for students and their families, and can be very stressful. Therefore, the chances of success without the advice and support of professional consultants and coaches are slim. As we said in the above-mentioned article, at Cluster Family Office, we have been helping many families to achieve their American dream for several years now. Our advisory service includes the entire process from beginning to end, from the moment the candidate is finishing secondary school until they are almost at the door of the plane that will take them to the universities in the USA that best suit their academic and economic potential in each case. We advise and accompany them throughout the process, including the selection of a list of universities to apply to, the Essays, letters of recommendation, scholarship applications, visa, residency and other family logistics, etc. In that final list of between 8 and 12 universities to which each candidate applies, we will include 3 or 4 Universities that meet their needs and where it is practically certain that they will be admitted; another 3 or 4 where they will have certain chances; and finally 3 or 4 more where the chances of access will be low (which we usually describe as the letter to the wise men and women), but that sometimes the flute may play and they may end up being admitted to a dream University, even though their percentage of acceptance is very low.

The main difference between American and Spanish universities is obviously the economic resources available to them in the USA. These million-dollar resources are converted into spectacular facilities, highly prestigious teaching staff, budgets available for research work for both postgraduates and new students, first-class student residences and canteens, and in short, money for students to give of themselves infinitely more, both academically and personally. The great American public and private universities are like real cities, with spectacular facilities for all kinds of sports, stadiums bigger than those of many Spanish first division football clubs, shops, banks, cinemas, theatres and even the university's own police force. All within the university campus. With these facilities, it is clear to no one that the student life of a student who stays in Spanish universities is radically different from the experiences during the university years in the USA.

.

Here are a few links to give you an idea of the flats, rooms, facilities and of the environment The experience of families who have gone through this process and receive the news of the final admission to the university of their dreams. And at the end of «Study at a university in the USA»You will also find a number of videos of what university life in the USA is really all about.

.

You can ask us for an interview in Madrid or Barcelona without obligation to assess the possibilities of your children through info@clusterfamilyoffice.com.

We’re going to summarise the study carried out by three renowned researchers and professors from Princeton and Columbia who are affiliated with the research team at the Federal Reserve Bank of New York, Mary Amiti, Stephen Redding and David Weinstein. In this study, they highlight the unsustainable costs that Trump’s tariff hikes would impose on the average American household if they were to be prolonged. For this reason, the likelihood of these tariffs bringing down the two most powerful economies on the planet is virtually nil. And they should be viewed as mutual posturing between a headless chicken and one with a head, which presents us with a very good opportunity to position ourselves in the stock markets (particularly Asian ones, as Mark Mobius also suggests in this article). Let’s look at the figures:

.

The current tariffs imposed on Chinese goods stand at 10%, and were recently increased to 25%, albeit with a 90-day moratorium to allow room for negotiation (an old tactic). To determine the impact of that additional 15% in tariffs, which Trump is threatening to impose if no agreement is reached before the end of that period, the calculation is based on the preliminary study on the impact of the current 10% taxes applied in 2018. It concludes that the impact amounts to an annual cost of $414 per family, comprising the extra expenditure that average families will have to incur to pay the additional taxes, and what they call loss of efficiency o deadweight. It is worth remembering here that a huge proportion of goods come from China, and that the rest contain Chinese components and/or are manufactured using Chinese processes; therefore, a temporary blockade by Xi Jinping would lead to an unimaginable global collapse. In short, the Chinese have the trade ‘nuclear button’ and the Americans do not. But let’s get back to the figures.

.

The extent of these costs depends on how customs tariffs affect the mark-ups importers add to their products, as well as on the demand for goods imported from China. Various studies, including the one mentioned, have concluded that the tariff increases imposed by the US imposed in 2018 have directly led to higher import prices, meaning that Chinese exporters did not reduce their prices at all to offset the increase in the final price for their US customers. The ratio of the increase in the final price to that of the customs duty was therefore practically 1 to 1. What that initial imposition of 10% on Chinese products did produce was, logically, a 43% drop in demand for Chinese imports, as the first logical move for importers is to postpone purchases and subsequently seek alternative suppliers and routes.

.

US buyers of Chinese goods now pay an additional 10% tariff on top of the usual base price; in other words, an item that used to cost a US consumer or importer $140 now costs $150. This adds $10 to their individual cost but not the US economy as a whole, as the government collects that additional $10 in the form of tax. The government, in turn, should – or could potentially – reinvest that same $10 and use it for the benefit of its citizens (including those who do not buy or import Chinese products).

It is worth noting here that demand naturally shifts between those who continue to buy more expensive Chinese products and those who switch to less expensive alternatives. Consequently, some importers or consumers will reorganise their trade arrangements or purchasing preferences, so that they buy substitute goods at a price lower than the $110 that Chinese products currently cost them. For example, a Vietnamese or Malaysian substitute item costing $105. In this case, the importer’s/buyer’s cost has increased by only $5, rather than the 10$ it would cost to continue buying the Chinese product. But beware, in this case The US economy as a whole also loses out, as there is no return on those $5 in the form of taxes that can be redistributed to the population. Furthermore, it has been amply demonstrated that importers will end up importing substitute products at a price only slightly below that of the Chinese product. In other words, imports will be at $108 or $109 and not at $101 or $105, as the comparison prior to the purchasing decision will be based on the current price of the Chinese product, i.e. $110. This principle will also hold true because suppliers will use the Chinese price of $110 as a benchmark to set their prices for the North American market. This increase in production chain costs, caused by the rise in import tariffs, is known as loss of efficiency or dead weight.

.

Economic theory tells us that this deadweight tends to rise more than proportionally as tariffs increase, as importers and consumers are forced to accept ever higher prices when taxes rise. Furthermore, very high customs tariffs lead to a fall in tax revenue, as buyers stop importing products from a country affected by those tariffs/sanctions and seek other suppliers/items from other countries, which are cheaper in terms of final price but less efficient. Let us consider that, up until that point, their suppliers and goods were Chinese because they had chosen that option as the most efficient of all the options that importers and consumers had considered. Therefore, these second and third options, beyond $100, which they are now forced to trade in, are by definition less efficient (worse value for money, worse logistics efficiency, poorer build quality, poorer after-sales service, worse marketing, worse packaging, poorer reliability, worse returns policy, repairs, etc.) than the Chinese products they had been buying at $100.

.

We can see how these two variables play out by comparing the estimated costs of the 2018 tariffs with the increase recently announced by Trump of an additional $200 billion on Chinese goods. As can be seen in the table below, in November 2018, with the 10% of current tariffs already in place, US importers were paying $3 billion a month in additional duties and suffering an additional $1.4 billion in efficiency losses or deadweight losses.

.

The total cost to US importers was therefore 1.44 billion per month. If we annualise these figures, we arrive at 52.8 billion, or 414 per household per year. Of this cost, $282 per household corresponds to money that goes into the US government’s coffers, and is therefore relatively recoverable by US society as a whole. However, efficiency losses or deadweight losses amount to $132 per household per year, and represent the net loss to the US economy beyond additional tax payments.

Based on these figures, we can calculate the cost of the additional tariff increase announced by Trump for the coming quarter, rising from the current 10% to 25%. The table shows how tax revenue for the government will fall from $282 to $211 per household per year, as the tax increase on Chinese products will be so costly that American consumers will begin to buy substitute goods that are not subject to these tariffs, such as products from Vietnam or other emerging countries, as we mentioned earlier. Let us remember that these second and third imported options are less efficient (more expensive than the cost of the Chinese product before the tariffs), and furthermore, the government no longer collects those taxes. Some of you may argue that the American consumer/importer can substitute Chinese products with other local American ones and thus avoid the loss of efficiency or deadweight. But the reality demonstrated by the studies The reality of the situation is that it is other emerging economies that are coming out on top, as products from developed countries such as the US have much higher production costs. And not only are their costs much higher, but they also have very limited production capacity (adapted to current demand and market share), which would take years and years to meet demand, even if they were to achieve the unachievable, namely the value-for-money efficiency of emerging countries. Furthermore, the deadweight loss from reduced efficiency increases whether consumers switch to more expensive foreign goods or to more expensive domestic ones.

.

As a result of this change, which importers and consumers are currently facing and will continue to face for the time being (until Trump blows his top or the lobbies force him to back down, as we will explain below), it is estimated that an increase in efficiency losses per household from 1Q132 to 1Q620 on an annual basis, bringing the total burden to be borne by the average American family up to $831 per year, if the threat of additional customs duties under Section 15% is carried out. Consequently, this increase in tariffs on Chinese imports will lead to enormous economic distortions in American society, as well as a substantial reduction in government revenue. But it is not only ordinary citizens who will be seriously affected. Just imagine the losses that giant American tech (and non-tech) companies could suffer as a result of the trade war and software boycotts targeting giants such as Huawei. Remember that Jinping has absolute control over a market of more than 1.3 billion potential consumers, and an enormous and growing influence over the rest of the Asian and African countries. All of this is already generating tit-for-tat retaliation that is causing, and will continue to cause, endless collateral damage which, no doubt, Trump and his team of ultra-nationalist Republicans have never calculated.

.

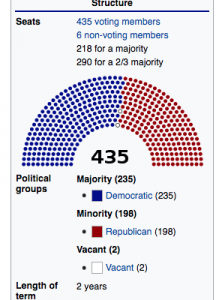

The million-dollar question is: what will major corporations such as Google, Amazon, Microsoft, Apple, etc. do in the face of Chinese reprisals which, although more discreet, will be just as brutal—if not more so—than those of the US administration that have been trumpeted by the Western media? Well, obviously, Faced with imminent losses running into tens of billions, they will prefer to spend billions on lobbying that will force Trump to reverse the situation. And billions, without a doubt, will enable the lobbies, in a perfectly legal manner, to exert pressure that is absolutely unbearable for the Trump administration. Let us not forget that in the US, Congress, with a qualified majority, can force the president and his government to do whatever it wants. Put another way, they can prohibit the Trump administration from imposing any kind of tariff or sanction on Chinese products with 290 out of 435 members of Congress. Currently, the Democratic majority in Congress stands at 54.1 per cent, so they would only need to «convince» 12.61 per cent of Republican members of Congress, some of whom will come round of their own accord as soon as the tariffs start to seriously hit their voters’ pockets.

.

Ultimately, the trade war between the US and China is so damaging – particularly to the US economy – that it has an expiry date. And Trump knows it. In this game of chicken, whoever has a Congress that keeps them in check, whoever depends on votes and corporate lobbies – in short, whoever lives in a democracy – knows they have lost the game. The winner can be none other than China, whose president implements plans spanning decades without caring about the opinion of voters (sic) or his corporations, which are at the service of the government and, of course, without any lobbying. Neither Trump nor anyone else in the US democracy will ever be able to politically or commercially subdue the Chinese dictatorship and its planned economy. Therefore, although Trump will need to bring his adventure to a dignified close, selling it to the Western media with headlines such as «we have secured the best trade deal in history, blah, blah…», the trade war cannot last more than a few quarters. The big US corporations will not allow it, via lobbies and a qualified majority in Congress. Even this «trade war» may effectively be defused whilst people are still publicly talking about it, due to Trump’s electoral political interests. But the reality can be no other than that of not causing significant or irreversible damage to the US corporate giants, since they have more than enough money to convince enough members of Congress, who in turn will force the US government to back down, even if this is not publicly acknowledged and the perception of a trade conflict continues to be fuelled. After all, Every US president has needed and provoked a war of some sort – one that is low-intensity in reality but generates a media frenzy, during their terms in office, for electoral gain. Trump has opted for a trade war, which will also attract intense media attention but is bound to be of low economic intensity.

.

For all these reasons, investors would do well to take advantage of the media skirmishes that trigger price falls to position themselves appropriately. In other words, they should go shopping for emerging companies whose figures will continue to grow beyond this fleeting, politically motivated trade war. For all the reasons set out in this article, The gloomier the outlook for the Asian markets becomes in the coming months, the closer their recovery will be. A golden opportunity to buy businesses, with the economic and demographic winds in their favour, at very attractive valuations. Remember that Volatility is a good investor’s friend and the enemy of bankers and other fearmongers, which strive to keep their customers trapped in schemes where the meagre returns are barely enough to cover the fees that are skimmed off along the way.

.

We simply need to be aware that the more heated the trade war appears in the media, the more we should invest in the best emerging-market-focused funds on the planet. Comparisons of the ‘fear funds’ peddled by the banks, with the best institutional fund managers on international stock markets are a pain. Volatility always goes hand in hand with double-digit annual returns over the medium and long term. And the best news is that There are funds of funds that provide access to these institutional funds, as we explained earlier in «Funds that make inaccessible funds accessible.»

.

The Chinese are well aware of the significance of the crisis Trump is creating with his trade war. It is no coincidence that there they define the word «crisis» as a synonym for «opportunity». And any self-respecting Western investor would do well to be less influenced by the Western media and more by the value criteria of the world’s best fund managers. This time is no different.

Our developed society seems to be frolicking in the sand by the seashore, totally oblivious to the tsunami that is crashing over us. This great wave that will sweep away everything we know is none other than the disruptive change that is already being generated by new technologies, and especially by advances in artificial intelligence (AI). The changes in society that we saw during the industrial revolution or the global implementation of the internet were child's play compared to what is coming our way. Technological and personal adaptation skills with constant training are already what our parents' and grandparents' literacy was. Without such skills and training, our old age, and more seriously, the lives of our children, are condemned to a marginalisation comparable to that of the illiterate of yesteryear.

.

The latest OECD study (Skills Outlook 2019) is devastating. It warns that the percentage of the population in Spain with the capacity to adapt to technological progress and the digitalisation of tasks is only 23%. These figures include people aged between 16 and 65, so if we think beyond the age of (pre)retirement, the scenario is even more terrifying. More than 3/4 of our society will be marginalised in the face of the technological advances that are already being implemented in the workplace. The figures improve slightly in countries with more advanced educational and social systems, such as Norway, Sweden, Finland, New Zealand, etc. But imagine the figures that could come out of less advanced societies such as those in Africa or deep Asia or South America. The extinction of jobs analogue is already and will be overwhelming.

.

But that is only the tip of the iceberg, since the artificial intelligence (AI) is a disruptive breakthrough as momentous as possibly the mastery of fire by early hominids. The AI revolution will eliminate not only the remnants of analogue jobs in the less developed corners of the globe, but also a good part of the digital ones. Until our generation, society and the global economy have been able to cope with, adapt to and take advantage of technological advances despite initial fears. We remember the trade union protests in the industrial revolution, when machines began to replace workers, who had to readapt to other work tasks. Another example would be digital photography, which overnight wiped out giants such as Kodak and their film developers. Or streaming content such as Netflix, HBO, Prime Video, etc., which are forcing the Hollywood empire itself to reinvent itself or die. The same will soon happen with other disruptive changes such as mobility in self-driving cars and a host of imminent changes that will make our society unrecognisable when our children try to enter the world of work. It is true that civilisation has been sufficiently assimilating these advances and more jobs have been created than destroyed, as economies have grown even faster than the population. But the speed of technological advances is exponential, and especially artificial intelligence will overwhelm society without having enough time to react and readapt as it has done in the past.

.

There is no antidote to the incoming tsunami. We continue to fiddle absentmindedly in the sand, wondering whether our children should learn English, Chinese or German, while they go to the university around the corner to get a degree in a subject for which we delusionally think they will have no shortage of work. Unfortunately this will not be the case. Experts warn that our children will have to adapt to work in professions that do not yet exist today and that no less than 75% of today's professions will cease to exist. The million-dollar question is what we can do to be as well prepared as possible for these radical changes. But the honest answer is that the disruptive advances of AI are so brutal and imminent, there is seemingly nowhere to take cover. The tsunami is already upon us, and all we can do is stop fiddling absentmindedly on the shore and face it head on and try to survive occupationally and socially.

.

To this end, we must educate our children at leading universities and in subjects whose employment opportunities will not be cannon fodder in the face of the global deployment of artificial intelligence. There is little else we can do. Professions such as teachers, doctors or manufacturing that can be replaced by 3D printing, to give just a few examples, will have to adapt radically to the new AI rules of the game if they are to survive. Others, such as those involving typing, telephone answering, etc. will probably become hopelessly extinct in the face of virtual assistants, of which Alexa, Siri, etc. are only primitive and crude versions. As the speaker in the video we link to at the end of this article says, they would be what we call «virtual assistants".«narrow AI«.

.

The prestigious MIT University in the US has created a project, 1 billion, no less, to train multidisciplinary students to adopt and combine their education of any degree, even if it is not technological, with artificial intelligence, very present in all their careers. As Gay de Liébana said in his lecture last month in Barcelona, parents must do everything possible to give their children the best training and qualifications for the global world they will face. That is what he did with his own son, who now lives and works in Los Angeles, and sent him to study at an American university. By the way, here you can read the costs and scholarship possibilities for Spanish students at universities in the USA, You will see that you don't have to have brilliant grades or be rich to send your children to the best university education system on the planet. Another of the virtues of the university system in the USA - key in the current and future environment - is the flexibility to transfer and validate credits from one degree to another without losing courses or money. In fact, it is so easy to reorient your studies throughout your college years that 70% of students graduate with a different degree than the one they started with, making decisions and adapting their study programme to their preferences each term. This flexibility, together with the technological edge of American universities, will be a feature of the American university system. It is vital for our children's educational process to be able to adapt more easily to the changes that will also occur during their university years.

.

In short, the machine revolution is already here, and our children will have to cope in a changing world, very different from the one we know. To do so, they will have to train and adapt throughout their lives, since the professional tasks they perform will be as ephemeral as the customs of the society in which they will live. They must avoid professions that will become extinct, and at the same time train constantly to adapt to new professions that will emerge from nowhere at breakneck speed and that we cannot even imagine today. We will experience this too, although it will probably affect us somewhat less as we will be close to retirement or already fully engaged in a contemplative but overwhelming life.

.

Finally, we leave you with this very interesting speech 8-minute film made last year by Michael Harrison, a graduate in Theoretical Physics at the MIT and with a Master's degree in Aerospace Systems Architecture from the USC. Artificial intelligence not only puts many of the present professions at risk at its levels of narrow AI y strong AI, but also the civilisation itself when it reaches the level of super-strong AI. But hopefully our children won't see that... but our grandchildren will.

After the Chapter 1: Indebtedness and the Chapter 2: Investment, let’s move on to Chapter 3: Berkshire Hathaway’s 2018 Letter to Shareholders. Here we’ll summarise some of the quotes and phrases with which Warren Buffett and Charlie Munger delighted shareholders this year. You can read the full letter, translated courtesy of our friends at the website Value School.

.

Regarding the share buyback (treasury shares) currently being carried out by their company, Buffett and Munger had the following to say:

.

For shareholders who stay on (those who do not sell their shares), the advantage is clear: if the market values the stake of a departing partner at, say, 90 pence on the pound, the remaining shareholders see an increase in intrinsic value per share with every buyback by the company. Obviously, buybacks must be price-dependent: blindly buying an overvalued share destroys value, something many CEOs overlook.

.

When a company says it is considering share buybacks, it is vital that all shareholders receive the information they need to make an informed assessment of the intrinsic value. Providing that information is what Charlie and I aim to do in this report. We do not want a shareholder to sell shares to the company because they have been misled or inadequately informed.

.

And on the subject of taxation and its decisive influence on the valuation of their holding company, the masters of value investing made some comments that are well worth noting:

.

Let’s start with an economic reality: whether we like it or not, the US government «owns» a share of Berkshire’s profits, the size of which is determined by Congress. In fact, the US Treasury holds a special class of our shares (something like an AA class), which receives large «dividends» (or taxes) from Berkshire. In 2017, as in many previous years, the corporate tax rate was 35%, which meant that the Treasury was very happy with its AA shares. In fact, the Treasury’s «shares», which paid no «dividend» when we took control in 1965, have become a position that provides billions of dollars annually to the federal government.

.

Last year, however, the 40% on the government’s «holding» (14/35) was refunded to Berkshire when the corporation tax rate was reduced to 21%. Consequently, our «A» and «B» shareholders saw a significant increase in the profit attributable to their shares.

.

This development substantially increased the intrinsic value of the Berkshire shares that you and I hold. Furthermore, it also increased the intrinsic value of almost all the shares held by Berkshire.

.

The tax benefits derived from our large utilities business were passed on to customers. Meanwhile, the tax rate applicable to the substantial dividends we receive from domestic businesses remained virtually unchanged, at around 13.1%. (This lower rate has long been logical because its subsidiaries already pay tax on the profit they subsequently distribute to the parent company.) Overall, the new laws have made the companies and shares we own considerably more valuable.

.

Nevertheless, his gratitude towards the US is absolute, for without the dynamism and growth of its economy, he could never have amassed such a fortune. Whilst the Germans predicted the success of their troops during the war, the Americans were confident that their children and heirs would inherit a better world. The education of subsequent generations has been one of the keys to the US’s success in leading the global economy over the last century (remember what the economist Gay de Liébana on the merits of sending our children to study at American universitiesand the affordable costs that can be found with the right advice).

.

Speaking of the accounting tricks that some executives routinely employ, Buffett said:

.

Over the years, Charlie and I have seen all manner of corporate malpractice—both accounting and operational—driven by management’s desire to meet Wall Street’s expectations. What starts as an «innocent» lie to avoid disappointing analysts (such as «padding» sales at the end of the quarter, turning a blind eye to insurance losses or withdrawing profits from our «slush fund») can actually be the first step towards outright fraud. The CEO’s intention may be to fiddle the accounts «just this once», but it is rare for it to be just once. And if it is acceptable for the boss to cut corners, it is easy for his subordinates to adopt similar behaviour.

.

On the need for BRK to have financial clout and the risks faced by companies seeking financing, Buffett and Munger came out with the following gem:

.

The Russian roulette equation (you usually win, sometimes you die) might make financial sense for someone who benefits from a company’s good news but doesn’t suffer from the bad. This strategy would be madness for Berkshire; sensible people do not risk what they have and need for what they do not have and do not need.

.

Buffett acknowledged that his fortune has been built almost exclusively on the growth and economic leadership of the US. However, he also noted that the world’s economic centre of gravity is shifting towards certain emerging economies, as in the coming years growth, coupled with the maturity of these markets, will no longer be the exclusive preserve of the US economy (it is worth noting here the investment guidelines Mark Mobius gave us a few weeks ago):

.

There are also other countries around the world with bright futures. We should be pleased about this: we Americans will be more prosperous and safer if all nations prosper. At Berkshire, we look forward to investing large sums of money abroad.

.

To round things off, here’s a medley of quotes and jokes taken from the letter to shareholders:

.

Abraham Lincoln once posed the question: «If you call a dog’s tail a leg, how many legs does it have?» And then he answered his own question: «Four, because calling a tail a leg doesn’t make it one.» Lincoln would have been misunderstood on Wall Street (there they would have argued over whether the dog has one or five).

Even at the ages of 88 and 95 (I’m the younger one), that hope (of making a purchase) is what makes my heart and Charlie’s race. (Just writing about the possibility of a big purchase has set my pulse racing.).

My plan to buy more shares is not a prediction of how the market will perform. Charlie and I have no idea how shares will perform next week or next year. We have never been interested in making that sort of prediction. Our focus, rather, is on calculating whether a stake in a good business is worth more than the market price suggests.

Forget it: it would be foolish to sell any of our wonderful companies, even if the sale were tax-free. Good companies are extremely hard to come by. Selling a business that you’re lucky enough to own makes no sense at all.

As things stand, Charlie and I have no interest in joining that group (people who are divesting). Perhaps we’ll become spendthrifts when we reach old age.

However, some investors may disagree with our valuation, whilst others may have found investments they consider more attractive than Berkshire shares. Some of those in the latter group will be right: there are undoubtedly many shares that will deliver returns far higher than ours.

A major disaster will strike that will make Hurricanes Katrina and Michael look like a joke – perhaps tomorrow, or perhaps decades from now. «The big mistake» could stem from a traditional source, such as a hurricane or an earthquake, or it could be a complete surprise involving, say, a cyberattack with disastrous consequences that insurers do not currently anticipate. When such a catastrophe strikes, we will bear our share of the losses, and they will be huge, absolutely huge. However, unlike many other insurers, we will be looking to acquire businesses the very next day.

In late 1995, after Tony had revitalised GEICO, Berkshire made an offer to buy the remaining 50% of the company for $2.3 billion, roughly 50 times what we paid for the first half (and people say I’m a tightwad!).

Christopher Wren, the architect of St Paul’s Cathedral, is buried inside this London church. On his tomb are the following words (translated from Latin): «If you seek my monument, look around you». Sceptics regarding the US economy would do well to heed this message.

For 54 years, Charlie and I have loved our jobs. Every day, we do what we find interesting, working with people we like and trust. And now our new management structure has made our lives even more enjoyable.

With everything in place—that is, with Ajit and Greg at the helm of operations, a strong business portfolio, a cash flow as robust as Niagara Falls, a team of talented managers and a strong corporate culture, your company is well-positioned for whatever the future may hold.

Berkshire paid $47 million for half of GEICO, roughly the same as what a luxury flat in New York would cost today.

Every year it is becoming more and more common for Spanish families to consider sending their children to study at American universities. Despite this, many still have the misconception that it is a luxury reserved for an elite of millionaires and/or gifted eggheads. However, study at a university in the USA is not difficult at all, and the reasons for sending our children to universities in the USA are multiple and justified. For example, the international prestige of a degree from a university there is far superior to that of comparable alternatives in Spain. It should also be borne in mind that the likelihood of finding more and better jobs upon return, either in the USA itself or in any other country in the world, is much higher with a US degree. As for personal experience, no doubt, living inside of a university that is like a real city in its own right, with its own flats, restaurants, cinemas, concert halls, sports stadiums, shops, gyms, libraries, banks or police, has no comparison with simply attend classes at a Spanish university.

The renowned economist Gay de Liébana he said last week in one of his lectures to an audience essentially made up of parents of teenagers: Families who are able to send their children to study at prestigious universities in talent-receiving countries will be doing them a huge favour, as they will have many more tools and contacts to shine in their professional future. On the other hand, the talents that remain in the Spanish university system will, unfortunately, have a much more difficult time and will probably fade away, becoming part of the multitude of young people who end up doing jobs that are much lower than what they would be entitled to for their extremely well-rounded university degrees. The Spanish economy and its university system and labour market cannot cope. His slogan was clear, parents who can materially push their children to fly through universities in countries like the US, where R&D budgets are infinitely higher than in Spain, will do the right thing.. As a significant fact, he explained that a single company such as Amazon spends more than twice as much money annually on R&D as the whole of Spain. Gay de Liébana himself has a son who trained and lives in Los Angeles, and his father could not be more satisfied with the effort made. Let us now turn to money and then we will explain accessibility for Spanish families of different purchasing power.

.

The budgets that American universities manage for facilities, research, faculty, student government and other internal operations are light years ahead of what is possible in our universities. There, it is very common for former students who have made a fortune over the years as entrepreneurs, in gratitude to the university that trained them academically and personally (their alma mater), donate millions of dollars. Thus, in addition to the income that universities receive from tuition fees, room rentals, maintenance and public subsidies, they also receive astronomical donations that allow them to provide specific scholarships or to build entire buildings to house all kinds of resources that donors want for their students. Because of all these abundant sources of income, most American universities are constantly expanding, improving their facilities, faculty and services year after year, because compete fiercely with each other to attract more and better students.

The million-dollar question in the title of this article is: Can I really send my children to a university in the USA? Most families would think that only an elite group with extremely bright sons or daughters can get enough scholarships to study there, unless the parents are millionaires and can afford to pay huge sums. But they are wrong. The flexibility of the American university system allows foreign families to access academic scholarships that are relatively suitable for any good student.. This is a true policy of attracting universal talent. Let's say that with a remarkably high average of the last 4 years of studies in Spain, that is, from 3rd ESO to 2nd Bachillerato, with grades between 7 and 9 out of 10, you can find scholarships that cover a very substantial part of the cost of tuition fees. Obviously there is also the cost of room and board for the student, but this is comparable to the cost of any student from here attending a university in a Spanish city other than their own, which would require them to pay for a student flat and daily meals.

.

Another way to access scholarships at American universities is for our son or daughter to have a good level in any sport, to have played it for some years and to be federated. In other words, they must have a demonstrable track record in sport, having competed in a local amateur league and, logically, have a certain ability that makes them stand out from the crowd. In addition, both scholarships are compatible, so you can have access to sports scholarships and also academic scholarships, thus greatly reducing the cost of tuition.

.

As mentioned above, there is total flexibility, i.e. there are universities for all tastes and academic levels. For example, a family with a child who has a grade point average in the lower range of the above mentioned can choose to go to a less prestigious university with a higher scholarship, to a higher level university with a small scholarship, or to a top university without a scholarship. The same applies to sports scholarships: If the student's level in his or her sporting discipline is very high, he or she can opt for a less prestigious university practically free of charge or for a more prestigious university paying most of the cost out of pocket. Depending on the circumstances of each student and the willingness and financial capacity of the family, a tailor-made option will be chosen. And of course there are also options for those students who simply pass the baccalaureate with averages of 5-6 out of 10 and do not excel in any sport, but without scholarships, which will force parents to cover the full cost. In fact, studying at a university in the USA is an extraordinary opportunity for the brightest, for simply good students and even for less bright students, who would not be able to reach the cut-off mark to be able to study at a Spanish university the degree they like the most, but could do so at various American universities, thanks to the aforementioned flexibility.

.

Advice and accompaniment throughout the process of preparation, selection and application to American universities is an essential part of the process. service that we have been offering since Cluster Family Office for several years now, not only to clients of our multi-family office, but also to our aanyfamilyinterested. For this purpose we have two specialists (one of them American) who graduated from universities in the USA, who know the secrets of the whole process from start to finish. For families who decide to start their children's path to American universities, we provide them with access to exclusive software that we use together with them as we complete the necessary stages and tasks. And we also maintain throughout the entire process (which can last between 9 and 18 months) constant meetings via skype and/or face-to-face meetings in our offices in Madrid or Barcelona.. They are assisted in the selection process of the universities that best suit them, both in terms of price and scholarships, size, diversity profile, geographical area, climate, rankings in their speciality, etc. Also in the preparation of the dreaded «best fit" lists.«essays«The cost of the service will depend on the needs of each case, but to give you an idea, it can range between 8,750 and 11,250 euros for a complete process, that is to say, between 8,750 and 11,250 euros for a complete process. The cost of the service will depend on the needs of each case, but to give you an idea it can range between 8,750 and 11,250 euros for a complete process, that is to say less than one tenth of what is usually available in academic or sporting scholarships. A cost that also makes the difference between carrying out a practical, resolute process that guarantees receiving at least a couple of letters of acceptance, or throwing oneself into a process that can be very stressful, labyrinthine and doomed to failure, and with the consequent frustration of having dedicated a great deal of effort, time and enthusiasm to a project that will end up with a pile of rejection letters.

.

This whole process of preparation requires a lot of advance notice. In fact, American students start preparing for their university entrance two and three years in advance, althoughthefamiliesSpanishcanhavesufficientiflomakedulyadvisedduringoncoursefrom1ºoincluding2ºfrombaccalaureate (if starting in 2nd year, access to university may not take place in the autumn of the same year as the end of the baccalaureate, but in January of the following year). During all this time the student must demonstrate a sufficient level of English by achieving a minimum grade of TOEFL, The level of the English language proficiency level should be higher or lower, depending on the level of demand of the university to which the student wishes to apply. Students with an insufficient level of English are usually enrolled in adaptation courses, so that they can reach the necessary level within a few months and become acclimatised to university life in the USA. SAT, This is a kind of selectividad exam whose minimum grade required will also depend on the level of demand of the universities to which you wish to apply for admission. Logically, families and students will be helped, trained and accompanied in all these processes.

.

In order for readers to get a practical idea of the costswithout grants The approximate costs that a Spanish student who decides to go to the USA to obtain a degree can assume, here are a few figures per year, The programme is based on a standard academic load, from mid-August to the beginning of May, with 24-30 credits per year and a 4-4.5 year expectation to graduate:

.

Tuition fees:

Between €10,000 and €55,000 depending on the prestige and quality of the university.

Cost of room and board:

Between 8 and 10 thousand euros

Books, materials, travel and miscellaneous expenses:

Between 2 and 3 thousand euros

Health insurance for international students:

Between €1,000 and €2,000

Therefore, if you want to send your child to an American university, you have to calculate logistical costs of between 11 and 15 thousand € per year, plus the annual tuition that depends entirely on the prestige and quality of the university, and all of this could come with a scholarship to a greater or lesser extent as we have already said. As you can see, the costs of room and board are the same as what it would cost to send our children to study in any city in Spain. And the annual tuition fees can be perfectly equivalent to the tuition fees in some private Spanish universities, even without access to any scholarship. SEE ALL THE COSTS AND DETAILS OF THE PROCESS HERE

.

Here you will find a example of housing where students from Arizona State University live. It is obvious that the atmosphere and quality of life is light years away from the student flats that university students usually rent during their studies in any city in Spain.

.

We have already seen in the price table above that with some scholarships, and even without any, the costs of sending our children to universities in the USA are affordable for many more families than we might think. However, it is undoubtedly an effort and financial sacrifice on the part of the family towards their children. But there is no better inheritance than to give them the best possible education during their lifetime so that they can defend themselves before the world with the best weapons and the most prestigious qualifications. Wouldn't it be infinitely more useful and profitable for them that we have paid for their studies at the best universities on the planet than to have left them a handful more money in our will? From our experience in the formation of heirs and the relationship of the new generations with the family heritage, we can assure you that this is the case. If our children are to make their way in the difficult world they will have to face, it will be of little use to them if we leave them only a basket full of fish as an inheritance. We must provide them with the best fishing rod, the best equipment and the best fishing instructors. And their training must enable them to find the most fish-filled international waters and to move in them with complete ease. That will be our greatest legacy.

.

One of the most important benefits of the whole application process is that, during the months of preparation, the pupils will give a huge qualitative leap in maturity and motivation. Their personality will mature due to the process of internal reflection that the pupils will go through as they work on their Essays with our coaches. They will have to explain in essays of only 500 to 600 words who they are and why the university should choose them over other candidates. What personal merits they have accumulated in their short life and what they want to make of it in their future. They will become aware of the high level of competition for admission to the university of their dreams (don't worry, the final list of universities to which they will apply will include options accessible to the student and no one will ever be left without at least one letter of admission). This whole process will make them appreciate much more and much better the financial effort made by their parents for them. For the first time in their lives, they will have to analyse who they are and present their best version of themselves to the world in order to be worthy of the prize of receiving an admission letter. Here we leave you a few videos with some of the emotional reactions of students when they receive the news that they have been admitted to the university of their choice. These videos which abound on YouTube, will give you an idea of what it means, for the teenagers who choose the American university path and for the whole family, to be rewarded at the end of the whole process of effort. You will not tire of watching them. When that time comes, we can guarantee that your children will have grown a great deal personally compared to when they started their journey 9, 12 or 18 months ago.

.

Applying to American universities is the best personal growth process they can undergo, and it will come at the best time in their lives (between the ages of 15 and 18) to make the leap in maturity they need.

For the investor, the definition of risk linked to volatility is not only misleading but also totally counterproductive. However, a large part of the financial sector and practically the entire banking sector determine - legally and in practice - the risk of investments through their volatility: The higher the volatility, the higher the risk (sic) and vice versa. But the worst thing is that this is how they qualify the risk profile of their clients, a profile that will determine the assets in which they will be able to invest, according to this volatility. As a result, we find aberrations such as considering an insolvent and expensive fixed income portfolio as a proposal suitable for conservative profiles. And we see how many investors are deprived of buying stocks simply because valuations are volatile in the short or medium term. And it does not matter to them that over the medium to long term the certainty of stock market returns is much, much higher than the likelihood that the bonds in the insolvent and expensive fixed income portfolio will return principal and interest without anycredit event (unless bailouts with public money, which we will pay back in the future in the form of taxes, avoid permanent losses, as we have seen in the last decade).

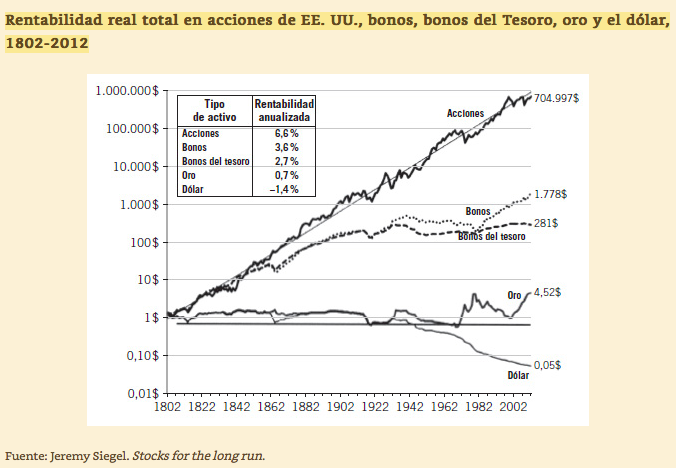

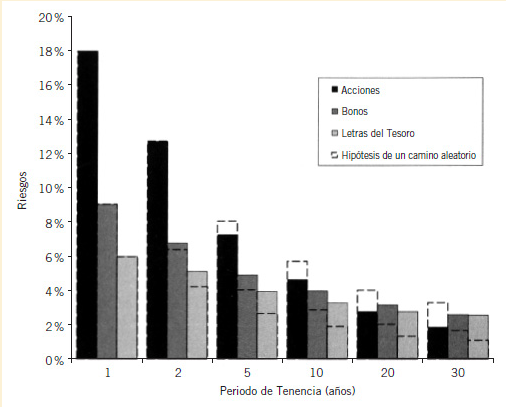

Francisco García Paramés explains it perfectly in his book «...".«Investing for the long term«From it we have extracted the graphs, which are devastating in terms of the fallacies instilled in investors by a large part of the banking and financial sector. As you can see in the graph above, the risk of long-term stock market losses is nil, while the risk of permanent losses in fixed income persists. Moreover, even volatility is lower over the long term in equities! In other words, by investing passively in listed equities, we will not only achieve higher returns over the long term, but we will do so with lower volatility and no downside risk. If we also do so actively through managers of bright backgrounds that outperform benchmarks on a consistent and sustained basis over time, we conclude that this is our best option as investors who want to preserve and grow our investments over the long term.

.

This is and should be the investment criterion: to preserve and increase our financial capital while avoiding permanent losses. What is a permanent loss? It is a loss from which we will not be able to recover before the opportunity cost, currency devaluation and inflation eat us to death.. In other words, a loss that will reduce the progression of our wealth so decisively that only inflation, devaluation and the passage of many years will allow us to recover it in nominal terms, but which will have crippled our purchasing power over a large part of our investment life. For example, a permanent loss is a credit event on a bond or debt asset, or the purchase of a property or share in the middle of a price bubble. In other words, paying far more for an asset than it is worth and will be worth for many years to come. Although obvious, it is worth remembering that a permanent loss is not a temporary short-term loss. Short-term temporary loss is simply volatility that affects us momentarily in an apparently negative way, but which will be recovered with greater or lesser speed depending on the intrinsic value of the asset relative to the fall in price.. And we say «apparently negative» because, as we shall see below, such a permanent loss provides us with golden opportunities.

Here are a few examples of the difference in risk that the same volatility can have, taken from the reflections of Didier Darcet about it. Let's say three neighbouring homeowners in the same neighbourhood, with three identical houses, suffer a major fire in the neighbourhood that completely destroys their properties. They thus have the same initial volatility, since their assets have depreciated identically in value and time:

.

The former has no insurance to compensate him for the losses, so he will suffer them permanently. It is true that over time inflation and the devaluation of your currency can make your empty plot of land worth nominally the same as your house was worth before the fire. But that inflation/devaluation and the opportunity cost squandered over a good part of his investment life will mean that his losses will have been permanent despite recovering the same nominal amount of money over time. For this first neighbour, suffering a fire was a real risk. And after the trauma he will probably decide to sell his plot of land unthinkingly or out of necessity, to move to another cheaper neighbourhood or to a rented house, where he believes he is safer from future risks.

The second neighbour does have fire insurance equivalent to the cost of building the house, so, say in the medium term, he can replace the asset and recover the loss suffered in the short term. Therefore, although he has the same short and medium-term volatility as the first neighbour, his risk would be virtually nullified by insurance. Some would say that he is a homeowner with no medium/long-term risk, but with undeniable volatility if a loss occurs. Would such a homeowner consider that he is at risk of losing part of his equity? In the short term yes, but no one in their right mind should consider them to be a risky owner or risk taker, if they are insured and will be recoverable with full certainty in the medium to long term.