For the investor, the definition of risk linked to volatility is not only misleading but also totally counterproductive. However, a large part of the financial sector and practically the entire banking sector determine - legally and in practice - the risk of investments through their volatility: The higher the volatility, the higher the risk (sic) and vice versa. But the worst thing is that this is how they qualify the risk profile of their clients, a profile that will determine the assets in which they will be able to invest, according to this volatility. As a result, we find aberrations such as considering an insolvent and expensive fixed income portfolio as a proposal suitable for conservative profiles. And we see how many investors are deprived of buying stocks simply because valuations are volatile in the short or medium term. And it does not matter to them that over the medium to long term the certainty of stock market returns is much, much higher than the likelihood that the bonds in the insolvent and expensive fixed income portfolio will return principal and interest without any credit event (unless bailouts with public money, which we will pay back in the future in the form of taxes, avoid permanent losses, as we have seen in the last decade).

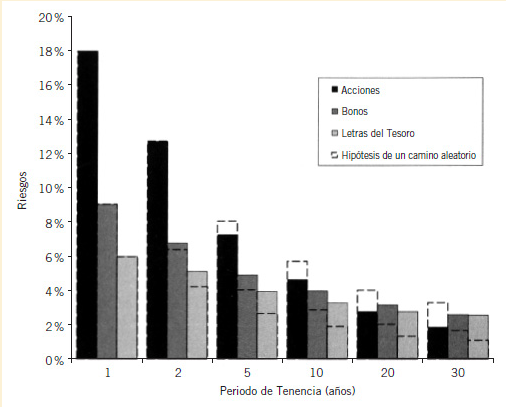

Francisco García Paramés explains it perfectly in his book «...".«Investing for the long term«From it we have extracted the graphs, which are devastating in terms of the fallacies instilled in investors by a large part of the banking and financial sector. As you can see in the graph above, the risk of long-term stock market losses is nil, while the risk of permanent losses in fixed income persists. Moreover, even volatility is lower over the long term in equities! In other words, by investing passively in listed equities, we will not only achieve higher returns over the long term, but we will do so with lower volatility and no downside risk. If we also do so actively through managers of bright backgrounds that outperform benchmarks on a consistent and sustained basis over time, we conclude that this is our best option as investors who want to preserve and grow our investments over the long term.

.

Here are a few examples of the difference in risk that the same volatility can have, taken from the reflections of Didier Darcet about it. Let's say three neighbouring homeowners in the same neighbourhood, with three identical houses, suffer a major fire in the neighbourhood that completely destroys their properties. They thus have the same initial volatility, since their assets have depreciated identically in value and time:

.

- The former has no insurance to compensate him for the losses, so he will suffer them permanently. It is true that over time inflation and the devaluation of your currency can make your empty plot of land worth nominally the same as your house was worth before the fire. But that inflation/devaluation and the opportunity cost squandered over a good part of his investment life will mean that his losses will have been permanent despite recovering the same nominal amount of money over time. For this first neighbour, suffering a fire was a real risk. And after the trauma he will probably decide to sell his plot of land unthinkingly or out of necessity, to move to another cheaper neighbourhood or to a rented house, where he believes he is safer from future risks.

- The second neighbour does have fire insurance equivalent to the cost of building the house, so, say in the medium term, he can replace the asset and recover the loss suffered in the short term. Therefore, although he has the same short and medium-term volatility as the first neighbour, his risk would be virtually nullified by insurance. Some would say that he is a homeowner with no medium/long-term risk, but with undeniable volatility if a loss occurs. Would such a homeowner consider that he is at risk of losing part of his equity? In the short term yes, but no one in their right mind should consider them to be a risky owner or risk taker, if they are insured and will be recoverable with full certainty in the medium to long term.

- The third owner also has insurance that covers the cost of construction and will allow him to replace his house. But he will also want and be able to take advantage of the current circumstances, and will buy his uninsured neighbour's plot at a good price, taking advantage of the need and/or fear that the latter may have because of the fire (temporary loss or volatility) suffered in the neighbourhood. Therefore, he will convert his temporary loss into a higher profit in the medium and long term. And the most curious thing is that the volatility of this third case will be even higher in the short and medium term than that of the two previous cases, while maintaining practically zero risk. In the case of a financial investor, buying the neighbour's house would be the equivalent of buying back more shares of good Value funds or shares of extraordinarily cheap companies, i.e. taking advantage of the fear and/or need of others to buy assets with high Value at a low price.

Here it is worth remembering that the first graph is based on investors (owners) as the second neighbour, i.e. they will recover their temporary losses in the medium and long term. But imagine now what this same graph would look like if the investor is also able to take advantage of moments of volatility (of fire) to invest more and additionally buy assets at unusually low prices. Obviously, recoveries from temporary losses would be much faster, dramatically shortening short-term loss periods and very substantially increasing long-term returns. This is easy to say but difficult to do, as the natural primitive impulse is to flee from loss-making assets, like the first neighbour flees the neighbourhood where there has been a fire.

.

Readers should therefore consider their financial investments in the same way as the third neighbour, provided they are able to invest in actively managed funds that consistently and permanently outperform indices. If they do so, their volatility and returns will be high, while maintaining zero risk of permanent losses. And if investors are unable to find such funds, they can always emulate the second neighbour through passively managed funds, assuming short to medium-term volatility in exchange for zero risk of permanent losses.

.