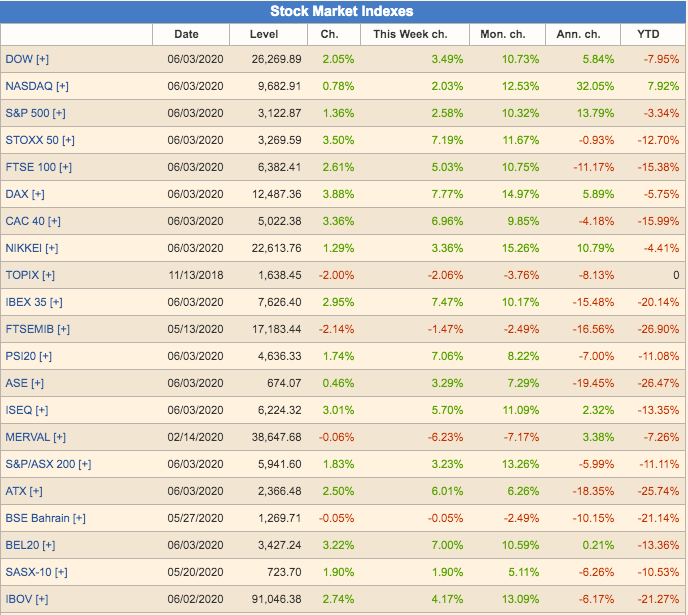

It is true that as of 3 June 2020 the S&P 500 is at -4% from the start of the year, the Dow Jones is at -9%, the German DAX is at -7% and the Hong Kong stock exchange is still at -15% YTD. It is also true that the stock markets of other countries are even further behind, such as those of Brazil, India, Russia, Indonesia or European countries like France, the UK, Italy or Spain. However, there are others which, to the surprise of many, are already at -2% levels, such as Japan or clearly in positive territory, such as Denmark.

.

And not all investment possibilities are limited to matching the general reference indices of the countries, which as you can see on any website like this one, are still quite red in general. We can find some sectoral indices such as the Healthcare, Biotech or the very same Nasdaq with positive returns, despite the travails of this fateful year.

.

But of course, having a portfolio full of international index funds or etfs, replicating only consistently winning sector indices, is almost as difficult as choosing a portfolio of world stocks that outperforms the market year after year.

Another possibility for the investor is to choose good actively managed funds that have managed to outperform their respective benchmarks for many years and are therefore already making money, net of fees, for their investors. The problem is that for the vast majority of retail investors (according to the unfortunate nomenclature used by Spanish regulation), finding funds that achieve substantial alpha and outperform their indices on a consistent and sustained basis over time is often as difficult, if not more so, than getting winning stocks or sector indices right.

.

Here it is worth recalling what we explained in «Why big international investors don't invest in the same funds as you do»The "outperformance" of funds that consistently outperform their benchmark indices. There are some, but investors must have a portfolio size of several million to exceed the minimum requirements of these funds for professional or institutional investors.

.

Fortunately, they can also be accessed through the back door, i.e. through the luxembourg funds of funds 125,000, as Luxembourg law considers a professional (non-retail) investor to be a professional investor above this minimum investment amount, and they aggregate sufficient volume to meet the minimums required by each institutional fund. Logically, the composition of these portfolios of funds of funds for professionals or institutional investors may be of higher or lower quality, outperforming or not the respective benchmark indices, since they obviously involve a fee in addition to the net returns obtained by the underlying institutional funds. It should not escape anyone's attention that being a fund for professional investors does not guarantee that it will outperform its respective index, as mediocrity is also rife among institutional funds. That said, the Luxembourg fund of funds that we have been using for our smaller Clients has also entered positive territory this week, in terms of net returns for the investor of course.

Therefore, those who are still negative so far this year could have done better, as there are options to invest a minimum of 125,000 euros and outperform the major international indices in terms of net returns. And that outperformance, that systematic cutting back in days weeks or months in the recovery period of losses generated by sell-offs like the one last March makes a huge difference to the performance we will achieve in the long run.. Because the quality of a fund or a portfolio management is not - only - measured by a lower fall in periods of crash or a higher rise in periods of euphoria, but above all by the quality of the fund or portfolio management. the speed of recovery of losses after a generalised drawdown. That is the key to those that consistently and permanently outperform the indices, and the degree to which they achieve this is critical to our earnings performance in the years ahead (of course it would also be critical to our performance to invest more in crash periods at rock bottom prices, but we have already discussed that). in the middle of a storm stock market).

.

That is why it is not the same to start making money in 2020 as early as 3 June, before the major general indices of the world's main stock exchanges, as it is to start making money at the end of the month, during the summer or even later. Y Market conditions in 2020 are the best test to take the pulse of the quality of our portfolios.. Obviously the markets will go up and down and up again in the coming weeks, and every day the numbers will dance enormously. But whoever is still in negative YTD today, either with portfolios of self-selected stocks, or with portfolios of passively managed sector funds or actively managed funds, should not be cheating himself, he could have done better.

The Wall Street Journal's special senior columnist, Justin Baer, published this article last week in WSJ which gives a perfect account of what happened behind the scenes of the financial markets the week of 16 March, in the midst of the Coronavirus Crash. The summary account of what happened is as follows, certainly worthy of the best scriptwriter of Hollywood Netflix.

.

Ronald O'Hanley, chief executive of State Street Corp, received an urgent call as soon as he sat down at his desk in his downtown Boston office. It was 8 a.m. on Monday, March 16, 2020. One of his senior managers told him that pension fund managers and treasurers at major companies, panicking about the economic damage that the Covid19 pandemic could have beyond the obvious, were withdrawing billions of dollars from money funds. This was forcing those funds to sell some of the bonds they held in their portfolios. But there were hardly any buyers. Everyone was suddenly desperate to cash in.

.

He and senior executive manager Cyrus Taraporevala had been talking the night before, trying to get a sense of how investors would react to the new deal. emergency rate cut by the Federal Reserve. Now they had the answer. In his 34 years of experience in the world of finance, Mr. O'Hanley had survived many battles in the markets, but none like this one. «The market is fearing the worst,» Mr. O'Hanley told Taraporevala.

.

16 March was the day when a microscopic virus brought the financial system to the edge of the abyss. Few realised how close we had come to plunging into the abyss.

The major money funds, where large institutional investors stash their money and buy huge amounts of short-term corporate debt - normally safe and boring - had outflows of $60 billion in that week, according to the money data agency Refinitiv. One of the biggest bleed-offs in history.

.

Interest rates on short-term corporate debt soared, surpassing the federal funds rate by 2.43 percentage points. Its highest level since October 2008, according to the Federal Reserve Bank of St. Louis.

.

The financial system has endured numerous credit crunches -or events in which liquidity disappears - and there have also been numerous crashes stock market. But seasoned investors and those who have Wall Street as their modus vivendi say that what they experienced in mid-March was most severe and withering. The stress on the financial system was greater than many had ever seen.

.

«The 2008 financial crisis was a slow-motion car crash compared with this,» said Adam Lollos, head of short-term credit at Citigroup Inc. «This has been like, ‘Boom!'».

.

The emergency levees of state programmes have long been preventing collapse. And what happened on one of the worst days ever experienced by financial markets shows that all efforts were more than justified and urgent.

.

The Fed set the stage on Sunday 15 March. Investors expected the central bank to announce its response to the crisis the following Wednesday. Instead, the FED announced at 5pm on Sunday afternoon that it was plunging interest rates and planned to buy $700 billion in bonds to unclog the markets. Perhaps the latest change of Fed chair, with Jerome Powella at the helm, did not help to provide reassurance either.

Traders monitor the opening at the New York Stock Exchange on Monday morning, March 16.

Instead of reassuring them, companies, governments, bankers and investors saw this decision as a signal to prepare for the worst-case scenario of the coronavirus pandemic. The drop in bond prices turned into a stampede.

.

Mr O'Hanley was in a good position all the same. His entity is an essential provider of administrative and accounting services to most of the major investors, and has its own giant asset management company.

Ronald O'Hanley, chief executive of State Street Corp.

Companies and pension fund managers have relied on money market funds that invest in short-term corporate debt and municipal debt holdings, which are considered safe enough to be classified as «...".«cash equivalents«. They function almost like a current account, helping businesses to manage their payments and finance their daily cash requirements.

.

But on that Monday, investors no longer considered certain money market funds to be equivalent to cash at all. As soon as everyone who was able to get their money out of it had done so, managers were no longer able to sell bonds to meet the outflows.

.

In theory, the system was supposed to be more fluid in these situations, as US regulators reworked the rules after the 2008 financial crisis. But those new rules could not stop such a panic assault. Rumours circulated that some of State Street's rivals had been forced to inject money into their funds. Within days, both Goldman Sachs and Bank of New York Mellon began buying assets from their own money funds. Both banks have declined to comment.

.

That was bad news not only for those funds and their investors, but also for the thousands of businesses and communities dependent on short-term debt markets to pay their employees. «If junk bonds collapse, people can understand and assume that,» Mr. O'Hanley said. «But there is no way to rationalise collapsing money funds and cash equivalents.».

.

A debt investment unit of Prudential Financial Inc., one of the world's largest insurers, also had serious difficulties with typically safe assets.

.

When PGIM Fixed Income traders tried to sell a batch of short-term bonds issued by highly rated companies that Monday, they found very few buyers. And banks were suddenly refusing to act as intermediaries as well.

A Bank of New York Mellon Corp. office building in New York.

«The community broker-dealer had frozen,» said Michael Collins, a senior fixed income manager at PGIM. «The situation was as bad as it was at the worst of the financial crisis.

.

In southern California, the head of debt trading at investment firm Capital Group Cos, Vikram Rao, was trying to find an explanation for the dysfunction. Mr Rao, who was teleworking that Monday, descended the 20 steps to his home office at 4:30 a.m. and discovered that the debt markets were off the rails. He started calling all the senior Wall Street managers he knew who worked in key positions in big banking.

Michael Collins, a senior investment officer at PGIM Fixed Income.

Executives told him that the massive rate cut the Fed had announced just hours earlier had blown up interest rate swaps in favour of banks. Companies had anchored themselves to pre-crash rates for the past year to lock in future debt. But when rates fell that Monday, companies suddenly owed banks additional collateral that they could not afford.

.

On that very Monday, banks were to book these new collaterals as assets on their books, with no room for manoeuvre.

.

So when Mr Rao called management to explain why they were unwilling to accept his operations, the answer was always the same. There was no capacity to buy bonds and other assets and still comply with the new directives imposed by regulators after the 2008 financial crisis. In other words, the capital rules that regulators imposed more than a decade ago to make the financial system more robust were, at least this time, further limiting the liquidity of the Markets. One of the managers put it bluntly: «We cannot make an offer for any assets that are added to our balance sheet at this time».

.

At the same time, increased stock market volatility, together with plummeting mortgage debt prices, forced the margin calls of many investment funds. This additional collateral owed to the banks was also added as assets to their balance sheets, thus adding more and more billions.

.

The collapse of mortgage bonds was so widespread that it also crunched one group of investors who had borrowed from banks to leverage their expected profits: real estate funds.

.

The Fed's bond-buying programme, made public that Sunday, spoke of 200 billion in mortgage bond purchases. But already on Monday managers discovered that, despite the good intentions, the Fed's figure was far too low.

.

«On that first day, the market already totally ran roughshod over the Fed,» said Dan Ivascyn, who manages one of the largest bond funds as chief investment officer at Pacific Investment Management Co (PIMCO). «This is where REITs and other leveraged mortgage products started to get into serious trouble.

.

On Tuesday, UBS Group AG closed two exchange-traded notes (ETNs) linked to real estate mortgage investment trusts. By Friday, a mortgage trust managed by hedge fund Angelo Gordon & Co. had already warned its creditors that it would not be able to meet its futures margin calls.

Jerome Powell, chairman of the U.S. Federal Reserve, at a news conference in Washington, D.C.

Panicked investors threw municipal debt into the market at any price, dealers cancelled billions of dollars of deals and new lending came to a screeching halt. There was less bond issuance in the week of 16 March than at any time during the 2008 financial crisis, the terrorist attack on the twin towers in 2001 or the black week of the 1987 crash and its Black Monday, according to Refinitiv's inflation-adjusted data.

.

In those few days in March, investors lost all faith in American public infrastructure. As schools and universities closed and airports and public transport systems emptied, the market began to question what had hitherto been safe bets on the major institutions that weave the fabric of American community life.

.

The peak of the market collapse was clearly in the early hours of 16 March.

.

Cities and states often rely on short-term debt that they issue through bond dealers, who in turn resell the asset to investors. Billions of dollars of such paper were floated the next day. Interest rates, which had been around 1.28%, could reach levels of 6%.

.

At the same time, trading in long-term municipal bonds disappeared from the market. During the week, Citigroup Inc, the second largest dealer in the municipal bond market, did not issue a single bond.

.

Staff in Citigroup's municipal debt market division worked from various locations that day, some from their homes, some from the bank's Manhattan headquarters and a few from the replacement office in Rurherford, NJ. Throughout the day, Citi representatives called state and local government finance officials to tell them the bad news: Their short-term borrowing costs had skyrocketed, and long-term operations had ground to a complete halt.

.

Patrick Brett, head of the firm's municipal debt capital markets, was making his calls from a rustic-style house in a Catskills forest. He had booked that Airbnb in March, just days after the head of the Port Authority of New York and New Jersey, one of the largest issuers of municipal debt, publicly confirmed he had tested positive for the coronavirus.

.

That weekend Mr. Brett and his family left Brooklyn in his grey Chevy Suburban, which was so heavily loaded that even his father-in-law carried packages of toilet paper rolls on his lap.

.

From a makeshift office, he spent all day Monday hanging on the phone. That night he thought what was happening was worse than in 2008. «I don't think anyone alive has ever experienced anything so violent in the financial markets,» he said in an email to the Wall Street Journal.

.

Citi bankers contacted Larry Hammel, chief financial officer of the Forsyth County school district, as the municipal debt market had dried up in the previous weeks. The district was scheduled to place $150 million in bonds on 17 March in order to continue construction of four new must-build schools.

Patrick Brett, head of municipal debt capital markets at Citigroup, works the phones in his makeshift office in the Catskills.

When Citi recommended postponing the operation for a while, Mr Hammel gathered his assistants and crunched the numbers. Without the cash injection, which was to be financed by public debt, construction would stop in July.

.

«It's one of those days when you don't know whether to throw yourself at the train or the engineer,» Mr Hammel said.

.

He started negotiating with a local bank to see if they could guarantee a bridge loan that would allow them to finance the work. Finally, on 30 March, the bonds found buyers, mainly thanks to government programmes that rescued markets from disaster.

.

Panic over the lack of liquidity quickly spread to the stock markets. Thomas Peterffy, president of Interactive Brokers group, an online brokerage platform popular with traders, found it hard to sleep on Sunday night. Early on Monday a call confirmed that futures had fallen by 5%, the maximum allowed in a single session.

.

As Mr. Peterffy began his day Monday morning from his home in Palm Beach, Fla., many investors had already been forced to sell their positions because they did not have enough liquidity to keep them open.

Interactive Brokers Group Chairman Thomas Peterffy.

Time and again Petterfy asked his team how much their clients' accounts were losing, and how much that might affect Ineractive Brokers if the disaster continued.

.

«The more the day goes on, the more and more positions are liquidated,» the team confessed to Mr Peterffy. In addition to the carnage, Mr Peterffy said, there were many options betting against volatility.

.

For more than a decade, the markets have been generally calm. And the conventional wisdom among traders large and small was that they would remain so. But volatility had been rising since the end of February.. On 16 March it was triggered.

.

The Cboe Volatility Index, known on Wall Street as the Fear Index, catapulted during the day, closing at an all-time high of 82.69.

.

Nor did it help that earlier that morning the Chicago trading floor, where most options are bought and sold, had to close. Fewer and fewer trading floors full of human brokers shouting and waving at the world, but the corridors of Cboe Global Markets maintain that frenetic daily grind.

.

Cboe took the decision to close the trading floor on Thursday as a precautionary measure, and executives spent all day Saturday working with brokers to check that the electronic market to be launched on Monday would work properly. The tests went well, but Sunday's massive sell-off in the futures markets complicated matters, said Chris Isaacson, head of trading at Cboe. After S&P 500 futures made their biggest drop ever, the Cboe opted to delay pre-market trading.

.

While the Cboe had sent most of its employees to work from home that week, Mr Isaacson went to the Kansas City offices that Monday to monitor the market along with operations and IT staff.

.

The massive sell-off in futures left no respite, and so correlated options remained locked all day Monday morning, waiting for the 9:30am opening. By then, Mr Isaacson and his team knew what awaited them: «The market is going to have a very tough opening,» he said.

.

Some options opened promptly only to be blocked a second later, when massive selling triggered their suspension mechanism. «It was one of the most intense mornings of my career,» Mr Isaacson said.

.

Malachite Capital Management, a New York fund, did not make it past Tuesday. On 17 March, the company announced its closure, due to «extremely adverse market conditions in recent weeks». Losses were also extreme for others who had traded on volatility. At JD Capital Management LLC, a manager run by Goldman Sachs veteran J. David Rogers, its Tempo Volatility Fund lost more than 75% in March.

.

On the same Monday, traders at Allianz Global Investors, a management company owned by the German insurance giant, were struggling to restructure their own collection of disastrous options.

.

The Allianz Structured Alpha funds have been great sellers of insurance against market sell-offs in the short term, as well as buyers in the long term. The strategy has been generating steady income, as the fund earned premiums from investors who wanted to hedge against potential downturns. The funds could lose money for a month on the back of a sell-off while restructuring their portfolio in the short term, but in the long term they would gain, fund manager Greg Tournant said during a video advertisement in May 2016.

.

«We are acting like an insurance company, collecting premiums,» Mr Tournant said. «When there is a catastrophic event, we may have to pay a lot, just like any insurance company. But we take positions to protect ourselves from those catastrophic shocks, sort of like reinsurance.».

.

When the hurricane hit last March, their strategy did not work.

.

As soon as the options contracts collapsed, Allianz managers tried to restructure their positions. They tried to hold on, but did not expect such speed in the downward spiral.

.

On 25 March, Allianz informed investors that two of its Structured Alpha funds managing almost $2.3 billion were to be liquidated.

.

Allianz management confirmed to investors that one of the funds had fallen by 97% since the start of the year. Even after the 25 March conference call with investors, some investors still did not understand what had gone wrong.

.

Allianz did not say how much money investors would get back, or when they would get it back. They are still waiting.

.

Perhaps the moral of this story is that stocks do better in the face of exceptional events. Because even though their fluctuations may be larger, if they are of quality, their contributions will be recovered much better than other assets insurance when the market breaks them into a thousand pieces.

.

Be very careful about possible contagions, continue to protect your health and take advantage of the investment opportunities.

Film buffs will have recognised the famous line from the title of the article. In one of the most difficult moments of the Apollo 13 odyssey, the Chief Engineer in the control room acknowledges aloud that they are facing what will be the toughest moments in NASA's history, to which the engineer played by the great Ed Harris replies: «...the crew will have to face the toughest moments in the history of NASA.«With all due respect Sir, I think this is going to be our finest hour.«one of the most legendary lines of the film, along with the well-known «Houston, we have a problem».

.

You may be wondering what this film has to do with investments and financial markets. Well, as you may know, it is common for fund and managed account managers to write newsletters and notes to investors in the worst moments of the markets. In them they usually report their view of the crisis situation, try to justify the losses, reason their strategies by reaffirming them or by giving a change of direction, etc. All this in an attempt to reassure investors, thus trying to prevent them from withdrawing their trust - and money - from their fund managers. Such communications abound and are almost obligatory for any self-respecting manager, since it is in difficult times that the relationship between managers and investors needs to be strengthened.

.

This time, however, our attention has been drawn to the letter written by one of the fund managers that form part of the group of funds and asset managers whose due diligence we are currently carrying out at Cluster Family Office, the identity of which you will allow us to reserve for our Clients. The curious thing about this letter, the title of which is the aforementioned phrase from Apollo 13, is that is not addressed to its investors, as would be expected, butto the managers of the companies in which they are invested. We consider this to be extraordinary, as it is not at all usual to address them publicly in times of stock market crisis, let alone in the terms we translate below from the original letter:

«With all due respect Sir, I think this is going to be our finest hour.»

Dear Partner,

We are all going through very difficult times, both in the health, social and economic areas. It is true that we are not «inside your company» and we are aware of our limitations, but we believe that our vision and perception of the situation can bring you something. Our company manages assets for long investors from all continents, with a high sense of fiduciary service and excellence. We have held 483 online meetings in the past few weeks with domestic and foreign companies, always seeking a better understanding of their business prospects in the current environment. If you in your company need any contact with any of the companies we have relationships with, please do not hesitate to let us know, we will be happy to help. At this time, perhaps a view from 30,000 feet, from a team that is studying various international cases and businesses, may be useful to you. In addition, as investors and partners in your business, we would like to tell you the following:

.

The number one priority at this time is to ensure the health of your professional teams and family members. The emotional stress you are all under is enormous, and being there for your staff and their families at this time is extremely important. Be transparent, empathy goes a long way and reinforces the meaning and mission of each employee.

Regarding the coming quarters, all company managers, owners and investors have uncertainties and questions. You are not alone. Visibility for this year is very low. Liquidity is king. We all know that the economy will weaken due to rising unemployment. However, we do not think that everything will be different. There will always be demand for good services and products at good prices. The main needs of consumers will remain the same. There is no need to panic or make ill-considered decisions.

Major crises often precipitate innovation. Trends that already existed will accelerate. We are seeing some companies adapting more nimbly to online commerce and creating digital tools for their businesses. We are excited by the adaptive and innovative capacity of companies and entrepreneurs in our country. We can offer you practical examples from inside and outside our borders.

These are times when it is interesting to rethink structural costs. But do not forget that people are your main asset. We don't want to be proselytising, but remember the time and effort it took you to find and train your professionals. If possible, don't lose your high potential and don't cut the pay of the key players in your company. And if you do, remember that the same cuts should also be applied proportionally to the top management.

In difficult times like these, social, environmental and corporate governance (ESG) marketing and practices may seem superfluous. This is understandable, of course, for companies struggling to stay afloat. However, we believe that ESG practices are even more important now. Consumers, investors and professionals will place an even higher priority on companies that take care of environmental, social and corporate governance practices. So don't forget your shareholders. The way you treat your suppliers, customers, employees, the environment and the community around you will be remembered for a long time to come. The old saying «treat others as you would like to be treated» has never been more relevant.

If possible, you should not only focus on a defensive business position, but it is also time to go on the offensive, as there may be excellent opportunities out there. That company you have always wanted to acquire, or that professional you have always wanted to recruit, may now be more open to talk and listen to your offers.

Stay focused. In times like these, anxiety makes us want to act hastily. Listen to everyone, but don't change too much or burden your team with new and unnecessary requests. Board members tend to ask for a lot and offer few suggestions at times like these. Maintain rigour.

Finally, we would like to emphasise our long-term vision. Do not sacrifice the long term to satisfy short-term investors.

There is a scene in the film Apollo 13 that is worth remembering. The mission is going through a very difficult moment. The «boss» says to his engineers: «This will be Nasa's worst moment”, and one of the engineers (Ed Harris) responds: “With all due respect sir, I believe this will be our finest hour! Moments like this define great leaders.

Good luck! Take good care of yourselves and remember the instructions given in case of emergency on all flights: Put on your oxygen mask first and then help the people sitting next to you to do so. If you are not well, it will be more difficult for you to take care of your families and your equipment.

.

You can count on us. Best regards.

https://youtu.be/OlR17RaMVmM

Not bad, is it? Unfortunately, not all fund managers take such a long-term, protective view of good business. Most of them are just trying to avoid being embarrassed by their benchmarks, a task in which they fail more than 90%. You can find plenty of articles and statistical studies on the ineffectiveness of most active managers by googling (here, here o here). But it is not impossible to find active managers who justify their fees by outperforming their indices in a convincing and sustained manner over time, especially if we eliminate the barrier of 10% of funds marketable in Spain and we can invest freely in the 100% of funds existing all over the world, as we have explained above. here o here.

.

Whether we are entrepreneurs, self-employed or employees, we can all be good investors in difficult times like these. All it takes is a few simple tips, which are otherwise very difficult to follow. Buy when others sell, sell when others buy. And to do so best possible way, outperforming the rates, as the managers who have written this note have been doing for more than 14 years.

,

Now, and for a couple of months now, So it is time to buy and not sell, at least until the shoeshine boy, the lift operator and the neighbour in the 5th floor 2nd floor come back to boast about their investments in the stock market and, of course, are vaccinated.

Those of you who read us regularly will know that we have been saying for years that the Eurozone, as we know it, is neither viable nor sustainable. We warned this almost a decade ago (how time flies!), when the banking crisis was straining the seams of the Eurozone to the limit, and the dreaded Men in Black (MIB) of the Troika were scrutinising the public accounts of the Mediterranean countries of the south. The much-vaunted and politically correct concept of «More Europe» repeatedly hit the wall of the rich and productive North, which preferred a simple and profitable market union to a political, monetary and fiscal union.

.

Thus, the MIBs more or less discreetly shielded the Memorandums of Understanding (MoU) to avoid the free bar that we demanded from the South. Only in exchange for this and the stubbornness of the Eurobureaucrats to kick the can down the road and postpone the moment of truth, the Eurozone went ahead with all its incompatibilities and manifest unsustainability. The hope - in which nobody believed any more - was that with the help of the ECB's QE, and a few years of pseudo-bonanza, the South would, macroeconomically speaking, catch up with the North for once and for all. But the circle has remained unsquared for all these years.

.

The final blow to the economies of the South has come in the form of the SARS-CoV2 coronavirus pandemic, also known as Covid-19 disease. In this mother of all health crises, which is as bloody as it is short-lived, economies as large as Italy or Spain would need a shower of billions in debt (Coronabonds, Eurobonds or whatever you want to call them), which the northern Europeans are not prepared to finance jointly. Paradoxically, this time Merkel is not the standard-bearer of the NO to the free bar but the Netherlands, although it is also true that it is easy for the Germans to play the good cop with the bad Dutch cops. For whatever reason, the South (including France) is trying to take advantage of the final stretch of Merkel's political career to make some desperate concessions in spite of fierce Dutch opposition. The fact is that whatever comes after Merkel is likely to be much less inclined to make concessions to the South, remember the populism that Wolfgang Schaeuble achieved with his proposal to expel Greece from the System. A proposal that, on the other hand, made all the economic sense in the world.

.

Today, what the Netherlands and its circle of influence openly propose is a Europe as a simple common market (sound familiar?). And this idea of the EU coincides with the UK's idea of the EU, which has always been so vilified by Euro-bureaucrats. So this drift towards a «Less Europe» with which the North would feel comfortable could be the way forward, despite the opposition of the countries of the South, since we know that he who pays the piper calls the tune. But there is one small detail that complicates this idea of Europe: the Euro. A Common Market loses much of its meaning and simplicity if the monetary policy of all its members must necessarily be the same. In other words, having the same currency exchange rate, the same price of money (interest rates) and a single issuing bank (ECB), puts us back at the same starting point where we are right now. In other words, the South urgently needs trillions to survive, as well as a depreciation of the currency to regain competitiveness and hopes for growth, but the North is not willing to grant it at the expense of its economies. And this constant refusal is generating the rejection also of the European project by the countries of the South, since they know that the - insufficient - financial aid granted by the North will bring with it the relentless return of the dreaded IMFs, which entail the absolute loss of budgetary, fiscal and economic sovereignty in the countries of the South. The EU seems to be finally facing the final wall of the cul-de-sac along which it has been kicking the can down the road since 2011.

.

The glimmer of lucidity in the face of this permanent flight forward that the coronavirus has precipitated seems to be coming from France. Emmanuel Macron told none other than the Financial Times this week that the pandemic has brought the EU to a «moment of truth».». It is no coincidence that Shahin Vallée, former advisor to the President of the European Council and strongman of the French Ministry of Finance, proposes to create what he calls «the coalition of the will» within the EU. In other words the EU to split into groups according to their intention to evolve towards «More» or «Less» Europe. Thus, countries that want more integration could keep their single currency and monetary policy, giving up sovereignty in exchange for a growing and irreversible fiscal and political union. But what is more curious is that those countries that want less integration, once freed from those who want «More» Europe, could also remain integrated. That is to say that the two incompatible parts would accommodate each other once they are freed from each other, resulting in a Europe not only with two speeds but with two different currency rates, two central banks and two different monetary policies. It would not be a Europe in perfect equilibrium, but it would be much more stable than the unsustainable powder keg in which Covid-19 leaves us.

.

All this could well be covered up under the same Europeanist sheep's clothing, of course. That is to say, using euphemisms that might even keep the less informed in European inopia (continue to call both currencies the Euro, continue to call both issuing banks the ECB, etc.). But there would be undeniable differences, such as, for example, the value of the euro in the southern countries, which could be 20 or 30% lower than the euro in the north. Of course, they would initially be quoted at par, intervened by the ECB, to avoid as far as possible the implementation of corralitos in order to prevent the flight of assets from the south, but they would necessarily drift apart over time. Post-covid19 rates would not diverge in the short or medium term, as everyone needs zero or negative rates at the moment. But in the medium term, Northern Europe could finally follow in the footsteps of the Fed. gradually increased the price of its strong Euro. Maybe we could even see a political and fiscal union beyond the mere common market in one of these - at least - two distinct zones, who knows, since the circle is much easier to square with truly converging economies and a club with fewer members and more common interests.

.

So, how should southern wealthy individuals position themselves in the face of such a post-pandemic scenario? Well, obviously they should avoid accumulating assets in the South or in the South, i.e. avoid having real estate anchored in the less wealthy EU countries (Spain, Italy, Greece, Portugal and even France). Instead, they could hold them in countries that are likely to be able to sell in Euros that are not affected by the depreciation against the Euro in the North. Or hold them directly outside the EU, for example real estate in the USA, buying them still with the only existing Euro and not with the future devalued Euro of the South. As for financial assets, obviously shares of companies from these southern countries should also be avoided in portfolios, and of course their public and private debt. Moreover, as we have said countless times before, and today more emphatically than ever, the more safety steps we can add between our money and the need to collect or confiscatory In the southern states, we will sleep better at night. We must be aware that in times of extreme situations, extreme solutions will be taken, which we would never have foreseen just 6 months ago.

.

What is undeniable is that even if this EU evolution takes more or less time to arrive and Euro-bureaucrats keep banging their heads against reality, this pandemic is going to leave the West's economic and political supremacy mortally wounded. Covid-19 will have a clear winner, if anyone is going to win in this pandemic, and that winner is none other than China. Not only because it has coped and preserved its economy in an exemplary manner during the epidemic, but also because the rest of the world will inevitably set back several years of economic growth. And that will radically accelerate the leadership of China and its very powerful economic orbit (Vietnam, Korea, Malaysia, Australia, Japan, Indonesia, etc., even India itself), making Asia the new centre of the world. It is true that many will say that the figures of contagions and deaths from the coronavirus in China are unreliable. But let's not kid ourselves, because the figures for many Western countries are not reliable either, and very few question them.

.

In these weeks and months of the pandemic, we have seen how each country has handled the health crisis in very different ways. The results are as diverse as the idiosyncrasies of the respective governments and citizens. And in the European Union, especially in the South, we find countries (read Spain and Italy) that are managing the health crisis in a more than dubious way. Once again we are seeing the differences between North and South within the EU, also in health policy management. The only thing that will probably remain of this European union after the pandemic will be the relative resilience of the northern economies, and the common market that has always been advocated by the most realistic.

.

Golden times for the awakened investor. We warned mid-March and also last day 1st April (by the way, the markets have risen close to 30% since the lows of that time). This crisis will change a lot of things in Europe, and at the same time it is uncovering huge opportunities. Imagine if we can take advantage of the restructuring of the Eurozone and the Euro, if we can invest in healthcare companies around the world and especially in China, or if we can take advantage of the pull of the stock markets and economies of what will be the new centre of the world. And all this with the wind at the back of every central bank on the planet. Unfortunately times are bad for the local investor with local assets.

For those of you for whom the trees of panic and volatility prevent you from seeing the forest of opportunities and returns that lie in the palm of your hands, let us explain Nick Maggiulli's simple, mathematical analysis of Ritholtz Wealth, which we fully endorse.

.

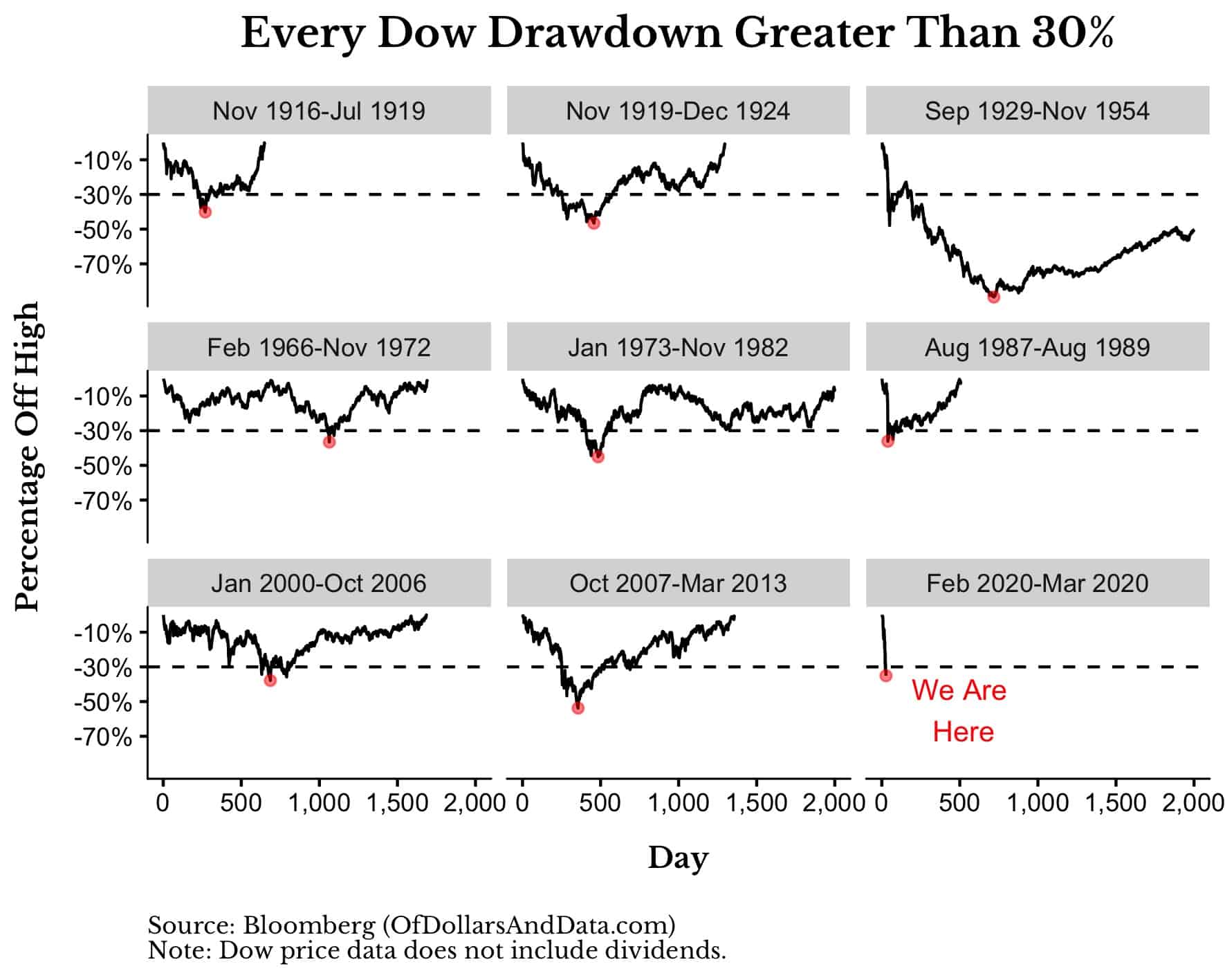

The crux of the matter is to shed light on asset purchases during times of panic. But first let us put the current crash in context.

.

As of today, the low for the Dow Jones has occurred on 23 March 2020 and has been 35% from its highs, making it one of the worst months in the history of the US stock market.

.

If we analyse all the crashes above 30% since 1915, we see that this crash is one of the fastest and fastest we have ever had.

Moreover, while in the past we see the little red dot that signals the floor, at this moment we still do not know if we have already seen the low of last week or if it is still to come in this coronavirus crash.

.

Nevertheless, there is no doubt that these are golden times for investors buying equities now. Every euro or dollar we invest in today's markets will grow much more than those invested in previous months as soon as the markets recover. Because we all assume that sooner or later the markets will recover and humanity as a whole will eventually beat this virus as it has beaten other health crises before, right?

.

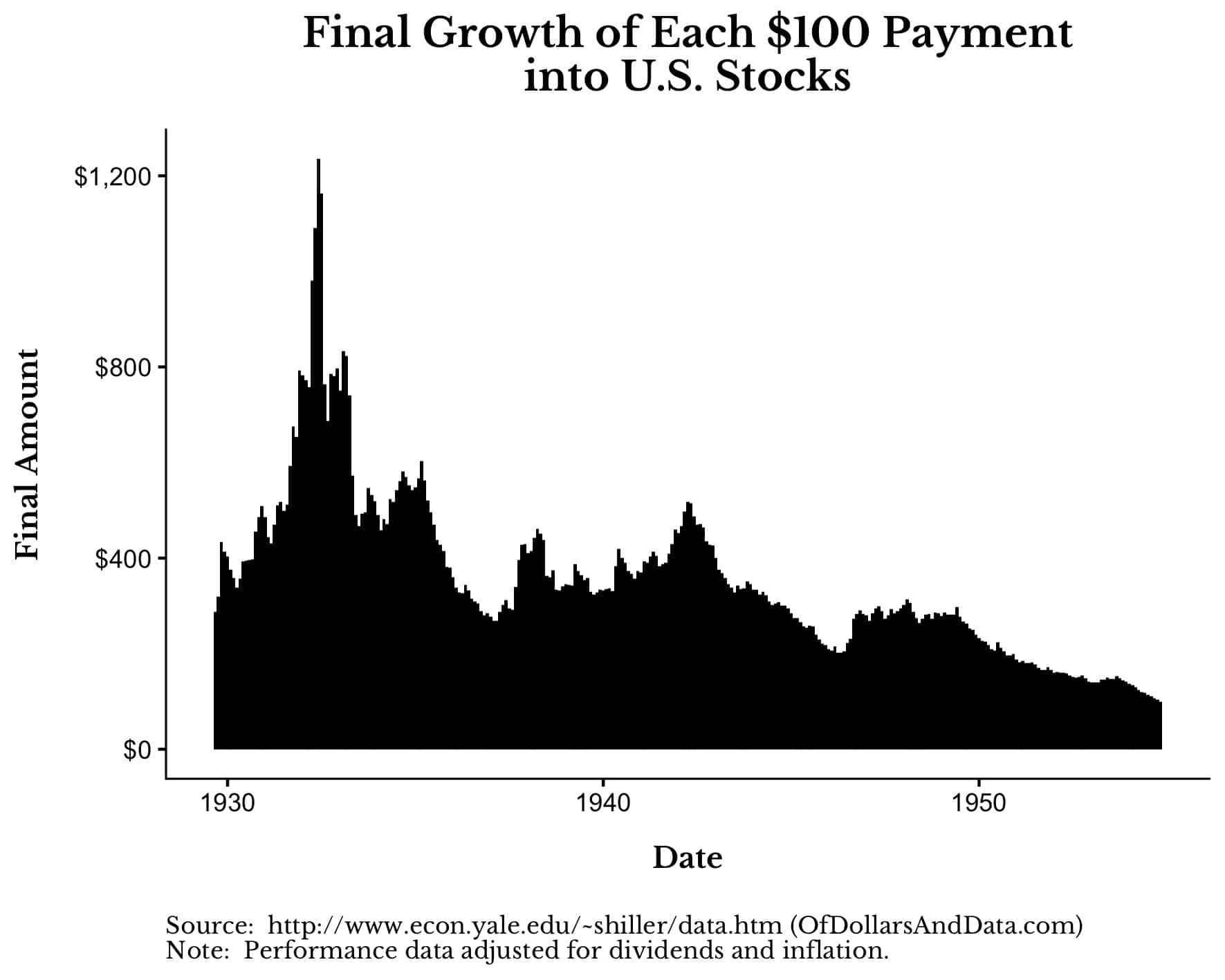

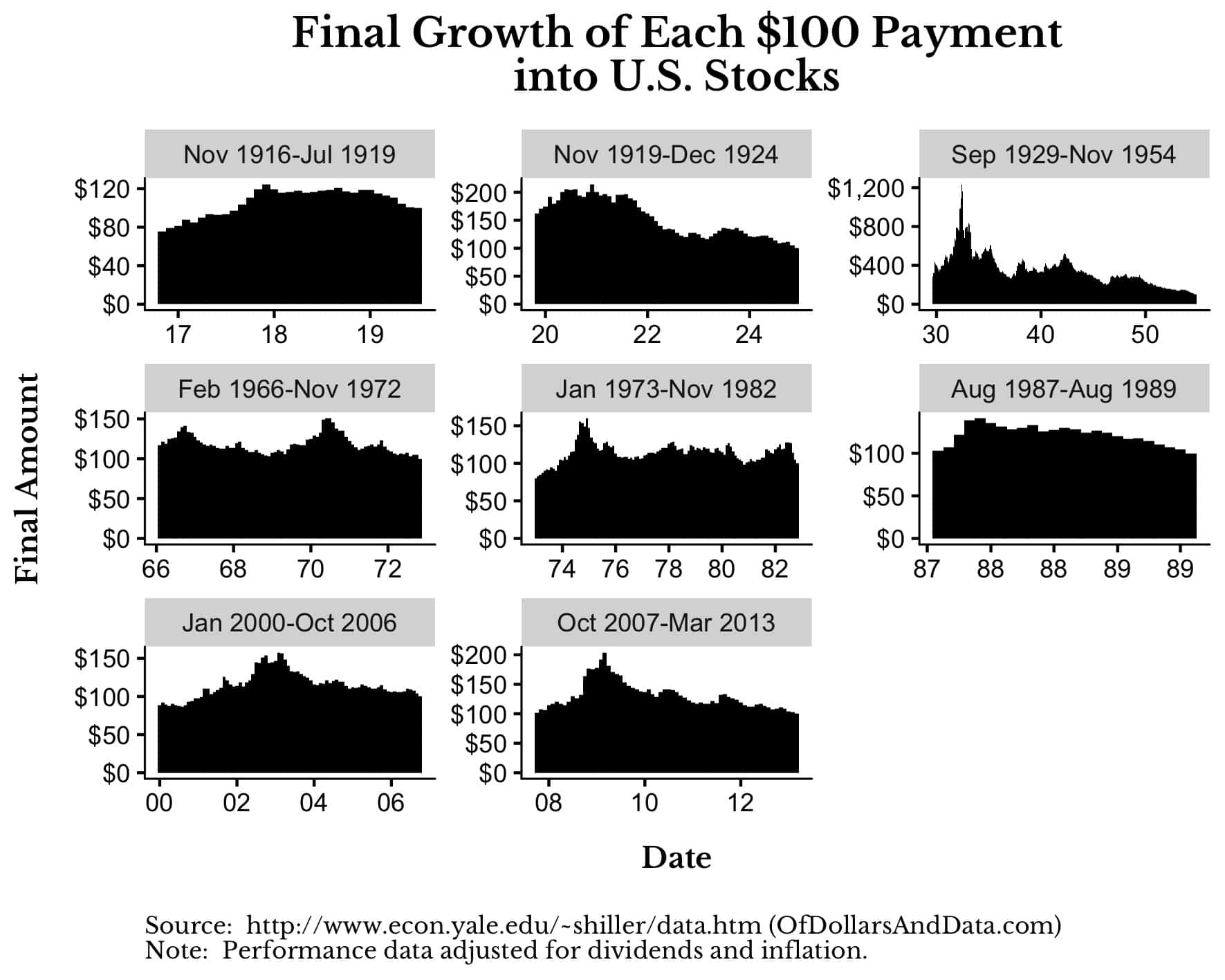

To demonstrate that every dollar invested today will yield much more than those invested before the crash, let us imagine that we decide to invest $100 every month in the US stock market from September 1929 to November 1954 (crash of 1929 and its subsequent long recovery).

.

If we had followed this strategy, this is what each $100 packet would have earned (including dividends and adjusted for inflation) until the recovery was completed in November 1954:

As you can see, the closer we bought to the low in the summer of 1932, the greater the long term benefit of that purchase. Each $100 invested at those lows grew $1200, which is three times as much as the $100 packs bought in 1930 ($400).

.

However, even if we look at the other falls above 30% shown in the first chart, we still see much higher profits if we buy during times of major panic and market declines:

This chart shows that buying near crashes (even if we don't hit their lows exactly) provides between 50 and 100% more profit compared to an investment at other times. That means that your $100 will grow $150 or $200 more (adjusted for inflation) when the market has recovered again.

.

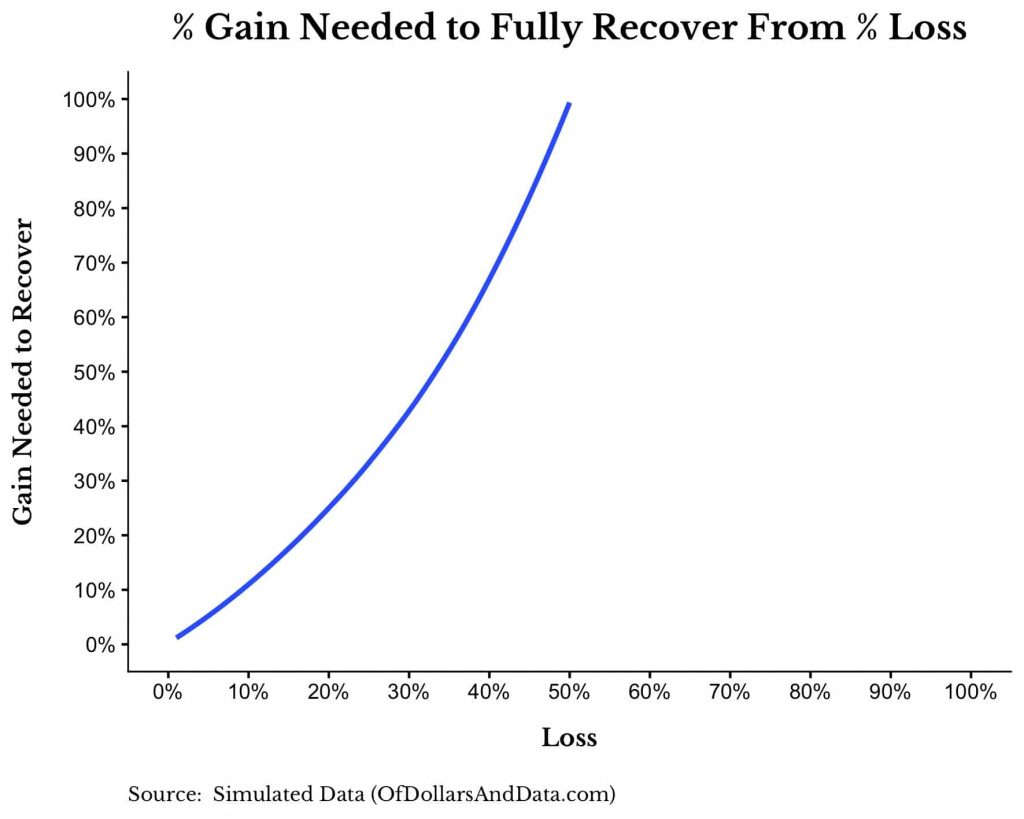

But where does such a spectacular increase come from? Well, besides being intuitive, its origin lies in simple mathematics: Every percentage loss requires a higher percentage gain to compensate for it. At this point in the film, it should not escape anyone's attention that a 10% fall requires an 11,11% rise to recover that loss. In the same way that a 20% loss requires a 25% rise and a 50% fall requires a 100% rise. You can see this exponential relationship very clearly in the graph below:

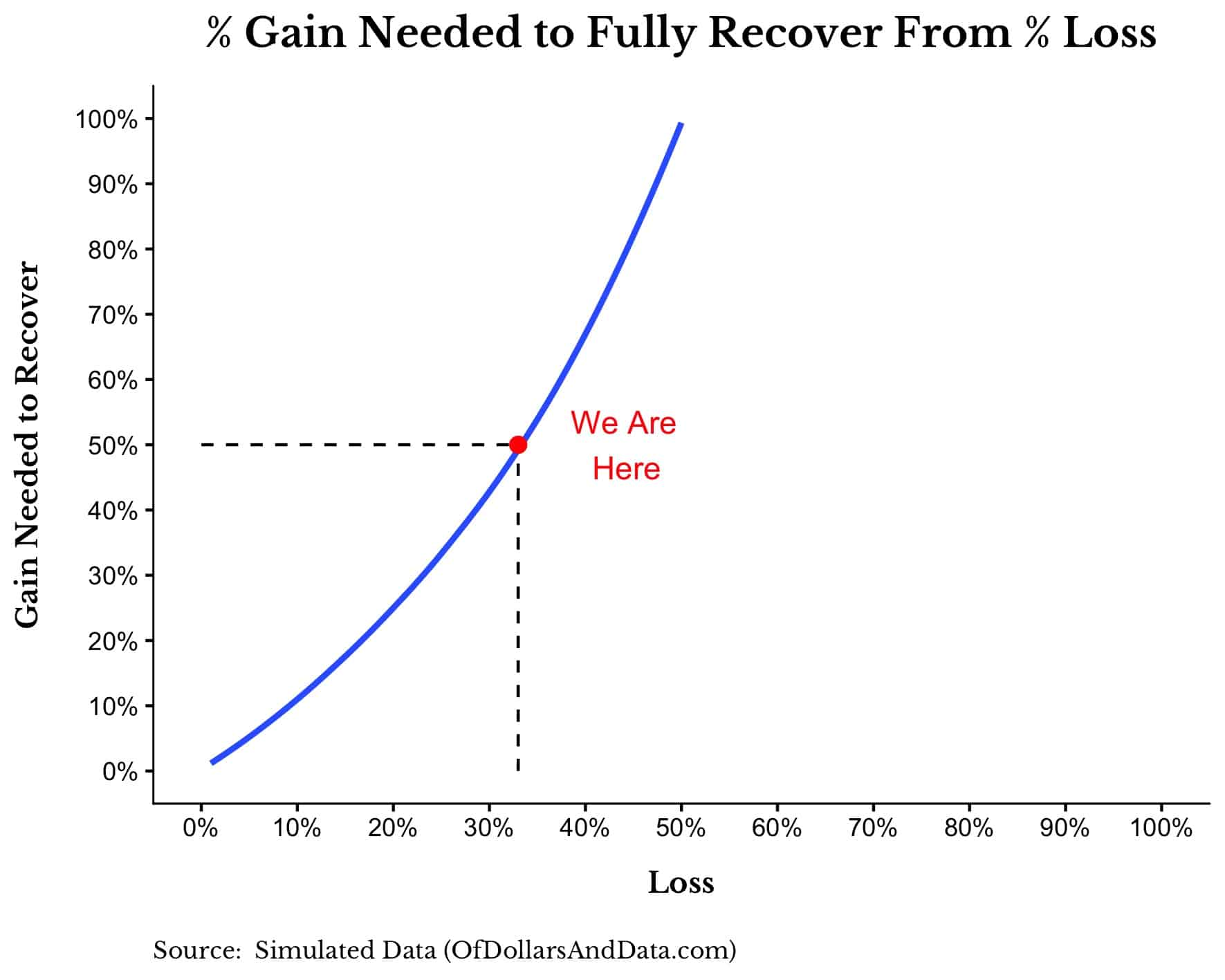

Let us now see what the chart would look like adapting it to the fall in the markets up to last week (-33%) and see the profit that would be needed to recover it:

If we do not see new lows, the recovery needed is 50%. And what a coincidence, for every $100 invested now they will generate $150 (a further 50%) when the recovery materialises.

.

But despite the obvious benefit of buying during the current panic, most investors are not doing so at all. Including those who have a lot of cash, either because they had it in other assets or because they sold during the crash in panic. And thank goodness they don't, because if they did, the crashes would no longer be crashes, and therefore the opportunities for good investors would vanish before they materialised. Excuses for not doing so can be diverse and very convincing for less good investors. Among them are «this time it's different» or «we don't know if it will fall further». As if a good investor is only one who is lucky enough to buy just on the day when the markets quote what will be the historic low of that crash. Remember that in graph 2 we talk about buying "as close as possible" to the low, without aiming to buy right on the bull's eye.

.

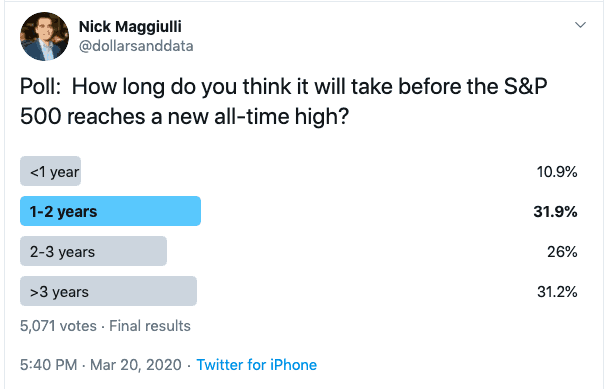

Let us now honestly answer the following question: How long do you think it will take for the markets to recover to the pre-pandemic highs? A month, a year, a decade? How long will it take for the indices to recover from that 33% decline? Answer yourselves.

.

Based on that answer, let us return again to the expected annual return in the future for our current investment. The equation is as follows:

Expected annual return = (1 + % Gain needed to recover)^(1/Number of years to recovery) - 1

But since we know that the percentage gain needed to recover is 50%, we can simplify it as follows:

Expected annual return = (1.5)^(1/Number of years to recovery) - 1

Therefore, if you think that the market will take time to recover:

1 year, then your expected annual return = 50%

2 years, then your expected annual return = 22%

3 years, then your expected annual return = 14%

4 years, then your expected annual return = 11%

5 years, then your expected annual return = 8%

Even taking 5 years for a full recovery, the market would be offering you the same return as the US stock market has historically yielded. Nick Maggiulli asked this same question on twitter and found that two out of three of his poll participants believe that the recovery will come within 3 years.

That means that if the majority of respondents are correct, any investment made now, is going to yield between 14% and 50% annualised until the market recovers. Think about what this means. Investors who choose not to buy at this time are either giving up an annualised return in excess of 14% for the next 3 years, or they believe that the market will take more than 5 years to recover and despise annualised returns of less than 8%. In short, the only reasonable reason not to do so is if you already have all your money invested and have no more at the moment (time to sell grandma to invest more in the stock market, as he said...).

.

Of course, new black swans may occur on the planet, delaying the recovery of markets, as has been the case for decades in Japan, for example. But it seems unlikely, especially in efficient economies such as the US and growing economies such as China and the other Asian economic orbit. Moreover, note that throughout the article we are referring to the market, i.e. the indices. But imagine the figures that will be achieved by those who also have the possibility of investing in actively managed funds that significantly outperform the benchmark indices. In other words, those who invest in portfolios where the management team selects the companies with the greatest potential for recovery at this time (Healthcare sector in China, for example). And we will not tire of repeating that, although the vast majority of actively managed funds do not outperform their benchmarks, especially within the limited universe of funds marketed in Spain, there are world-renowned managers who have been doing so for decades. Unfortunately, however, they are not easily accessible to the average Spanish investor, as we explain in detail in «Why don't large international investors invest in the same funds as you?«.

.

As he once said Jim O'Shaughnesy, Many people confuse possibility with probability, and the two are almost opposites. Keep this in mind as you face new challenges that will come in these days.

.

One of the things that still surprises me is to see how simple mathematics can help us to clarify the thickets in which our own minds entangle us. Our fears and passions are our worst ally in the face of the crash caused by the covid19 virus. Objective figures are certainly a glimmer of sanity to handle Mr. Market's schizophrenia. And the numbers show us that, assuming the market (and even more so our well selected stocks by the world's best managers) will recover in the coming quarters or semesters, the returns we will get are very, very attractive. And therefore, any hypothetical new low in the stock markets would be nothing more than an additional buying opportunity and even higher profits. Fortunately for a minority, the majority do not see it this way and are still waiting to see the floor, like those who are permanently waiting to catch the next train, which will probably be an AVE train that does not stop at their particular station.

After the much read and commented in networks «The lies of the Spanish government and health authorities about the coronavirus«In the third instalment of articles dedicated to the global crisis caused by the SARS-Cov-2 coronavirus and Covid-19 disease. In our first article entitled «Realistic coronavirus figures and the opportunities of an unfortunate crisis»We were already anticipating this: The effects on the entire world economy are devastating in the short term. But only in the short term since the infection has a clear expiry date, Unlike other geopolitical, military or social conflicts, which also generate panic in the markets. Y It is this temporality that should awaken the good investor in us and change our fear for the famous greed that Buffett and other investment greats recommend when the rest of us panic.

.

In this pandemic, which is now beginning to sweep the West, the investment opportunity is one of those that are often called once in a life time, This is one of those rare occasions in the course of a lifetime of investing. This is because, although there is always room for doubt due to imponderables that can complicate scenarios, business activity will probably recover to pre-pandemic levels in the medium term at best. Obviously these imponderables include, for example, a mutation that makes the virus more resistant and/or deadly, war conflicts that add more instability to the world order, or other health crises that could arise and coincide in time with the current pandemic. But if none of these things happen, the recovery in the tone of the economy will be no more than a few months. a couple of quarters, And what should a few quarters mean on the horizon for a good investor? Nothing.

.

Therefore, it's time to go shopping (or hunting, as Buffett would say) and take advantage of the fact that the results of countless good companies around the world are going to be temporarily and exceptionally bad. Because the fall in profits and turnover will not be due to poor business performance but to a lull in global economic activity that is as exceptional as it is temporary. If we talk about airlines, we will find some at half the price of last year. If we look at the energy transport sector, the falls and fluctuations have been insane. And what can we say about the China's health sector, The winning horses, for example, have an exceptional horizon ahead of them because they will be the almost exclusive providers of pandemic and post-pandemic material on a planetary level.

.

But how to find these pearls with such a promising future? Decades ago we learned that it is much more efficient to select the best international fund managers than trying to analyse the best companies on the planet. The knowledge that good local management teams will have of the best companies in their respective countries (Vietnam, India, Brazil, China, etc.) will always be infinitely superior to ours or to that of any multinational management company that tries to make its selection through a manager located in London or New York, even if its forefathers were originally from those countries. We would therefore be well advised to invest our money now in those investment funds who have local and comprehensive knowledge of China (or the specific health sector as mentioned above) or any other country.

.

And those good local managers will not only choose good businesses, but also cheap ones, with bright prospects for recovery. Because if we think that a company may be losing a whole quarter of its turnover due to the pandemic, for example, and we buy it now at a panic price, its growth prospects in terms of turnover over the next 4 or 6 quarters will be spectacular. In other words, we will be investing with Value criteria but with a Growth potential that is as exceptional as it is profitable. If we add to this the fact that we will be selecting companies whose business is based on taking advantage of growing economies and demographics such as those in Asia, the tailwind will further boost our future profits.

.

As the image on the left hand side of the Cobas March Newsletter, It is now, when our neighbours in the 3rd 5th are beginning to realise that perhaps the coronavirus is not just a simple flu, that we should invest without fear and give free rein to our good investor's greed. Now, when our less informed friends and acquaintances are alarmed by the market crashes that are all over the TV news. Just like the lift man who recommended shares to Groucho Marx. in this essential book, or Rockefeller's shoeshine boy invested in the stock market. In other words, when the less informed panic about the coronavirus epidemic and the markets go into a tailspin, it is the most appropriate time to invest in the quality assets that have been exaggeratedly depreciated in recent days. It is perfectly possible, as we have already said, that things will get even more complicated, and that the investments we make today will temporarily lose an additional 20% or 30%. But if they do, and our investments are of quality and made with the good judgement of the best fund managers on the planet, it will be for a very short time. On the other hand, if we remain fearful out of the market, it is likely that we will not see that additional 20-30% fall but a sharp recovery and miss out on much of the upside, having blown this one. «once in a life time».» opportunity.

.

We know that many will read this article but will not follow the recommendation, as it is easy to understand that you have to buy when everyone else is selling, but it is difficult to dare to put it into practice. And thanks to the majority who won't dare and those who don't even agree with our arguments, a few of us will be able to make substantial profits in the coming years.

It is regrettable to see the differences in the handling of the emergency situation in the coronavirus pandemic between different countries around the world. But what is worrying is the attitude of the Spanish political and health authorities in the face of this crisis, as they strive time and again to distort the facts and data in order to minimise its stark reality. A mixture of cowardice and misunderstood paternalism that justifies, in the eyes of some, the absence of courageous decisions. The Spanish authorities' determination to deceive the public stands in sad contrast to the realistic and serious warnings of other governments and global health organisations.

.

The Minister Spokesperson of the Government, Maria Jesús Montero, has declared in different media, and without any blushes, that Covid-19 is nothing more than a «...a new and unacceptable project".«new flu, similar to normal flu and with an even lower mortality rate than normal flu».» (for example in minute 10 of the following interview with him on RAC1 last week).

.

.

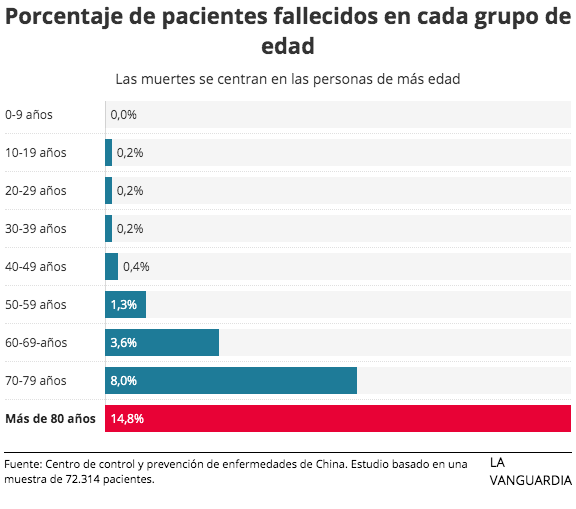

The unfortunate reality is that the lethality of this virus is much higher than that of seasonal flu. And any well-informed scientist, whose rigour is not contaminated by the government's political slogans, will admit statistical figures of around 3 or 4 deaths per 100 infected. Some Spanish authorities use mortality figures for normal 2% flu, but for hospital admissions and not for those infected, thus inflating the mortality rate and making it incomparable with that of Covid-19. On the other hand, also maliciously, they proclaim that the mortality of the coronavirus is 0.7%, taking the death figures for those infected just at the beginning of the epidemic in Europe, which means that the sick who are going to die have not yet done so. To further embarrass the minister, here is the official comparison between the mortality rate of the common flu and the US CDC's Covid-19:

.The most statistically reliable figures are found in China, where there are more and older cases of coronavirus. And those figures are now in the 3,75% mortality3012 deaths out of 80409 infected. Unfortunately, a fraction of those infected today will also die, while the number of new infections is already declining, so that this percentage is also tending to increase by about 0.04% per day, as it has done in the last few days. In other words, if the official figures in China are to be believed, mortality is indeed frighteningly close to 4%. And if we don't believe the official figures (I personally do) and think that the Chinese government is making up the mortality, then that's the end of the story. You can follow the daily evolution of the official figures in China at this page from Wikipedia, and the official figures for the rest of the world at this one.

.

However, some news which many people dismiss as being tremendist, infodemic or fake news, are in line with what is published in the majority of the world's media. international media with up-to-the-minute timelines of any new developments regarding the coronavirus,and spare no means or adjectives to keep the people of their respective countries on alert and on the lookout for health emergency. Because this state of alert and emergency does indeed punish the economy in the short term, but it saves lives. Thus, countries such as the US, where the spread of the virus is currently still proportionally lower than in Spain, are giving unequivocal instructions to their citizens to be prepared for imminent confinement o emergency situation This is because, mortality rate aside, what is clear is that this coronavirus is highly contagious, and its spread across the planet is unstoppable. Mortality rates aside, what is very clear is that this coronavirus is highly contagious, and its spread across the planet is unstoppable. That is why responsible governments are alerting and preparing their citizens for a massive infection. According to the calculations of Harvard Professor of Epidemiology Marc Lipsitch, Between 20 and 60% of the world's population will be infected by the coronavirus if we do not take drastic measures as China has done and/or an effective and viable drug does not emerge for everyone. And pending such a drug, our only option is to slow the pandemic. That means, even with optimistic mortality rates, millions and millions of deaths across the globe, at a brutal cost at all levels. What a contrast to the statements happy flowers of our ministers and health spokespersons who keep talking about «new flu that kills less than normal flu», right?

.

.

It is undeniable that a realistic warning about what is coming makes the population radically modify its usual activity, and with it consumption, productivity and therefore the economy plummets, as has happened in China. But courageous (albeit belated) measures, such as those taken and implemented with martial rigour by Xi Jinping, will save his country's economy in the medium and long term. Because an uncontrolled epidemic, with the mortality rate that this coronavirus entails, would have a far greater impact on the economy in the medium term than the short-term slump. Economically we could see a V-shaped economic downturn and recovery, but without bold measures by the already growth-anemic developed economies, we in the West will not even see a U-shaped recovery.

.

In Italy, the epidemic is just a few weeks ahead of us, and yesterday the decision was taken,The government's decision to close all schools and universities in the country, albeit belatedly, was a belated one. In Spain, on the other hand, despite recognise at least 3 infections in children school-age children, the closure of schools is not (yet) being considered. Not only that, but in one case it was the mother who insisted time and time again that her daughter be tested for the coronavirus, while the health authorities kept telling her to find a family member (as both parents had to stay at home because they were infected) to take her to school normally! What a botched job we are doing on such a serious issue in which we all have so much at stake! Because the fact that the vast majority of children and young people overcome the infection with mild or even asymptomatic symptoms does not in any way prevent these children and young people from infecting their parents, grandparents and teachers. These are all groups that will suffer serious consequences and whose mortality is very high, as we have seen above. Moreover, it is absurd to try to contain the epidemic by keeping infected parents at home and letting their children, who are also infected but many of them do not know it, move freely in the streets, buses and other environments with which they usually interact.

.

Another example: In Spain, the authorities have gone out of their way to emphasise that the existing infections were not from the EU (locally infected) but imported, from Italy, China, etc. They insistently stressed that this was a very important detail, trying to convince the population that Spain was in a perfectly controlled situation since our infections were all imported, ignoring the fact that it is only a matter of time before there are, as there have been, community infections in Spain. However, when faced with infections whose origin is not imported, the Spanish authorities still describe them as of «unknown origin», without yet recognising that they are already Community infections, i.e. local.

.

On the other hand, in the United Kingdom, despite having fewer people infected than in Spain today, there are already clearly warn The population should be made aware that community infections are an imminent reality and that the population needs to be aware of this in order to be better prepared.

.

Even in the American universities clearly warns that if students take advantage of spring break (similar to Easter holidays in Spain) to leave the country or visit areas with a high incidence of the virus, they will have problems to be readmitted back, unless they stay in the country for the rest of the year. two-week quarantine in a suitable location before returning to their rooms on campus. Just like here...

.

The situation is very serious, because unless a medication emerges within a few days that drastically reduces mortality and is feasible for mass administration, what is happening in Italy will only be the tip of the iceberg in the rest of Europe. And neither the health services (already overstretched in Italy) nor the logistics of essential supplies will be able to cope with a massive contagion. That is why it is vital to take courageous measures of blockade and isolation as China has done, even if it means a short-term economic collapse. However, the first decision the EU took was to take the option of closing intra-European borders off the table, thus paving the way for the free movement of Europeans and Covid-19 from Lisbon to Berlin. Yes, those same intra-European borders they did not hesitate to close instead, unilaterally suspending the agreement on Schengen, The refugees were arriving by the millions in the heart of Germany.

.

The paradox that China will now face is that it will have to continue to close its borders (to people, not goods) to prevent, once its domestic epidemic has been controlled, the virus from infecting them again, now coming from countries like the Europeans where the infection will be out of control due to late and cowardly political decisions. This is why we will see the recovery of the courageous Asian giant sooner than that of the old and cowardly Europe, which represents an extraordinary investment opportunity, as we already advanced in «Realistic coronavirus figures and the opportunities of an unfortunate crisis«. China begins its path back to business. And it does so having acquired a priceless technological know-how to handle the next health crises, as we can read in this WeekInChina article.

.

In short, the handling of information and alerts to the public say a lot about each country. And unfortunately in Spain we have authorities who are more concerned with bread for today than with deaths and hunger for tomorrow. They focus the State's communication efforts on keeping the population in the dark, who consequently live without any foresight in the face of a health emergency, i.e. without stockpiling food and medicines or any family or personal contingency plan whatsoever. Even the Director of the Alerts and Emergencies Coordination Centre, Fernando Simon, has gone so far as to say that wearing a mask in the street is counterproductive because people would laugh at us or believe that we are infected, insisting time and again that masks do not protect us from infection in any way. And then admitting with a small mouth that if the population buys masks, health professionals will not have enough, proving that they are an efficient and necessary element of protection. Let us remember that in countries like China they are compulsory masks for the entire population in risk areas and punish those who go out on the streets without them. Other governments, such as the French or German directly confiscate or prohibit the export of facemasks so that their health professionals can have them, without treating their citizens as imbeciles by telling them that they are no protection against infection and that they will make fools of themselves if they put one on.

.

It is true that some young and healthy readers may dismiss this article as being tremendist, but they should bear in mind that although they would overcome the infection with hardly any symptoms, they would probably fatally infect other less healthy and younger people in their family and professional environment, or simply strangers with whom they share, for example, a simple public transport. In the end, it is better to continue informing ourselves in international media and preparing ourselves for the worst, while we cross our fingers that we will soon have a medication available to everyone that will reduce the real mortality rate to the levels of a simple flu.

It is not a question of being tremendists but simply of having a minimum of critical sense in the face of the barbarities that media, politicians and other official agencies in many Western countries proclaim according to their own interests and/or ignorance. For example, the 2% coronavirus mortality figure that is being bandied about is simply not realistic. And to realise this you just need to know how to multiply and divide as well as to know the reality.

.

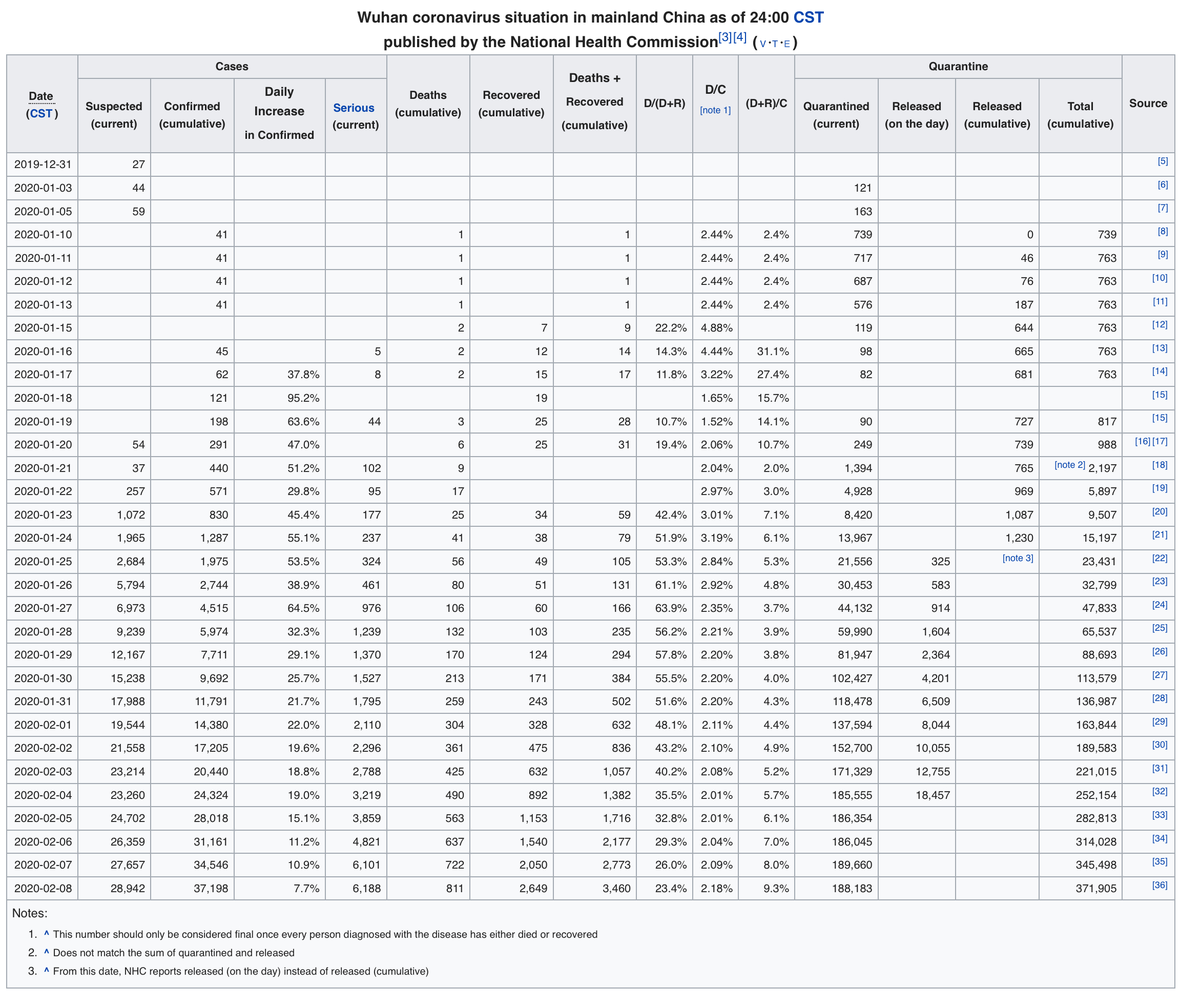

Although it may come as a surprise to many, the Wikipedia (graph below) is one of the sources with the most up-to-date and up-to-date data on the progression of the pandemic. We will take for granted the figures officially published by China to see that the mortality rate is probably much higher than the 2% mentioned, because if we think that the real figures are even worse (what other reason would the Chinese authorities have to manipulate them), the situation and the outlook would be even more terrifying. In the daily updates of those infected by the new or novel coronavirus we see a significant slowdown in the last few days, with the percentage going from over 30% to 7.7% in the last 10 days.

The same is true for the number of deaths, whose increase is also seen to slow down from levels above 35% to the current 12%. Obviously the mortality of an epidemic should be calculated as the number of deaths relative to the total number of infected, and this is what those who claim that the mortality rate of the new coronavirus (2019-nCoV) is around 2% are miscalculating. But it should not escape anyone's attention that they are making a gross error in calculating deaths to date with those infected to date, since many of those infected counted today will, unfortunately, die in the next few days. In other words, the mortality rate should be calculated when the epidemic has already passed, because if we do so during the (current) expansion period, we will be assuming that none of those currently alive will die. Such a basic error can hardly be attributed to the ignorance of those who use the 2% mortality rate as an argument for the inhabitants of the planet to remain unconcerned and live a normal life. The death toll today already exceeds the death toll from SARS. This epidemic only infected 8,000 people in 9 months, while in China alone there are already more than 37,000 officially infected in barely 2 months, and with a real mortality rate that we will now try to guess.

.

It is obviously very difficult to guess how many of those infected today will die in the next few days, and even more difficult to guess how many days they will survive. But just thinking that a fifth of the seriously ill (with altered vitals, i.e. really very sick), who currently account for almost 17% of those infected today, may end up dying in the next 4 days, let's say, and adding those who have already died, the calculation of the mortality rate shoots up to levels above 4%. And that is not counting the fact that none of those infected during the next 4 days will die in the following 4 days... We are therefore facing a pandemic whose mortality rate can only be calculated in retrospect, but which all indications are that it will probably double the 2% proclaimed by most of the media. Remember that the death rate from influenza is much lower than 1%, there is a relatively effective vaccine, and yet it still causes hundreds of thousands of deaths each year worldwide. If we add to this realistic mortality rate of this new coronavirus the chilling ease of contagion it is demonstrating and the fact that the vaccine has yet to arrive, the explosive cocktail is served. Moreover, imagine how this infection will behave in societies adjacent to China such as, for example Vietnam, Myanmar, Laos, Thailand, Philippines, India, Indonesia, Malaysia, etc., with 1.5 billion inhabitants whose hygiene, sanitation and epidemiological control systems are far more precarious than those of today's China. There, the proliferation of the virus cannot be controlled, as it is happening in China according to the official figures of the last few days, but only an accessible and timely medication or vaccine would prevent extravagant mortality.

.

It is worth reading the very interesting analysis by Tyler Durden on Zerohedge, The report rightly points out that in a country like the US itself, the situation could also become very complicated due to the high cost of the health system for the population that cannot afford good private insurance. This would lead the infected Americans to avoid using health services, with the consequent lack of control of the epidemic, despite being one of the societies with the highest per capita income on the planet. Moreover, in most Western democracies, governments would be far more reluctant than the Chinese government to harm their domestic economies to try to control the epidemic. By definition and unfortunately, most Western democracies would be more concerned about bowing to their lobbies and taking populist measures that would not jeopardise their re-election, the economy, or their partisan interests, than they would be about ordering courageous but unpopular measures. We see daily examples of health ministers and mayors downplaying the risks and calling for business as usual so that nothing disturbs the fragile economic balance in southern Europe. Without going any further, it is shameful that it is the companies themselves who have to suspend their participation in the Mobile World Congress in Barcelona, while the local authorities continue to insist on convincing them not to cancel their reservations for hotels, restaurants, chauffeurs and other unmentionable expenses.

.

That said, we should obviously not pin our hopes on controlling the pandemic globally, but on effective treatments and subsequent vaccines that can be made available to the world's population in the coming weeks. Because if we do not have those drugs for several months, the pandemic could reach our own neighbourhoods and claim millions of victims, especially in Asia. But it is not enough to discover an effective drug or vaccine; we must also be able to produce it on a mass scale and at a cost that is affordable for the vast majority of the world's population and/or states.

.

Health sector companies such as Inovio, China, a leader in research into viruses such as Ebola, MERS and Zika, is already testing potential vaccines for 2019-nCoV in animals. And probably the criticised «shortcuts» in international clinical trial protocols that China is surely taking will accelerate the achievement of an effective treatment that will save millions of lives around the world. Because given the extremely high rate of spread and mortality of this coronavirus, time is more than gold, it is Life.

.

But how is this pandemic affecting the global economy? Well, we are just seeing the tip of the iceberg of the destructive effects on economic growth. Obviously the first on the list to be affected is China's economy. But the cascading effect can be devastating because of the interconnectedness between Chinese products and those of the rest of the world. Just look at the Chinese components (often internal and invisible parts) around you, and think that they are already materially temporarily no longer being produced.

.

That word, the temporality, is the key to turning an unfortunate global health crisis into an opportunity. Because even if the treatment or vaccine arrives in time to prevent the global epidemic, the crisis in China is already an inevitable fact. But the fact that a large part of the country has already collapsed, with businesses closed, transport blocked and people locked in their homes, does not mean that this situation cannot be reversed in the coming quarters, but precisely means that China's resurgence is closer. Because, unlike other crises such as a trade war, an economic embargo, a military war or any other geopolitical conflict, this epidemic is not a crisis that can be reversed in the coming quarters. has an expiry date. This is not only because the infection will generate a natural peak and will eventually control itself, but also because any vaccination or medication will drastically shorten this period and the mortality it entails, minimising its effects and invigorating recovery.

.

Assuming that such medication or vaccine arrives in time to prevent a pandemic severely affecting Europe and America, what will be the post-epidemic scenario in Asia? Natural epidemiological timing indicates that a return to normalcy in China may come much sooner than in its neighbours. Moreover, China has far more resources, discipline and health structure to effectively medicate its population when the time comes. The Chinese state's strong political will and economic capacity to recover its economy through financial stimulus, which may even dwarf the QE carried out by Western central banks, will also be decisive. We should therefore expect a massive post-epidemic response from Xi Jinping's government. No effort will be spared to help the Chinese economy make up for lost time, which, let us remember, will not last more than a couple of quarters, given that the treatments (Chinese or Western) will not take long to appear and will be available to whoever pays for them. It is therefore foreseeable that during the second half of 2020 (or even earlier) the recovery of the Chinese economy will be underway, and it will be a matter of state and national pride to return to the path of dominance of the world economy to which the Chinese seem to be destined. Moreover, the trade war with the US has not spilled blood into the river, as we have already predicted almost a year ago, so there is even less reason for pessimism about China's economic recovery.

.

Therefore, in addition to preparing ourselves and our environment for the worst-case scenario of the pandemic (remember that the more than likely current mortality rate is much higher than 2% as we have seen), we would do well to position our investments to take the best advantage of this textbook black swan called the coronavirus. We should therefore take advantage of possible falls in the Asian markets - especially the sectorhealthcareChinese- to buy shares in companies that will rise from the ashes of this epidemic with a strength and pride that we are unlikely to see in the West. Significantly, however, share price falls to date have been surprisingly modest, perhaps in anticipation of such a stunning economic recovery, or perhaps the result of Mr. Market's chronic schizophrenia, who knows.

.