For those of you who have not yet done so, we recommend that you read the first part of this article, in which we described a future that is much closer than some believe. In that near future, interest rates in the north of the EU could no longer be anchored to interest rates in the south. This break between the price of money in the rich countries and the price of money in the poor countries will inevitably lead to a different exchange rate for the other currencies. And as the old man said, if it walks like a duck, flies like a duck, swims like a duck and quacks like a duck, it is a duck. In other words, if it has different rates, it will have different exchange rates, and therefore the single currency will cease to be single, which means that we will have at least two Euros, if the nomenclature is maintained.

.

For the most sceptical we bring you today the articleprepared by Yves Longchamp's Director of Analysis Yves Longchamp from Ethenea Advisors. In this article Longchamp quantifies the interest rates that economies as disparate as Germany's or Italy's can bear. And it is not just that they can bear different rates but that they must be able to have them, thus adapting them to the needs of each of their economies. No reader should be unaware of the terrible consequences for economies when the price of money does not adjust to the cycle and the needs of the economic machine. And unfortunately, economic convergence ceased to be plausible for northern and southern Europeans years ago.

.

Thus, Ethenea says that while Germany could currently operate with a rate range of between EUR 1.5 and EUR 1.5 per cent, it would be possible for the EU to operate with a rate range of between EUR 1.5 and EUR 1.5 per cent. 4,8-6,1%, Italy would not be able to withstand rates - at least - higher than 0,6-1,5%. The difference between one economy and another is abysmal, and three quarters of the same could be said about the needs of rates between other countries in the North and the South. I recommend that you read the aforementioned study Longchamp because for more than one person it will be a slap in the face of reality that will, at the very least, give them pause for thought.

.

The inevitable consequences of such disparate interest rate requirements (and moreover increasing day by day) are the breakdown of the uniformity of the price of the Euro. Germany will not be able to withstand rising inflation for many more years, while in the south of the EU we are mired in debt for many decades, which requires a quasi-free price of money in order to be able to continue paying the interest. Remember that in the south we are still running budget deficits, i.e. we owe more and more money every day, despite having negative interest rates for years! The consequence of this is that in the south it is not materially possible to keep up with the rate hikes that the north of the EU will soon be demanding, following in the footsteps of the US Federal Reserve.

.

We have warned many times over the last 7 or 8 years. The single currency is doomed to cease to be unique. And investors would do well to prepare their money, their custodian banks, their investment vehicles and of course its investments for such a scenario of different rates and prices, even if the bureaucrats continue to dissemble and come up with a creative euphemism for the break-up of the Euro. Studies such as the one by Ethenea's Director of Analysis can say it louder, but not clearer. And since Cluster Family Office We will never tire of warning of the risk unwittingly taken by investors in the South who do not prepare for their investments to be priced and priced in the North and to be geographically and qualitatively safe. As Longchamp says in his article: «Ignoring a reality does not make it less real».»

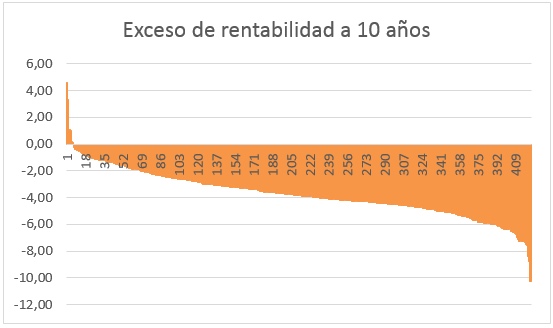

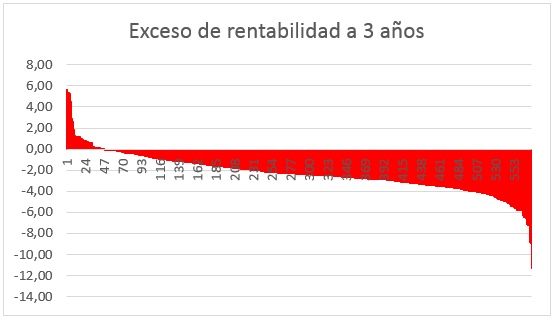

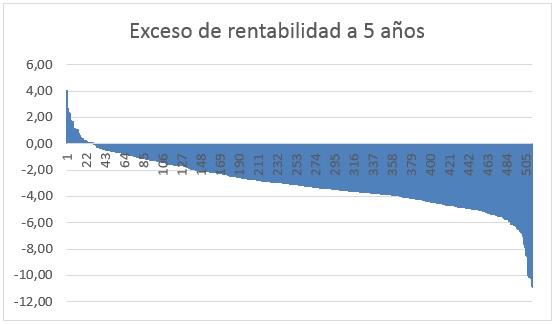

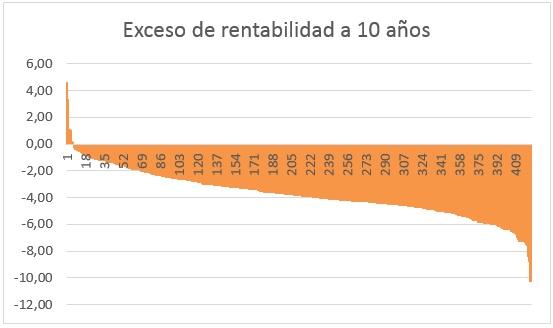

The answer is NO, unless you have the extremely rare ability to choose one of the very few pension plans that outperform their benchmark index over a 10-year period. And even then, 10 years is a very short time when we consider that the investment horizon is usually very long when we’re talking about pensions for old age. But the secondary question we must ask ourselves is: What realistic chances do we have of investing in a pension plan that won’t condemn us to mediocrity? That is when the answer starts to become more uncomfortable if we want to be objective and honest. The fact is that the percentage of investment funds that do not outperform their respective benchmark indices is very low – let’s say between 1% and the 12%, depending on the source, the time frame and the sectors under consideration. But if we look at the performance of pension schemes relative to their benchmark indices, the proportion of funds that justify their fees is even lower.

.

Let’s take a look at the latest charts report produced by Morningstar of pension schemes that outperform their respective three-, five- and ten-year benchmarks. Devastating:

Naturally, the longer the time horizon, the more the Monte Carlo effect—which we’ve already discussed—is minimised a decade ago. Just look: if we focus on a 10-year period – which is by no means unreasonable, especially when we’re talking about pension plans that we’re not supposed to touch until retirement age – the percentage of funds that outperform their benchmark is less than 11%! But the fact is that many people are still more than 20 or 30 years away from retirement, meaning the probability of outperforming the index through a pension plan is approaching zero at a dangerous and alarming rate.

.

What conclusion should we draw from this stark set of figures? Well, if it is already difficult to find a «normal» investment fund within the universe of funds available in Spain that outperforms its benchmark over the long term, finding a pension plan that manages to do so over a 10-year horizon is almost mission impossible for most of us. And how do banks and other salespeople manage to place so many billions into pension plans if they are so mediocre? Well, that’s what the free cookware sets, the smart TVs, the bonus cash deposited into accounts and… the tax breaks are for. Yes, those very tax breaks that many tout as the panacea for saving on tax whilst we prepare for retirement.

.

The fundamental problem is that those who argue that it is more tax-efficient to invest in a pension scheme than in a standard investment fund, despite the hefty tax bill when the moment of truth arrives, fail to take into account that the level of mediocrity in the management of pension plans is substantially higher than that of investment funds in general. Therefore, the main reason to steer clear of pension plans is NOT that we will pay tax on the income tomorrow on the savings we make today through contribution exemptions (we could debate whether or not such a tax break is worth it), but rather that The teams that manage pension schemes perform even worse than the average for standard investment funds sold in Spain.

.

For all these reasons, if an investor is able to find funds whose managers consistently outperform their benchmark over the long term (and such funds do exist; we refer you to this article we published in COBAS (a few months ago), you should never trade in that gem for a pension scheme that is poorly managed, no matter how many tax benefits or freebies its salespeople offer you. Tax breaks and cash or in-kind gifts, however tempting they may be, are nothing more than a short-term fix that condemns us to mediocre returns for the rest of our investment lives. Another issue is how to invest in funds that consistently outperform their indices and belong to that 90% universe of funds that are NOT investable from Spain. But we have already explained this repeatedly in articles such as «The advantages of investing from Luxembourg«.

Europa año dos mil veintipico. Después del trauma que supuso la negociación in extremis del Brexit, la UE tuvo que afrontar el siguiente elefante blanco en su habitación: La inflación. Aunque crecía tímidamente, era ya un tema que los tipos del norte no querían ignorar por más tiempo. La demografía y el crecimiento económico anémico, lastrado por la ingente deuda en toda Europa, había permitido aplazar la gran decisión a pesar de que en los EE.UU. ya habían normalizado el precio de sus dólares y el resto de su política monetaria.

.

Las comparaciones entre la economía norteamericana y el babel europeo eran odiosas. Y los tipos del norte, germánicos y escandinavos, con sus economías fuertes y saneadas no podían ni querían soportar el riesgo de una inflación descontrolada. Sus empresas multinacionales habían soportado admirablemente un Euro caro (que no fuerte), pero con la devaluación de la moneda única potenciada por unos tipos negativos, la inflación amenazaba ya muy seriamente la decisión del BCE de mantener la financial repression bajo cero.

.

Los tipos del sur, los mediterráneos, en cambio seguían necesitando que la inflación se les comiera un endeudamiento impagable. Rezaban para que un aumento generalizado de precios y sueldos, aunque acompañada de pérdida de poder adquisitivo, hiciera más pagadero un papel mojado que sólo el BCE les estaba comprando desde hacía ya una década. Pero los tipos del sur seguían sangrando déficit en sus presupuestos. Debían más y más, año tras año. Y ni sus gobernantes populistas ni sus niveles de productividad eran capaces de conseguir el equilibrio presupuestario necesario para detener la hemorragia.

.

Sin crecimiento económico consistente que incrementase los ingresos de los Estados del sur, y sin una inflación persistente que devaluase la deuda impagable, la única opción que quedaba para evitar el default masivo de los tipos del sur era el austericidio, pero esa vía se había demostrado también inútil para salvar a los griegos. La lata chutada desde hacía años, por fin topaba contra el muro que los tipos del norte y los del sur tenían ya frente a sus narices.

.

Los tipos del norte y los tipos del sur tenían idiosincrasia, productividad, datos económicos y necesidades opuestas. Pero paradójicamente unos tipos tan distintos tenían unos tipos iguales: Los tipos de interés. La cobardía y la obstinación de los euroburócratas de los últimos 25 años les había condenado a compartir moneda y tipos de interés a tipos muy distintos. Quizá había llegado el momento de que los tipos del norte y los del sur se adaptasen a sus respectivas economías.

.

Pero que nadie se equivoque llegado el momento de los tipos distintos: Aunque le sigamos llamando euro, si su precio es distinto para los tipos del norte y para los tipos del sur, cotizarán distinto y la moneda única será, de facto, historia. Y algunas pistas de ello no faltaron para los más suspicaces en todos estos años.

.

La pregunta del millón es si la separación de tipos norte y sur es inevitable o hay alguna opción más. Hace un par de años bautizamos como «The Big Write-down» and «Wtrite-down selectivo de deuda» la única forma de conseguir que los tipos del norte y los del sur siguieran compartiendo tipos, al menos durante algunas décadas más. Quizá en pocos años la UE esté ya muy cerca de tener que tomar la decisión final: Tipos distintos norte y sur, o bien write-downs selectivos del único acreedor que puede permitirselo, el BCE.

.

Hasta hoy la UE no ha hecho lo correcto sino lo necesario para aplazar el desastre, veremos a partir de ahora qué camino deciden tomar los tipos poderosos. Porque como bien dice Jonathan Tepper en este tuit, la decisión no la votaran los tipos del sur sino que la tomarán los tipos del norte cuando no tengan más remedio.

.

La segunda pregunta del millón es si los inversores están preparados, no sólo para evitar los efectos negativos de cualquiera de los dos caminos que la UE va a tomar, sino para aprovecharse de ellos.

The Luxembourg-based insurer Lombard International Assurance has recently published this article in Fundspeople in which he explains that the Spanish Directorate General for Taxation has responded favourably a few months ago to the binding consultations (V3070-17 y V2516-17) in which the possibility was raised of avoidWealth Tax for unit-linked policies with no right of surrender for a certain period of time. Obviously, this novelty is extremely important for those people who reside in autonomous communities that are not subsidising, or will cease to subsidise in the future, this Wealth Tax.

.

In the aforementioned binding consultations, the D.G. of Taxes confirms that during the time in which the policyholder voluntarily establishes their explicit renunciation to redeem their money, this amount will not be taxed in their calculation of Wealth Tax. In other words, the inevitable and indefinite taxation of money that has already been taxed in the past and which is not going to be used and enjoyed in the present is a thing of the past.

.

The Luxembourg unit-linked savings insurance is also a versatile and cost-effective investment vehicle The fund is the only one of its kind, as it allows any fund in the world to be included in the portfolio, whether or not it is registered for marketing in Spain. This fact alone justifies the creation of the vehicle, as we have explained in «Investment Funds: There are still classes«, However, if we also add the savings in wealth tax during the years in which the money is not going to be used, and the legal and banking security of Luxembourg, the convenience of having a personal/family Unit Linked becomes a necessity for those who have at least 250,000 euros. The D. G. de Tributos could say it louder, but not clearer.

Here is the newsletter sent out this week by Louis V. Gavel, from the prestigious research team at Gavekal, in which he talks about the effect of ETFs and the shift of the centre of the world from traditionally developed to emerging countries. A translated version of this article is proof of this:

.

«Another clear symptom that the investment world environment has changed is that the underperformance of emerging markets, which prevailed between 2011 and 2016 (when oil fell, the USD rose and yields remained low), is now clearly history. We are now living in a world where bond yields will tend to rise, the USD will tend to fall, and oil prices could show upward pressure. In such a world, exposure to emerging markets is once again rewarding. Indeed, an interesting feature of the recent falls is to see how volatility in US equity markets has actually been much higher than in most emerging markets. Even after this week's fall, Asian markets are significantly outperforming global equities.»

.

It is curious to see how, little by little, the centre of the investment world is shifting from the US and Europe to Asia, and with it, volatility is taking the opposite path. In other words, while development reaches the emerging countries, volatility travels to countries where development is weighed down by over-indebtedness. And the unfortunate thing is that for most advisors and private banking managers, investment proposals towards countries where there is economic and demographic growth with decreasing volatility (emerging countries), are of greater «risk» than traditional European and American funds, where anaemia and volatility take over their growth. The difficulty of finding good emerging funds that can be marketed in Spain, without having a suitable investment vehicle (where any fund, hedge fund or private equity in the world can fit, deferring taxation as if it were any fund sold to you by the bank on the corner) helps portfolios to continue to be filled with the usual funds. But reality is stubborn and the centre of the world is inexorably shifting towards Asia, where there are impressive managers who achieve spectacular alphas.

.

Here is the newsletter of Louis-Vincent Gave The complete, which is virtually unmissable:

In Agatha Christie's Murder on the Orient Express, the victim is stabbed by twelve different individuals.

The same is often true of bull markets; when they die, one finds many a finger-print on the murder weapon.

With that in mind, one could pin the death of the bond bull market on accelerating inflation, or on the globally synchronized global growth surge, or on the lack of investments in new capacity over the past decade (see A Brave New New World, attached), or even on the demographic shift unfolding in the Western World (see The Savings Glut's Long Life and Slow Death), or simply on the realisation that fiscal policies all around the world are bound to stay extraordinarily loose for far too long (see US Budget Deficits, attached)... But whichever reason one wants to hang one's hat on, the bond bear market is likely here to stay. After all, if bonds can't even rally by a few basis points as equity markets meltdown, then we must have a structural bond bear market on our hands.

And at the risk of stating the obvious, this structural bond bear market is now clearly a headwind for equities.

It also marks a profound shift in the investment environment.

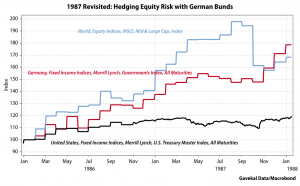

In a piece written close to the market top (see A Once in a Generation Shift - attached), we highlighted that OECD bonds had been the perfect counterweight to equity positions for decades. However, it wasn't always so. In periods when inflation picks up, OECD bonds do not protect portfolios against downside risk. Instead, they add to the downside risk. We also showed that one way to know whether we were in an ‘inflationary’ environment or a ‘deflationary’ environment was to look at the relative performance of long dated US Treasuries to Gold as both had asset classes tend to ‘trend’ over long periods of time. And when the ratio ‘gold to bonds’ moves ABOVE its 4 year moving average, that is typically a confirmation that we are moving into an inflationary environment. As the chart below highlights, following this week's rise in yields, such a move has now just occurred:

So if OECD bonds are no longer a sound hedge for equity risk, what is an investor looking to reduce the overall volatility of his portfolio, to do?

In the 1970s, and again in the 1987 crash, one of the best hedges (aside from gold), were German (and Swiss) bunds. Back then, the DM was slowly but surely establishing itself as Europe's trading and reserve currency; a genuine alternative to a US$ weighed down by too many years of US ‘guns and butter’ policies. Take 1987 as an example: US interest rates rose until they broke the back of the (then) roaring equity bull market. But as equities cracked and the fed slashed rates, investors sought out the safe haven of the inflation-fighting Bundesbank. So much so that, by the end of 1987, for an investor looking back at January 1986, German bunds had actually outperformed not only US Treasuries (that wasn't even close), but global equities as well:

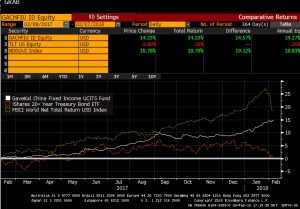

So, as Yogi Berra once said, is it ‘deja-vu all over again’? After all, in the US today, we not only have guns and butter; we should also soon have bridges, and tunnels, and hip replacements and student loan write-offs etc... (see The US Budget Deficits, attached). At the same time, we have China making a concerted push to turn the RMB into Asia's DeutscheMark, a currency that will increasingly fund Asia's trade and Asia's capital spending. And sure enough, just as global equities (World MSCI in the chart below) and US Treasuries (TLT US in the chart below) have started to roll over, Chinese bonds (represented below by the Gavekal China Fixed Income UCITS fun) have held their own. In fact, like German bunds in the fall of 1987, the Gavekal China Fixed Income UCITS fund has returned over 14% in US$ terms which handily beats the flat return of long dated US Treasuries, and could approach the return of global equities should global equities repeat the past week in the near future!

Another clear sign that the investment environment has changed is that the underperformance of emerging markets, which prevailed between 2011 and 2016 (as oil fell, the US$ rose and bond yields stayed low) is now clearly over. We are now living in a world where bond yields will trend higher, the US$ is trending lower, and oil prices could show upside pressures. In such a world, exposure to emerging markets once again becomes rewarding. In fact, one of the interesting feature of the current pullback is how volatility on US equities has actually been much worse than that of most emerging markets. Even after this week's pullback, Asian markets are significantly outperforming global equities. For example, our Asian Value UCITS fund (which focuses on developing Asia) is up +31.12% over the past 12 months, while our Asian Opportunities (which includes Japan, Australia and Asian bonds) is up +23.61% over the past 12 months. This compares favourably to the +19.4% gain in the World MSCI for the past year.

Still, the question at hand is whether we are now confronting a correction? The start of a crash? Or the unfolding of a genuine bear market?

ARGUMENTS FOR A CORRECTION:

We were due: record RSI indicators, record stretch without a 5% correction, first year without a down month etc...

As mentioned above, the investment environment is changing. Deflation should no longer be a concern. Central banks will no longer be as supportive of asset prices. The US$ is done rising. Oil is done adding liquidity to the system. Interest rates are moving higher... Any one of these forces would be a lot for the market to digest. But all together, they may be like Diderot's proverbial apricot, or Monty Python's wafer-thin mint: a little too much to chew on.

However, fundamentally, interest rates remain low, global growth is solid and so investors are likely to keep chasing returns?

“It's not a crash, it's a correction”.”

ARGUMENTS FOR A CRASH

Old card-sharks will always say that “if you sit down at a poker table and after 30 minutes, you have not figured out who the fish is, then you are the fish”.

Of course, in recent years, there have been no fish. Everyone won as all asset prices rose: equities, bonds, corporate bonds, real estate... It was just a question of relative performance with equities doing best of all. Still, as the equity bull market matured, it also evolved. Widening its reach and grasping the savings of an ever wider percentage of the population. So much so that, to a large extent, the bull market of recent years could be described as the ETF bull market. Indeed, according to data from research firm ETFGI, the ETF industry's assets under management (AUM) stood at $4.569 trillion in November 2017, compared to $3.396 trillion at the end of 2016. Assets under management of ETFs have grown by more than a trillion dollars in less than a year. Over 2016, in comparison, ETF assets grew by a relatively paltry $522 billion. Still, over the past two years, more than US$1.5 trillion of assets have flooded into ETFs. To put things in perspective, in 2017, the US mutual fund industry recorded a growth in assets of US$91bn. In short, last year, the growth of AUM in the ETF industry was basically ten times that of the mutual fund industry.

Now I manage money for a living. In fact, I took over the management of the Gavekal Global Equities Strategies almost exactly one year ago... and while the past three weeks have been tough (our overweight energy positioning did us no favors), we are still ahead of the World MSCI for the past 12 months (net of all fees):

The reason I highlight this is that I am sometimes called upon by our sales team to go pitch the fund. And invariably, a question that always comes up amongst smarter investors is “who are your other investors?”. And the reason smart potential investors ask this question is obvious enough: they don't care much for owning a fund with ‘Nervous Nellie’ investors who will panic at the first sign of trouble, hereby forcing the management of the fund (i.e.: my team and I) into liquidating assets at the trough of a cycle, when we should instead be focusing on picking up bargains.

The premise behind the (often-asked) question is that owning assets with a bunch of ‘weak hands’ is not an attractive long-term proposition.

This obvious enough common-sense brings me back to the massive inflows into ETFs that we witnessed in the past two years. Are the ETF inflows “sticky money” that will stay invested through the market's turmoils? Apparently, we witnessed US$30bn in ETF outflows last week (the first outflows in quite a while) and that was enough to create the dislocation we witnessed. What would happen to markets if those outflows reached 10% of the increase of the past two years, or US$150bn? What if the ETF outflows over the coming weeks reached 20%, or US$300bn? Who will take the other side of such large, incremental, marginal, trades?

To be clear: we have no way to know how sticky the ETF money will prove to be; if only because the inflows we have witnessed in the past two years are simply unprecedented. Meanwhile, the past few years have been so steady on financial markets that we have no real data to model how stable the ETF industry's AUM could prove to be in periods of stress. The only thing we know for sure is that the ETF industry is today a much larger beast than it was in 2008. And it is by and large an untested, and unknowable beast. And then, we also know that:

Historically, in periods of market stress, money tends to stay into mutual funds because mutual funds often charge upfront fees (the sunk cost fallacy), or because investors trust the managers they chose more than they trust themselves to navigate the market's choppy waters (the expert fallacy), or because they have done a fair amount of due diligence and thus want to validate their hard work (the sunk cost fallacy, again...) etc... Meanwhile, the whole point of ETFs is that they cost next to nothing to trade, that they do not require large amounts of due diligence, nor a relationship with a manager, etc... Thus, if we assume that the reason some of the ETF investors like ETFs is that they are easy to get into, and just as importantly easy to get out of, then should we not worry that some of the investors who chose ETF for the ‘easy liquidity’ will likely wish to exercise that very ‘easy liquidity’ now that the markets have started to head south?

Aside from higher liquidity, the other main reason investors like ETFs is the (perceived) low fees. And this is where the potential for disappointment could set in because of the difference in how ETFs and mutual funds trade. Let me use my own fund as an example. If tomorrow, an investor (Nellie Nervous), decides that she doesn't like the look of markets and no longer wants exposure to a global equity strategy, Nellie puts in her redemption form (before the agreed cut-off time) for, let's say, US$500k. I am then notified that by closing time tomorrow, US$500k will be leaving the fund. It is then up to me to decide whether I wish to reduce holdings across my 40 names proportionately, sell some of my exposure in US oil producers (in order to reduce the pain from my overweight energy stance), reduce some of my cash buffer etc... But whatever decision I have taken, by the next closing day, the money leaves the fund , Nellie Nervous receives her cash, which she can then deposit in short term UST, bitcoins, modern art, gold bars, etc...

Meanwhile, if Nellie owned US$500k of the QQQ (or SPX, or EWJ etc...), and decided to sell her ETF, what actually happens is that she places her sell-order with a broker, who (through the exchange) then turns to one of the “market-making” firms for that ETF. Assuming that, at this precise time, no-one is coming in to buy Nellie's ETF (hereby allowing for the shares to simply move from one investor's hands into another), then the market-maker (maybe Deutsche Bank, or Credit Suisse, or Morgan Stanley etc....) will give the exchange the price at which the market maker feels comfortable that it can unwind the position in the Nasdaq 100, or S&P 500, or MSCI Japan etc... And as we saw during the flash crash of May 2010, when markets unravel quickly, it can be hard for market-makers to keep up. At such times, the market-makers may well quote prices with greater and great discounts to NAV; which is how, back in May 2010, we saw a number of ETFs lose up to a third of their value, and sometimes more, while their underlying benchmarks were down just a few percent.

That was then. When the ETF market was much smaller, quainter, and less the plaything of the retail investment public than it is today. And so, with retail investors now in a full-on love affair with ETFs, let us imagine that, like a bad first husband coming out of prison, all of a sudden a liquidity squeeze like the 1987 crash or the 1998 LTCM meltdown re-appears. Not the start of a recession (a la 2001), nor a massive banking crisis (a la 2008), for neither looks likely today. But simply a good old fashioned liquidity squeeze, as investors realise that the investment portfolios they have constructed are now inadequate for the world in which we are moving (see A Once in a Generation Shift). With that, less us imagine US$150bn (or 10% of the past two year's rise in AUM) of outflows from ETFs (To be clear: this is pure speculation, for who is to know what the retail investors will decide to do tomorrow? For all we know, he/she may decide that the recent 10% dip is a terrific buying opportunity and buy more ETFs!). If this were to occur, then the questions that will rapidly appear will be:

Will the market-makers have the balance sheets to take on these transactions? If so, then

Will the market-makers have the appetite to take on these transactions? And if so, then

At what cost to the investment public, and profits to themselves (through higher spreads and discounts to NAVs) will the market markers decide to take on these transactions? If History is any indication, most likely a fairly large one. After all, what put the gold in “Goldman Sachs” and the more in “Morgan Stanley” has historically been the ability of investment banks to provide liquidity, at a high cost, to clients in the middle of a crisis. And if so, then

Will the general investment public conclude that both the ‘liquidity’ and ‘low fees’ attributes of ETFs turned out to be “bull market mirages”? And if so then

Will that realisation encourage yet more ETF selling, bringing us back to square one, above? Wash, rinse, repeat...

In other words, was May 6th 2010 the dress-rehearsal for what could soon happen in the ETF world?

Back then, a number of investors found out the hard way that the ETF's low fees hardly made up for the massive discounts to NAV that they suffered in the midst of a panic. With the experience of May 2010 in our rear-view mirror, and with a broader market sell-off now in the front and centre of any investors’ concerns, will investors once again be forced to confront the question of what is the point of saving 0.2% per annum in management fees if, when one wishes to sell in a panic, one ends up selling one's ETF at a 20% or more discount to NAV? Are ETF investors who think they can liquidate in a downturn going to have proven themselves to be “penny wise and pound foolish”? Will they be the fish to the card-shark investment banks?

ARGUMENTS FOR SOMETHING WORSE?

In the Spring of 2008, the global economy was humming along. In fact, for those of us sitting in Asia, it was hard not to feel very enthusiastic about the future: the Asian Crisis was falling off of our ten year rear-view mirror, China was delivering the greatest rise in purchasing power, over the greatest number of people in one generation, ever recorded in the history of Mankind (that's humankind for our Canadian friends). India looked set to join the global economy. Indonesia and Malaysia were developing fast, partly thanks to rising commodity prices, and partly thanks to attractive demographic profile. Even Brazil, of whom it was once said that “it is the next emerging market, and always will be’, was thriving.

Things were good. And then things turned bad very quickly.

Things were bad because the financial regulators, especially in the US but also to some extent in Europe, fell asleep on the job. They allowed banks to expand their leverage from the time-tested 10x, up to 40x and beyond. They rubber-stamped the creation of financial products that made little sense, (such as squared CDOs, PIK loans etc...) except that they allowed yield starved investors to gorge themselves - but without realising the risks they were taking as they did.

Could History repeat itself?

Probably not, if only because banks are nowhere near as levered as they were in 2008.

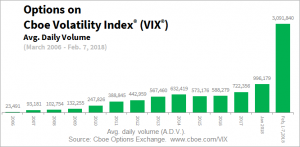

Still, one nagging concern is that, for the past five years, investors of all size and stripes (even small retail investors) came into the market day-in/day-out to sell volatility (daily volume on VIX options has risen from 23k in 2006 to 3m today!). This constant selling of volatility was just another way to ‘reach for yield’. And needless to say, the consequent downward pressure on volatility was very bullish for risk assets.

Projecting ourselves forward however, we can probably assume that the number of investors rushing to sell volatility forward will now be constrained to a smaller group of traders who actually understand what they are doing? Logically, this should mean that volatility should settle back closer to its long term mean of roughly 17%. If so, then that would mean that we would now confront an environment of higher interest rates and higher volatility.… And if we have higher interest rates and higher volatility baked into the cake, doesn't that almost guarantee lower PEs?

Following up on the above idea, we have seen in recent years, especially in the US, a rapid growth in quant funds, CTAs and risk parity strategies (witness the steady rise in SPX options trading). However, a number of these strategies were, in essence, levered longs on bonds and equities simultaneously, on the premise that bonds and equities are negatively correlated. However, as we surmised in our most recently Monthly, what happens if bonds and equities stop being negatively correlated? Well, obviously we now know the answer: the risk-parity, quants and algo traders have to start deleveraging their balance sheets aggressively in a market where the marginal buyer has, all of a sudden, disappeared. And the reason the marginal buyer has disappeared is that in recent years’ (as the picture below makes clear), the marginal buyer has started to look very different from the marginal buyer of past bull markets:

Which brings us back to the “yield-chasers” mentioned above. In my careers, every bear market has started with the ‘yield-chasing’ investors getting burnt. It is almost as if “the bear” enters a room and decides ‘First, I will eat the yield chasers. They are the easy preys. Then, if I am still hungry, I will eat the momentum guys. And if I am still hungry after that, I will have the value investors for desert’.

The fact that the yield chasers just got destroyed doesn't mean that, de facto, the momentum and value guys are next. Maybe the bear has had its fill, and goes back to sleep (after all, it is hibernating season)? But still, when the yield chasers get eaten, we momentum and value guys have to realise that we are potentially next on the menu...

And all this brings me to perhaps the single most important reason to be cautious given recent developments: namely the fact that this is now the second crisis in a decade where US regulators have shown themselves to the world to be completely hapless.

After all, if the current sell-off really is the direct consequence in the implosion in the XIV.US, and other such products, then the first question we should ask ourselves is why these products even existed in the first place? I mean, what economic interest was served by allowing retail investors to pile their hard-earned cash into a product that, through its very conception, had an extremely high probability of being worth zero at least once, if not twice, a decade?

Are we back to where we were ten years ago, when all of a sudden, we all had to figure out what a CDO-squared was and how they could implode the global financial system?

It is it just that, this time around, it's just a different bunch of letter but the core principle stays the same: let's create products that allow the average punter to reach for extra yield, even at the cost of getting blown up once a decade! The ultimate “eat like a bird and sh.t like a cow” trade?

Honestly: why would US regulators even allow things like 3x levered Brazil ETFs, or worse yet, inverted VIX ETFs who, by design, are destined to go to zero in a time of market stress? What economic benefit is there to have such products offered to the general public? Or more appropriately, what point is there to have a financial regulator is the regulator allows for things like a reverse VIX ETF, or futures on Bitcoins?

Unfortunately however, if the past is any indication, regulators will respond to this latest market hic-cup by telling money managers how they can pay for research, or by clamping down further on offshore tax havens, or by dictating firm's compensation policies... More regulations, of things that had nothing to do with the crisis in the first place! Thus, if the end result of all this is more lawsuits (one can bet one's bottom dollar that a number of the investors wiped out in the Volageddon will not take their losses lying down), more regulations, higher interest rates and higher volatility... then it is hard to walk away from the past week with a strong “risk on” mentality?

Or at the very least, a strong “buy the dip” mentality. For there are still risks that offer attractive returns across a number of equity markets around the world. It may however, be very different markets, and different segments of the markets, from those who have done so well for investors over the past five years.

As always, please do not hesitate to reach out if you have any comments or questions.

Yours truly,

Louis-Vincent Gave

PS: PLEASE NOTE THAT THE ABOVE REPRESENTS MY PERSONAL VIEWS AND IS IN NO WAY AN OFFER TO BUY/SELL ANY SECURITIES.

Although we have been writing about it for many years now, it may be worth updating for those who do not know about it, some of the advantages of having our investment portfolios deposited in banks in Luxembourg. For most, the most obvious advantage would be to be able to hold the money while avoiding country risk or the risk of insolvency of Spanish banks, with Luxembourg being the EU Wall Street par excellence, once London ceases to be so due to Brexit. However, there is a much more powerful reason to manage most of our financial wealth from Luxembourg. And that reason is access to any investment fund, private equity, real estate fund, etc. in the world, even if it is not registered for marketing in Spain.

.

This freedom of access is no trifle when one realises that only 10% of the existing funds worldwide have this registration with the CNMV in order to be marketed in Spain. Therefore, investors who do not have adequate advice will never be able to access a 90% of funds, which logically include some of the best managed funds in the world. Furthermore, no bank in Spain, not even to its private banking clients, offers just that 10% registered with the CNMV in its entirety, as the sales catalogues are usually limited to 2, 3 or 5 thousand funds, with the excuse that they belong to different trading platforms, etc. Therefore, the opportunity cost of magnificent investment options that the local investor cannot access is enormous. In fact, this condemnation of mediocre investment is one of the main reasons for the the causes of brick abuse in Spain, although we have already discussed it extensively in other articles.

.

The question many of you will ask is why most funds are not registered in Spain for marketing, or at least why the star funds managed by some of the world's leading managers do not do so. There are several reasons: among them are funds that do not consider marketing in Spain because it is expensive for the small volume they would achieve in our country. We must not forget that marketing in Spain, through the network of financial institutions and platforms that operate here, in many cases involves a cut of more than 50% of the commissions charged by the fund manager. In fact, some fund managers, such as Carmignac, decided at the time to create an ad hoc class in their funds for marketing in Spain, with higher fees than those applied to the rest of their classes, in order to satisfy the voracity of local financial institutions. At Carmignac, these classes were shamefully labelled with the «E» for Spain.

.

However, the marketers' bites are not the only reason that many international fund managers have for not registering their funds for sale in Spain. Another important reason is that the only doors that registration in Spain would open for them is to access Spanish retail clients, since larger or institutional clients can access funds that are not registered in Spain without great difficulty. Investors with a few million and who are well advised already have their own investment vehicles in banks abroad that allow them to access all types of funds beyond the CNMV's list of marketable funds. In other words, fund managers not registered in Spain do not need to register or pay any bribes to attract these Spanish millionaires.

.

There are also other reasons for some managers to disdain the Spanish retail investor market, such as specialisation in institutional clients or geographical remoteness. It is common that some managers from China, Thailand, India, etc., whose investors are essentially Asian, Middle Eastern or North American, do not prioritise attracting Spanish retail clients at all. And they usually focus on marketing in Europe through the British or German market, either for retail or institutional investors, but with higher volumes and lower bites than in Spain.

.

The consequence of all this is that the Spanish retail investor is condemned to a very limited portfolio of funds that have previously agreed to pay juicy commissions to the financial institutions that market them in Spain. And for these investors who do not have tens of millions, the fact of being able to invest much more modest amounts from Luxembourg, with exclusive personal vehicles that open the doors to any fund in the world, means the difference between mediocrity and brilliance of investments in terms of quality and results.

.

Luxembourg, as a good «EU friendly» financial centre, has various types of investment vehicles that adapt to the needs of each size and type of investor. But for the smaller investor, who is the most disadvantaged by the restricted range of funds to which he has access in Spain, there is a a personal and exclusive Luxembourg vehicle from which you can invest your portfolio with complete flexibility,from as little as 250,000 euros. Obviously not all retail investors have a minimum of 250,000 euros, but it is a huge step for the average investor to be able to put their investments on a par with those of any institutional investor with 10 or 20 million from as little as 1/4 million. And these vehicles not only allow access to any fund in the world, but also to any fund in the world. also allow for the deferral of capital gains generated within these vehicles indefinitely., The tax is only levied on the proportional part of the capital gain when it is decided to redeem part or all of the investment. In other words, once we have this minimum of 250,000 euros in our own investment vehicle, we will be able to buy and sell any fund, share or whatever we want, without paying tax on the capital gains until we need to withdraw all or part of our money. Taxation is exactly the same as when we buy any fund registered in Spain that is sold to us by the bank on the corner, but without the need to jump from one transferable fund to another within the limited list of funds registered with the CNMV, but with total and absolute freedom in the world universe of UCITS, non-UCITS, AIFMD, Private Equity, Real Estate Funds, shares and other financial products. This is why we chose a Luxembourg vehicle, totally «friendly» with the taxation and transparency of EU countries.

.

These vehicles are logically deposited in banks in Luxembourg, although as mere depositaries, it matters little that they are more solvent than Spanish banks, since we will only use them for the safekeeping of the vehicles and the portfolios with the fund units or shares that we are going to buy and sell in them.

.

As for costs, we have been able to fine-tune them over the years due to the growing volume of clients. And currently the total cost of a Luxembourg unit-linked vehicle for a small investor (minimum 250,000 eur) can be around 0,6-0,7%annual, The volume of vehicles in the market is significantly reduced as the volume increases. Furthermore, in certain circumstances, these vehicles also avoid the payment of Wealth Tax, which in some Autonomous Communities does not have a rebate.

.

Obviously, as Luxembourg is the financial centre of choice for the EU - replacing the City of London - any capital to be invested in such vehicles must have a justified origin, be fully declared and transparent, as Luxembourg's tax haven connotation is now completely behind us and definitively buried by the EU's own imperative.

.

In short, in 250,000 can access vehicles that cost less than 0.6-0.7%, that efficiently defer Capital Gains, that can save Wealth Tax, that allow access to investing in the best investment fund managers on the planet rather than just 10% of them, and with the banking and legal security of a world-class financial centre in the heart of the Eurozone. That is nothing, in these times of uncertainty, insolvency and disguised risks.

.

For those who see the remoteness of having their money in Europe as a handicap, I would like to remind you that, in addition to being able to manage it conveniently, swiftly and closely through Spanish advisors and professionals, having a Luxembourg investment vehicle is not exclusive. In other words, most investors combine a (more or less majority) part of their assets in Luxembourg with a part held in banks in Spain, as a temporarily invested treasury, which will be consumed or used over the coming quarters, semesters or even years.

It is very curious to see how in Spain there is a very different mentality regarding the allocation of household assets to that of American households. As you can see in the interesting chart published by Inbestia and reproduced below, approx. 80% of Spaniards' assets are allocated to real estate, i.e. the main residence and additional real estate. Therefore, less than 20% are allocated to financial assets, such as shares (listed or unlisted), investment funds, pension funds, life insurance, deposits, etc.

.

If we compare the allocation between Americans and Spaniards, we will see that the preference for companies in the world's leading economy is much greater than in Spain and most other countries (although it would be interesting to know the figures for the north of the EU, which we suspect must be closer to those of the US). The entrepreneurial culture of North Americans is much greater, and half of their assets are invested in both listed and unlisted shares (mostly in their own businesses or with partners), investment funds, pensions and life insurance.

Why are Americans more inclined to allocate their wealth and savings to companies in general? Do we in the rest of the world not like our money to work for ourselves? Haven't the real estate bubbles affected Americans as much or more than Spaniards? The answers are not simple, but rather an accumulation of factors that make up the difference between one financial allocation and the other. Let's look at some of these reasons:

.

The financial culture in which American society is growing up has an entrepreneurial tradition and the majority of the population is clear that the only engine that moves the country and that can lead them to well-being is to participate in one way or another in the creation of wealth achieved by companies. Either as employees seeking hierarchical job progression or as small entrepreneurs (franchisees or with small personal businesses). They expect little more financially from their state. By contrast, in Spain and much of the rest of the Western world, there is less of an entrepreneurial culture, and more reliance on state-dependent labour activities, which are generally a little less liberal and a little more interventionist than in the USA.

.

Another aspect that makes Spaniards more inclined to accumulate our wealth in real estate than Americans is precisely the unpleasantness that the financial sector has been giving us in recent decades. For our banks, even today, volatility is the demon from which they recommend their clients to flee. To this end, they offer them all kinds of products and structured products with the obsession to reduce volatility, a concept that they mistakenly consider to be synonymous with risk. And of course, when volatility is confused with risk, it is much easier for the banking sector to sell low-volatility products than high-volatility ones. What customer will not try to avoid a high-volatility product if they are told about high risk?

.

Therefore, the general opinion of Spanish savers is that it is much riskier to invest in the stock market than in less volatile banking products or in real estate. And here we come to the second derivative: How have the low-volatility banking products sold by banks in recent years been performing? Well, in the best of cases they have been mediocre, and in the worst of cases they have been abused or have been directly sentenced to court, as in the case of the preference shares. This unhappy end to many of the low volatility products has exacerbated Spanish investors' appetite for real estate, reaching the extremes in Spain that we have seen in the graph: almost 90% in real estate and assets of their own personal business, such as self-employment, etc.

.

The right balance of wealth should moderate real estate and boost financial investment to levels similar to those seen in the USA (not for nothing is it the society with the leading wealth and GDP per capita on the planet). Families should enjoy financial investments that work to generate wealth for their old age, as the state pension is not going to do this sufficiently (and even less so in Spain). In addition, the US regulator limits more and better the access of retail investors to structured products and other nonsense that Spanish banks sell with impunity to any retiree without financial knowledge. This limitation on the sale of complex products to retail clients in the USA also channels a good part of these small savers to ordinary equity funds, which are less afraid of volatility and more inclined to buy the idea of investing in companies.

.

And what about real estate - does it not also guarantee the generation of income for our old age? The answer is yes, but with some additional risks that need to be highlighted: By massively concentrating our assets in real estate, we will be at the mercy of geographical risk, local economic risk or country risk, and the risk that the real estate cycle will no longer be favourable to us when its growth becomes saturated. Not to mention the risk of non-payment, maintenance and rising taxes on property owners. The diversification and freedom of movement that comes from acquiring shares in good companies all over the world, creating wealth in the most diverse sectors and countries on the planet, is hard to achieve with real estate investment. And the capacity of the business world to adapt and overcome whatever the future circumstances of the economy may be in the coming decades will never be able to be achieved by the inert brick.

.

Finally, the common characteristic of new clients who come to Cluster Family Office has always been the overload of properties in their portfolio. A lack of diversification that many paid dearly for with the bursting of the real estate bubble after 2007. And one of the first things we do for new Clients is to replace real estate and rentals with financial investments through versatile and fiscally efficient vehicles. They should make their money work for the family, either by generating alternative income to rents by buying good alternative funds or by seeking to grow portfolios by buying good equity funds from around the world. The volatility - not risk - that can be assumed by each family and professional circumstance in the financial portfolio should determine the proportion of investments in company shares or in alternative strategies that generate more stable income.

As Machado said, only a fool confuses value and price. From the point of view of the long-term investor, who buys shares in good companies at attractive prices relative to their present and future earnings multiples, it would already be absurd and foolhardy to buy and sell these shares in the short term without associating these decisions with the value of the respective businesses. But it would be even more absurd to do so. short term trading in a portfolio of actively managed mutual funds, The investor can also set up tempting automatic buy and stop-loss (sic) orders, with portfolios at the free will of their respective managers.

.

That is what ING offers to their clients, with the consequent benefit to the bank for this service, obviously. But as it is not as simple operationally to automatically buy and sell a fund at a pre-established price as it is for a share, what they offer their clients is a «warning» service when the fund's price reaches the marked price. It is then that the client will decide whether or not to sign a buy-sell-transfer order for these funds, which will usually take a couple of days to execute. Oh, and of course, this «service» is only available for ING brand funds, which means that everything stays at home.

.

In a review of the practice of share trading (including stop-loss), we have to say that it is the usual modus operandi of savers who are less qualified as investors. In other words, those who move away from long term investment by buying businesses whose good value/price ratio they know, and instead approach the mere bet on any ticker listed, regardless of the good or bad performance of the listed company's business. They are even oblivious to whether there are prospects and an adjusted valuation of a company's business, a commodity, an index or any derivative behind that ticker. For most of them, it is enough to have a ticker or a changing price to bet on more or less frantically, conveniently dressing up this practice with all kinds of trading courses, technical analysis and macros that disguise their gambling with a patina of expert investment.

.

However, generally speaking, an investor who knows the value of the companies in his portfolio will be more interested in buying them the more the price of their shares falls. Conversely, the more expensive the shares are in relation to the value of the company, the more interested he/she will be in selling them. In contrast, short-term stock trading is associated with completely ignoring the real value of the company. This is why technical analysis and other trading methods usually recommend buying stocks when prices are rising and selling them when they are falling. (Here we could make the exception of the very few quantitative hedge funds that have been making money for decades, but they would be the exception that proves the rule and would only be the exception that proves the rule. accessible to well-informed investors and with capital in excess of 300.000′- euro).

.

As we said, ING is now tempting its clients to carry out this trading practice also in their portfolios of actively managed funds. Active management is so called because the manager of each fund actively makes decisions by buying and selling stocks or bonds. From there, the net asset value of the fund will be the -usually- daily quotation of the entire portfolio at market price, after deducting the commissions and expenses of the active management itself and of the fund (on active and passive management you will be interested in the article that Cluster Family Office recently published on the website of COBAS AM, the manager of Francisco García Paramés: «Passive Management, Active Management»). Therefore, it makes even less sense for the saver to make decisions to buy or sell the fund when, not only does he not know the value of the businesses bought, he does not even know which businesses he has bought and sold. The manager of such a fund or the liquidity it accumulates on a daily basis. It would also not allow you to benefit from one of the key investment drivers that every value manager strives to achieve: co buy low and sell high, since such trading and stop-losses would completely detract from good active management.. Moreover, as fund trading is an absurd and rare practice, the saver would not even have the possibility to benefit from the self-fulfilling prophecy that technical analysis sometimes offers.

.

In short, yet another brainstorming strategy of the Machiavellian marketing department on duty, whose priority has never been and never will be the customer's benefit, but that of the financial institution itself. More wood to keep savers away from the right investment path.

El Euro sube. Y lleva ya casi un 5% de recuperación desde sus mínimos por debajo del 1,04 respecto al dólar. Pareciera que puede más la fortaleza de la locomotora alemana que la debilidad del Sur y el Este de la UE. Como si por el hecho de haber reconocido que se avanzará a -al menos- dos velocidades, ello permitiera que la divisa única dejase atrás sus incertidumbres.

.

Es como si la cifra publicada por el IFO alemán (112,3) superior a la esperada (111), fuera capaz de reafirmar y acelerar la subida de tipos en Europa, al más puro estilo norteamericano. Es cierto que esa y otras cifras reafirman la recuperación económica germana, pero esos árboles de optimismo inequívoco no nos deben impedir ver el bosque en el que está sumido la moneda única. Y ese bosque no es otro que la inviabilidad precisamente de su cualidad de única. O sea, que aún se comparte el Euro entre muchos países que están lejísimos de ni tan siquiera imaginar una relajación de las facilidades cuantitativas con las que inunda el BCE las economías del Sur. Y ello hace imposible una subida de tipos que, paradójicamente está descontando el Mercado con la recuperación del Euro respecto al dólar.

.

¿A dónde nos lleva esta paradoja? Pues a que cuanto más descuente el Mercado una subida de tipos del Euro y una reducción de la relajación cuantitativa por parte del BCE, más próximos estaremos a la materialización de las dos velocidades de la Eurozona, y por tanto de la ruptura de la cotización única del Euro. Ya que, o bien el Euro pierde su condición de moneda única y empieza a cotizar de manera distinta en cada velocidad de la Eurozona, o bien la subida de tipos es imposible, en cuyo caso el precio del Euro respecto al dólar y resto de hard currencies debería volver a cotizar el riesgo de explosión de la propia Eurozona (según el adjetivo utilizado por los propios dirigentes de la UE para justificar esas dos o más velocidades) y caer de nuevo a mínimos.

.

Si se mantiene una única cotización del Euro, es imposible subir los tipos, puesto que en el Sur no nos lo podemos permitir. Aquí necesitamos tipos cero e inflación abundante que se coma la deuda poco a poco. Sin embargo, en el núcleo duro alemán, lo que no pueden ni van a permitir es no subir tipos y que su temidísima inflación les repunte más allá de lo deseable. Por lo tanto, ante tal dicotomía, o bien Mr. Market está caminando en dirección contraria, o bien las ya anunciadas dos velocidades están a la vuelta de la esquina.

.

Tampoco es baladí la ruda reacción de Dijsselbloem, que denota que muchos europeos del norte ya no se sienten obligados a tener ni siquiera corrección política con quienes consideran que de facto ya no forman parte de su core o núcleo duro europeo. Sus disculpas, forzadas, ligeras y tardías delatan ese sentimiento de desapego y desconexión que los habitantes e inversores del Sur parece que todavía no hemos comprendido. Lo curioso es que el inversor de a pie del Sur ha asumido lo de las dos velocidades sin percatarse de que ello implica dos cotizaciones de divisa y dos tipos de interés diferenciados. No en balde Guy Verhofstadt (sí, el mismo que está supervisando desde la UE la negociación del Brexit) ya dijo públicamente que debía crearse un segundo banco central en Bruselas. Dos velocidades, dos autoridades monetarias… Blanco y en botella, y hay que estar preparado para ese escenario.

.

Para hacer la tortilla de las dos velocidades hay que romper la cáscara del Euro. Hay que partir la moneda «única» en dos. Y aunque aunque lleven el mismo nombre y tengan prácticamente la misma cotización inicial para evitar pánicos, tendrán valoraciones distintas y tipos de interés distintos al cabo de poco tiempo. Serán diferencias de tipos y cotización acordes con las necesidades de las distintas economías, como no podría ser de otra manera. Y lo más curioso es que incluso algunos inversores institucionales, que sí llegan a imaginarse la materialización de esas dos velocidades y dos políticas monetarias, confían sorprendentemente en que España estará en la primera velocidad! ¿Por qué? Pues porque el gobierno español así lo ha dicho, enarbolando el mayor crecimiento de PIB de la Eurozona, pero obviando el déficit presupuestario, el endeudamiento y el paro estremecedor y endémico. Y ya se sabe, los gobiernos, especialmente los de la periferia europea, siempre aciertan en sus pronósticos ¿verdad?

It is now official. In the covers The inevitable news of a death more than foretold by a few, who branded us as quasi-aliens for predicting the break-up of the Eurozone five years ago, has already been published all over Europe. Hollande and Merkel have chosen the pompous Palace of Versailles to announce that the EU of 27 has no future and that the Eurozone of 19 should at least go at two speeds. And so as not to panic the markets in the face of such an official statement, the announcement was staged with two guests of stone. The two guests with the largest - and therefore most dangerous - economies in the Eurozone: Italy and Spain.

.

In this way, the statement manages to give the desired image of North-South coordination. I mean coordination as such, not as an image of unity in any case. After all, it would be strange if the announcement of a two-speed Eurozone were staged exclusively with representatives of the first speed, wouldn't it? Moreover, as if the announcement were not already a hot enough potato in itself, it has been taken up by four presidents, three of whom are in precarious positions at the helm of their countries. Hence the precariousness also of the only apparent control of the situation.

.

Nor is the tone and vocabulary chosen by Hollande in the the interview a chorus of journalists from the media chosen ad hoc to cover the Versailles announcement (Le Monde, The Guardian, La Stampa and Süddeutsche Zeitung). When the journalists asked the French president why he was staging the announcement together with Merkel, Gentiloni and Rajoy, his answer was precisely scripted: «...the French president's answer to the question was: 'I am not a Frenchman, but a Frenchman.«Angela Merkel and I consult each other regularly. Before all European Councils and on all issues. It is in Europe's interest. But it is not an exclusive relationship. With the 60th anniversary of the treaty being celebrated in Rome on 25 March, it seemed logical to us to associate Italy and invite Spain«. In other words, Hollande and Merkel are managing the decisions, and for the staging (to be in the photo) willingly and graciously associate themselves with Italy (as a gesture of respect and recognition of a historical partner of the EU since its creation) and invitegenerously to Spain. Both as representatives of those of us who do not belong to the hard core of decision-making or to the high-speed economies. A gesture to reassure a periphery that might otherwise reject such a statement outright as totally alien to it if «someone of its own» is not included in the photo.

.

We are undoubtedly facing the official recognition of the opening of a melon that no one is even remotely sure how to handle. But whose staging, with representatives of the two speeds hand in hand and in apparent agreement (as it could not be otherwise), should open the eyes of all of us who seem condemned, due to our bad head/economy, to the 2nd speed. At this point we must insist once again on the warnings (here, here y here) that we have been making to investors in order to avoidance of asset depreciation(both financial and real estate) that such a broken Eurozone and 2nd speed inherently entail.

.

Now that it is no longer taboo or politically incorrect to talk openly about a two- or multi-speed Eurozone, political and financial analysts around the world have begun to publish its possible scenarios. Particularly surgical is the analysis of Wishart, Rojanasakul and Fraher from Bloomberg, in which they present 3 scenarios involving the break-up of the Euro. And 3 other scenarios that would allow maintaining a single Eurozone and a status quo as it is today for some time to come. In any case, we are already in a Europe that is somewhat more realistic and very different from the one that has been simulated for so many years. The 2017 ballot boxes will largely decide when the Eurozone breaks up and the future of today's Europe, which is much better than what happened in the old Europe whose destiny has historically been marked by wars. In the meantime, investors in the south should take safety measures and prepare to live in 2nd gear but enjoying 1st gear assets.

We have been made aware of phishing and spoofing attempts involving fraudulent email addresses and domains that closely resemble our official company communications. These unauthorized communications are not sent by our company and may falsely impersonate our employees or representatives.

Our company is not responsible for communications, requests, or transactions originating from fraudulent or unauthorized email addresses or domains. Please verify that all communications originate from our official email domain before responding or sharing any information.

If you receive a suspicious email claiming to be from our company, please do not respond, click any links, or provide any information. Contact us directly using the contact information published on this website to verify its authenticity.

Luxembourg, as a good «EU friendly» financial centre, has various types of investment vehicles that adapt to the needs of each size and type of investor. But for the smaller investor, who is the most disadvantaged by the restricted range of funds to which he has access in Spain, there is a a personal and exclusive Luxembourg vehicle from which you can invest your portfolio with complete flexibility, from as little as 250,000 euros. Obviously not all retail investors have a minimum of 250,000 euros, but it is a huge step for the average investor to be able to put their investments on a par with those of any institutional investor with 10 or 20 million from as little as 1/4 million. And these vehicles not only allow access to any fund in the world, but also to any fund in the world. also allow for the deferral of capital gains generated within these vehicles indefinitely., The tax is only levied on the proportional part of the capital gain when it is decided to redeem part or all of the investment. In other words, once we have this minimum of 250,000 euros in our own investment vehicle, we will be able to buy and sell any fund, share or whatever we want, without paying tax on the capital gains until we need to withdraw all or part of our money. Taxation is exactly the same as when we buy any fund registered in Spain that is sold to us by the bank on the corner, but without the need to jump from one transferable fund to another within the limited list of funds registered with the CNMV, but with total and absolute freedom in the world universe of UCITS, non-UCITS, AIFMD, Private Equity, Real Estate Funds, shares and other financial products. This is why we chose a Luxembourg vehicle, totally «friendly» with the taxation and transparency of EU countries.

Luxembourg, as a good «EU friendly» financial centre, has various types of investment vehicles that adapt to the needs of each size and type of investor. But for the smaller investor, who is the most disadvantaged by the restricted range of funds to which he has access in Spain, there is a a personal and exclusive Luxembourg vehicle from which you can invest your portfolio with complete flexibility, from as little as 250,000 euros. Obviously not all retail investors have a minimum of 250,000 euros, but it is a huge step for the average investor to be able to put their investments on a par with those of any institutional investor with 10 or 20 million from as little as 1/4 million. And these vehicles not only allow access to any fund in the world, but also to any fund in the world. also allow for the deferral of capital gains generated within these vehicles indefinitely., The tax is only levied on the proportional part of the capital gain when it is decided to redeem part or all of the investment. In other words, once we have this minimum of 250,000 euros in our own investment vehicle, we will be able to buy and sell any fund, share or whatever we want, without paying tax on the capital gains until we need to withdraw all or part of our money. Taxation is exactly the same as when we buy any fund registered in Spain that is sold to us by the bank on the corner, but without the need to jump from one transferable fund to another within the limited list of funds registered with the CNMV, but with total and absolute freedom in the world universe of UCITS, non-UCITS, AIFMD, Private Equity, Real Estate Funds, shares and other financial products. This is why we chose a Luxembourg vehicle, totally «friendly» with the taxation and transparency of EU countries.