Following on from our article entitled «The shortcomings and dirty secrets of ETFs and index funds«, in which we explained that not all that glitters is gold when it comes to passive management – which is so fashionable these days – we’re going to summarise and discuss the an interesting study carried out by Alexey Panchekha, CFA, on the blog CFA Institute’s Enterprising Investor. In this study, this specialist and researcher in mathematical applications for risk management – who has worked for Goldman Sachs and Bloomberg, amongst others – explains what he has termed the The Active Manager’s Paradox. Let’s see what he is referring to and how the findings of his study might be useful to the average investor.

.

The million-dollar question is: Is the reason why active management has lost ground to passive management over the last decade down to the high fees they charge, the fund managers’ lack of skill, or some other factor?

.

What is needed to answer this question rigorously is not a thoughtless, speculative or emotionally charged response from fans of one management style or another. That is why this study is based on facts regarding the decisions made by active fund managers. As the saying goes, you can hardly manage what you cannot measure.

.

Panchekha has analysed how active managers generate alpha with their selection of companies. They have carried out a multi-year study covering 114 US investment funds belonging to 57 different fund families, and have evaluated more than 400,000 one-year periods of returns (details of the methodology used in the study can be found at the end of this article). Taken together, the study’s sample represents 2 trillion (US trillions) in assets under management.

.

The key lies in the managers’ level of conviction. In other words, the level of certainty that fund managers have regarding each sub-group of companies in their portfolios. To determine this, the study distinguishes between overweight and underweight positions rather than simply the absolute volume, which could be distorted by the mandatory weightings in their respective benchmarks. The study therefore distinguishes between three types of shares in portfolios:

Those with a higher weighting or where there is greater conviction

Those that are underweighted or where conviction is lower

The neutrals

The components of these three categories are identified by measuring their portfolios and weightings on a daily basis, with each group being rebalanced every 14 days. The data was obtained from the Hercules database, provided by Turing Technology Associates. The results, shown in the chart below, illustrate the success rate of each category compared with its respective benchmark indices over successive one-year periods, as well as the annual alphas achieved during those periods.

The Impact of High-Conviction Overweights, Excluding Fees

The Impact of High-Conviction Overweights, Net of 85 basis points’ Fees

As can be clearly seen, overweight or high-conviction positions – comprising the fund managers’ best ideas – are the only category that actually generates alpha in excess of the indices. In 84% of cases when looking at gross returns, and in 74% of them when considering net returns with an average of 85 basis points in fees paid. By comparison, both underweight (lower-conviction) and neutral positions generated a gross success rate of 50% (pure beta), which would fall below that threshold after paying those same fees.

Warren Buffett, Letter to Shareholders, 1966.

.

High-conviction overweight positions – that is, those in which fund managers have the greatest confidence and certainty – are the only parts of their portfolios that generate returns in excess of their benchmark indices. Therein lies the paradox: although active fund managers demonstrate an ability to outperform the indices when selecting their preferred shares, they lose that ability when designing the rest of their portfolios in their eagerness to round them off, diversify them, balance them or reduce their «risk», once again confusing risk with volatility. In some cases, it is a lack of courage, a lack of conviction, or simply that many of them have their hands tied by the ratios and indices which, according to their prospectuses, they are required to follow in a certain way. The reason doesn’t matter. What the study shows is that only overweight holdings and those with high conviction manage to outperform the market. Any other asset allocation will reduce returns.

.

But that’s not all. Furthermore, according to the study, the average fund manager self-sabotages their returns by reducing their high-conviction positions to a meagre 55% of their portfolios. The corresponding allocation to underweight and neutral assets, accounting for almost half of their portfolios, therefore amounts to a beta ballast unbeatable. To illustrate this, Panchekha gives an example from American football, but the equivalent here would be as if the Barça manager only fielded Messi for 55% of the 90 minutes of play.

Of course, there is a reason why fund managers choose to carry this beta burden. For example, adding a market-neutral component reduces the fund’s tracking error relative to its benchmark – something that is surprisingly valued by the sector and some investors. It also reduces the likelihood that the fund’s performance will be exposed to the competition, which is out to poach clients from one another. But in any case, the study shows that all these «risk management» measures – which are of such concern to the industry and to poorly advised investors – inevitably come at the expense of returns, and are acts of cowardice or, at best, of insecurity.

.

The result of this combination of a lack of conviction (in the quality of their analysis) on the part of active fund managers, their lack of courage to set themselves apart from other fund managers, and the regulatory and corporate constraints they face, leads them to manage «risk» in a way that is – paradoxically – risky which causes them to lose everything they have gained and more. The following graph illustrates the harsh reality, Most active fund managers do not deserve the fees that investors pay them to outperform the market, since almost half of their portfolios fail to do so, and the costs do the rest. The problem is that the statistics do not distinguish between diversified and concentrated portfolios. In other words, portfolios in which 90 or 100% of the shares are high-conviction picks, compared with portfolios where, according to the statistics, only 55% of the shares are high-conviction picks.

Actively Managed Large-Cap Mixed-Asset Mutual Funds vs. the S&P 500

Whilst it is common practice in the financial industry to blame high fees for the poor performance of most actively managed funds, Panchekha’s study reveals that fees are only a secondary factor. In other words, Diluting the sole source of alpha in portfolios to levels of 55% has a far more devastating effect on returns than the fees paid. Returning to the football analogy, whilst Barça fans are blaming the team’s mediocre form on the exorbitant bonuses the manager receives (or on the condition of the pitches, or the weather, or injuries, or the referees, etc.), they should instead be criticising him for systematically leaving Messi on the bench for almost half of the matches. Panchekha states, and I quote:

«Whilst it is standard practice in the industry to attribute these outcomes to higher fees, our research suggests that fees are only a secondary factor. Diluting the sole source of stock-selection alpha to a minority component of a portfolio has a far greater structural impact than higher fees.»

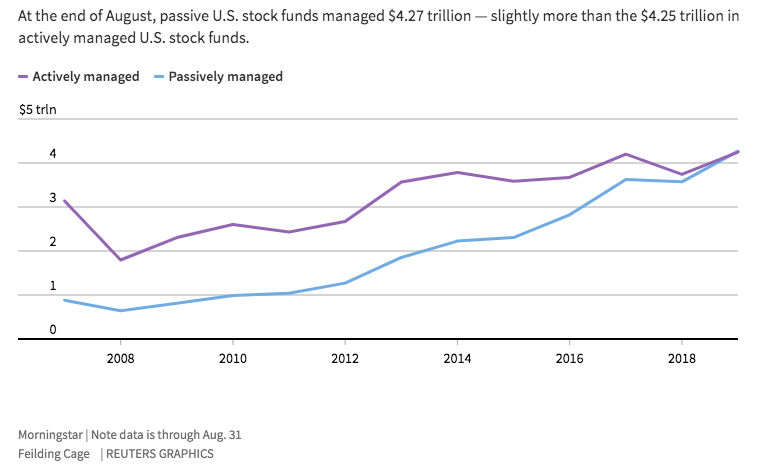

The now legendary underperformance of most actively managed investment funds relative to their benchmark indices has led US investors to withdraw $1.3 trillion (US trillions) from these funds and invest it in the growing passive fund and ETF sector, according to data from Morningstar.

.

The study presents averages and samples of funds without distinguishing between concentrated and diversified portfolio managers. If we separate the wheat from the chaff, that is to say, if we select managers of small portfolios, composed entirely of shares in which they have a very high degree of certainty and conviction, we will find a great deal of alpha and very little drawdown, despite their fees which, as we mentioned in the previous article, tend to be quite high. The NET returns of these star-manager funds, with boldly concentrated portfolios and an in-depth understanding of the businesses in which they invest, clearly and consistently outperform their respective benchmark indices over time, regardless of their TER. Or does any Berkshire Hathaway shareholder really care about Buffett’s salary or that of any of its current executives? And if, at any point, the returns on that holding company were to decline alarmingly, shareholders should be looking more closely at whether its management is beginning to compromise the quality of the holding company – for the first time in decades – rather than at whether Buffett or his successors are receiving high or low salaries.

.

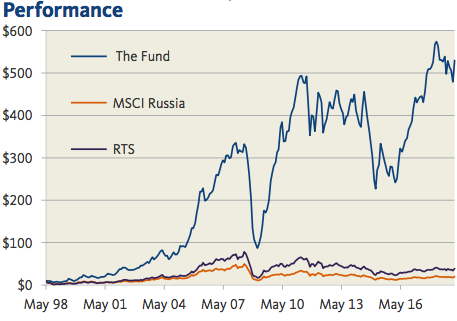

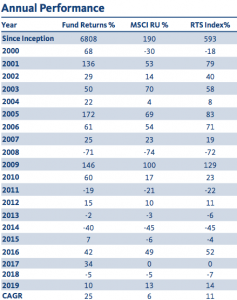

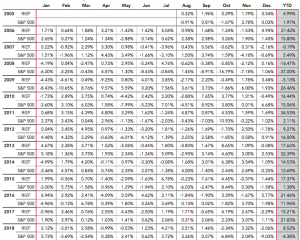

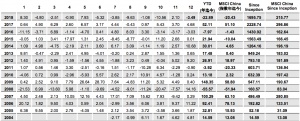

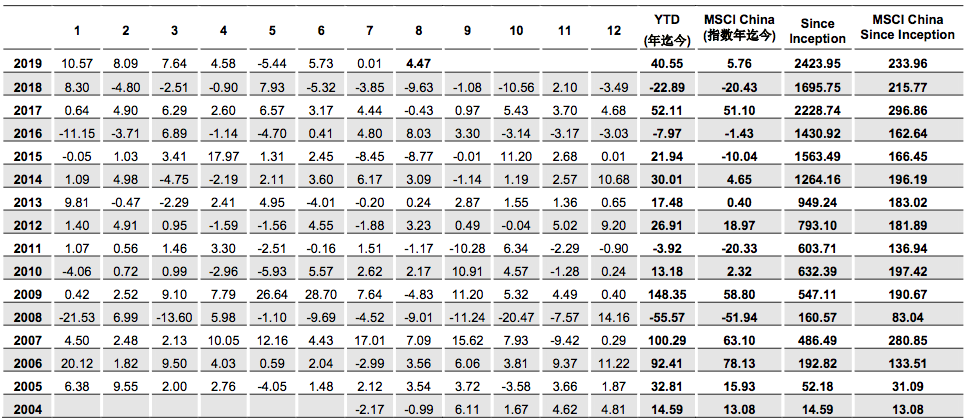

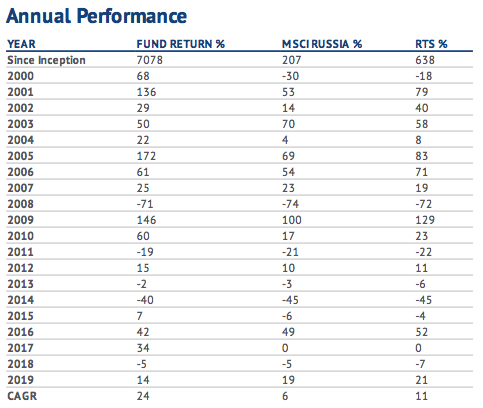

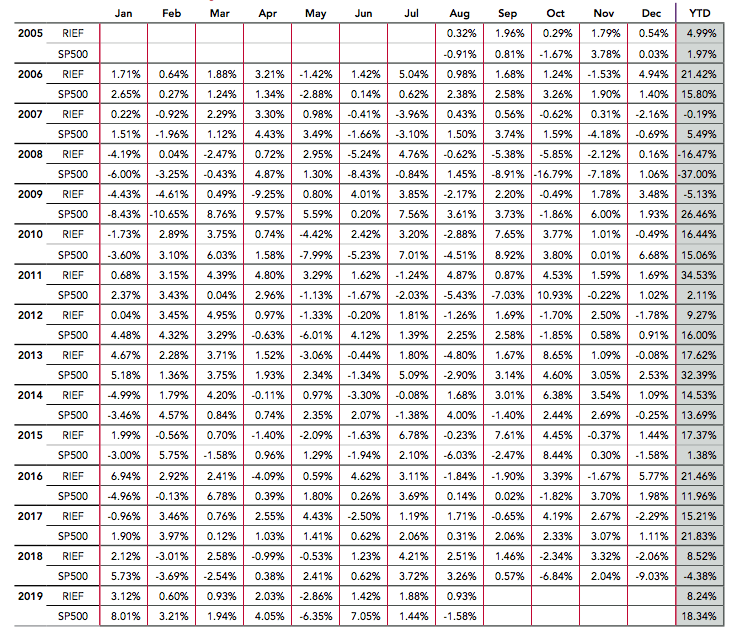

For the sceptics and others groupies When it comes to passive funds and ETFs, the study carried out by Panchekha should be the litmus test: The main reason for the mediocrity of active fund managers is their limited ability and/or lack of courage to concentrate their portfolios 100% on their «best ideas» or high-conviction companies. And this is, after all, an open secret that the world’s best value investors have always proclaimed: Why would you invest in your twentieth-best idea when you can invest in your first, second and third? The only answer is a lack of conviction, a fear of making a mistake, or corporate or regulatory obligations. High management fees are merely the final nail in the coffin for portfolios that are overly diversified and lack conviction and quality. How else could one explain the fact that active funds with the best NET returns on the planet (many of which are already closed to new investors) have fees significantly higher than the average of 85 basis points cited in the study? Let’s look at some examples of spectacular alphas in terms of NET returns in US dollars over the last few decades, the first against the MSCI China Index, the second against the Russian RTS Index and the third against the S&P 500 itself:

Finding funds that overcome the Active Manager’s Paradox is key for investors. But it is also crucial for the active fund industry that more and more managers overcome their fear of standing out from their competitors, that they overcome the self-imposed limitations in their prospectuses, and that they stop viewing concentration and volatility as risk factors. The real risk faced by most active managers who are content merely with not being the worst in their class is that they will eventually become extinct. And their extinction, whilst well-deserved, will increasingly favour the growth of index funds with portfolios that select companies in a far simpler and more superficial manner. Passive funds that behave as if a flat buyer were to decide to go to the solicitor simply by taking a few superficial ratios into account, without fully understanding the property’s condition, its energy efficiency, its building specifications or the neighbourhood, to give just a few examples. Obviously, it is better to buy a flat by taking a few superficial ratios into account than simply buying on a friend’s recommendation or at random, of course. But that is not the way in which our investments will perform adequately in the long term.

.

In short, the good news is that active fund managers as a whole create value. The bad news is that the vast majority of them lose it before it reaches their investors. Investors therefore have two options: To do sufficient research to be able to identify the fund managers with the greatest conviction and concentration in their portfolios; or simply to blame the mediocre performance of active fund managers on the fees paid, and throw themselves into the arms of even more diversified portfolios with less conviction but with low-cost fees. For those who choose to select the active funds they feel most strongly about for their portfolios, it is almost essential that expand their investment universe to include 100% of the world’s existing funds and don’t just settle for the 10% model sold in Spain.

.

Below are the details of the study’s methodology:

Research Design and Methodology

This analysis is based on a proprietary database of daily fund positions and portfolio weights compiled and maintained by Turing Technology Associates Inc. The specific funds included in the research dataset comprise 114 unique US equity mutual funds, from 57 fund families, representing $1.996 trillion in assets under management (AUM).

Fund Selection Process

The funds selected for use in the research were drawn from the set of mutual funds included within a series of investment portfolios known as Ensemble Active Management (EAM) Portfolios. Turing licences a series of proprietary technologies to clients to support their creation of such EAM Portfolios. Each EAM Portfolio is typically constructed from a set of 10 to 15 underlying mutual funds with a corresponding industry benchmark. As of early August 2019, Turing had 24 client-designed EAM Portfolios in live production.

All 114 funds used in the study were selected by Turing’s clients or prospective clients in connection with the design of an EAM portfolio. As Turing’s clients selected the underlying funds and the corresponding benchmark, the fund selection process remained independent of the researchers.

Each pair of a fund and a benchmark is the subject of the analysis. The benchmarks included the S&P 500, Russell 1000, Russell 2000, Russell 1000 Value and Russell 1000 Growth. The time periods used were either January 2014 to July 2019, or January 2016 to July 2019, depending on the data available.

Source of Daily Fund Positions

To access daily fund holdings, Turing applied its proprietary fund-replication technology known as the Hercules System. Hercules is a machine learning-based platform that processes a vast amount of publicly available data, with the core concepts behind the approach having been in use and under development for more than a decade. Hercules is not a regression-based approach. Daily estimated positions are generated by the Hercules System, with the out-of-sample portfolios rebalanced every 14 days.

For reference, the Hercules estimates of fund holdings and weights for the funds used in this study typically generated a tracking error of less than 1%, and a correlation with actual fund returns of more than 99.7%.

Isolating the Manager’s Conviction

The aim of this research was to analyse the impact of manager's conviction in security selection, and so we incorporated two key design elements into the study. Firstly, securities were categorised and evaluated on the basis of their portfolio weights relative to the benchmark. Rather than focusing on actual portfolio weights – which are heavily influenced by benchmark weights – the emphasis was placed on a manager’s decisions to overweight or underweight securities and the scale of those overweight or underweight positions. Second, we divided each fund into multiple, non-overlapping sub-portfolios determined by the level of manager conviction involved, and evaluated their performance separately. Each sub-portfolio was rebalanced every 14 days and treated as a distinct model portfolio. The three sub-portfolios analysed were:

High-Conviction Overweights: A sub-portfolio comprising the fund’s largest overweight positions in equities. The sub-portfolio was selected to cumulatively represent 80% of the portfolio’s aggregate overweight positions relative to the benchmark.

Underweights: A sub-portfolio comprising the fund’s largest underweight positions in shares. The sub-portfolio was selected to cumulatively represent 80% of the portfolio’s aggregate underweights relative to the benchmark.

Neutral Weights: A sub-portfolio comprising overweight securities that are not included in the Overweight sub-portfolio and underweight positions that are not included in the Underweight sub-portfolio.

All sub-portfolios reflect distinct choices made by a fund manager. The dynamic portfolio weights for each sub-portfolio are proportional to the original fund weights, normalised to 100%. Securities not included in the benchmark were excluded as they cannot be properly assessed against a benchmark. All performance data was calculated both gross of any fees and after factoring in a hypothetical 85 bps fee. Neither result reflected transaction costs.

The performance data presented consists of rolling one-year data (daily intervals), which was analysed to determine the percentage of rolling periods in which each sub-portfolio outperformed the corresponding benchmark (Success Rate), and the average excess (or negative) relative return.

A sub-portfolio comprising securities included in the benchmark but not held by the mutual fund (i.e., zero weights) was constructed and analysed. This fourth subgroup was not included in the research results because the only way to capture any potential alpha would be through a 100% short portfolio, which is not permitted in a traditional mutual fund. For reference, the Zero Weight portfolio underperformed the benchmark by 78 basis points, on average. Unfortunately, even a frictionless short portfolio of Zero Weight securities would not be able to generate enough returns to cover the fees of even a standard long-only mutual fund.

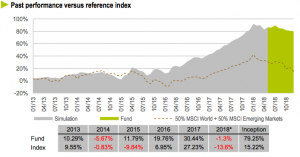

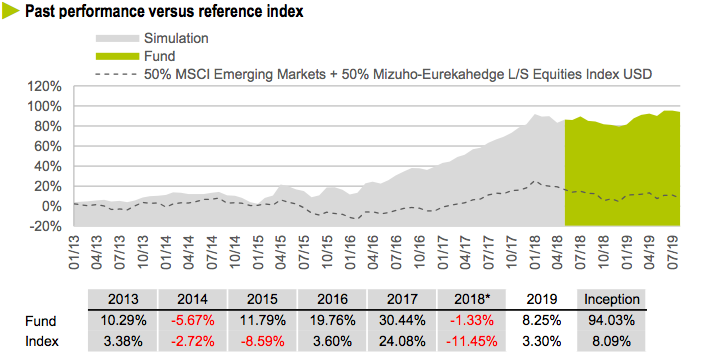

Index funds now account for more than 50% of the US equity fund market. And in Europe and the rest of the world, they are also gaining more and more followers. The main culprits for this are undoubtedly those pulling the strings of actively managed funds, whose mediocre net returns are driving disillusioned investors into the arms of passively managed funds. The reasoning of these disillusioned investors is simple: if we’re going to earn little, at least let’s pay low fees for it. But the fact that the majority of actively managed funds (between 8 and 9 out of 10) are mediocre and fail to outperform their respective indices does not mean that investors should settle for this and stop looking for that minority that outperforms them by a wide margin, as we explained in our article published on the COBAS website a couple of years ago. Here’s an example of the alpha in NET returns achieved by certain star fund managers, outperforming any index fund and with lower volatility:

Obviously, for investors who look beyond the products peddled by banks in Spain, there are gems like the one in the chart above, which outperform ETFs and other index funds by a mile. But what’s more, the comparisons are even more damning if we analyse in depth what is happening in the index fund and ETF industry. Let’s look at some of its shortcomings:

.

Just as a junk food manufacturer is a far cry from a good chef, those in charge of massive index funds such as those from BlackRock, Vanguard Group o State Street Corp They have nothing in common with good value fund managers. The former are only concerned with filling millions of cardboard boxes with something that looks like food, is cheap and appeals to shoppers. They couldn’t care less whether their customers end up with obesity, high blood pressure or any other health problems. All they care about is selling more and more volume every day at low cost. Similarly, index funds focus exclusively on pouring more and more millions into their portfolios, without caring in the slightest whether what they are buying are good or bad businesses, well or poorly managed, without caring about their fair value, let alone the long-term returns they will offer their shareholders. After all, why should they care, when more and more investors are turning away from expensive restaurants and resigning themselves to satisfying their hunger with cheap junk food?

What many people don’t realise is that these three giants of the index fund and ETF industry are responsible for keeping inefficient managers in the companies in which they invest. On reflection, the reasons may well be down to sheer carelessness, but if we scratch beneath the surface a little, hidden motives emerge, as we shall explain later. The fact is that its size is becoming such that their votes on the boards of directors are decisive to retain or replace management teams. The result is that not only do they invest indiscriminately in both good and bad companies (something inherent in passive or index-based management), but their votes also serve to keep poor managers in their posts. The million-dollar question is what interest these index fund owners could possibly have in retaining and paying out million-pound bonuses to inept managers. As always, the devil is in the detail.

.

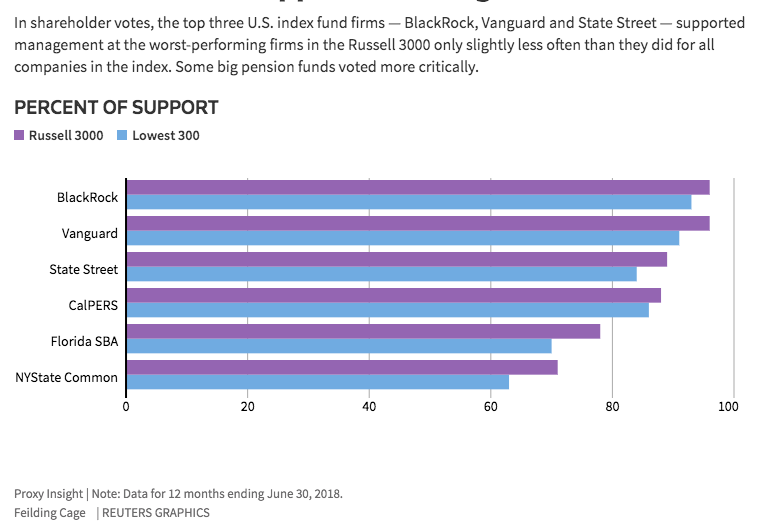

A study carried out by Reuters through the company Proxy Insight (lower graph) shows that in the 300 worst Among companies in the Russell 3000 index where proxy votes were cast, BlackRock voted in favour of management in 931 out of 1,000 cases, Vanguard in 911 out of 1,000, and State Street in 841 out of 1,000. The study concludes that these three giants supported the management of the worst-performing companies only slightly less than that of the other companies in the index, in other words, without caring in the slightest whether or not the management was harming the profits and performance of their companies.

The litmus test is that the percentage of support given by large pension funds to management teams at poorly performing companies is falling significantly. Of course, pension funds do care about returns for their future pensioners.

.

Some might argue that active fund managers do not usually go against the management in place either, but the reality is that active managers no longer invest in companies whose management is performing poorly or with whom they disagree. In fact, that is the essence of active management: identifying good businesses run by good managers, whilst also taking into account their price relative to their intrinsic value, in the case of value investing (Compare these returns with those of any passive fund). What’s more, even if a mediocre, lazy or ill-informed active manager were to invest in a poor-performing company and, through their proxy vote, support a poor management team, the influence they would have on the vote would be infinitely less significant than that of a massive index fund or ETF.

.

Consequently, there is a very real risk that mediocre companies with mediocre management will continue to exist indefinitely, due to the proxy votes cast by giant shareholders such as ETFs and index funds. Why would those passive funds care about the performance of the companies in their portfolios if their aim is not to outperform the index but simply to track it? Why would they confront their incompetent managers, replace them or deny them a huge bonus, if their sole incentive is to grow the fund rather than maximise returns for investors?

.

Another reason – this one more Machiavellian and immoral – for not going against the bad managers of large corporations is that it is those very same executives who are promoting these passive investment funds to their thousands upon thousands of employees. How else can one explain the fact that Vanguard, State Street and BlackRock all voted in favour of doubling the salary of the CEO of the energy company PG&E Corp, just after its shares plummeted following indications that the company was liable for the California wildfires? Or that they approved astronomical bonuses for executives at the cosmetics company Coty Inc – including half a million dollars to pay for their children’s school fees– after the company had been reeling from its reckless acquisition of Procter & Gamble’s beauty division. They have also unanimously vetoed an attempt by the other shareholders to separate the executive powers of the CEO and Chairman of the Board of General Electric Co, following a decade of poor results, etc., etc., etc… Even in the few cases in the Russell 3000 study where shareholders managed to veto executive bonuses, in 601 of those cases BlackRock attempted to award them bonuses through its vote.

.

Bear in mind that the largest holdings in index funds and ETFs, just like the indices they track, are in very large companies – that is, those with the highest number of employees worldwide. This is a vicious circle, as those executives are, after all, fund managers in return for fund owners voting in favour of their million-pound bonuses at board meetings. A win-win for them, but a lose-lose for investors in ETFs and index funds, and for the economy as a whole.

.

As it is the investors in these funds themselves who are most affected by the poor quality of the portfolios, it might seem that this circle is finally closing with a certain sense of justice. But we must not underestimate the damage being done to the global economy, because every day the markets are channelling more and more millions into mediocre companies and teams, with no one seeming to care about this inefficient allocation of capital. Furthermore, Western central banks continue with their free-for-all of cheap money, and with these trillion-dollar injections, alongside those from passive investment funds, We are undermining Darwin's theory of evolution. In other words, propping up zombie companies and executives with money created out of thin air and from investors more concerned with saving on fees than with investing their money wisely.

Ya lo dijo Mark Mobius, ex-chairman ejecutivo de Templeton y fundador de Mobius Capital Partners en un artículo del mes de Marzo: Hay que invertir en las bolsas de los aún llamados países emergentes. Y esta vez es el think-tank financiero Gavekal Research quien publica un informe titulado «Wealth transfer to Emerging Markets» que no tiene desperdicio. En él se dice que la era Keynesiana, es decir, de represión financiera, de facilidades cuantitativas (QE) o en definitiva la Era en la que los principales bancos centrales del mundo (FED, BCE, BoJ, etc) reducen el precio del dinero para reactivar el crecimiento anémico de las economías Occidentales del planeta, son chutes de crecimiento económico directamente en las venas de las economías Emergentes.

.

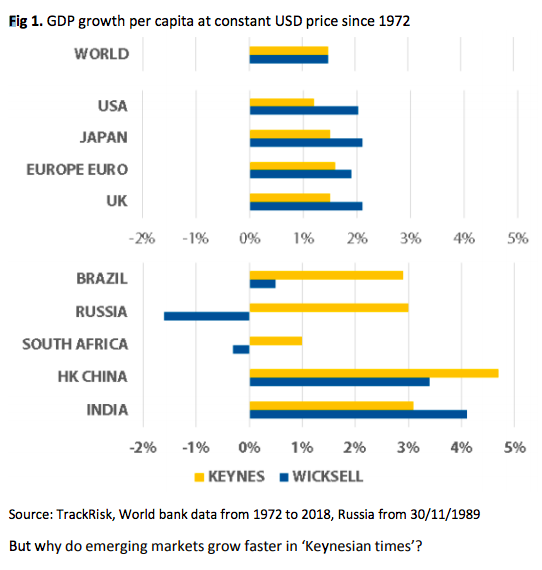

Cuando el rendimiento del Oro supera al de las principales divisas desarrolladas del planeta, el mundo entra en lo que llaman una Era Keynesiana. Si a ello le añadimos una acción coordinada de los bancos centrales de las economías desarrolladas, las políticas actuales de quantitative easing y tipos por los suelos son la eutanasia del rentista. La cuestión es, ¿quién se beneficia de esta muerte anunciada? Los mercados Emergentes, sin duda. Y comprobaremos esa clara transferencia de dinero desde los mercados desarrollados hacia los emergentes en este gráfico núm 1:

.

El eje inferior determina el crecimiento del PIB per capita (a precio de USD constante) desde el fin del patrón oro. Vemos como, tanto en épocas Keynesianas como en épocas Wicksellianas (por Knut Wicksell, que abogaba por unos tipos siguendo la corriente del crecimiento económico y no como herramienta correctora), el crecimiento es el mismo si tomamos el mundo en su conjunto. Pero fijaos que si distinguimos los países emergentes de los desarrollados, la cosa cambia radicalmente. Ahí el crecimiento de las economías emergentes se ve claramente favorecido por las épocas Keynesianas, justo al contrario de lo que sucede con los países desarrollados. Y también al contrario de lo que en principio se pretende con la política Keynesiana.

.

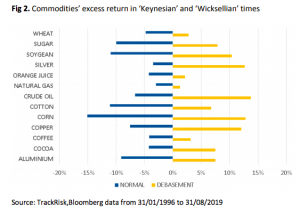

¿Por qué sucede esto, cuando intuitivamente parecería que las políticas monetarias laxas en divisas occidentales debieran favorecer el resurgir precisamente de las economías de los países desarrollados y no las de los emergentes? La primera razón es que los emergentes, muchos de ellos exportadores de materias primas, aumentan sus beneficios debido al aumento de precios de sus exportaciones. Y es que los activos reales (commodities) tienden a encarecerse cuando las divisas occidentales se deprecian respecto al resto de activos y divisas, cosa que ocurre en las Eras Keynesianas de bajos tipos.

.

Lo vemos muy claro en el gráfico núm. 2, donde, por el contrario, las épocas Wicksellianas son poco menos que la ruina de los exportadores de materias primas.

.

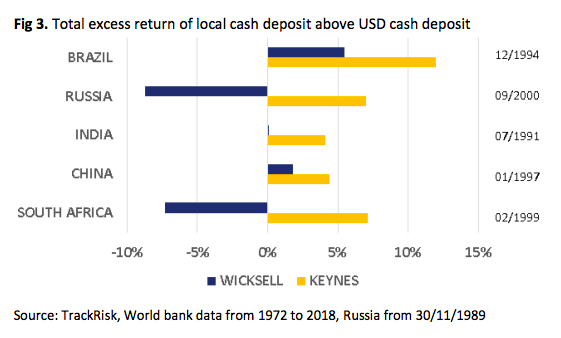

La segunda razón es que la deuda externa en USD de las empresas de países emergentes se abarata con los tipos bajos de las eras Keynesianas, lo cual genera beneficios adicionales a dichas empresas. Muy especialmente de aquellas que pertenecen a países con economías saneadas, poco endeudadas y muy productivas, donde sus divisas se mantienen estables o incluso se aprecian.

.

El gráfico núm. 3 mide el exceso que pagan los depósitos en moneda local respecto al USD. Dicho de otra manera, el coste de financiación que esas empresas ahorran respecto al coste que tendrían en divisa local durante las eras Keynesianas. Concretamente el exceso de coste de moneda local está entre el 4% y el 12% anual en los países BRICS. El ahorro es muy significativo para los mercados emergentes, tanto como lo es a la inversa para los desarrollados, que a su vez se beneficiaran de esa era Keynesiana al colocar su capital en economías emergentes asumiendo el riesgo divisa local. O sea, que el capital vuela hacia las economías Emergentes por diversas vías en estos tiempos de dinero gratis en Occidente. Entre otras razones porque es un dinero gratis que en el propio Occidente no hay donde colocarlo para que rinda lo más mínimo.

.

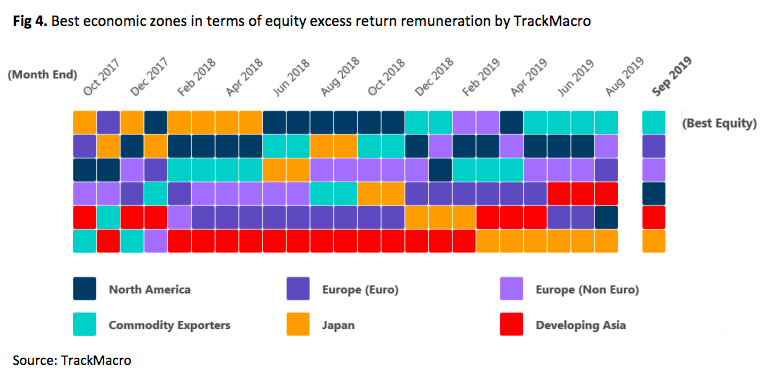

Además, TrackMacro confirma que a fecha de este mes de Septiembre 2019, el ranking de riesgos de poseer acciones de empresas en los diversas economías mundiales es el que podemos ver en el gráfico núm 4. Es decir, que los países exportadores de materias primas empiezan a hacer su Agosto desde el pasado Agosto, liderando el gráfico en los últimos 5 meses. Notad que en el grupo de «Developing Asia» se excluyen los asiáticos exportadores de materias primas, que se computan como «Commodity exporters». Por tanto, obviamente no todos los países emergentes gozan de estos flujos de dinero, del mismo modo que tampoco podemos considerar al mismo nivel la economía alemana y la griega, a pesar de que ambas sean «desarrolladas europeas».

.

Para acabar de reafirmar la conveniencia de invertir en ciertos Mercados Emergentes, TrackMacro también publica que de acuerdo a los indicadores macro fundamentales, los principales exportadores de materias primas como Rusia o Brasil disfrutan de una atractiva relación valor/riesgo. Si a todo ello añadimos las medidas en la buena dirección que están tomando distintos gobiernos emergentes, como por ejemplo la bajada de impuestos de sociedades en India, que les permite su bajo endeudamiento y una demografía productiva, la recomendación es aún más potente. Hay que invertir en economías de paises emergentes con la naturalidad, la confianza y las mejores perspectivas, como antaño tenían los mercados desarrollados. Pero eso sí, haciéndolo a través de los mejores gestores de fondos de inversión locales, que conocen perfectamente no solo las empresas de su país sino también sus intríngulis legislativos, contables, fiscales e incluso culturales.

Invertir con el viento a favor de los mercados Emergentes y evitar los vientos en contra (endeudamiento, demográfico, recesión, escasa productividad, etc.) va a ser la clave en los próximos años. Para los tenedores de las típicas carteras de acciones españolas ahí va un dato demoledor: Hoy el Ibex35 está al mismo nivel que en 1998, la bolsa alemana se ha multiplicado en ese mismo periodo x2,5, la de USA x2,7 y la de India x10,5. Pero lo peor para unos y lo mejor para otros está por llegar.

.

Conclusión: Las políticas Keynesianas en las principales economías desarrolladas deberían en teoría luchar contra las inercias deflacionarias, estimular el crecimiento local y fortalecer a las compañías occidentales ante los competidores de países emergentes. Pero el resultado de dicha política de facilidad cuantitativa y tipos bajo cero puede ser exactamente el contrario. La depreciación de las divisas occidentales conduce a una inyección de ingentes masas de dinero hacia las economías emergentes (que por otra parte son de por sí imanes para la inversión natural, aún sin medidas desesperadas en Occidente). Los inversores hoy en día sufren una situación asimétrica, donde sus divisas principales han dejado de ser valores refugio a causa de los tipos bajos. Esta Era de los Bancos Centrales favorece a priori el oro, los activos reales y las acciones de empresas emergentes, y lo hace en detrimento de las economías desarrolladas, la deuda soberana y las acciones de empresas occidentales.

.

Como bien decía Mark Mobius en el artículo citado, a finales de los años ochenta las economías emergentes tan sólo pesaban un 5% del Mercado global, pero ahora suponen más de un 40%, y subiendo rápidamente. En esos años los inversores no podían invertir en más de media docena de bolsas, y sin embargo ahora tenemos más de 70 mercados abiertos a la creciente inversión extranjera, perfectamente dotados de los medios técnicos más punteros y supervisados por reguladores de alto nivel profesional. Esto permite en la actualidad una enorme diversificación y seguridad, y nos marca el camino a seguir: Es el momento de invertir en determinadas economías emerging - or already emerging donde se está produciendo una tremenda recuperación y crecimiento económico.Además, la guerra comercial USA-China no es más que oportunidad de oro para hacerlo a precios moderados. Y quien siga vendiendo el miedo a invertir en los mercados emergentes está desinformado y obsoleto, o bien obedece órdenes de sus superiores para vender un pescado deflacionario, recesivo y que huele muy mal ya desde que los bancos centrales abrieron el grifo para mantener en pie economías y empresas zombies.

We’re going to summarise the study carried out by three renowned researchers and professors from Princeton and Columbia who are affiliated with the research team at the Federal Reserve Bank of New York, Mary Amiti, Stephen Redding and David Weinstein. In this study, they highlight the unsustainable costs that Trump’s tariff hikes would impose on the average American household if they were to be prolonged. For this reason, the likelihood of these tariffs bringing down the two most powerful economies on the planet is virtually nil. And they should be viewed as mutual posturing between a headless chicken and one with a head, which presents us with a very good opportunity to position ourselves in the stock markets (particularly Asian ones, as Mark Mobius also suggests in this article). Let’s look at the figures:

.

The current tariffs imposed on Chinese goods stand at 10%, and were recently increased to 25%, albeit with a 90-day moratorium to allow room for negotiation (an old tactic). To determine the impact of that additional 15% in tariffs, which Trump is threatening to impose if no agreement is reached before the end of that period, the calculation is based on the preliminary study on the impact of the current 10% taxes applied in 2018. It concludes that the impact amounts to an annual cost of $414 per family, comprising the extra expenditure that average families will have to incur to pay the additional taxes, and what they call loss of efficiency o deadweight. It is worth remembering here that a huge proportion of goods come from China, and that the rest contain Chinese components and/or are manufactured using Chinese processes; therefore, a temporary blockade by Xi Jinping would lead to an unimaginable global collapse. In short, the Chinese have the trade ‘nuclear button’ and the Americans do not. But let’s get back to the figures.

.

The extent of these costs depends on how customs tariffs affect the mark-ups importers add to their products, as well as on the demand for goods imported from China. Various studies, including the one mentioned, have concluded that the tariff increases imposed by the US imposed in 2018 have directly led to higher import prices, meaning that Chinese exporters did not reduce their prices at all to offset the increase in the final price for their US customers. The ratio of the increase in the final price to that of the customs duty was therefore practically 1 to 1. What that initial imposition of 10% on Chinese products did produce was, logically, a 43% drop in demand for Chinese imports, as the first logical move for importers is to postpone purchases and subsequently seek alternative suppliers and routes.

.

US buyers of Chinese goods now pay an additional 10% tariff on top of the usual base price; in other words, an item that used to cost a US consumer or importer $140 now costs $150. This adds $10 to their individual cost but not the US economy as a whole, as the government collects that additional $10 in the form of tax. The government, in turn, should – or could potentially – reinvest that same $10 and use it for the benefit of its citizens (including those who do not buy or import Chinese products).

It is worth noting here that demand naturally shifts between those who continue to buy more expensive Chinese products and those who switch to less expensive alternatives. Consequently, some importers or consumers will reorganise their trade arrangements or purchasing preferences, so that they buy substitute goods at a price lower than the $110 that Chinese products currently cost them. For example, a Vietnamese or Malaysian substitute item costing $105. In this case, the importer’s/buyer’s cost has increased by only $5, rather than the 10$ it would cost to continue buying the Chinese product. But beware, in this case The US economy as a whole also loses out, as there is no return on those $5 in the form of taxes that can be redistributed to the population. Furthermore, it has been amply demonstrated that importers will end up importing substitute products at a price only slightly below that of the Chinese product. In other words, imports will be at $108 or $109 and not at $101 or $105, as the comparison prior to the purchasing decision will be based on the current price of the Chinese product, i.e. $110. This principle will also hold true because suppliers will use the Chinese price of $110 as a benchmark to set their prices for the North American market. This increase in production chain costs, caused by the rise in import tariffs, is known as loss of efficiency or dead weight.

.

Economic theory tells us that this deadweight tends to rise more than proportionally as tariffs increase, as importers and consumers are forced to accept ever higher prices when taxes rise. Furthermore, very high customs tariffs lead to a fall in tax revenue, as buyers stop importing products from a country affected by those tariffs/sanctions and seek other suppliers/items from other countries, which are cheaper in terms of final price but less efficient. Let us consider that, up until that point, their suppliers and goods were Chinese because they had chosen that option as the most efficient of all the options that importers and consumers had considered. Therefore, these second and third options, beyond $100, which they are now forced to trade in, are by definition less efficient (worse value for money, worse logistics efficiency, poorer build quality, poorer after-sales service, worse marketing, worse packaging, poorer reliability, worse returns policy, repairs, etc.) than the Chinese products they had been buying at $100.

.

We can see how these two variables play out by comparing the estimated costs of the 2018 tariffs with the increase recently announced by Trump of an additional $200 billion on Chinese goods. As can be seen in the table below, in November 2018, with the 10% of current tariffs already in place, US importers were paying $3 billion a month in additional duties and suffering an additional $1.4 billion in efficiency losses or deadweight losses.

.

The total cost to US importers was therefore 1.44 billion per month. If we annualise these figures, we arrive at 52.8 billion, or 414 per household per year. Of this cost, $282 per household corresponds to money that goes into the US government’s coffers, and is therefore relatively recoverable by US society as a whole. However, efficiency losses or deadweight losses amount to $132 per household per year, and represent the net loss to the US economy beyond additional tax payments.

Based on these figures, we can calculate the cost of the additional tariff increase announced by Trump for the coming quarter, rising from the current 10% to 25%. The table shows how tax revenue for the government will fall from $282 to $211 per household per year, as the tax increase on Chinese products will be so costly that American consumers will begin to buy substitute goods that are not subject to these tariffs, such as products from Vietnam or other emerging countries, as we mentioned earlier. Let us remember that these second and third imported options are less efficient (more expensive than the cost of the Chinese product before the tariffs), and furthermore, the government no longer collects those taxes. Some of you may argue that the American consumer/importer can substitute Chinese products with other local American ones and thus avoid the loss of efficiency or deadweight. But the reality demonstrated by the studies The reality of the situation is that it is other emerging economies that are coming out on top, as products from developed countries such as the US have much higher production costs. And not only are their costs much higher, but they also have very limited production capacity (adapted to current demand and market share), which would take years and years to meet demand, even if they were to achieve the unachievable, namely the value-for-money efficiency of emerging countries. Furthermore, the deadweight loss from reduced efficiency increases whether consumers switch to more expensive foreign goods or to more expensive domestic ones.

.

As a result of this change, which importers and consumers are currently facing and will continue to face for the time being (until Trump blows his top or the lobbies force him to back down, as we will explain below), it is estimated that an increase in efficiency losses per household from 1Q132 to 1Q620 on an annual basis, bringing the total burden to be borne by the average American family up to $831 per year, if the threat of additional customs duties under Section 15% is carried out. Consequently, this increase in tariffs on Chinese imports will lead to enormous economic distortions in American society, as well as a substantial reduction in government revenue. But it is not only ordinary citizens who will be seriously affected. Just imagine the losses that giant American tech (and non-tech) companies could suffer as a result of the trade war and software boycotts targeting giants such as Huawei. Remember that Jinping has absolute control over a market of more than 1.3 billion potential consumers, and an enormous and growing influence over the rest of the Asian and African countries. All of this is already generating tit-for-tat retaliation that is causing, and will continue to cause, endless collateral damage which, no doubt, Trump and his team of ultra-nationalist Republicans have never calculated.

.

The million-dollar question is: what will major corporations such as Google, Amazon, Microsoft, Apple, etc. do in the face of Chinese reprisals which, although more discreet, will be just as brutal—if not more so—than those of the US administration that have been trumpeted by the Western media? Well, obviously, Faced with imminent losses running into tens of billions, they will prefer to spend billions on lobbying that will force Trump to reverse the situation. And billions, without a doubt, will enable the lobbies, in a perfectly legal manner, to exert pressure that is absolutely unbearable for the Trump administration. Let us not forget that in the US, Congress, with a qualified majority, can force the president and his government to do whatever it wants. Put another way, they can prohibit the Trump administration from imposing any kind of tariff or sanction on Chinese products with 290 out of 435 members of Congress. Currently, the Democratic majority in Congress stands at 54.1 per cent, so they would only need to «convince» 12.61 per cent of Republican members of Congress, some of whom will come round of their own accord as soon as the tariffs start to seriously hit their voters’ pockets.

.

Ultimately, the trade war between the US and China is so damaging – particularly to the US economy – that it has an expiry date. And Trump knows it. In this game of chicken, whoever has a Congress that keeps them in check, whoever depends on votes and corporate lobbies – in short, whoever lives in a democracy – knows they have lost the game. The winner can be none other than China, whose president implements plans spanning decades without caring about the opinion of voters (sic) or his corporations, which are at the service of the government and, of course, without any lobbying. Neither Trump nor anyone else in the US democracy will ever be able to politically or commercially subdue the Chinese dictatorship and its planned economy. Therefore, although Trump will need to bring his adventure to a dignified close, selling it to the Western media with headlines such as «we have secured the best trade deal in history, blah, blah…», the trade war cannot last more than a few quarters. The big US corporations will not allow it, via lobbies and a qualified majority in Congress. Even this «trade war» may effectively be defused whilst people are still publicly talking about it, due to Trump’s electoral political interests. But the reality can be no other than that of not causing significant or irreversible damage to the US corporate giants, since they have more than enough money to convince enough members of Congress, who in turn will force the US government to back down, even if this is not publicly acknowledged and the perception of a trade conflict continues to be fuelled. After all, Every US president has needed and provoked a war of some sort – one that is low-intensity in reality but generates a media frenzy, during their terms in office, for electoral gain. Trump has opted for a trade war, which will also attract intense media attention but is bound to be of low economic intensity.

.

For all these reasons, investors would do well to take advantage of the media skirmishes that trigger price falls to position themselves appropriately. In other words, they should go shopping for emerging companies whose figures will continue to grow beyond this fleeting, politically motivated trade war. For all the reasons set out in this article, The gloomier the outlook for the Asian markets becomes in the coming months, the closer their recovery will be. A golden opportunity to buy businesses, with the economic and demographic winds in their favour, at very attractive valuations. Remember that Volatility is a good investor’s friend and the enemy of bankers and other fearmongers, which strive to keep their customers trapped in schemes where the meagre returns are barely enough to cover the fees that are skimmed off along the way.

.

We simply need to be aware that the more heated the trade war appears in the media, the more we should invest in the best emerging-market-focused funds on the planet. Comparisons of the ‘fear funds’ peddled by the banks, with the best institutional fund managers on international stock markets are a pain. Volatility always goes hand in hand with double-digit annual returns over the medium and long term. And the best news is that There are funds of funds that provide access to these institutional funds, as we explained earlier in «Funds that make inaccessible funds accessible.»

.

The Chinese are well aware of the significance of the crisis Trump is creating with his trade war. It is no coincidence that there they define the word «crisis» as a synonym for «opportunity». And any self-respecting Western investor would do well to be less influenced by the Western media and more by the value criteria of the world’s best fund managers. This time is no different.

Most investors know little or nothing about the inner workings of what is considered the best investment fund in the world, due to its stratospheric performance over more than 30 years, the Medallion Fund. We have therefore decided to write this article unveiling the information we have gathered and the ins and outs we learned when we visited its management,Renaissance Technologies, a couple of years ago. Despite the length of the article, we believe it will be very interesting for readers to learn about the background, inner workings, curiosities and eccentricities of this great group of scientists, who have been recognised as the best managers in the world for their ability to beat the market for decades.

.

The first piece of bad news is that since 1993, Medallion has only managed money for its just over 300 employees and, of course, the owners of the management company. The good news is that Medallion's fund manager Renaissance, has 3 funds open to some institutional clients. But the second piece of bad news is that to invest in these institutional funds you have to have a minimum of $5 million, and also pass the due diligence that the fund manager performs on new investors. Yes, you read that correctly, to access Renaissance's institutional funds it is not enough to have a minimum investment of 5 million dollars, but the managers reserve their right of admission. But do not be discouraged, read on because At the end of the article we will explain how an investor with a minimum of 125,000 euros/dollars can access these funds.

.

According to Bloomberg, the size of the Medallion, which is the fund set aside for «...", has been reduced to the size of the Medallion.«friends & family».» The current owner's fund size is approximately $11 billion, which together with the other funds that Renaissance manages for an elite group of institutional clients, make up the $62 billion under management in total (figures as of January 2019).

.

We will now explain the origins and evolution of the world's best fund manager, and at the end of the article we will tell you about our personal visit to the Renaissance Technologies facilities, after passing both their due diligence and ours and thus becoming institutional clients of their funds.

.

The origin and evolution of Medallion and Renaissance performance:

On the north shore of the luxurious Long Island, just a couple of hours' drive from Manhattan, lies the area popularly known as the Renaissance Riviera. Not for nothing are the biggest billionaires in the area scientists working for Renaissance Technologies in neighbouring East Setauket. This elite group created in 1988 what has been the biggest money-making machine in the financial world, the Medallion Fund. A quantitative fund that has far exceeded the returns of other legendary managers such as Ray Dalio or George Soros. And what is even more spectacular is that it has done so in less time and from a smaller size.

.

This fund almost never loses money. Its worst 5-year performance has been -0.5%. According to Andrew Lo, professor of finance at MIT and chairman of AlphaSimplex, another quantitative fund manager, «Renaissance is the financial and commercial version of the Manhattan Project«. Andrew Lo praises Jim Simons, the mathematician who founded Renaissance in 1982, for bringing so many scientists and intelligence together in a single enterprise. «They are the pinnacle of quantitative investing. No one is even close to their level.». Very few companies generate so much fascination, buzz and speculation. Everyone has heard of Renaissance and the mythical Medallion but hardly anyone knows what goes on in there. Apart from Simons, a somewhat more public figure who retired in 2009 with a personal fortune estimated at more than $16 billion, little is known about the rest of its small group of founding scientists, whose wealth exceeds the GDP of several countries.

.

For those who are wondering whether such astronomical returns (see graph below) and such sustained returns over time are really possible, it is worth commenting here on the words of Simons, in his lecture last week at the Massachusetts Institute of Technology (MIT), when he was asked for the umpteenth time in his career whether he had ever been compared to the fraudster Madoff: «Of course, with our results and after what happened with Madoff, shortly after that the SEC (US regulator) looked at us and investigated us thoroughly. Of course they didn't find anything.». But this team of scientists who have been beating the markets for more than 30 years, with a fund closed exclusively to them, and 3 others with entry barriers of USD 5 million, really care little about the sceptics.

.

Renaissance is unique among hedge funds, institutional funds and closed-end funds. Its partners and managers are as cool as they are eccentric. Of the more than 300 employees, 90 are doctors (Ph.D) in disciplines such as mathematics and physics. Peter Brown, who co-heads the firm, used to sleep on a folding bed in his office. His counterpart, Robert Mercer, rarely speaks. And the identical twins, Stephen and Vincent Della Pietra, PhDs specialising in string theory, often argue loudly with each other. The rest of the staff can't be called typical office workers either. There is too much talent for vulgarity.

.

For the outsiders, the mystery is how Medallion has been able to win so close to the top of the table. an annual 80% before commissions, The fund, by the way, takes almost half of the return, although in reality almost all of it stays at home as it is a fund exclusively for members and employees. And the most surprising thing is that despite three decades of experience, they have not been able to copy them enough to come close to their results. The reasons are to be found in the power of its computational capacity, because the computers in their bunker basements are among the most advanced on the planet. Their talented employees have more and better data in which to find patterns and models that can be exploited. And they also fine-tune the costs of their transactions, of which there are many, while taking into account the consequences that their own trading generates in the markets.

.

But it should not be forgotten that the origins of most of its founders come from IBM back in the 1980s. There they used statistical analysis for the first linguistic challenges faced by mathematicians and computer scientists. Jim Simons, mathematical genius, professor at MIT and Harvard, winner of the Oswald Veblen Prize in Geometry and co-creator of the Chern-Simons Theory, was also a code breaker for the Institute for Defence Analyses (IDA).IDA) of the USA. (the current location of the Renaissance headquarters may not be coincidental, given that East Setauket was the area known as Culper Spy Ring, The birthplace of espionage, which enabled Goerge Washington to confront British troops with prior knowledge of their secret plans at the end of the 18th century). The aim of quantitative analysis is similar: to build models that find hidden signals in the «noise» of the markets.. Often they are just whispers, but some are able to predict how the price of a share, a bond or a barrel of oil will make a profitable move, however imperceptible it may be. The problem is complex. Prices depend on fundamentals and flows and the often irrational behaviour of the actors who are buying and selling. Despite (or because of) the fact that Simons lost his job at IDA after publicly denouncing the Vietnam War in a New York Times article, the cryptographic connections he researched helped him create Renaissance, and a few years later Medallion. On his way out, he sought out and surrounded himself with cryptographers and mathematicians such as Elwyn Berlekamp and Leonard Baum, former colleagues at IDA, Stony Brook and professors Henry Laufer and James Ax, for his initial project: Statistical price prediction.

.

The beginnings were bittersweet, and trend following and conversion to the mean caused them problems. Gradually they built models and more models. The initial results were mixed: +8.8% in 1988 and -4.1% in 1989. But in 1990, after explicitly focusing on short-term trading, Medallion achieved a profit of +56% net of commissions. The scientists went on to develop an internal programming language for their models. Today, Medallion uses dozens of «strategies» that run together as one. The computer code they use includes several million lines of code, which is soon to be said. Several teams are responsible for specific areas of research, but in practice everyone can work on everything. Every week there is a meeting where new ideas are tested and discussed to extreme limits by almost a hundred PhDs and other gifted minds.

.

In the early 1990s, spectacular yields became the norm at Renaissance: 39.4%; 34%; 39.1%. And customers began to flock to Medallion. The fund manager never bothered with marketing, in fact today its website still looks like a relic from 20 years ago. In 1993 Renaissance stopped accepting new customers. Fees were multiplied from 5% management + 20% success fee to 5% + 44%. Brutal, but even so, their net returns still stood out far above the rest. Not only that, but also In 2005, they had already expelled from the fund all former investors who were neither partners nor employees, leaving Medallion exclusively for them, and creating for the outsiders the first of the 3 institutional funds of which we will give details later: RIEF, RIDA and RIDGE.

.

Scientific background applied to markets:

The success encouraged Simons to hire more and more brilliant scientists. The next batch of gifted people to join the Renaissance family was a team of mathematicians from IBM's research centre in Yorktown Heights, NY, who were struggling at the time to get machines to recognise, emit and translate human speech. Let's just say that the parents of Siri, Alexa and Google Translate.At first mathematicians tried to rely on linguists to codify grammar, but they soon realised that the problems they faced were much better solved by mathematical probabilities than by language experts.. Mercer for example disappeared for months to type conjugations of French verbs into a computer. Processing his data allowed him to write an algorithm that found the most plausible translation for each sentence: «Le chien est battu par Jean» translated as «John does beat the dog», which was a dramatic improvement on the literal translation that systems without such algorithms were running up against. With every linguist they fired and mathematician they signed up, the system took a step forward. A similar thing happened with speech recognition: «Given an auditory signal x, the speaker probably said y«. «Recognition and translation are the intersection between mathematics and programming,» said Ernie Chan, who worked in the 1990s in IBM's research department and today manages QTS Capital Management.

.

Mercer and Brown then made a bold proposition to IBM: «Let us build a computer model to manage a part of your pension fund».». At the time IBM was managing a $28 billion fund for its employees. IBM rejected the proposal, thinking what would language programmers know about the investment world? But Mercer and Brown were already determined to apply their knowledge to making money in the financial markets. IBM was also at a low ebb, and it was easy for Simon, Mercer and Brown to recruit talent at the time. Renaissance was created by mathematicians who learned to program, not the other way around. They learned how to build large systems where many people were working at the same time. That was another competitive advantage of Renaissance.

.

Talented additions came and went, the Della Pietra twins (String Theory), Lalit Bahlt (responsible for human speech recognition algorithms), Mukund Padmanabhan (digital signal processing specialist). Almost all of them had worked together at IBM. They soon realised that tackling the market was much more demanding than the advances required at IBM. Either your algorithm was better than the rest - which were starting to flood the markets - and you made money, or it was worse and you went broke. High pressure was tremendously productive. Renaissance spent a lot of resources collecting, sorting and cleaning data, and making it accessible to its researchers. «If you have an idea, you want to test it quickly. And if you have to get the data you want to use right first, it slows the process down enormously,» said Patterson, another code breaker who worked for British intelligence and was part of Renaissance until 2001. But intellectual challenges are not the only incentives for this group of data-hungry brains. They also enjoy something more intangible: The feeling of a family of top-level scientists and the complicity and satisfaction that this brings them. Simons was like the benevolent father figure who added emotional intelligence to a group as diverse as they were geeky.

.

When the IBM scientists joined Renaissance, Medallion was already earning more than 30% net of commissions. And almost a third of that came from futures trading. In those early days, the inefficiencies of the market were more visible and exploitable than they are today. For example, one of their scientists noticed that there was a 15-minute gap between the close of options and futures, which allowed them to create a specific system to exploit that for a time. The market was full of aberrations, and the scientists investigated each one to death. The sum of all of them generated very large amounts of money for them. In the beginning it was millions, but after a few years it was in the billions. But as the financial system became more sophisticated with the proliferation of other quantitative funds, inefficiencies became scarce.

.

When Mercer and Brown came to Renaissance, they started working separately, but soon realised that they were more powerful working together. They fed off each other: Brown was the optimist and Mercer the sceptic. «Peter is very creative with a lot of ideas, and Bob says, I think we need to go deeper on this one,» Petterson said. They took over the group working on listed stocks, which were losing money. It took no less than 4 years to make the system work.. But Jim Simons was very patient. The investment paid off, and even Today, listed equity managers, through their derivatives and leverage (let's not forget that inefficiencies today are much more subtle) still generate the lion's share of Medallion's profit.

.

Simons explained in an interview in Institutional Investor back in 2000 that a winning [quantitative] system must be highly layered. «With every new idea you have to determine: Is it really new or is it somehow implicit in something we've already done? Once that's determined, the team has to figure out how much it should weigh in the mix.» He explained that signals can cool off at any given moment, but that vigilance must be maintained because they can emerge again at any time, or even withdrawing that vigilance can have an impact on the performance of the whole. The trade can be in any asset class and last for fractions of seconds or many months. In a lecture Brown gave in 2013 he explained an example that they shared with outside investors at the time, and was therefore public: By studying the weather in financial centres around the globe they found that local markets have a subtle tendency to rise more on sunny days than on cloudy ones. «It turned out that if it is cloudy in Paris, the French stock market is less likely to rise that day than if the sun shines during the opening hours of its market».» he said. It was not a big money maker, as that only happened slightly above the 50% of the time. But with the right tools and system in place, they are exploitable signals, along with many others. Brown continued: «The point is that there can no longer be obvious and powerful signals, because they would have been exploited by others as soon as they were incipient. What we do is look for huge amounts of signals, and for that we have 90 PhDs in mathematics and physics, who just have to sit there every day to distinguish them from the noise of the markets. We have over 10,000 processors (year 2013) down there who are constantly gutting very diverse data in search of those signals». Nowadays the methods of profiting from the market are as secret as they are difficult to imagine. A couple of years ago information was leaked that they were planning to use GPS (atomic) clocks to synchronise buy and sell orders in different markets, through nearby servers that manage to take massive positions without their purchases altering the market price and before even the HFT (High Frequency Trading) funds have time to react. We cannot even imagine what they will (or do) with quantum computers.

.

In addition to language specialists, Astrophysicists have been especially successful throughout history in deciphering systems. Such scientists shine above the rest when it comes to finding patterns in a sea of data. noisy.String theorists have also been particularly successful in filtering data. And the Della Pietra brothers, who along with others of their team at IBM were involved in the listed equity area at Renaissance, were among the first to shine in their field. These identical twins, now 58 years old, have never been apart from each other. Both attended an advanced honours programme at Columbia at the age of 16, graduated from Princeton with a degree in physics and received their PhDs from Harvard in 1986. They always sat next to each other, recalls his former professor of abstract algebra at Princeton. «Their conversations were full of argumentation. They were passionate mathematical discussions, and they were always correcting their professors». The fact that they are identical twins seems to take them to another dimension. «They are almost telepathic,» says Ernie Chan. At Renaissance, the Della Pietra's have always had adjoining offices with a large window for constant communication. «They are very creative and competitive with each other,» adds Patterson, to whom they reported directly for a few years.

.

The IBM team focused on constantly improving system efficiency and performance. As the Renaissance models were essentially short term, focused on fine-tuning transaction costs and how their own movements affected markets, both very difficult problems to solve, according to other fund managers. quants. They also ensured that trades and profits were in line with the system, since a bad price or any other crack could spoil the whole outcome of that particular operation.

.

Medallion reserved exclusively for members and employees:

The amount of money invested by an employee in Medallion depends on his or her overall contribution to the company. And collaboration with the environment is seen as key to having a bigger slice of the pie. Employees are allowed to buy a limited number of shares in the fund. In addition, a quarter of their salary is invested directly in the fund for at least 4 years. They all pay, of course, the tremendous 5% mgmt fee + 44% performance fee. Simons made it clear from the start that the size of the fund matters, and that too much money hurts performance. Renaissance currently limits the size of Medallion to 10-12 billion, which is double what it was a decade ago. It is therefore not uncommon for partners and employees to disinvest large sums of money to maintain a manageable fund size. Profits are also usually distributed on a semi-annual basis.

.

Thanks to Medallion, Simons, who still owns the company's 50%, amasses a fortune of 16 billion, according to the Bloomberg Billionaires Index. The other Renaissance heavyweights such as Laufer, Mercer and Brown have unquantified fortunes publicly, but have probably amassed many hundreds of millions each. But in a way, money, like the family atmosphere among the partners, keeps them together, with the exception of a few scientists who, already wealthy, have preferred to devote their intellect entirely to research or philanthropy. In general, few employees and partners leave Renaissance over the years. Why should they?The intellectual challenges are as attractive as they are constant, the colleagues are top-notch and the salaries are astronomical.. As all the employees have become wealthy, their lifestyles have changed. Trains to Manhattan have given way to private helicopters. Scientists have traded in their Hondas for Porsches, and expensive hobbies have become the norm. Simons' cousin Robert Lourie, who heads the futures research team, built stables and a riding arena for his daughter. State-of-the-art yachts are also the order of the day, and spending on company trips for team building activities is unmentionable. Simons, a heavy smoker, even took out a fire insurance policy with his favourite restaurant to allow him to continue smoking his beloved Merit after dinner. You will understand better now why the coast where the management company is located is known as the Renaissance Riviera.

.

However, the money has, of course, also brought them some displeasure. In 2001 they hired a Russian scientist, Alexander Belopolsky. Patterson was reluctant to hire him because Belopolsky had previously worked on Wall Street, where he had jumped from one job to another. His fears were well-founded. In 2003 Alexander and another Russian, Pavel Volfbeyn, announced that they were leaving to work at another hedge fund, Millennium Partners, where they would be working on a new project. had negotiated multi-million dollar bonuses in exchange for trying to copy Renaissance's know-how.. Of course, both the Russian scientists and Millennium were sued in court by Renaissance, and the matter was subsequently settled by a financial settlement of which no details are known.

.

However, not all Russians were unhappy at the company. Around that time, another scientist named Alexey Kononenko, who came out of the former USSR and received his PhD from Penn State in 1997, was promoted and moved up the Renaissance organisational chart with a bang, raising some eyebrows among the more senior staff. Kononenko was seen having dinner at Simons' house, and that was a sure sign that the Russian had a gift that made him more special than the rest of the company's gifted brains. Time proved him right, and Medallion achieved returns in excess of 40% per annum net after that dinner.

.

Building on the crash of 2007 and 2008, what is the secret of Renaissance?

When competitors or former investors are asked how Renaissance can continue to achieve such impressive results, the answer is unanimous: They run and evolve more than the rest.. Even so, they have not been without their scares. According to sources close to the fund manager, in August 2007 the mortgage market crashed, wiping out many hedge funds along the way, which literally disappeared from the map, including the 30 billion giant managed by Goldman Sachs. The disasters of so many trapped investors and leveraged quantitative and non-quantitative hedge funds flooded the markets with sell orders, making the situation much worse. Medallion suffered a loss of almost a billion in a matter of days, almost 20% of its size at the time.. This, which had never happened before in the fund's almost 30-year history, gave the team of scientists food for thought. They even considered whether they should reduce risk to ensure the fund's survival by selling off some positions. Fortunately, the scientists put their hearts aside and focused on their brains, letting the systems do their job. In the last four months of the year, they not only recovered their losses but closed the year with a brutal profit of +85.9% net.But it doesn't stop there. In 2008, the year of the stock market crash, profits were even higher, close to 100% net. The Renaissance partners reaffirmed their principles: «Don't mess with the models». And they also learned a lesson: the damage that large third-party bankruptcies can cause to the market must also be calculated.

.

Quantitative managers often say that there is no system that is effective forever. The variables are infinite and the markets as changeable and diverse as the human race and its globalisation. So one wonders how much longer Renaissance will be able to deliver these superior returns. The reality is that almost a decade after Simons' official retirement, the money-making machine is still running, and the old ex-IBM team is still between 50 and 65 years old.

.

The visit of Cluster Family Office to the Renaissance facilities:

We will now tell you our impressions of the visit we made a couple of years ago to the Renaissance bunker in Long Island (images below from google maps). We will start by saying that, once they passed their due diligence to be accepted as institutional investors, we had to insist that we were allowed to visit their headquarters., The majority of those selected are only shown their Manhattan offices, which are more «than the Manhattan offices".«commercial»but also spectacular. About 40 people work in Manhattan on a regular basis, but the offices are large enough to house the more than 300 employees who work at renaissance. Why is that? Well, because in Manhattan they have a backup and servers equivalent to the equipment they use in the bunker, and from time to time they practice a drill as if it had been rendered inoperative, moving all personnel for a day or two to Manhattan., in order to ensure that they continue to work perfectly in the event of an emergency in the bunker. That's how geeky and rigorous they are.

Why do we call the Renaissance headquarters on Long Island a bunker, if it appears to be a building (or several), large, yes, but just like any other? Well, because in addition to the access control on the road and the fact that it is surrounded by a lush forest that naturally conceals the facilities, inside there are a multitude of access controls, depending on the degree of restriction desired for each part of the building. Some doors were crossed when our companions swiped a simple magnetic strip through the reader, but others, closer to the heart of the company, required additional codes and even their fingerprints.. In addition to its two-storey height and its whimsical shape, which is slightly reminiscent of the Pentagon building, the main block also has two underground levels which house, among other secrets, the computer room. They agreed to show us around for a few minutes. It was a huge, white-walled, perfectly cooled space with a double-height ceiling. In the centre of the room, half a dozen 2-metre-high columns were lined with processors lined up on either side, forming long corridors between each column. The length of each column was impressive - we estimated at a rough guess that they must be between 50 and 60 metres long., The processors, as they allowed us to walk down those aisles from one end to the other. Obviously the figure of more than 10,000 processors that Brown talked about in 2013 was no exaggeration. Inside that room was another smaller room, to which we did not have access, which must have contained other mainframe computers. Interestingly, all the cooling machinery was outside that large room, so that even the air-conditioning maintenance technicians didn't have to enter the computer room at all. We had never seen anything like this before, and probably very few private companies have such a computer arsenal. We immediately understood what other big names in quantitative management were talking about when they said that «...the new system is a new way of doing business.«No one is at Renaissance's level in terms of data processing and analysis, not even close.»

.

During the visit to the rest of their facilities we could see that indeed all the individual offices are identical in size and decoration, following the guidelines of the partners. We did not see a single closed office door, everyone works with their door open to facilitate interaction and the exchange of ideas., as Simons states in an interview. They explained some of their internal processes, such as the challenges that rapporteurs of new proposals to be incorporated into the system have to overcome. Any new idea must overcome a huge number of Ph.Ds (PhDs in physics, mathematics, etc.) trying to smash it mercilessly. Ythe proposal of the rapporteur(s) will only progress if it overcomes the criticism and convinces the eminent. The next step is to test the proposal with models for a period of time. If it continues to work, it is tested with operations and real money in small amounts for another period of time. And if finally all the results are positive and there is no affectation or interference with the rest of the systems, it is implemented. The process can take months or even years, It is not fully implemented until it is empirically well proven and tested. It was impressive to see the challenges, where these new proposals are debated to death. There was a large screen presiding over a huge oval table with about forty seats, and around it a second ring of chairs for a total audience of more than a hundred. Imagine that room full of Ph.Ds arguing vehemently and trying to find the cracks in any new proposal. Truly, nothing that does not certainly improve the existing system will make it through that first theoretical filter and subsequent practical implementations.

.