Unfortunately, ordinary investors are almost completely unaware of the world of institutional funds. We are referring to retail investors, of course, but also to those who have several million and are looked after by the most luxurious private banking departments in Spain. Both are condemned to invest in a universe of national and international funds that are authorised for marketing in Spain, which leaves out practically no less than 90% of existing funds worldwide, as we have already explained in articles such as «The Spanish fund of funds", "The Spanish fund of funds" and "The Spanish fund of funds".«Investment Funds: There are still classes«We recommend you to read it.

.

As we have explained on other occasions, the most economical and viable solution for small and medium-sized investors is to have a own Luxembourgish vehicle. But even so, it will be very difficult for investors who do not have several million euros at their disposal to play in the Champions League of funds: Institutional funds and hedge funds. How do they differ from other international funds? Well, they do not have classes suitable for smaller investors, which makes these funds a select club to which only well-informed investors with enough millions to exceed the minimum investment in these funds and to have a properly diversified portfolio have access.

.

The minimum investment in these funds ranges from USD 500,000 to USD 1, 5, 10 or even USD 25,000,000. Not to be confused with traditional funds that have, in addition to retail classes, institutional classes, as these would not be considered truly institutional, but rather retail funds with commission rebates for the volume contributed. Truly institutional funds are those that do NOT have accessible classes with amounts that are affordable for ordinary investors. Some of you may be wondering why a fund manager would want to skip a retail class, thus disregarding the inflow of money from small investors. The answer is very simple: they are usually successful funds that sooner or later will end up closing their doors, even to institutional clients, because they have already reached the limit of assets under management that allows the correct execution of their different investment strategies. These successful funds and hedge funds have no need at all for the «traffic» of small amounts in and out of their portfolios constantly, simply because they already make enough money with their large and loyal investors. The question that should be asked is the reverse, why does a fund need to create retail classes and accept inflows and outflows of small amounts, which consume time and resources and are a real administrative headache for the fund managers. Obviously the answer is that they would not earn enough from their institutional or large investors alone, which leads to the conclusion that they are not successful enough in meeting the return expectations of their investors.

.

.

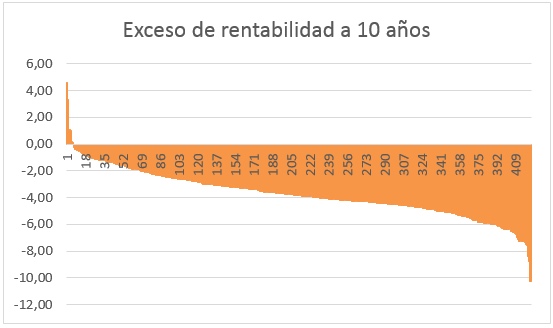

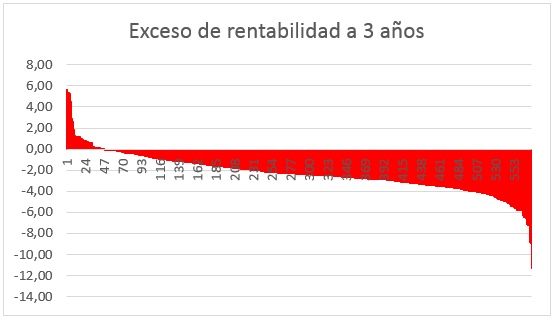

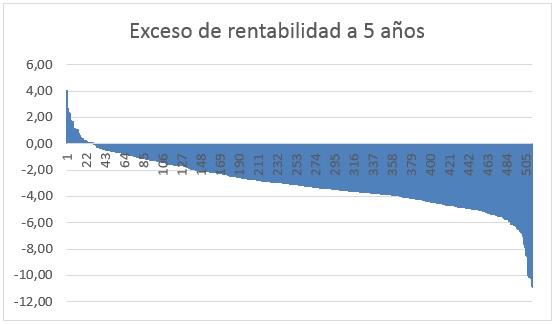

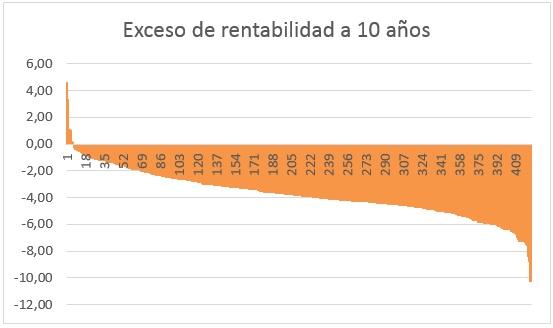

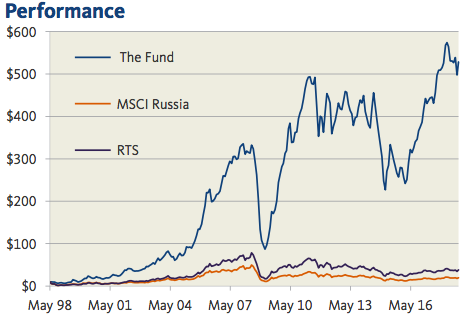

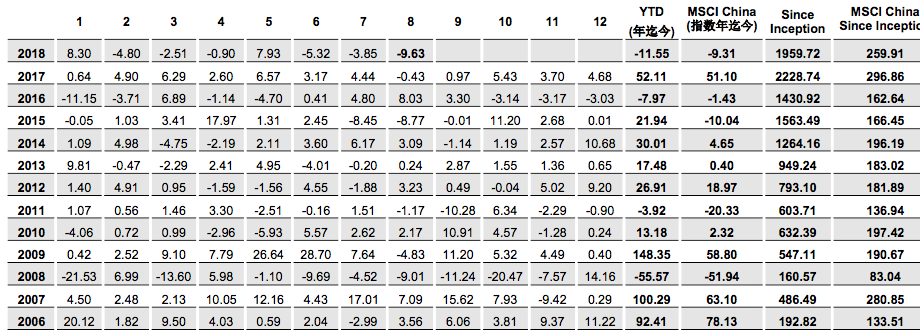

Fortunately, there are funds of funds that «slice and dice» these investment minimums required by institutional funds in exchange for a fee on top of the original fee. In other words, the small investor can invest in these funds of funds, which in turn invest in institutional funds with prohibitive minimums, with tickets as low as 125,000, which is the minimum regulatory amount to be considered a qualified or well-informed investor. Not in all, but in some cases the potential of the underlying funds is such that it is more than worth paying the double commission toll. Or is it not worth being able to invest from as little as 125,000 euros in such inaccessible funds as the heirs to the famous Medallion, Bridgewater or emerging funds with such spectacular alphas as the ones we see in the images published in this article?

Although we may not entirely agree with some of his convictions, there is no doubt that Daniel Lacalle is one of the people who knows the most about macroeconomics. Not only because of his PhD in Economics but especially because of his approach to the abuse of central banks that we have been suffering for more than a decade.

Although we may not entirely agree with some of his convictions, there is no doubt that Daniel Lacalle is one of the people who knows the most about macroeconomics. Not only because of his PhD in Economics but especially because of his approach to the abuse of central banks that we have been suffering for more than a decade.