The answer is NO, unless you have the extremely rare ability to choose one of the very few pension plans that outperform their benchmark index over a 10-year period. And even then, 10 years is a very short time when we consider that the investment horizon is usually very long when we’re talking about pensions for old age. But the secondary question we must ask ourselves is: What realistic chances do we have of investing in a pension plan that won’t condemn us to mediocrity? That is when the answer starts to become more uncomfortable if we want to be objective and honest. The fact is that the percentage of investment funds that do not outperform their respective benchmark indices is very low – let’s say between 1% and the 12%, depending on the source, the time frame and the sectors under consideration. But if we look at the performance of pension schemes relative to their benchmark indices, the proportion of funds that justify their fees is even lower.

.

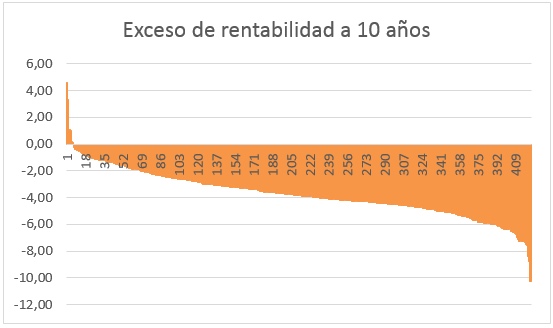

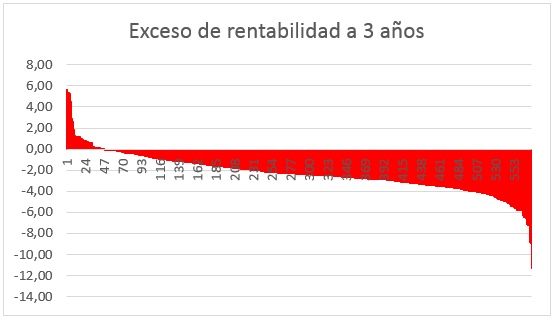

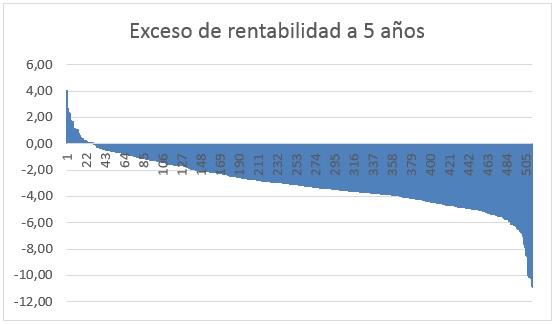

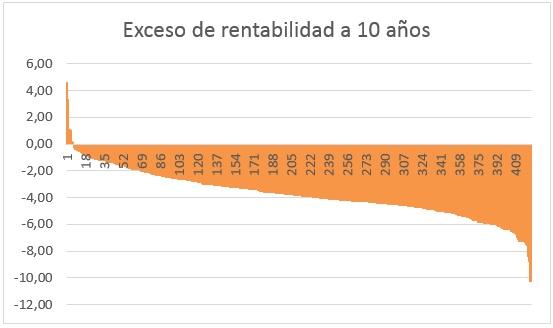

Let’s take a look at the latest charts report produced by Morningstar of pension schemes that outperform their respective three-, five- and ten-year benchmarks. Devastating:

Naturally, the longer the time horizon, the more the Monte Carlo effect—which we’ve already discussed—is minimised a decade ago. Just look: if we focus on a 10-year period – which is by no means unreasonable, especially when we’re talking about pension plans that we’re not supposed to touch until retirement age – the percentage of funds that outperform their benchmark is less than 11%! But the fact is that many people are still more than 20 or 30 years away from retirement, meaning the probability of outperforming the index through a pension plan is approaching zero at a dangerous and alarming rate.

.

What conclusion should we draw from this stark set of figures? Well, if it is already difficult to find a «normal» investment fund within the universe of funds available in Spain that outperforms its benchmark over the long term, finding a pension plan that manages to do so over a 10-year horizon is almost mission impossible for most of us. And how do banks and other salespeople manage to place so many billions into pension plans if they are so mediocre? Well, that’s what the free cookware sets, the smart TVs, the bonus cash deposited into accounts and… the tax breaks are for. Yes, those very tax breaks that many tout as the panacea for saving on tax whilst we prepare for retirement.

.

The fundamental problem is that those who argue that it is more tax-efficient to invest in a pension scheme than in a standard investment fund, despite the hefty tax bill when the moment of truth arrives, fail to take into account that the level of mediocrity in the management of pension plans is substantially higher than that of investment funds in general. Therefore, the main reason to steer clear of pension plans is NOT that we will pay tax on the income tomorrow on the savings we make today through contribution exemptions (we could debate whether or not such a tax break is worth it), but rather that The teams that manage pension schemes perform even worse than the average for standard investment funds sold in Spain.

.

For all these reasons, if an investor is able to find funds whose managers consistently outperform their benchmark over the long term (and such funds do exist; we refer you to this article we published in COBAS (a few months ago), you should never trade in that gem for a pension scheme that is poorly managed, no matter how many tax benefits or freebies its salespeople offer you. Tax breaks and cash or in-kind gifts, however tempting they may be, are nothing more than a short-term fix that condemns us to mediocre returns for the rest of our investment lives. Another issue is how to invest in funds that consistently outperform their indices and belong to that 90% universe of funds that are NOT investable from Spain. But we have already explained this repeatedly in articles such as «The advantages of investing from Luxembourg«.