Although most investors have never looked beyond the Solvency Standard, we must not forget that it is now 48 years since the US monetary authorities decided to abandon the Gold Standard – that is, the pegging of the dollar’s value to that of the precious metal. The practice of pegging money to a commodity that conferred intrinsic value upon it was widespread not only in ancient times but also throughout the 19th and 20th centuries, and so its abolition in the early 1970s caused considerable unease amongst US savers, who were accustomed to sleeping soundly in the knowledge that they could exchange their bank notes for a proportion of gold. The difficulties faced by issuers in maintaining the value backing for their currencies were in crescendo, with the result that the proportion of intrinsic value in the money issued gradually decreased, thereby allowing the money in circulation to increase beyond the limit originally set by material wealth (commodity) itself.

.

From that point onwards, intrinsic value began to be gradually and more or less subtly replaced by confidence (fiat) in the issuer. In fact, in some countries such as China, parts of what is now Canada, and other European countries and kingdoms, this path of no return towards fiat money began centuries ago. The new fiat money standard quickly took hold in the West during the 20th century, driven by the economic pressures resulting from the world wars, thereby placing the value of money entirely in the hands of (fiat) in the states, which were, unsurprisingly, delighted by the opportunities for political manipulation of money that this afforded them. With the end of the Bretton Woods Agreement in 1971, the US definitively buried the intrinsic value of its currency, and fiat money became the global standard – in case anyone still had any doubts. From then on, obviously, some states fared better than others – take, for example, the US versus Argentina, Venezuela or the ‘banana republics’ and their hyperinflation. But even for the top performers, the confidence of most savers in their respective governments has not been enough to prevent a loss of purchasing power over the years.

.

The fiat money system is here to stay, clearly, and we will never again see our money pegged to any real asset. It is simply too tempting for governments to have the power to create an infinite supply of electronic (formerly printed) money. But despite this endless possibility, which hyperinflationary ‘banana republics’ have been abusing, That Fiat standard was self-imposed, based on a criterion that has been key for almost 50 years: solvency. In this way, by linking the ability to create an infinite amount of money to the limits of solvency for repaying debts, Fiat money has, in fact, been the replacement of the gold standard with the solvency standard. In other words, trust in the state had a limit, which was none other than its actual ability to repay its debts and balance its books between public spending and tax revenue from the population without causing inflation to spiral out of control. For this reason, for decades there have been countries whose currencies depreciated against others due to mismanagement, forcing those states to cover their budgetary excesses with new money or public debt, which in turn fuelled inflation. This public debt had to be considered attractive enough for private capital from domestic and foreign investors to finance it. Investors who, consequently, demanded in return an interest rate commensurate with the risk that that state would be unable to pay its debts without printing banknotes, and that inflation would therefore erode its purchasing power. In other words, interest rates which in turn placed a price on the currency issued by each state, based on its ability to balance its books and its inflation rate, that is to say its Solvency.

The fiat money system is here to stay, clearly, and we will never again see our money pegged to any real asset. It is simply too tempting for governments to have the power to create an infinite supply of electronic (formerly printed) money. But despite this endless possibility, which hyperinflationary ‘banana republics’ have been abusing, That Fiat standard was self-imposed, based on a criterion that has been key for almost 50 years: solvency. In this way, by linking the ability to create an infinite amount of money to the limits of solvency for repaying debts, Fiat money has, in fact, been the replacement of the gold standard with the solvency standard. In other words, trust in the state had a limit, which was none other than its actual ability to repay its debts and balance its books between public spending and tax revenue from the population without causing inflation to spiral out of control. For this reason, for decades there have been countries whose currencies depreciated against others due to mismanagement, forcing those states to cover their budgetary excesses with new money or public debt, which in turn fuelled inflation. This public debt had to be considered attractive enough for private capital from domestic and foreign investors to finance it. Investors who, consequently, demanded in return an interest rate commensurate with the risk that that state would be unable to pay its debts without printing banknotes, and that inflation would therefore erode its purchasing power. In other words, interest rates which in turn placed a price on the currency issued by each state, based on its ability to balance its books and its inflation rate, that is to say its Solvency.

.

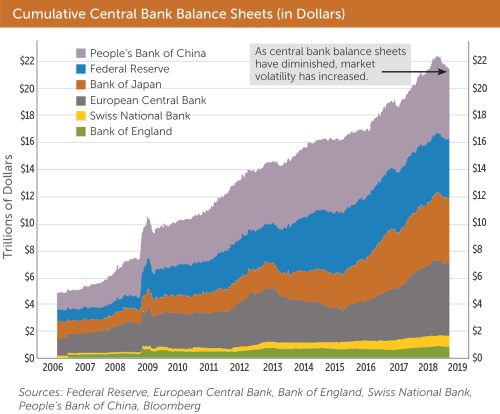

We therefore had a system whose insolvency was self-regulating, since anyone caught in an unstoppable spiral of debt at rising interest rates and galloping inflation would default within a few years, dragging their economy and that of their ill-advised fellow citizens into ruin. But as politicians have never known how to steer the economy, the abuse of debt – even in countries that kept their inflation under control – began to bubble up. Until the debt crisis of 2007 struck, followed by the crash of 2008. By then, excessive debt was so widespread and insolvency so high that the risk of default by insolvent parties was systemic, starting with the entire Western banking system. Solution: Draghi’s famous phrase, «whatever it takes«In other words, central banks will generate as much money as is needed to turn the insolvent into the solvent and thus save the system. Because with infinite liquidity, the insolvent party never goes bankrupt; they simply extend and roll over their debts to infinity and beyond, allowing creditors to avoid having to set aside provisions for bad debts beyond what their balance sheets can bear. It’s a bit like the ostrich that buries its head in the sand.

.

The new standard is therefore that of fiat money, but for the past decade it has also been infinite by decision of the world’s most powerful central banks. In other words, The money needed to keep banks, large systemic companies and the states themselves afloat is being created and will continue to be created, as is the case in the southern part of the eurozone, by adding zeros to its debt and with negative interest rates (we already discussed this 6 years ago in financial repression). Some of the obvious drawbacks are that we are allowing zombie companies – inefficient and up to their ears in debt – to survive, as they repay their maturing debts with new money created by central banks in exchange for their worthless IOUs. Another fatal drawback is that sub-zero interest rates not only keep insolvent public and private entities afloat but also provide even greater incentives for private borrowing. For all these reasons Solvency is no longer a ratio to be taken into account. It will also be chaotic that all these ultra-low-yield instruments are sweeping aside anyone who has made income their modus vivendi or modus operandi – that is to say, private rentiers, pension funds, insurance companies, sovereign wealth funds and other sources of capital seeking to avoid stock market volatility. To date, we have only A decade of zero interest rates, but the damage that quantitative easing will cause in the medium and long term is devastating for the sustainability of funded pension schemes (just as the ageing population we are also experiencing is for pay-as-you-go pension schemes).

The new standard is therefore that of fiat money, but for the past decade it has also been infinite by decision of the world’s most powerful central banks. In other words, The money needed to keep banks, large systemic companies and the states themselves afloat is being created and will continue to be created, as is the case in the southern part of the eurozone, by adding zeros to its debt and with negative interest rates (we already discussed this 6 years ago in financial repression). Some of the obvious drawbacks are that we are allowing zombie companies – inefficient and up to their ears in debt – to survive, as they repay their maturing debts with new money created by central banks in exchange for their worthless IOUs. Another fatal drawback is that sub-zero interest rates not only keep insolvent public and private entities afloat but also provide even greater incentives for private borrowing. For all these reasons Solvency is no longer a ratio to be taken into account. It will also be chaotic that all these ultra-low-yield instruments are sweeping aside anyone who has made income their modus vivendi or modus operandi – that is to say, private rentiers, pension funds, insurance companies, sovereign wealth funds and other sources of capital seeking to avoid stock market volatility. To date, we have only A decade of zero interest rates, but the damage that quantitative easing will cause in the medium and long term is devastating for the sustainability of funded pension schemes (just as the ageing population we are also experiencing is for pay-as-you-go pension schemes).

.

However, the most curious thing about the current situation is that it may be surprisingly sustainable, as it has advantages such as the fact that we can kick the can down the road when it comes to mass bankruptcies for decades – who knows, perhaps even for generations. We simply need to get used to the idea (and we’re already doing so) that sovereign debt, for example, far exceeds 100% or even 200% of GDP. After all, what does the debt-to-GDP ratio matter if solvency is a problem that central banks have left behind with their new «Infinite Money Standard»? Thus, we see how states keep themselves and their banks solvent by creating money without it entering significant circulation, since the vast majority of these flows do not leave the debt circuit perpetuated between central banks, private banks and state-owned, quasi-state-owned or systemic companies. In a word, we are living in the paradise of ‘too big to fail’. Under this new system of infinite liquidity, the effects of the dreaded ‘austericide’ – championed by the German hawks – can be mitigated, as it fosters inefficient and anaemic economic growth whilst keeping inflation at rock-bottom levels and also warding off the dreaded deflation. But the short-sighted benefits do not end there; in this vicious cycle, politicians can secure re-election without having to make bold decisions or think beyond one or two parliamentary terms – which is their usual intellectual horizon.

.

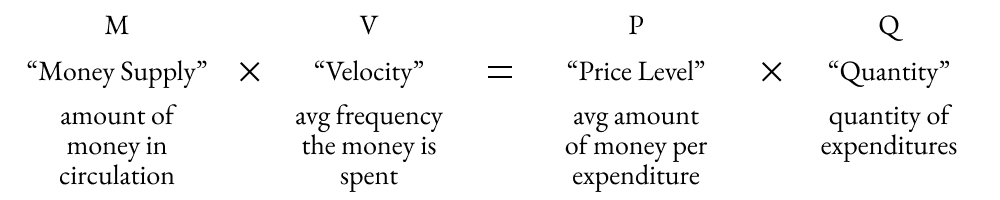

So what are the risks of this infinite liquidity? Well, as well as providing the perfect breeding ground for the inefficient allocation of money whose price is close to zero, hyperinflation would be another factor that could ultimately cause this new system to implode. But as we saw 10 years ago in «The illusion of wealth and the Quantitative Theory«An increase in the money supply without a corresponding increase in the velocity of circulation is not sufficient to drive up prices. And the tap controlling the speed at which money flows through the veins of the population – that is, the so-called real economy – is entirely controlled by central banks, governments and private banks.”.

We are therefore entering a profound era in which the Solvency Standard has become obsolete, and in which infinite liquidity will keep zombie companies, banks, states and governments afloat, whilst also giving them an air of normality to which we are already becoming scandalously accustomed. So let’s put the low volatility aside and the comfortable life of the rentiers of yesteryear, the natural selection of the insolvent and inefficient, and a reasonable cost of capital.

.

.

The million-dollar question is whether we can throw the savings of the most conservative investors into the arms of virtually zombie banking products, trusting that the era of infinite money is here to stay. The answer is that many have been doing so for a decade and it has worked out relatively well for them (although they have hardly kept pace with real inflation), given that no deposit, guaranteed product or fixed-income portfolio has gone bust under the leadership of Draghi, Yellen or Bernanke. But the fact that a political decision has been taken to keep insolvency afloat does not make those investments solvent. Therefore, barring a very few exceptions involving alternative income-generating assets – such as life settlements or certain segments of the US mortgage market, which exhibit moderate volatility but offer quarterly liquidity and selective access – the most conservative investors would do well to accept the volatility of the stock markets countries whose economies are still growing and will continue to grow for at least a decade. And to invest in those growing assets and markets, they must look for the best funds in the world, without the huge restrictions imposed by minimum investment amounts or marketing regulations in Spain.

.

In this era of infinite money, which is here to stay – as the famous soap opera used to say – one could say that without volatility, there is no paradise.