After the rally and subsequent fall in the price of cryptocurrencies in the last 2 or 3 months, at Cluster Family Office we have received several potential clients who have generated very considerable sudden fortunes thanks to holding and/or trading all kinds of tokens: Bitcoin (BTC), Bitcoin Cash (BCH), Litecoin (LTC), Ether (ETH), Ripple (XRP), Cardano (ADA), NEO, Dash and many others that most of us mortals did not even know about. And most of them started from a modest financial situation, so they are facing totally new situations for themselves and their families.

.

The needs faced by these new millionaires are delicate, since the way to declare these enormous realised and potential profits to the tax authorities is still confusing even for Montoro himself. The fact is that the scarce information generated by most foreign online platforms through which transactions are carried out, together with the large number of operations and cryptocurrency crosses included in each movement, make the figures that must be presented to the Treasury a maze of spreadsheets that are difficult to defend against the voracity of a future requirement or inspection. In addition, it should be borne in mind that the holding of currency accounts (not cryptocurrencies, for the moment...) exceeding 50,000 euros must be included in the famous form 720.

.

Thank goodness that the profile of most of the cryptocurrencies« nouveau riche come from the tech world, and our tax professionals get this profile of Clients to provide them with this puzzle of necessary information quite thoroughly and diligently. However, there are many crypto-millionaires out there who are being much more careless and chaotic when it comes to compiling their trading trail. And their carelessness will cause them to incur serious tax problems in the near future, i.e. less than 4 years, before the statute of limitations expires in the tax year where they concentrate a large part of the crypto »buck".

.

But it is not just taxation they face that is difficult to defend. The million-dollar question these new cryptocurrency millionaires must ask themselves is, obviously, what to do with their fortune and how it will inevitably change their lives. Most of them want to keep a portion of their tokens or cryptocurrencies invested in anticipation of new highs and thus higher profits, but they have already made sales worth millions with which they must make decisions they have never had to face before. Not only that, but they are beginning to experience the harassment that banks, real estate companies and other predators are subjecting them to as soon as they smell fresh blood.

.

Our recommendation is similar to that of any profile of sudden fortune (tech entrepreneur who sells his company, lucky prize winners, etc.). lottery or chance, athletes elite or artists, heirs, etc.), i.e. they should postpone hasty decisions and design and implement, together with professionals, a balanced and tax-efficient distribution of their wealth. To this end, we propose a final picture of what their personal fortune should look like in a couple of years' time. For their part, they express their preferences in terms of the goals or dreams that they will now be able to realise. And they will do so with the help of a team that, above all, we are there to prevent them from making mistakes that they would regret in the future, costing them money and displeasure. The world is full of examples of sudden fortunes that have shattered the lives and happiness of their protagonists - and their descendants. And the envy-stricken circles of these crypto-millionaires may be eager to see how they squander their fortunes, and thus not feel so bad about not having been able to participate in the technological boom.

.

Some of the new millionaires may wonder when is the right time to sell Bitcoins or whatever crypto. The question is unfortunately not an easy one to answer as it will depend on the degree of greed, the volume achieved and the previous and present family and asset situation. But a good starting point to find that answer would be to «set aside» and conveniently diversify enough money to ensure a comfortable life for their families for the rest of their lives through sound financial and real estate income. Thereafter, any substantial increase or loss of cryptocurrencies still held in their wallets or purses will be seen in a different light.

.

There is no fortune more ephemeral and problematic than sudden fortune without proper advice. And as an anonymous sage once said:

«We don't learn to be sons until we are parents. We don't learn to be parents until we are grandparents. It seems that we don't learn to live until life is gone... So, obviously, we don't learn to be wealthy until we have lost most of our money.»

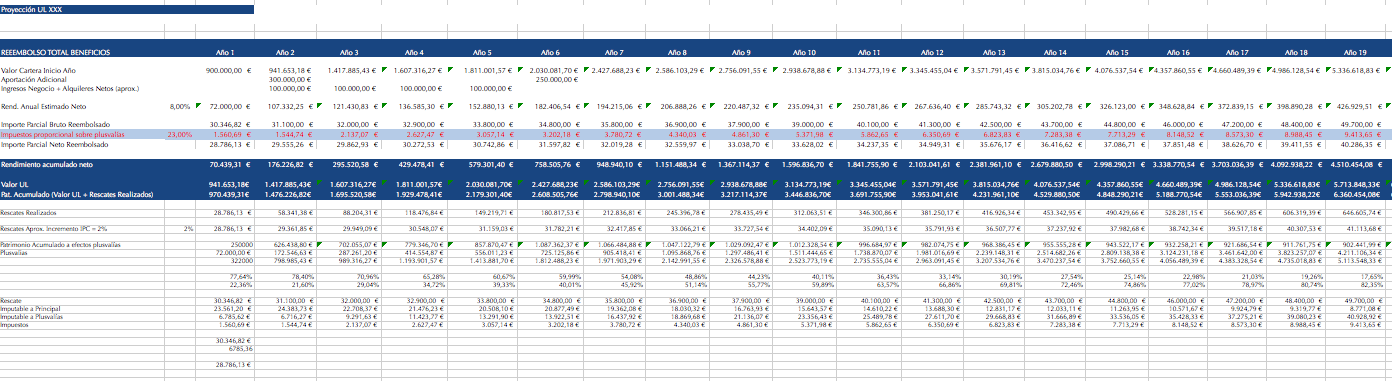

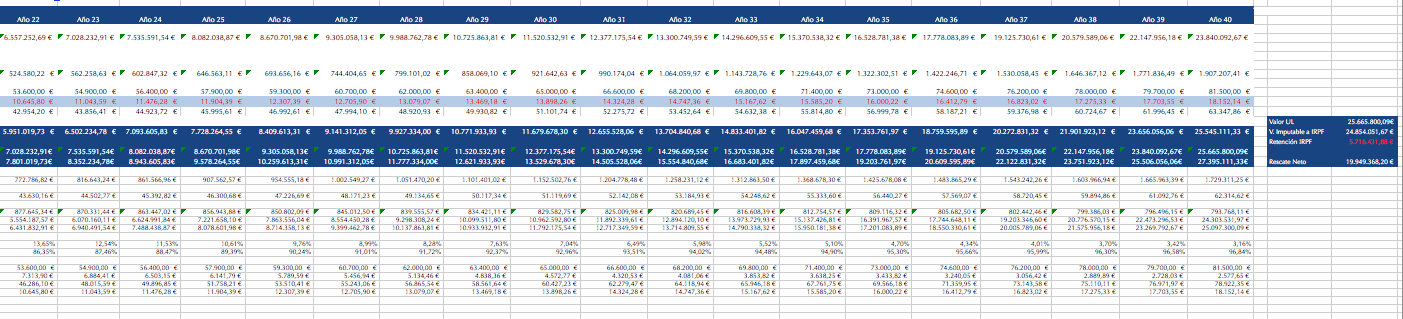

Luxembourg, as a good «EU friendly» financial centre, has various types of investment vehicles that adapt to the needs of each size and type of investor. But for the smaller investor, who is the most disadvantaged by the restricted range of funds to which he has access in Spain, there is a a personal and exclusive Luxembourg vehicle from which you can invest your portfolio with complete flexibility, from as little as 250,000 euros. Obviously not all retail investors have a minimum of 250,000 euros, but it is a huge step for the average investor to be able to put their investments on a par with those of any institutional investor with 10 or 20 million from as little as 1/4 million. And these vehicles not only allow access to any fund in the world, but also to any fund in the world. also allow for the deferral of capital gains generated within these vehicles indefinitely., The tax is only levied on the proportional part of the capital gain when it is decided to redeem part or all of the investment. In other words, once we have this minimum of 250,000 euros in our own investment vehicle, we will be able to buy and sell any fund, share or whatever we want, without paying tax on the capital gains until we need to withdraw all or part of our money. Taxation is exactly the same as when we buy any fund registered in Spain that is sold to us by the bank on the corner, but without the need to jump from one transferable fund to another within the limited list of funds registered with the CNMV, but with total and absolute freedom in the world universe of UCITS, non-UCITS, AIFMD, Private Equity, Real Estate Funds, shares and other financial products. This is why we chose a Luxembourg vehicle, totally «friendly» with the taxation and transparency of EU countries.

Luxembourg, as a good «EU friendly» financial centre, has various types of investment vehicles that adapt to the needs of each size and type of investor. But for the smaller investor, who is the most disadvantaged by the restricted range of funds to which he has access in Spain, there is a a personal and exclusive Luxembourg vehicle from which you can invest your portfolio with complete flexibility, from as little as 250,000 euros. Obviously not all retail investors have a minimum of 250,000 euros, but it is a huge step for the average investor to be able to put their investments on a par with those of any institutional investor with 10 or 20 million from as little as 1/4 million. And these vehicles not only allow access to any fund in the world, but also to any fund in the world. also allow for the deferral of capital gains generated within these vehicles indefinitely., The tax is only levied on the proportional part of the capital gain when it is decided to redeem part or all of the investment. In other words, once we have this minimum of 250,000 euros in our own investment vehicle, we will be able to buy and sell any fund, share or whatever we want, without paying tax on the capital gains until we need to withdraw all or part of our money. Taxation is exactly the same as when we buy any fund registered in Spain that is sold to us by the bank on the corner, but without the need to jump from one transferable fund to another within the limited list of funds registered with the CNMV, but with total and absolute freedom in the world universe of UCITS, non-UCITS, AIFMD, Private Equity, Real Estate Funds, shares and other financial products. This is why we chose a Luxembourg vehicle, totally «friendly» with the taxation and transparency of EU countries.