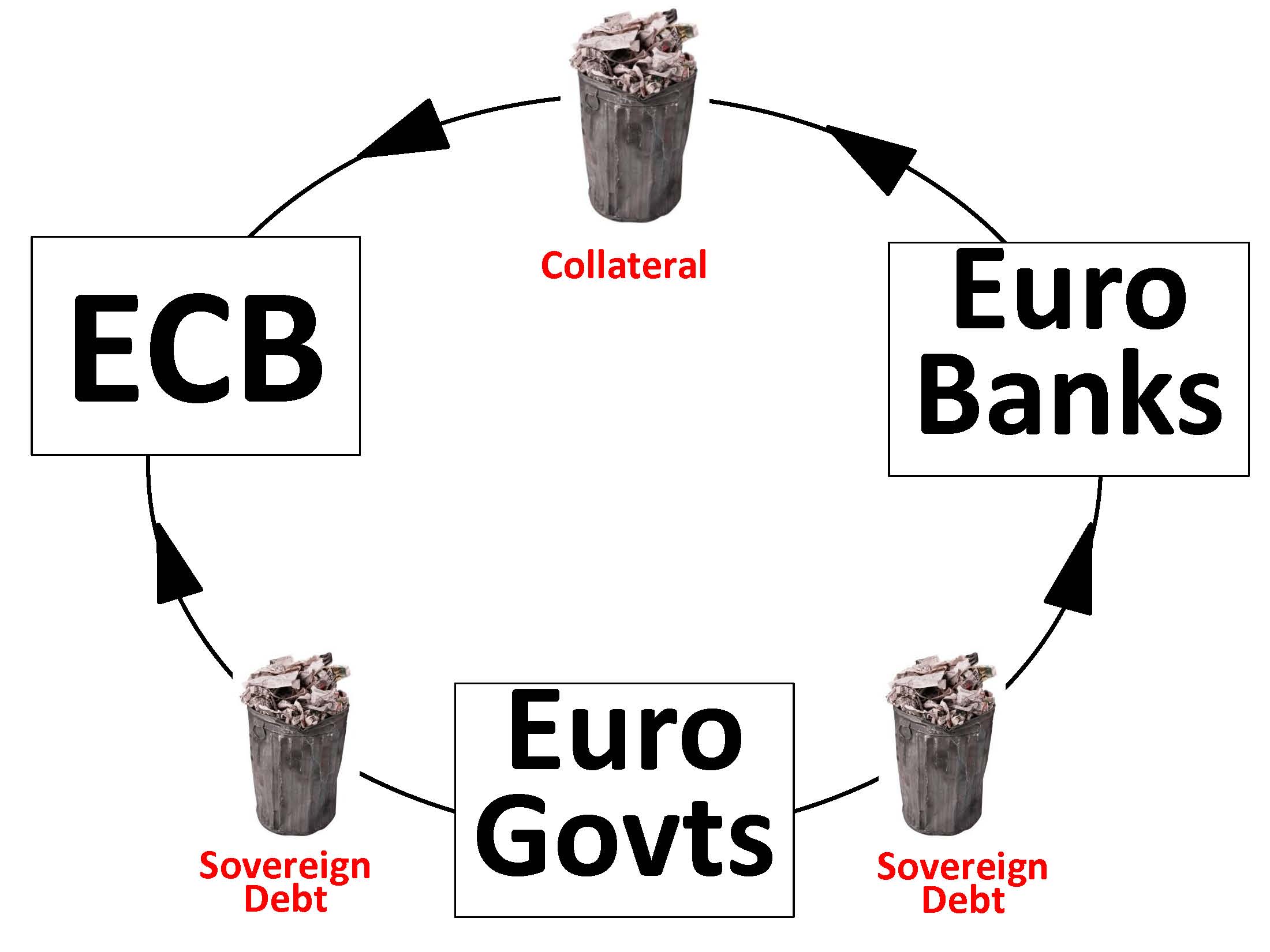

Generating income when rates can only go up, and doing so in an environment of recession or anaemic growth, is at best a pipe dream. The fact is that there comes a point at which trying to scrape a tenth of a yield by adding risk (and we are not talking about mere volatility but the dreaded insolvency) is not only reckless but also increasingly difficult to achieve. A few examples to illustrate this point: The Spanish 10-year sovereign bond, with government indebtedness of 100% of GDP and its persistent public deficit of -7%, offers an incredible yield of 1.96% per annum. Or the high yield corporate debt of companies in the developed world, as over-indebted as the countries, with yields that are less and less «high» and which will be mercilessly crushed by the rise in interest rates. And what can we say about Greece itself, the paradigm of insolvency and the impossible rescue by states also in need of a bailout, offering a ridiculous 7.79% for 10 years. In other words, the investor receives 7.79 per annum in exchange for Greece being able to pay back its euros intact in 2024... Insane. The sovereign debt that many investors have in their portfolios (ignoring the fact that there is life beyond traditional listed fixed income), which has risen as much as the Spanish risk premium has fallen in the last two years, reminds me a lot of the turkey sentiment before Christmas... (more…)

Los maestros de la inversión como Warren Buffett lo tienen grabado a sangre y fuego en su ADN: Invertir es como jugar a cualquier deporte centrándonos en el desarrollo del juego, mientras que hacerlo centrándonos en el marcador es pura especulación. Los partidos, los campeonatos y las glorias merecidísimas se las llevan quienes se concentran en el terreno de juego, en el desarrollo de una constante mejora de estrategia y habilidad competitiva a la hora de seleccionar empresas en las que invertir, y no en la especulación absurda de administrar un dígito reflejado en un luminoso, que por otra parte es tan volátil como nuestra propia incompetencia.

Los maestros de la inversión como Warren Buffett lo tienen grabado a sangre y fuego en su ADN: Invertir es como jugar a cualquier deporte centrándonos en el desarrollo del juego, mientras que hacerlo centrándonos en el marcador es pura especulación. Los partidos, los campeonatos y las glorias merecidísimas se las llevan quienes se concentran en el terreno de juego, en el desarrollo de una constante mejora de estrategia y habilidad competitiva a la hora de seleccionar empresas en las que invertir, y no en la especulación absurda de administrar un dígito reflejado en un luminoso, que por otra parte es tan volátil como nuestra propia incompetencia. La fiesta sigue. Después de los rallys de bolsas americanas y europeas -especialmente la española- parece que la mayoría de inversores va a volver a tropezar con la piedra de siempre. Cuándo? No se puede precisar, pero lo que es seguro es que la piedra está ahí y los inversores, ebrios de tanta subida, corren alocados como pollos sin cabeza. ¿Y cuál es la piedra en la que van a tropezar muchos? Pues lógicamente unas valoraciones de bolsas desarrolladas que para nada son ya baratas, por no decir que empiezan a estar ya caras. Sobre todo si tenemos en cuenta que los beneficios empresariales están en máximos y los tipos de interés en mínimos, lo cual inevitablemente nos acerca a su fin e inicio del ciclo inverso.

La fiesta sigue. Después de los rallys de bolsas americanas y europeas -especialmente la española- parece que la mayoría de inversores va a volver a tropezar con la piedra de siempre. Cuándo? No se puede precisar, pero lo que es seguro es que la piedra está ahí y los inversores, ebrios de tanta subida, corren alocados como pollos sin cabeza. ¿Y cuál es la piedra en la que van a tropezar muchos? Pues lógicamente unas valoraciones de bolsas desarrolladas que para nada son ya baratas, por no decir que empiezan a estar ya caras. Sobre todo si tenemos en cuenta que los beneficios empresariales están en máximos y los tipos de interés en mínimos, lo cual inevitablemente nos acerca a su fin e inicio del ciclo inverso.