Those of you who read us regularly will know that we have been saying for years that the Eurozone, as we know it, is neither viable nor sustainable. We warned this almost a decade ago (how time flies!), when the banking crisis was straining the seams of the Eurozone to the limit, and the dreaded Men in Black (MIB) of the Troika were scrutinising the public accounts of the Mediterranean countries of the south. The much-vaunted and politically correct concept of «More Europe» repeatedly hit the wall of the rich and productive North, which preferred a simple and profitable market union to a political, monetary and fiscal union.

.

Thus, the MIBs more or less discreetly shielded the Memorandums of Understanding (MoU) to avoid the free bar that we demanded from the South. Only in exchange for this and the stubbornness of the Eurobureaucrats to kick the can down the road and postpone the moment of truth, the Eurozone went ahead with all its incompatibilities and manifest unsustainability. The hope - in which nobody believed any more - was that with the help of the ECB's QE, and a few years of pseudo-bonanza, the South would, macroeconomically speaking, catch up with the North for once and for all. But the circle has remained unsquared for all these years.

.

The final blow to the economies of the South has come in the form of the SARS-CoV2 coronavirus pandemic, also known as Covid-19 disease. In this mother of all health crises, which is as bloody as it is short-lived, economies as large as Italy or Spain would need a shower of billions in debt (Coronabonds, Eurobonds or whatever you want to call them), which the northern Europeans are not prepared to finance jointly. Paradoxically, this time Merkel is not the standard-bearer of the NO to the free bar but the Netherlands, although it is also true that it is easy for the Germans to play the good cop with the bad Dutch cops. For whatever reason, the South (including France) is trying to take advantage of the final stretch of Merkel's political career to make some desperate concessions in spite of fierce Dutch opposition. The fact is that whatever comes after Merkel is likely to be much less inclined to make concessions to the South, remember the populism that Wolfgang Schaeuble achieved with his proposal to expel Greece from the System. A proposal that, on the other hand, made all the economic sense in the world.

.

Today, what the Netherlands and its circle of influence openly propose is a Europe as a simple common market (sound familiar?). And this idea of the EU coincides with the UK's idea of the EU, which has always been so vilified by Euro-bureaucrats. So this drift towards a «Less Europe» with which the North would feel comfortable could be the way forward, despite the opposition of the countries of the South, since we know that he who pays the piper calls the tune. But there is one small detail that complicates this idea of Europe: the Euro. A Common Market loses much of its meaning and simplicity if the monetary policy of all its members must necessarily be the same. In other words, having the same currency exchange rate, the same price of money (interest rates) and a single issuing bank (ECB), puts us back at the same starting point where we are right now. In other words, the South urgently needs trillions to survive, as well as a depreciation of the currency to regain competitiveness and hopes for growth, but the North is not willing to grant it at the expense of its economies. And this constant refusal is generating the rejection also of the European project by the countries of the South, since they know that the - insufficient - financial aid granted by the North will bring with it the relentless return of the dreaded IMFs, which entail the absolute loss of budgetary, fiscal and economic sovereignty in the countries of the South. The EU seems to be finally facing the final wall of the cul-de-sac along which it has been kicking the can down the road since 2011.

.

.

All this could well be covered up under the same Europeanist sheep's clothing, of course. That is to say, using euphemisms that might even keep the less informed in European inopia (continue to call both currencies the Euro, continue to call both issuing banks the ECB, etc.). But there would be undeniable differences, such as, for example, the value of the euro in the southern countries, which could be 20 or 30% lower than the euro in the north. Of course, they would initially be quoted at par, intervened by the ECB, to avoid as far as possible the implementation of corralitos in order to prevent the flight of assets from the south, but they would necessarily drift apart over time. Post-covid19 rates would not diverge in the short or medium term, as everyone needs zero or negative rates at the moment. But in the medium term, Northern Europe could finally follow in the footsteps of the Fed. gradually increased the price of its strong Euro. Maybe we could even see a political and fiscal union beyond the mere common market in one of these - at least - two distinct zones, who knows, since the circle is much easier to square with truly converging economies and a club with fewer members and more common interests.

.

So, how should southern wealthy individuals position themselves in the face of such a post-pandemic scenario? Well, obviously they should avoid accumulating assets in the South or in the South, i.e. avoid having real estate anchored in the less wealthy EU countries (Spain, Italy, Greece, Portugal and even France). Instead, they could hold them in countries that are likely to be able to sell in Euros that are not affected by the depreciation against the Euro in the North. Or hold them directly outside the EU, for example real estate in the USA, buying them still with the only existing Euro and not with the future devalued Euro of the South. As for financial assets, obviously shares of companies from these southern countries should also be avoided in portfolios, and of course their public and private debt. Moreover, as we have said countless times before, and today more emphatically than ever, the more safety steps we can add between our money and the need to collect or confiscatory In the southern states, we will sleep better at night. We must be aware that in times of extreme situations, extreme solutions will be taken, which we would never have foreseen just 6 months ago.

.

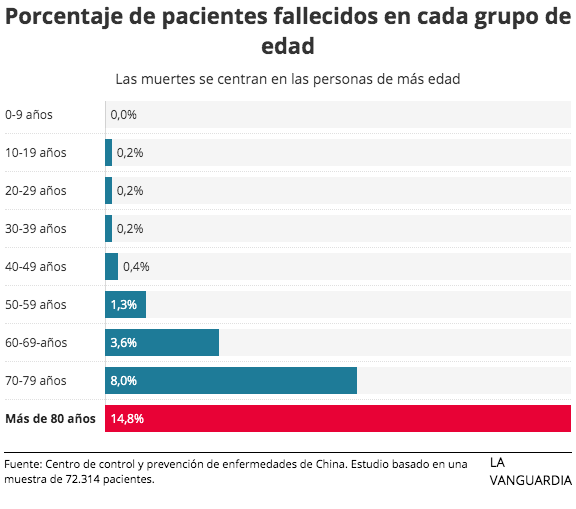

What is undeniable is that even if this EU evolution takes more or less time to arrive and Euro-bureaucrats keep banging their heads against reality, this pandemic is going to leave the West's economic and political supremacy mortally wounded. Covid-19 will have a clear winner, if anyone is going to win in this pandemic, and that winner is none other than China. Not only because it has coped and preserved its economy in an exemplary manner during the epidemic, but also because the rest of the world will inevitably set back several years of economic growth. And that will radically accelerate the leadership of China and its very powerful economic orbit (Vietnam, Korea, Malaysia, Australia, Japan, Indonesia, etc., even India itself), making Asia the new centre of the world. It is true that many will say that the figures of contagions and deaths from the coronavirus in China are unreliable. But let's not kid ourselves, because the figures for many Western countries are not reliable either, and very few question them.

.

In these weeks and months of the pandemic, we have seen how each country has handled the health crisis in very different ways. The results are as diverse as the idiosyncrasies of the respective governments and citizens. And in the European Union, especially in the South, we find countries (read Spain and Italy) that are managing the health crisis in a more than dubious way. Once again we are seeing the differences between North and South within the EU, also in health policy management. The only thing that will probably remain of this European union after the pandemic will be the relative resilience of the northern economies, and the common market that has always been advocated by the most realistic.

.

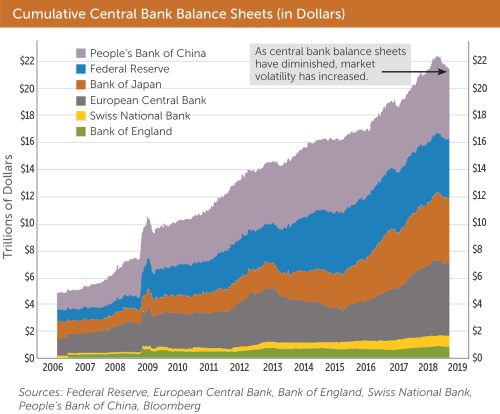

Golden times for the awakened investor. We warned mid-March and also last day 1st April (by the way, the markets have risen close to 30% since the lows of that time). This crisis will change a lot of things in Europe, and at the same time it is uncovering huge opportunities. Imagine if we can take advantage of the restructuring of the Eurozone and the Euro, if we can invest in healthcare companies around the world and especially in China, or if we can take advantage of the pull of the stock markets and economies of what will be the new centre of the world. And all this with the wind at the back of every central bank on the planet. Unfortunately times are bad for the local investor with local assets.

In this pandemic, which is now beginning to sweep the West, the investment opportunity is one of those that are often called once in a life time, This is one of those rare occasions in the course of a lifetime of investing. This is because, although there is always room for doubt due to imponderables that can complicate scenarios, business activity will probably recover to pre-pandemic levels in the medium term at best. Obviously these imponderables include, for example, a mutation that makes the virus more resistant and/or deadly, war conflicts that add more instability to the world order, or other health crises that could arise and coincide in time with the current pandemic. But if none of these things happen, the recovery in the tone of the economy will be no more than a few months. a couple of quarters, And what should a few quarters mean on the horizon for a good investor? Nothing.

In this pandemic, which is now beginning to sweep the West, the investment opportunity is one of those that are often called once in a life time, This is one of those rare occasions in the course of a lifetime of investing. This is because, although there is always room for doubt due to imponderables that can complicate scenarios, business activity will probably recover to pre-pandemic levels in the medium term at best. Obviously these imponderables include, for example, a mutation that makes the virus more resistant and/or deadly, war conflicts that add more instability to the world order, or other health crises that could arise and coincide in time with the current pandemic. But if none of these things happen, the recovery in the tone of the economy will be no more than a few months. a couple of quarters, And what should a few quarters mean on the horizon for a good investor? Nothing.

Another example: In Spain, the authorities have gone out of their way to emphasise that the existing infections were not from the EU (locally infected) but imported, from Italy, China, etc. They insistently stressed that this was a very important detail, trying to convince the population that Spain was in a perfectly controlled situation since our infections were all imported, ignoring the fact that it is only a matter of time before there are, as there have been, community infections in Spain. However, when faced with infections whose origin is not imported, the Spanish authorities still describe them as of «unknown origin», without yet recognising that they are already Community infections, i.e. local.

Another example: In Spain, the authorities have gone out of their way to emphasise that the existing infections were not from the EU (locally infected) but imported, from Italy, China, etc. They insistently stressed that this was a very important detail, trying to convince the population that Spain was in a perfectly controlled situation since our infections were all imported, ignoring the fact that it is only a matter of time before there are, as there have been, community infections in Spain. However, when faced with infections whose origin is not imported, the Spanish authorities still describe them as of «unknown origin», without yet recognising that they are already Community infections, i.e. local.

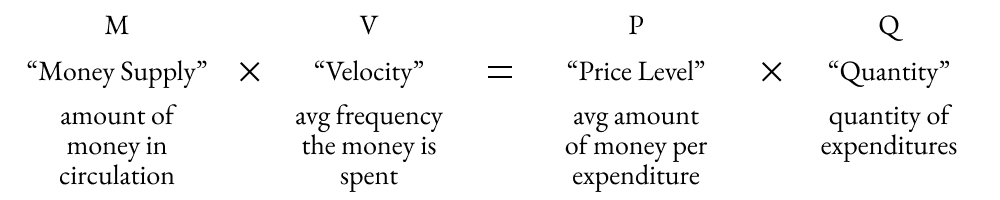

The fiat money system is here to stay, clearly, and we will never again see our money pegged to any real asset. It is simply too tempting for governments to have the power to create an infinite supply of electronic (formerly printed) money. But despite this endless possibility, which hyperinflationary ‘banana republics’ have been abusing, That Fiat standard was self-imposed, based on a criterion that has been key for almost 50 years: solvency. In this way, by linking the ability to create an infinite amount of money to the limits of solvency for repaying debts, Fiat money has, in fact, been the replacement of the gold standard with the solvency standard. In other words, trust in the state had a limit, which was none other than its actual ability to repay its debts and balance its books between public spending and tax revenue from the population without causing inflation to spiral out of control. For this reason, for decades there have been countries whose currencies depreciated against others due to mismanagement, forcing those states to cover their budgetary excesses with new money or public debt, which in turn fuelled inflation. This public debt had to be considered attractive enough for private capital from domestic and foreign investors to finance it. Investors who, consequently, demanded in return an interest rate commensurate with the risk that that state would be unable to pay its debts without printing banknotes, and that inflation would therefore erode its purchasing power. In other words, interest rates which in turn placed a price on the currency issued by each state, based on its ability to balance its books and its inflation rate, that is to say its Solvency.

The fiat money system is here to stay, clearly, and we will never again see our money pegged to any real asset. It is simply too tempting for governments to have the power to create an infinite supply of electronic (formerly printed) money. But despite this endless possibility, which hyperinflationary ‘banana republics’ have been abusing, That Fiat standard was self-imposed, based on a criterion that has been key for almost 50 years: solvency. In this way, by linking the ability to create an infinite amount of money to the limits of solvency for repaying debts, Fiat money has, in fact, been the replacement of the gold standard with the solvency standard. In other words, trust in the state had a limit, which was none other than its actual ability to repay its debts and balance its books between public spending and tax revenue from the population without causing inflation to spiral out of control. For this reason, for decades there have been countries whose currencies depreciated against others due to mismanagement, forcing those states to cover their budgetary excesses with new money or public debt, which in turn fuelled inflation. This public debt had to be considered attractive enough for private capital from domestic and foreign investors to finance it. Investors who, consequently, demanded in return an interest rate commensurate with the risk that that state would be unable to pay its debts without printing banknotes, and that inflation would therefore erode its purchasing power. In other words, interest rates which in turn placed a price on the currency issued by each state, based on its ability to balance its books and its inflation rate, that is to say its Solvency. The new standard is therefore that of fiat money, but for the past decade it has also been infinite by decision of the world’s most powerful central banks. In other words, The money needed to keep banks, large systemic companies and the states themselves afloat is being created and will continue to be created, as is the case in the southern part of the eurozone, by adding zeros to its debt and with negative interest rates (we already discussed this 6 years ago in

The new standard is therefore that of fiat money, but for the past decade it has also been infinite by decision of the world’s most powerful central banks. In other words, The money needed to keep banks, large systemic companies and the states themselves afloat is being created and will continue to be created, as is the case in the southern part of the eurozone, by adding zeros to its debt and with negative interest rates (we already discussed this 6 years ago in

Although we may not entirely agree with some of his convictions, there is no doubt that Daniel Lacalle is one of the people who knows the most about macroeconomics. Not only because of his PhD in Economics but especially because of his approach to the abuse of central banks that we have been suffering for more than a decade.

Although we may not entirely agree with some of his convictions, there is no doubt that Daniel Lacalle is one of the people who knows the most about macroeconomics. Not only because of his PhD in Economics but especially because of his approach to the abuse of central banks that we have been suffering for more than a decade.