It is not a question of being tremendists but simply of having a minimum of critical sense in the face of the barbarities that media, politicians and other official agencies in many Western countries proclaim according to their own interests and/or ignorance. For example, the 2% coronavirus mortality figure that is being bandied about is simply not realistic. And to realise this you just need to know how to multiply and divide as well as to know the reality.

.

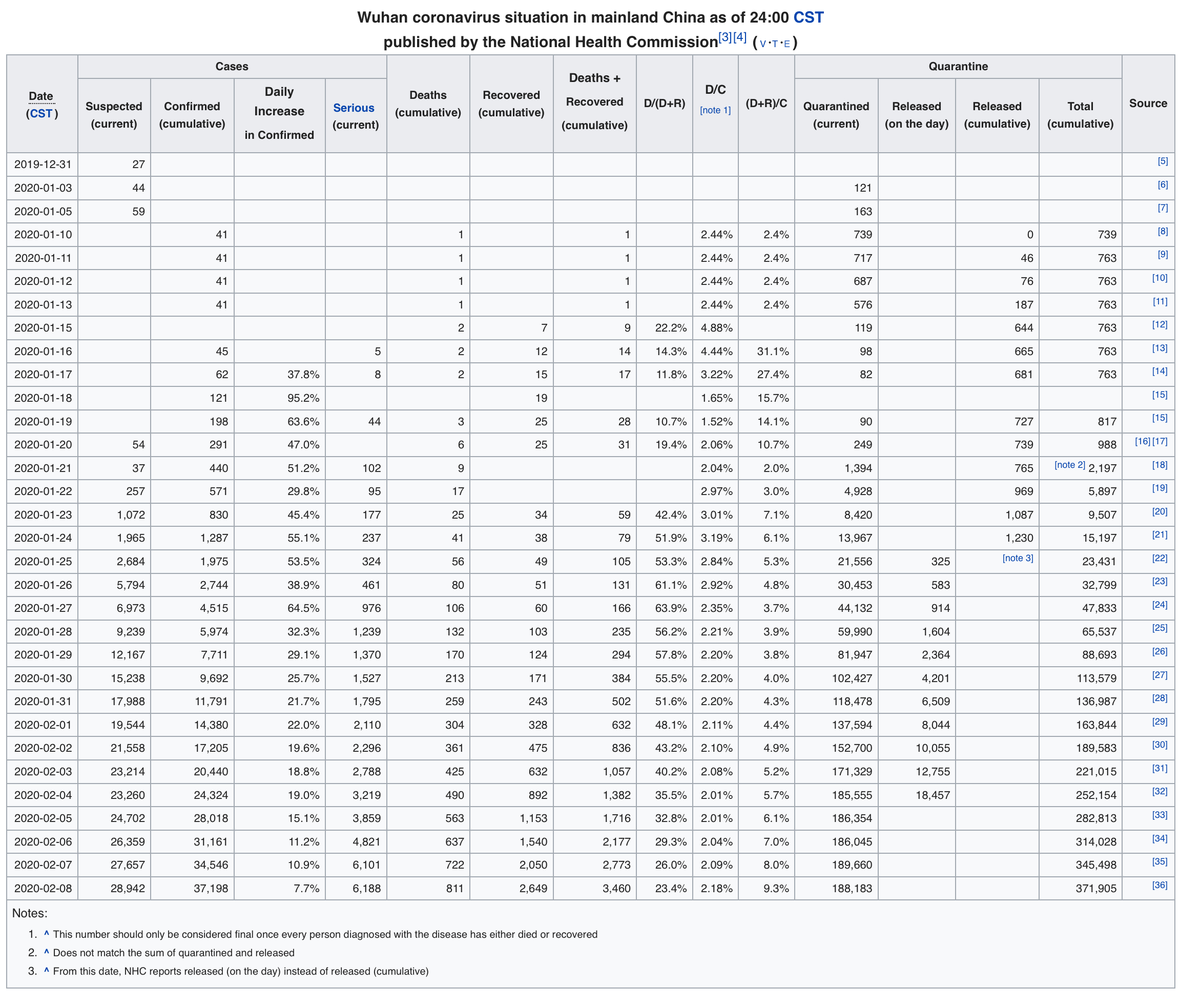

Although it may come as a surprise to many, the Wikipedia (graph below) is one of the sources with the most up-to-date and up-to-date data on the progression of the pandemic. We will take for granted the figures officially published by China to see that the mortality rate is probably much higher than the 2% mentioned, because if we think that the real figures are even worse (what other reason would the Chinese authorities have to manipulate them), the situation and the outlook would be even more terrifying. In the daily updates of those infected by the new or novel coronavirus we see a significant slowdown in the last few days, with the percentage going from over 30% to 7.7% in the last 10 days.

.

It is obviously very difficult to guess how many of those infected today will die in the next few days, and even more difficult to guess how many days they will survive. But just thinking that a fifth of the seriously ill (with altered vitals, i.e. really very sick), who currently account for almost 17% of those infected today, may end up dying in the next 4 days, let's say, and adding those who have already died, the calculation of the mortality rate shoots up to levels above 4%. And that is not counting the fact that none of those infected during the next 4 days will die in the following 4 days... We are therefore facing a pandemic whose mortality rate can only be calculated in retrospect, but which all indications are that it will probably double the 2% proclaimed by most of the media. Remember that the death rate from influenza is much lower than 1%, there is a relatively effective vaccine, and yet it still causes hundreds of thousands of deaths each year worldwide. If we add to this realistic mortality rate of this new coronavirus the chilling ease of contagion it is demonstrating and the fact that the vaccine has yet to arrive, the explosive cocktail is served. Moreover, imagine how this infection will behave in societies adjacent to China such as, for example Vietnam, Myanmar, Laos, Thailand, Philippines, India, Indonesia, Malaysia, etc., with 1.5 billion inhabitants whose hygiene, sanitation and epidemiological control systems are far more precarious than those of today's China. There, the proliferation of the virus cannot be controlled, as it is happening in China according to the official figures of the last few days, but only an accessible and timely medication or vaccine would prevent extravagant mortality.

.

It is worth reading the very interesting analysis by Tyler Durden on Zerohedge, The report rightly points out that in a country like the US itself, the situation could also become very complicated due to the high cost of the health system for the population that cannot afford good private insurance. This would lead the infected Americans to avoid using health services, with the consequent lack of control of the epidemic, despite being one of the societies with the highest per capita income on the planet. Moreover, in most Western democracies, governments would be far more reluctant than the Chinese government to harm their domestic economies to try to control the epidemic. By definition and unfortunately, most Western democracies would be more concerned about bowing to their lobbies and taking populist measures that would not jeopardise their re-election, the economy, or their partisan interests, than they would be about ordering courageous but unpopular measures. We see daily examples of health ministers and mayors downplaying the risks and calling for business as usual so that nothing disturbs the fragile economic balance in southern Europe. Without going any further, it is shameful that it is the companies themselves who have to suspend their participation in the Mobile World Congress in Barcelona, while the local authorities continue to insist on convincing them not to cancel their reservations for hotels, restaurants, chauffeurs and other unmentionable expenses.

.

That said, we should obviously not pin our hopes on controlling the pandemic globally, but on effective treatments and subsequent vaccines that can be made available to the world's population in the coming weeks. Because if we do not have those drugs for several months, the pandemic could reach our own neighbourhoods and claim millions of victims, especially in Asia. But it is not enough to discover an effective drug or vaccine; we must also be able to produce it on a mass scale and at a cost that is affordable for the vast majority of the world's population and/or states.

.

Health sector companies such as Inovio, China, a leader in research into viruses such as Ebola, MERS and Zika, is already testing potential vaccines for 2019-nCoV in animals. And probably the criticised «shortcuts» in international clinical trial protocols that China is surely taking will accelerate the achievement of an effective treatment that will save millions of lives around the world. Because given the extremely high rate of spread and mortality of this coronavirus, time is more than gold, it is Life.

.

But how is this pandemic affecting the global economy? Well, we are just seeing the tip of the iceberg of the destructive effects on economic growth. Obviously the first on the list to be affected is China's economy. But the cascading effect can be devastating because of the interconnectedness between Chinese products and those of the rest of the world. Just look at the Chinese components (often internal and invisible parts) around you, and think that they are already materially temporarily no longer being produced.

.

That word, the temporality, is the key to turning an unfortunate global health crisis into an opportunity. Because even if the treatment or vaccine arrives in time to prevent the global epidemic, the crisis in China is already an inevitable fact. But the fact that a large part of the country has already collapsed, with businesses closed, transport blocked and people locked in their homes, does not mean that this situation cannot be reversed in the coming quarters, but precisely means that China's resurgence is closer. Because, unlike other crises such as a trade war, an economic embargo, a military war or any other geopolitical conflict, this epidemic is not a crisis that can be reversed in the coming quarters. has an expiry date. This is not only because the infection will generate a natural peak and will eventually control itself, but also because any vaccination or medication will drastically shorten this period and the mortality it entails, minimising its effects and invigorating recovery.

.

Assuming that such medication or vaccine arrives in time to prevent a pandemic severely affecting Europe and America, what will be the post-epidemic scenario in Asia? Natural epidemiological timing indicates that a return to normalcy in China may come much sooner than in its neighbours. Moreover, China has far more resources, discipline and health structure to effectively medicate its population when the time comes. The Chinese state's strong political will and economic capacity to recover its economy through financial stimulus, which may even dwarf the QE carried out by Western central banks, will also be decisive. We should therefore expect a massive post-epidemic response from Xi Jinping's government. No effort will be spared to help the Chinese economy make up for lost time, which, let us remember, will not last more than a couple of quarters, given that the treatments (Chinese or Western) will not take long to appear and will be available to whoever pays for them. It is therefore foreseeable that during the second half of 2020 (or even earlier) the recovery of the Chinese economy will be underway, and it will be a matter of state and national pride to return to the path of dominance of the world economy to which the Chinese seem to be destined. Moreover, the trade war with the US has not spilled blood into the river, as we have already predicted almost a year ago, so there is even less reason for pessimism about China's economic recovery.

.

Therefore, in addition to preparing ourselves and our environment for the worst-case scenario of the pandemic (remember that the more than likely current mortality rate is much higher than 2% as we have seen), we would do well to position our investments to take the best advantage of this textbook black swan called the coronavirus. We should therefore take advantage of possible falls in the Asian markets - especially the sector healthcare Chinese- to buy shares in companies that will rise from the ashes of this epidemic with a strength and pride that we are unlikely to see in the West. Significantly, however, share price falls to date have been surprisingly modest, perhaps in anticipation of such a stunning economic recovery, or perhaps the result of Mr. Market's chronic schizophrenia, who knows.

.

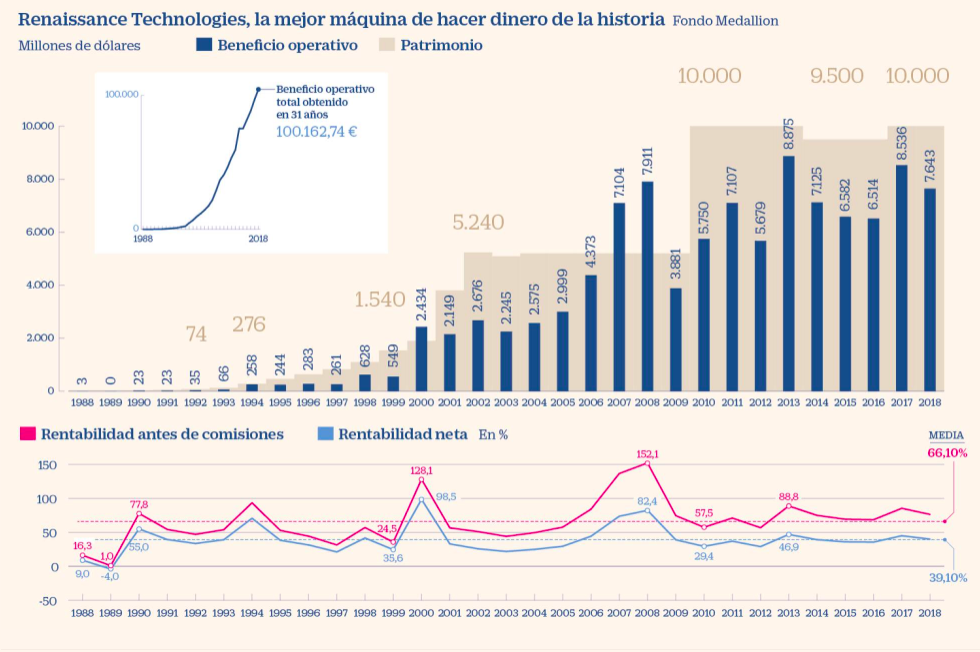

We have long seen Asia's growing economies as the only robust economic growth niche on the planet, and so we are now looking to Asia's growing economies as the world's only economic growth niche. we have said it repeatedly. Only there are the two indispensable factors for economic growth: high productivity; and a demography with a majority of productive young people and a minority of extractive retirees. It is no coincidence that a good number of funds in which we invest are managed in Asia and by local managers. That is why this unfortunate black swan comes, like all of them, accompanied by an opportunity that is rare in the course of an investment life. For the moment the Asian markets seem oblivious to the blockade in the making, and if the pharmacological solution arrives before the stock markets fall, so much the better. But if we see significant price declines in the coming weeks, it will certainly be an opportunity to buy and overweight Asian companies, especially in China, with huge potential in the coming semesters and years.

But what if we’ve missed the boat and are already in our second year of sixth form? Well, that doesn’t mean our hopes of studying in the US are over. We’ll just have to work a bit harder, and we’ll probably need to apply to start university in the Spring Term and not in the Autumn Term. In other words, there is still time, and they won’t miss a whole academic year; they will simply start a term later. This is because, at American universities, new students arrive every term to begin their degrees. There is enormous flexibility within the US university system, both in terms of the academic calendar and when it comes to switching from one degree programme to another and transferring credits.

But what if we’ve missed the boat and are already in our second year of sixth form? Well, that doesn’t mean our hopes of studying in the US are over. We’ll just have to work a bit harder, and we’ll probably need to apply to start university in the Spring Term and not in the Autumn Term. In other words, there is still time, and they won’t miss a whole academic year; they will simply start a term later. This is because, at American universities, new students arrive every term to begin their degrees. There is enormous flexibility within the US university system, both in terms of the academic calendar and when it comes to switching from one degree programme to another and transferring credits.

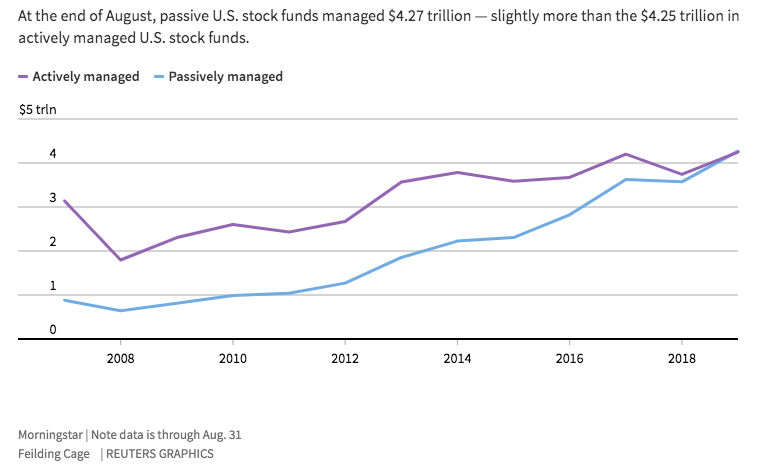

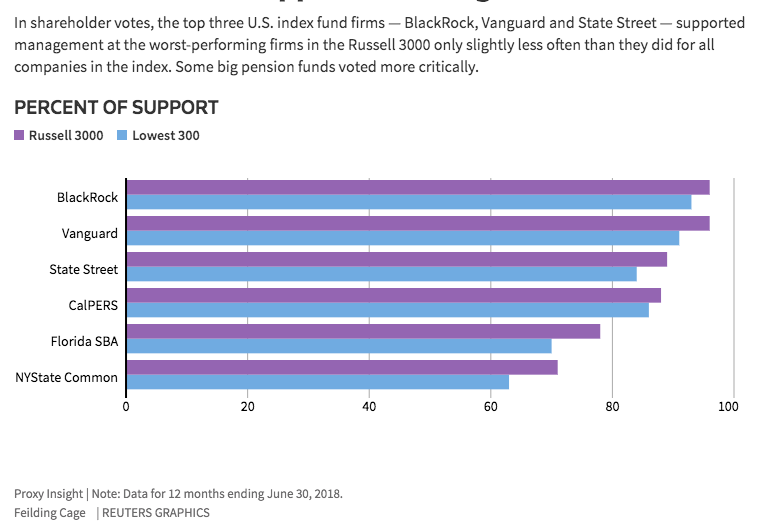

Another reason – this one more Machiavellian and immoral – for not going against the bad managers of large corporations is that it is those very same executives who are promoting these passive investment funds to their thousands upon thousands of employees. How else can one explain the fact that Vanguard, State Street and BlackRock all voted in favour of doubling the salary of the CEO of the energy company PG&E Corp, just after its shares plummeted following indications that the company was liable for the California wildfires? Or that they approved astronomical bonuses for executives at the cosmetics company Coty Inc – including half a million dollars to pay for their children’s school fees– after the company had been reeling from its reckless acquisition of Procter & Gamble’s beauty division. They have also unanimously vetoed an attempt by the other shareholders to separate the executive powers of the CEO and Chairman of the Board of General Electric Co, following a decade of poor results, etc., etc., etc… Even in the few cases in the Russell 3000 study where shareholders managed to veto executive bonuses, in 601 of those cases BlackRock attempted to award them bonuses through its vote.

Another reason – this one more Machiavellian and immoral – for not going against the bad managers of large corporations is that it is those very same executives who are promoting these passive investment funds to their thousands upon thousands of employees. How else can one explain the fact that Vanguard, State Street and BlackRock all voted in favour of doubling the salary of the CEO of the energy company PG&E Corp, just after its shares plummeted following indications that the company was liable for the California wildfires? Or that they approved astronomical bonuses for executives at the cosmetics company Coty Inc – including half a million dollars to pay for their children’s school fees– after the company had been reeling from its reckless acquisition of Procter & Gamble’s beauty division. They have also unanimously vetoed an attempt by the other shareholders to separate the executive powers of the CEO and Chairman of the Board of General Electric Co, following a decade of poor results, etc., etc., etc… Even in the few cases in the Russell 3000 study where shareholders managed to veto executive bonuses, in 601 of those cases BlackRock attempted to award them bonuses through its vote.

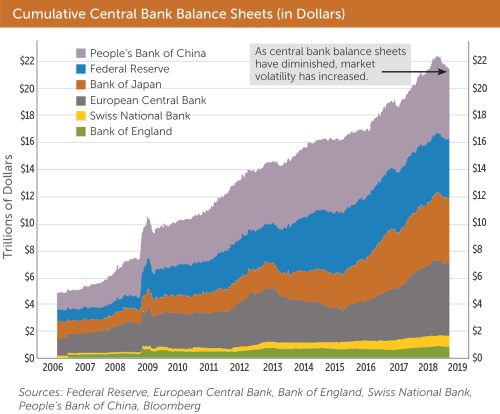

The fiat money system is here to stay, clearly, and we will never again see our money pegged to any real asset. It is simply too tempting for governments to have the power to create an infinite supply of electronic (formerly printed) money. But despite this endless possibility, which hyperinflationary ‘banana republics’ have been abusing, That Fiat standard was self-imposed, based on a criterion that has been key for almost 50 years: solvency. In this way, by linking the ability to create an infinite amount of money to the limits of solvency for repaying debts, Fiat money has, in fact, been the replacement of the gold standard with the solvency standard. In other words, trust in the state had a limit, which was none other than its actual ability to repay its debts and balance its books between public spending and tax revenue from the population without causing inflation to spiral out of control. For this reason, for decades there have been countries whose currencies depreciated against others due to mismanagement, forcing those states to cover their budgetary excesses with new money or public debt, which in turn fuelled inflation. This public debt had to be considered attractive enough for private capital from domestic and foreign investors to finance it. Investors who, consequently, demanded in return an interest rate commensurate with the risk that that state would be unable to pay its debts without printing banknotes, and that inflation would therefore erode its purchasing power. In other words, interest rates which in turn placed a price on the currency issued by each state, based on its ability to balance its books and its inflation rate, that is to say its Solvency.

The fiat money system is here to stay, clearly, and we will never again see our money pegged to any real asset. It is simply too tempting for governments to have the power to create an infinite supply of electronic (formerly printed) money. But despite this endless possibility, which hyperinflationary ‘banana republics’ have been abusing, That Fiat standard was self-imposed, based on a criterion that has been key for almost 50 years: solvency. In this way, by linking the ability to create an infinite amount of money to the limits of solvency for repaying debts, Fiat money has, in fact, been the replacement of the gold standard with the solvency standard. In other words, trust in the state had a limit, which was none other than its actual ability to repay its debts and balance its books between public spending and tax revenue from the population without causing inflation to spiral out of control. For this reason, for decades there have been countries whose currencies depreciated against others due to mismanagement, forcing those states to cover their budgetary excesses with new money or public debt, which in turn fuelled inflation. This public debt had to be considered attractive enough for private capital from domestic and foreign investors to finance it. Investors who, consequently, demanded in return an interest rate commensurate with the risk that that state would be unable to pay its debts without printing banknotes, and that inflation would therefore erode its purchasing power. In other words, interest rates which in turn placed a price on the currency issued by each state, based on its ability to balance its books and its inflation rate, that is to say its Solvency. The new standard is therefore that of fiat money, but for the past decade it has also been infinite by decision of the world’s most powerful central banks. In other words, The money needed to keep banks, large systemic companies and the states themselves afloat is being created and will continue to be created, as is the case in the southern part of the eurozone, by adding zeros to its debt and with negative interest rates (we already discussed this 6 years ago in

The new standard is therefore that of fiat money, but for the past decade it has also been infinite by decision of the world’s most powerful central banks. In other words, The money needed to keep banks, large systemic companies and the states themselves afloat is being created and will continue to be created, as is the case in the southern part of the eurozone, by adding zeros to its debt and with negative interest rates (we already discussed this 6 years ago in