At last someone is speaking clearly and openly on the subject. And, of course, the information had to come from COBAS AM. Here is a summary of some of the paragraphs we consider most interesting from the article signed by Gema Martín Espinosa, which you will find below in this link to the Cobas blog. A bolg that you should certainly follow closely, and in which we have had the opportunity to publish some articles in which we talked about the differences between passive and active management (yes, now that ETFs are so fashionable).

.

So let's look at the real reasons why many Spanish independent fund managers, all international fund managers and most investors shy away from the Spanish fund format for their investment vehicles:

.

«The essential thing for the investor to know is that when a fund manager offers both Luxembourg law funds and Spanish law funds, it is in fact the same product. In other words, the same management team, the same philosophy, the same investment process and the same portfolio.

.

The differences come from the other actors that a collective investment vehicle must necessarily have. In both cases a custodian bank is necessary, and some investors, faced with political uncertainty or instability in their country, choose to invest in a fund whose assets are deposited in a bank in Luxembourg rather than in a local bank (...)

.

With the European passport, it is true that you can choose to incorporate funds in Ireland, Malta or other EU countries, but over the years the Luxembourg brand has led the biggest flow of funds for cross-border distribution, not only in Europe, but also in Latin America and Asia.»

.

Here it should be noted that Spanish and Luxembourg funds are governed by the same directives, either the well-known UCIT (for plain vanilla vehicles) or the lesser known AIFM (for alternative or professional investor vehicles). The crux of the matter is that investors from outside Spain cannot invest in Spanish funds through omnibus accounts., The use of the new technologies, which are widely used in the rest of the world.

.

«What are omnibus accounts and why are they so relevant?

.

The holder of the omnibus account is the trading entity and not the final customer of the account. It allows the total of customer subscription and redemption orders to be transacted in a single transaction, without the customer's details being known or shared (...).

.

The financial institution issues a global order for each fund manager. Likewise, end customers do not open an account with other fund managers, but can access third-party funds through their marketing entity and from their own account.

.

Since Spanish funds are not marketed through omnibus accounts, the international investor must necessarily open an account with a marketing entity in Spain or with the fund manager itself in order to invest.

.

This operational barrier makes the Spanish fund very unattractive to international and institutional investors outside Spain, which is why several fund managers choose to manage the same fund in Luxembourg in order to give access to foreign clients.

.

These accesses are usually provided by international platforms, the vast majority of which do not contemplate operations with funds under Spanish law because they cannot comply with the requirements of transferring the details of the end investor in the operation. In addition to the platforms, European central depositories and custodians provide direct access to institutional clients by operating directly with the transfer agents or fund managers.

.

The lack of omnibus accounts in Spain also has a negative impact on Spanish fund managers when marketing their funds through other entities in Spain. And this is fundamentally for two reasons.

.

The first, and most powerful, is that the largest Spanish fund managers are part of banking groups with distribution networks (branches) where it would be impossible to think of them offering a competing product.

.

Secondly, even if the barrier of selling competing products were overcome, the fact that the marketing of a Spanish fund would necessarily involve transferring key data on unit-holders to the fund manager would come into play.

.

Although it is the fund manager who would receive this data and would be subject to the strictest confidentiality and non-use of the data, in general the fear of transferring client data tends to block definitively the marketing of Spanish funds by third parties in Spain.

.

For this reason, some Spanish independent fund managers choose to manage only Luxembourg funds, which are then marketed in Spain through third parties and cross-border through marketing agreements with platforms and distributors, thus resembling an international fund manager which, curiously, Spanish distribution networks do not perceive as “competitors”.

.

It is also important to dispel legends and myths. A Spanish fund is no better or worse than its Luxembourg brother.. Both are options that asset managers offer to respond to their clients as a whole, and have nothing to do with tax havens, high net worth or the “glamour” that is sometimes implied by their English names (...)».»

.

The advantages of investing from Luxembourg personal vehicles and banks is clear about doing it from traditional Spanish banks, with or without a sicav, but we have already discussed this at length in the article: «...".«The advantages of investing from Luxembourg«.

.

We hope that this post will finally help to clarify the issue. By the way, to differentiate at a glance between a Spanish fund and a Luxembourg fund, it is enough to look at the first two letters of its ISIN code: ES (Spain), LU (Luxembourg), IE (Ireland), FR (France), HK (Hong Kong), US (United States), etc.

Here is the newsletter sent out this week by Louis V. Gavel, from the prestigious research team at Gavekal, in which he talks about the effect of ETFs and the shift of the centre of the world from traditionally developed to emerging countries. A translated version of this article is proof of this:

.

«Another clear symptom that the investment world environment has changed is that the underperformance of emerging markets, which prevailed between 2011 and 2016 (when oil fell, the USD rose and yields remained low), is now clearly history. We are now living in a world where bond yields will tend to rise, the USD will tend to fall, and oil prices could show upward pressure. In such a world, exposure to emerging markets is once again rewarding. Indeed, an interesting feature of the recent falls is to see how volatility in US equity markets has actually been much higher than in most emerging markets. Even after this week's fall, Asian markets are significantly outperforming global equities.»

.

It is curious to see how, little by little, the centre of the investment world is shifting from the US and Europe to Asia, and with it, volatility is taking the opposite path. In other words, while development reaches the emerging countries, volatility travels to countries where development is weighed down by over-indebtedness. And the unfortunate thing is that for most advisors and private banking managers, investment proposals towards countries where there is economic and demographic growth with decreasing volatility (emerging countries), are of greater «risk» than traditional European and American funds, where anaemia and volatility take over their growth. The difficulty of finding good emerging funds that can be marketed in Spain, without having a suitable investment vehicle (where any fund, hedge fund or private equity in the world can fit, deferring taxation as if it were any fund sold to you by the bank on the corner) helps portfolios to continue to be filled with the usual funds. But reality is stubborn and the centre of the world is inexorably shifting towards Asia, where there are impressive managers who achieve spectacular alphas.

.

Here is the newsletter of Louis-Vincent Gave The complete, which is virtually unmissable:

In Agatha Christie's Murder on the Orient Express, the victim is stabbed by twelve different individuals.

The same is often true of bull markets; when they die, one finds many a finger-print on the murder weapon.

With that in mind, one could pin the death of the bond bull market on accelerating inflation, or on the globally synchronized global growth surge, or on the lack of investments in new capacity over the past decade (see A Brave New New World, attached), or even on the demographic shift unfolding in the Western World (see The Savings Glut's Long Life and Slow Death), or simply on the realisation that fiscal policies all around the world are bound to stay extraordinarily loose for far too long (see US Budget Deficits, attached)... But whichever reason one wants to hang one's hat on, the bond bear market is likely here to stay. After all, if bonds can't even rally by a few basis points as equity markets meltdown, then we must have a structural bond bear market on our hands.

And at the risk of stating the obvious, this structural bond bear market is now clearly a headwind for equities.

It also marks a profound shift in the investment environment.

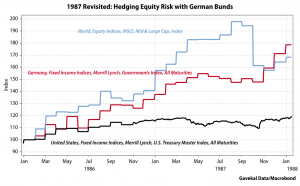

In a piece written close to the market top (see A Once in a Generation Shift - attached), we highlighted that OECD bonds had been the perfect counterweight to equity positions for decades. However, it wasn't always so. In periods when inflation picks up, OECD bonds do not protect portfolios against downside risk. Instead, they add to the downside risk. We also showed that one way to know whether we were in an ‘inflationary’ environment or a ‘deflationary’ environment was to look at the relative performance of long dated US Treasuries to Gold as both had asset classes tend to ‘trend’ over long periods of time. And when the ratio ‘gold to bonds’ moves ABOVE its 4 year moving average, that is typically a confirmation that we are moving into an inflationary environment. As the chart below highlights, following this week's rise in yields, such a move has now just occurred:

So if OECD bonds are no longer a sound hedge for equity risk, what is an investor looking to reduce the overall volatility of his portfolio, to do?

In the 1970s, and again in the 1987 crash, one of the best hedges (aside from gold), were German (and Swiss) bunds. Back then, the DM was slowly but surely establishing itself as Europe's trading and reserve currency; a genuine alternative to a US$ weighed down by too many years of US ‘guns and butter’ policies. Take 1987 as an example: US interest rates rose until they broke the back of the (then) roaring equity bull market. But as equities cracked and the fed slashed rates, investors sought out the safe haven of the inflation-fighting Bundesbank. So much so that, by the end of 1987, for an investor looking back at January 1986, German bunds had actually outperformed not only US Treasuries (that wasn't even close), but global equities as well:

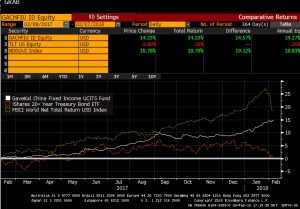

So, as Yogi Berra once said, is it ‘deja-vu all over again’? After all, in the US today, we not only have guns and butter; we should also soon have bridges, and tunnels, and hip replacements and student loan write-offs etc... (see The US Budget Deficits, attached). At the same time, we have China making a concerted push to turn the RMB into Asia's DeutscheMark, a currency that will increasingly fund Asia's trade and Asia's capital spending. And sure enough, just as global equities (World MSCI in the chart below) and US Treasuries (TLT US in the chart below) have started to roll over, Chinese bonds (represented below by the Gavekal China Fixed Income UCITS fun) have held their own. In fact, like German bunds in the fall of 1987, the Gavekal China Fixed Income UCITS fund has returned over 14% in US$ terms which handily beats the flat return of long dated US Treasuries, and could approach the return of global equities should global equities repeat the past week in the near future!

Another clear sign that the investment environment has changed is that the underperformance of emerging markets, which prevailed between 2011 and 2016 (as oil fell, the US$ rose and bond yields stayed low) is now clearly over. We are now living in a world where bond yields will trend higher, the US$ is trending lower, and oil prices could show upside pressures. In such a world, exposure to emerging markets once again becomes rewarding. In fact, one of the interesting feature of the current pullback is how volatility on US equities has actually been much worse than that of most emerging markets. Even after this week's pullback, Asian markets are significantly outperforming global equities. For example, our Asian Value UCITS fund (which focuses on developing Asia) is up +31.12% over the past 12 months, while our Asian Opportunities (which includes Japan, Australia and Asian bonds) is up +23.61% over the past 12 months. This compares favourably to the +19.4% gain in the World MSCI for the past year.

Still, the question at hand is whether we are now confronting a correction? The start of a crash? Or the unfolding of a genuine bear market?

ARGUMENTS FOR A CORRECTION:

We were due: record RSI indicators, record stretch without a 5% correction, first year without a down month etc...

As mentioned above, the investment environment is changing. Deflation should no longer be a concern. Central banks will no longer be as supportive of asset prices. The US$ is done rising. Oil is done adding liquidity to the system. Interest rates are moving higher... Any one of these forces would be a lot for the market to digest. But all together, they may be like Diderot's proverbial apricot, or Monty Python's wafer-thin mint: a little too much to chew on.

However, fundamentally, interest rates remain low, global growth is solid and so investors are likely to keep chasing returns?

“It's not a crash, it's a correction”.”

ARGUMENTS FOR A CRASH

Old card-sharks will always say that “if you sit down at a poker table and after 30 minutes, you have not figured out who the fish is, then you are the fish”.

Of course, in recent years, there have been no fish. Everyone won as all asset prices rose: equities, bonds, corporate bonds, real estate... It was just a question of relative performance with equities doing best of all. Still, as the equity bull market matured, it also evolved. Widening its reach and grasping the savings of an ever wider percentage of the population. So much so that, to a large extent, the bull market of recent years could be described as the ETF bull market. Indeed, according to data from research firm ETFGI, the ETF industry's assets under management (AUM) stood at $4.569 trillion in November 2017, compared to $3.396 trillion at the end of 2016. Assets under management of ETFs have grown by more than a trillion dollars in less than a year. Over 2016, in comparison, ETF assets grew by a relatively paltry $522 billion. Still, over the past two years, more than US$1.5 trillion of assets have flooded into ETFs. To put things in perspective, in 2017, the US mutual fund industry recorded a growth in assets of US$91bn. In short, last year, the growth of AUM in the ETF industry was basically ten times that of the mutual fund industry.

Now I manage money for a living. In fact, I took over the management of the Gavekal Global Equities Strategies almost exactly one year ago... and while the past three weeks have been tough (our overweight energy positioning did us no favors), we are still ahead of the World MSCI for the past 12 months (net of all fees):

The reason I highlight this is that I am sometimes called upon by our sales team to go pitch the fund. And invariably, a question that always comes up amongst smarter investors is “who are your other investors?”. And the reason smart potential investors ask this question is obvious enough: they don't care much for owning a fund with ‘Nervous Nellie’ investors who will panic at the first sign of trouble, hereby forcing the management of the fund (i.e.: my team and I) into liquidating assets at the trough of a cycle, when we should instead be focusing on picking up bargains.

The premise behind the (often-asked) question is that owning assets with a bunch of ‘weak hands’ is not an attractive long-term proposition.

This obvious enough common-sense brings me back to the massive inflows into ETFs that we witnessed in the past two years. Are the ETF inflows “sticky money” that will stay invested through the market's turmoils? Apparently, we witnessed US$30bn in ETF outflows last week (the first outflows in quite a while) and that was enough to create the dislocation we witnessed. What would happen to markets if those outflows reached 10% of the increase of the past two years, or US$150bn? What if the ETF outflows over the coming weeks reached 20%, or US$300bn? Who will take the other side of such large, incremental, marginal, trades?

To be clear: we have no way to know how sticky the ETF money will prove to be; if only because the inflows we have witnessed in the past two years are simply unprecedented. Meanwhile, the past few years have been so steady on financial markets that we have no real data to model how stable the ETF industry's AUM could prove to be in periods of stress. The only thing we know for sure is that the ETF industry is today a much larger beast than it was in 2008. And it is by and large an untested, and unknowable beast. And then, we also know that:

Historically, in periods of market stress, money tends to stay into mutual funds because mutual funds often charge upfront fees (the sunk cost fallacy), or because investors trust the managers they chose more than they trust themselves to navigate the market's choppy waters (the expert fallacy), or because they have done a fair amount of due diligence and thus want to validate their hard work (the sunk cost fallacy, again...) etc... Meanwhile, the whole point of ETFs is that they cost next to nothing to trade, that they do not require large amounts of due diligence, nor a relationship with a manager, etc... Thus, if we assume that the reason some of the ETF investors like ETFs is that they are easy to get into, and just as importantly easy to get out of, then should we not worry that some of the investors who chose ETF for the ‘easy liquidity’ will likely wish to exercise that very ‘easy liquidity’ now that the markets have started to head south?

Aside from higher liquidity, the other main reason investors like ETFs is the (perceived) low fees. And this is where the potential for disappointment could set in because of the difference in how ETFs and mutual funds trade. Let me use my own fund as an example. If tomorrow, an investor (Nellie Nervous), decides that she doesn't like the look of markets and no longer wants exposure to a global equity strategy, Nellie puts in her redemption form (before the agreed cut-off time) for, let's say, US$500k. I am then notified that by closing time tomorrow, US$500k will be leaving the fund. It is then up to me to decide whether I wish to reduce holdings across my 40 names proportionately, sell some of my exposure in US oil producers (in order to reduce the pain from my overweight energy stance), reduce some of my cash buffer etc... But whatever decision I have taken, by the next closing day, the money leaves the fund , Nellie Nervous receives her cash, which she can then deposit in short term UST, bitcoins, modern art, gold bars, etc...

Meanwhile, if Nellie owned US$500k of the QQQ (or SPX, or EWJ etc...), and decided to sell her ETF, what actually happens is that she places her sell-order with a broker, who (through the exchange) then turns to one of the “market-making” firms for that ETF. Assuming that, at this precise time, no-one is coming in to buy Nellie's ETF (hereby allowing for the shares to simply move from one investor's hands into another), then the market-maker (maybe Deutsche Bank, or Credit Suisse, or Morgan Stanley etc....) will give the exchange the price at which the market maker feels comfortable that it can unwind the position in the Nasdaq 100, or S&P 500, or MSCI Japan etc... And as we saw during the flash crash of May 2010, when markets unravel quickly, it can be hard for market-makers to keep up. At such times, the market-makers may well quote prices with greater and great discounts to NAV; which is how, back in May 2010, we saw a number of ETFs lose up to a third of their value, and sometimes more, while their underlying benchmarks were down just a few percent.

That was then. When the ETF market was much smaller, quainter, and less the plaything of the retail investment public than it is today. And so, with retail investors now in a full-on love affair with ETFs, let us imagine that, like a bad first husband coming out of prison, all of a sudden a liquidity squeeze like the 1987 crash or the 1998 LTCM meltdown re-appears. Not the start of a recession (a la 2001), nor a massive banking crisis (a la 2008), for neither looks likely today. But simply a good old fashioned liquidity squeeze, as investors realise that the investment portfolios they have constructed are now inadequate for the world in which we are moving (see A Once in a Generation Shift). With that, less us imagine US$150bn (or 10% of the past two year's rise in AUM) of outflows from ETFs (To be clear: this is pure speculation, for who is to know what the retail investors will decide to do tomorrow? For all we know, he/she may decide that the recent 10% dip is a terrific buying opportunity and buy more ETFs!). If this were to occur, then the questions that will rapidly appear will be:

Will the market-makers have the balance sheets to take on these transactions? If so, then

Will the market-makers have the appetite to take on these transactions? And if so, then

At what cost to the investment public, and profits to themselves (through higher spreads and discounts to NAVs) will the market markers decide to take on these transactions? If History is any indication, most likely a fairly large one. After all, what put the gold in “Goldman Sachs” and the more in “Morgan Stanley” has historically been the ability of investment banks to provide liquidity, at a high cost, to clients in the middle of a crisis. And if so, then

Will the general investment public conclude that both the ‘liquidity’ and ‘low fees’ attributes of ETFs turned out to be “bull market mirages”? And if so then

Will that realisation encourage yet more ETF selling, bringing us back to square one, above? Wash, rinse, repeat...

In other words, was May 6th 2010 the dress-rehearsal for what could soon happen in the ETF world?

Back then, a number of investors found out the hard way that the ETF's low fees hardly made up for the massive discounts to NAV that they suffered in the midst of a panic. With the experience of May 2010 in our rear-view mirror, and with a broader market sell-off now in the front and centre of any investors’ concerns, will investors once again be forced to confront the question of what is the point of saving 0.2% per annum in management fees if, when one wishes to sell in a panic, one ends up selling one's ETF at a 20% or more discount to NAV? Are ETF investors who think they can liquidate in a downturn going to have proven themselves to be “penny wise and pound foolish”? Will they be the fish to the card-shark investment banks?

ARGUMENTS FOR SOMETHING WORSE?

In the Spring of 2008, the global economy was humming along. In fact, for those of us sitting in Asia, it was hard not to feel very enthusiastic about the future: the Asian Crisis was falling off of our ten year rear-view mirror, China was delivering the greatest rise in purchasing power, over the greatest number of people in one generation, ever recorded in the history of Mankind (that's humankind for our Canadian friends). India looked set to join the global economy. Indonesia and Malaysia were developing fast, partly thanks to rising commodity prices, and partly thanks to attractive demographic profile. Even Brazil, of whom it was once said that “it is the next emerging market, and always will be’, was thriving.

Things were good. And then things turned bad very quickly.

Things were bad because the financial regulators, especially in the US but also to some extent in Europe, fell asleep on the job. They allowed banks to expand their leverage from the time-tested 10x, up to 40x and beyond. They rubber-stamped the creation of financial products that made little sense, (such as squared CDOs, PIK loans etc...) except that they allowed yield starved investors to gorge themselves - but without realising the risks they were taking as they did.

Could History repeat itself?

Probably not, if only because banks are nowhere near as levered as they were in 2008.

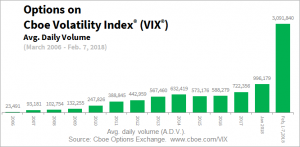

Still, one nagging concern is that, for the past five years, investors of all size and stripes (even small retail investors) came into the market day-in/day-out to sell volatility (daily volume on VIX options has risen from 23k in 2006 to 3m today!). This constant selling of volatility was just another way to ‘reach for yield’. And needless to say, the consequent downward pressure on volatility was very bullish for risk assets.

Projecting ourselves forward however, we can probably assume that the number of investors rushing to sell volatility forward will now be constrained to a smaller group of traders who actually understand what they are doing? Logically, this should mean that volatility should settle back closer to its long term mean of roughly 17%. If so, then that would mean that we would now confront an environment of higher interest rates and higher volatility.… And if we have higher interest rates and higher volatility baked into the cake, doesn't that almost guarantee lower PEs?

Following up on the above idea, we have seen in recent years, especially in the US, a rapid growth in quant funds, CTAs and risk parity strategies (witness the steady rise in SPX options trading). However, a number of these strategies were, in essence, levered longs on bonds and equities simultaneously, on the premise that bonds and equities are negatively correlated. However, as we surmised in our most recently Monthly, what happens if bonds and equities stop being negatively correlated? Well, obviously we now know the answer: the risk-parity, quants and algo traders have to start deleveraging their balance sheets aggressively in a market where the marginal buyer has, all of a sudden, disappeared. And the reason the marginal buyer has disappeared is that in recent years’ (as the picture below makes clear), the marginal buyer has started to look very different from the marginal buyer of past bull markets:

Which brings us back to the “yield-chasers” mentioned above. In my careers, every bear market has started with the ‘yield-chasing’ investors getting burnt. It is almost as if “the bear” enters a room and decides ‘First, I will eat the yield chasers. They are the easy preys. Then, if I am still hungry, I will eat the momentum guys. And if I am still hungry after that, I will have the value investors for desert’.

The fact that the yield chasers just got destroyed doesn't mean that, de facto, the momentum and value guys are next. Maybe the bear has had its fill, and goes back to sleep (after all, it is hibernating season)? But still, when the yield chasers get eaten, we momentum and value guys have to realise that we are potentially next on the menu...

And all this brings me to perhaps the single most important reason to be cautious given recent developments: namely the fact that this is now the second crisis in a decade where US regulators have shown themselves to the world to be completely hapless.

After all, if the current sell-off really is the direct consequence in the implosion in the XIV.US, and other such products, then the first question we should ask ourselves is why these products even existed in the first place? I mean, what economic interest was served by allowing retail investors to pile their hard-earned cash into a product that, through its very conception, had an extremely high probability of being worth zero at least once, if not twice, a decade?

Are we back to where we were ten years ago, when all of a sudden, we all had to figure out what a CDO-squared was and how they could implode the global financial system?

It is it just that, this time around, it's just a different bunch of letter but the core principle stays the same: let's create products that allow the average punter to reach for extra yield, even at the cost of getting blown up once a decade! The ultimate “eat like a bird and sh.t like a cow” trade?

Honestly: why would US regulators even allow things like 3x levered Brazil ETFs, or worse yet, inverted VIX ETFs who, by design, are destined to go to zero in a time of market stress? What economic benefit is there to have such products offered to the general public? Or more appropriately, what point is there to have a financial regulator is the regulator allows for things like a reverse VIX ETF, or futures on Bitcoins?

Unfortunately however, if the past is any indication, regulators will respond to this latest market hic-cup by telling money managers how they can pay for research, or by clamping down further on offshore tax havens, or by dictating firm's compensation policies... More regulations, of things that had nothing to do with the crisis in the first place! Thus, if the end result of all this is more lawsuits (one can bet one's bottom dollar that a number of the investors wiped out in the Volageddon will not take their losses lying down), more regulations, higher interest rates and higher volatility... then it is hard to walk away from the past week with a strong “risk on” mentality?

Or at the very least, a strong “buy the dip” mentality. For there are still risks that offer attractive returns across a number of equity markets around the world. It may however, be very different markets, and different segments of the markets, from those who have done so well for investors over the past five years.

As always, please do not hesitate to reach out if you have any comments or questions.

Yours truly,

Louis-Vincent Gave

PS: PLEASE NOTE THAT THE ABOVE REPRESENTS MY PERSONAL VIEWS AND IS IN NO WAY AN OFFER TO BUY/SELL ANY SECURITIES.

It is very curious to see how in Spain there is a very different mentality regarding the allocation of household assets to that of American households. As you can see in the interesting chart published by Inbestia and reproduced below, approx. 80% of Spaniards' assets are allocated to real estate, i.e. the main residence and additional real estate. Therefore, less than 20% are allocated to financial assets, such as shares (listed or unlisted), investment funds, pension funds, life insurance, deposits, etc.

.

If we compare the allocation between Americans and Spaniards, we will see that the preference for companies in the world's leading economy is much greater than in Spain and most other countries (although it would be interesting to know the figures for the north of the EU, which we suspect must be closer to those of the US). The entrepreneurial culture of North Americans is much greater, and half of their assets are invested in both listed and unlisted shares (mostly in their own businesses or with partners), investment funds, pensions and life insurance.

Why are Americans more inclined to allocate their wealth and savings to companies in general? Do we in the rest of the world not like our money to work for ourselves? Haven't the real estate bubbles affected Americans as much or more than Spaniards? The answers are not simple, but rather an accumulation of factors that make up the difference between one financial allocation and the other. Let's look at some of these reasons:

.

The financial culture in which American society is growing up has an entrepreneurial tradition and the majority of the population is clear that the only engine that moves the country and that can lead them to well-being is to participate in one way or another in the creation of wealth achieved by companies. Either as employees seeking hierarchical job progression or as small entrepreneurs (franchisees or with small personal businesses). They expect little more financially from their state. By contrast, in Spain and much of the rest of the Western world, there is less of an entrepreneurial culture, and more reliance on state-dependent labour activities, which are generally a little less liberal and a little more interventionist than in the USA.

.

Another aspect that makes Spaniards more inclined to accumulate our wealth in real estate than Americans is precisely the unpleasantness that the financial sector has been giving us in recent decades. For our banks, even today, volatility is the demon from which they recommend their clients to flee. To this end, they offer them all kinds of products and structured products with the obsession to reduce volatility, a concept that they mistakenly consider to be synonymous with risk. And of course, when volatility is confused with risk, it is much easier for the banking sector to sell low-volatility products than high-volatility ones. What customer will not try to avoid a high-volatility product if they are told about high risk?

.

Therefore, the general opinion of Spanish savers is that it is much riskier to invest in the stock market than in less volatile banking products or in real estate. And here we come to the second derivative: How have the low-volatility banking products sold by banks in recent years been performing? Well, in the best of cases they have been mediocre, and in the worst of cases they have been abused or have been directly sentenced to court, as in the case of the preference shares. This unhappy end to many of the low volatility products has exacerbated Spanish investors' appetite for real estate, reaching the extremes in Spain that we have seen in the graph: almost 90% in real estate and assets of their own personal business, such as self-employment, etc.

.

The right balance of wealth should moderate real estate and boost financial investment to levels similar to those seen in the USA (not for nothing is it the society with the leading wealth and GDP per capita on the planet). Families should enjoy financial investments that work to generate wealth for their old age, as the state pension is not going to do this sufficiently (and even less so in Spain). In addition, the US regulator limits more and better the access of retail investors to structured products and other nonsense that Spanish banks sell with impunity to any retiree without financial knowledge. This limitation on the sale of complex products to retail clients in the USA also channels a good part of these small savers to ordinary equity funds, which are less afraid of volatility and more inclined to buy the idea of investing in companies.

.

And what about real estate - does it not also guarantee the generation of income for our old age? The answer is yes, but with some additional risks that need to be highlighted: By massively concentrating our assets in real estate, we will be at the mercy of geographical risk, local economic risk or country risk, and the risk that the real estate cycle will no longer be favourable to us when its growth becomes saturated. Not to mention the risk of non-payment, maintenance and rising taxes on property owners. The diversification and freedom of movement that comes from acquiring shares in good companies all over the world, creating wealth in the most diverse sectors and countries on the planet, is hard to achieve with real estate investment. And the capacity of the business world to adapt and overcome whatever the future circumstances of the economy may be in the coming decades will never be able to be achieved by the inert brick.

.

Finally, the common characteristic of new clients who come to Cluster Family Office has always been the overload of properties in their portfolio. A lack of diversification that many paid dearly for with the bursting of the real estate bubble after 2007. And one of the first things we do for new Clients is to replace real estate and rentals with financial investments through versatile and fiscally efficient vehicles. They should make their money work for the family, either by generating alternative income to rents by buying good alternative funds or by seeking to grow portfolios by buying good equity funds from around the world. The volatility - not risk - that can be assumed by each family and professional circumstance in the financial portfolio should determine the proportion of investments in company shares or in alternative strategies that generate more stable income.

As Machado said, only a fool confuses value and price. From the point of view of the long-term investor, who buys shares in good companies at attractive prices relative to their present and future earnings multiples, it would already be absurd and foolhardy to buy and sell these shares in the short term without associating these decisions with the value of the respective businesses. But it would be even more absurd to do so. short term trading in a portfolio of actively managed mutual funds, The investor can also set up tempting automatic buy and stop-loss (sic) orders, with portfolios at the free will of their respective managers.

.

That is what ING offers to their clients, with the consequent benefit to the bank for this service, obviously. But as it is not as simple operationally to automatically buy and sell a fund at a pre-established price as it is for a share, what they offer their clients is a «warning» service when the fund's price reaches the marked price. It is then that the client will decide whether or not to sign a buy-sell-transfer order for these funds, which will usually take a couple of days to execute. Oh, and of course, this «service» is only available for ING brand funds, which means that everything stays at home.

.

In a review of the practice of share trading (including stop-loss), we have to say that it is the usual modus operandi of savers who are less qualified as investors. In other words, those who move away from long term investment by buying businesses whose good value/price ratio they know, and instead approach the mere bet on any ticker listed, regardless of the good or bad performance of the listed company's business. They are even oblivious to whether there are prospects and an adjusted valuation of a company's business, a commodity, an index or any derivative behind that ticker. For most of them, it is enough to have a ticker or a changing price to bet on more or less frantically, conveniently dressing up this practice with all kinds of trading courses, technical analysis and macros that disguise their gambling with a patina of expert investment.

.

However, generally speaking, an investor who knows the value of the companies in his portfolio will be more interested in buying them the more the price of their shares falls. Conversely, the more expensive the shares are in relation to the value of the company, the more interested he/she will be in selling them. In contrast, short-term stock trading is associated with completely ignoring the real value of the company. This is why technical analysis and other trading methods usually recommend buying stocks when prices are rising and selling them when they are falling. (Here we could make the exception of the very few quantitative hedge funds that have been making money for decades, but they would be the exception that proves the rule and would only be the exception that proves the rule. accessible to well-informed investors and with capital in excess of 300.000′- euro).

.

As we said, ING is now tempting its clients to carry out this trading practice also in their portfolios of actively managed funds. Active management is so called because the manager of each fund actively makes decisions by buying and selling stocks or bonds. From there, the net asset value of the fund will be the -usually- daily quotation of the entire portfolio at market price, after deducting the commissions and expenses of the active management itself and of the fund (on active and passive management you will be interested in the article that Cluster Family Office recently published on the website of COBAS AM, the manager of Francisco García Paramés: «Passive Management, Active Management»). Therefore, it makes even less sense for the saver to make decisions to buy or sell the fund when, not only does he not know the value of the businesses bought, he does not even know which businesses he has bought and sold. The manager of such a fund or the liquidity it accumulates on a daily basis. It would also not allow you to benefit from one of the key investment drivers that every value manager strives to achieve: co buy low and sell high, since such trading and stop-losses would completely detract from good active management.. Moreover, as fund trading is an absurd and rare practice, the saver would not even have the possibility to benefit from the self-fulfilling prophecy that technical analysis sometimes offers.

.

In short, yet another brainstorming strategy of the Machiavellian marketing department on duty, whose priority has never been and never will be the customer's benefit, but that of the financial institution itself. More wood to keep savers away from the right investment path.

We are delighted to announce that we have entered into a partnership with the asset management firm Cobas AM, led by the well-known Francisco García Paramés, so that we can contribute our articles to their blog. We recently published the following post on the Cobas AM blog, entitled «Passive management, active management«.

We know that more and more money is flowing into ETFs and passive and quantitative (with or without AI) portfolio management every day. This increase in the volume of passive management reduces market efficiency, which allows Investors (with a capital ‘I’) to capitalise on these inefficiencies and find value at a good price. In other words, fortunately, most of those who buy and sell in the markets are not looking for value but for profits (sic), which they tend to seek out in a cyclical and reckless manner, lurching from one loss to the next. They are not looking for good businesses to buy, but for winning tickers to bet on. And to do so, they use fleeting crystal balls which they discard one after the other as soon as the future proves them wrong.

.

Furthermore, active management fails to outperform the markets in more than 8 out of 10 cases. And this dismal statistic gets even worse the longer the investment period. All of this contributes to increasing market inefficiencies, which a good “value” fund manager (and there are some) capitalises on over time. The key for investors is obvious: knowing how to select that small percentage of active fund managers who consistently and sustainably outperform their benchmark indices over the years.

.

Then, amongst that small percentage of brilliant active fund managers, we can choose between different approaches, depending on the investor’s preferences or circumstances: deep value, value, long-only, long/short with a long bias, etc… But they must always outperform their indices with relatively concentrated and locally focused portfolios and fund managers, as diversification and distance are inversely proportional to one’s knowledge of the businesses in which one is investing.

.

That in-depth understanding of the businesses in which one invests is the foundation upon which results are built over the years. And to achieve this, it is not enough simply to study the balance sheets published periodically by companies (many active fund managers tend to limit themselves to that, at best). You have to travel, to get to know the companies first-hand – their management, facilities, suppliers, competitors, the local market and customers, and so on.

.

That is why, decades ago, we realised that, as investors and managers of our own and our clients’ assets, we would be far more efficient by specialising in the selection of fund managers and funds rather than in the selection of individual shares in which to invest. Because, however capable our team may be, it is impossible to match the level of knowledge possessed by these select fund managers, whose teams are constantly on the move, personally visiting executives and corporate premises throughout the year.

.

This select group of star fund managers, who have stood out from the crowd for decades, have teams of dozens of analysts at their fund management firms; some even have private jets, enabling them to visit in person and on a regular basis the companies and management teams in which they invest their own money and that of their investors. In this way, they regularly scrutinise business plans, future strategies and all manner of corporate decisions, which go far beyond the thorough analysis of balance sheets carried out at the fund managers’ headquarters.

.

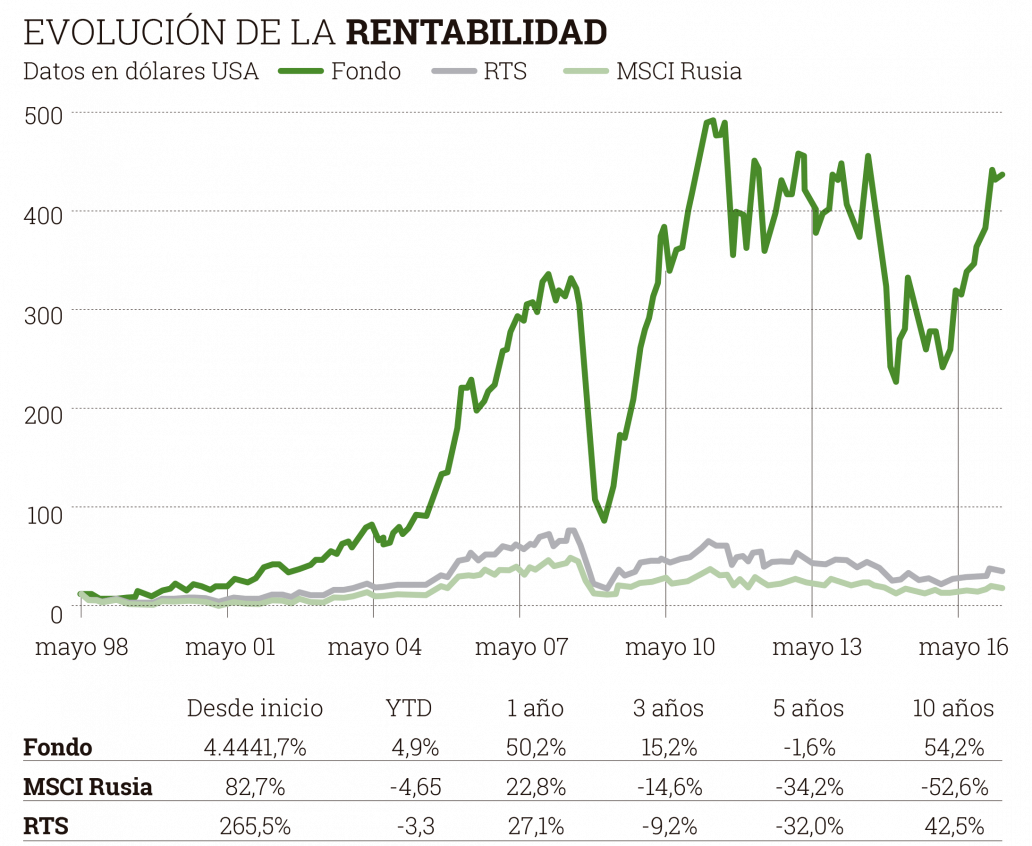

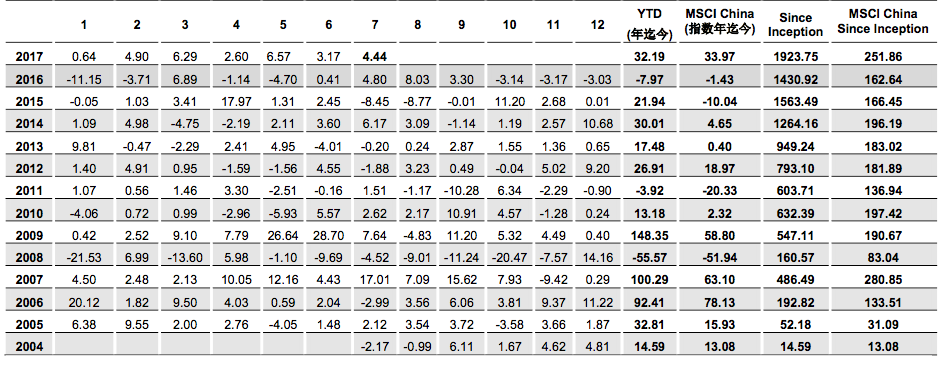

To give readers an idea of the scale of what we are discussing, one particular management firm in our portfolios carried out 2,200 face-to-face visits to various companies last year (not including telephone calls). This forms part of their standard routine in prospecting for and conducting exhaustive research into the businesses in which they are, or may become, partners through their investment funds. Below, you can see a sample of fund returns where their “value” managers have been consistently achieving extraordinary alphas over more than a decade, in extreme markets such as Russia or China (where they have, unsurprisingly, found greater exploitable inefficiencies and volatility than in fully developed markets):

.

.

But the difficulty of finding these fund managers amongst the sea of actively managed funds – which private banks tend to promote – is what leads many investors to turn to passive management, tired of paying management fees only to fail to even match the benchmark index. Unfortunately, it is very difficult to find good fund selectors in the financial sector, whose product ranges are limited to funds registered with the CNMV that pay them hefty commissions, but which have little track record and management teams that are as transient as they are anonymous.

.

Fortunately, actively managed funds – with stable teams comprising named individuals and a track record stretching back more than 10 years – still focus on results, consistently and sustainably outperforming indices, ETFs and semi-passive or fundamental ETFs.

.

The proper analysis and valuation of companies is, and must be, a true art form. And there are certainly those who are masters of this art, and they are the very reason for the existence of a good fund manager.

Note: The table showing the returns on the China fund does not appear in the article on the Cobas website because it was not compatible with the mobile operating system.

Like any wounded animal, a bank can be dangerous. More dangerous than usual, that is. The fact is that the army of bank employees usually carries out their superiors’ orders without question, whether out of a lack of ethical concern; or out of a desire to climb the bank’s corporate ladder; or simply out of a survival instinct as an employee who cannot afford to be sacked; or a very sad combination of all three.

.

Today we bring you a real-life example of what a Spanish bank like Banco Popular was capable of doing in the final months of its existence, before being «sold» for €1 to virtually the only entity capable of taking on such a financial black hole.

.

The events we are about to describe were, as always, perpetrated against an inexperienced small business owner, who in this case applied for a loan to start up his small business. We are talking about a loan of around €100,000, for the approval of which the bank asked the customer for all the necessary personal and financial details of the business. So far, so normal. The bank employee, a friend of his (of course), gave him high hopes that the loan would be approved, as his personal credit history was good and the business viable, so the customer began to set up his business despite not having the final go-ahead.

.

The surprise came a few weeks later, when his friend—the branch manager—confirmed the bad news that the delays had already led him to suspect: his loan application was not going to be approved, despite meeting the usual reasonable criteria. «Orders from above…» At that point, the problem for the client was enormous, as he would have to rush to another institution to secure financing and meet the commitments he had already made for his fledgling business. He also had to start the whole bank loan application process from scratch with unfamiliar bankers (not friends), and with no guarantee that the application wouldn’t also be rejected by that other bank. Nerves and insomnia took hold of the client and his family that first night, as you might expect.

.

The next day, the chummy manager at the branch called them in again and told them there was a chance of getting approval under «certain conditions, which I’ll explain when you come in». The client discussed this with his partner, feeling noticeably relieved, and they agreed that they could expect the loan terms to be tightened at their next meeting with the banker. They immediately took out their laptop and, together with their partner, began to recalculate the business plan in anticipation of a rise in the interest rate, a reduction in the loan amount to just €75,000, and a shorter repayment term. With their homework done, and having accepted these new, manageable red lines for themselves and their business, the couple headed to their meeting with the manager full of hope.

.

The surprise came when their friendly manager told them that, for their application to be approved, the loan couldn’t be for €100,000 or €75,000, but would have to be for the staggering sum of €150,000! ‘How is that possible? Does the bank want to lend us more money than we need for our business?’ asked the couple. ‘That’s right,’ replied the manager, ‘but on the condition that you use that surplus of 50,000 euros to buy shares in our bank. If you don’t accept these terms, unfortunately no loan will be approved.’

.

As everyone knows, a few months later Banco Santander had toinject €13 billion on the very day it «bought» the bank, technically for 1 euro, and that Popular’s shares were immediately written off to zero. But the perversion and precariousness of the Spanish financial system is such that banks in distress prefer to run headlong into the problem by lending excessively to customers, knowing full well that this money will be thrown into a bottomless pit. And knowing, moreover, that this diabolical over-lending condemns a solvent customer to insolvency and will be almost impossible to recover.

.

We are no longer talking about lending recklessly to customers to finance their dubious businesses, as happened with loans to property developers and builders during the property bubble; no. This is quite simply coercing customers with unsolicited money to finance the bank itself, which is on the brink of collapse, in order to keep it afloat for a few more months, weeks or days. Who cares if crimes are committed along the way and the lives of entrepreneurs who sustain the country with their taxes are ruined? Sadly, it seems that nobody does, at least nobody close to power or the financial system cares. Incidentally, the protagonists of this story signed up to the deal whilst their banker friend told them that, with a bit of luck, the shares would rise, as «they’re very cheap», and they would thus be able to repay their loan more comfortably. Obviously, they lost practically €50,000, which they will have to repay religiously, along with the other €100,000, suffocating their fledgling business and their lives beyond words.

.

Some of you might say that this happens to those who choose the wrong banks to work with. It is true that most Spanish banks have a greater risk than that ofother, more financially sound markets. And it’s not just a matter of securing finance; above all, investing through Spanish banks comes at the cost of the corresponding risk premium (which is why we still pay a positive rate on deposits here, whilst the most creditworthy institutions charge for them). But for the small business owner or investor, it is almost impossible to secure loans from more solvent foreign banks, and they are forced to finance themselves and invest in the ailing bank on the corner. The problem is that a dangerous animal, if wounded, is doubly lethal.

Once again, the disaster has come close to happening. And at the last minute, unspeakable pressure from the government has succeeded in getting Banco Santander to take over the huge hole in Banco Popular. Before it got this far, of course, capital was raised with money from unsuspecting new shareholders, bondholders and any other naïve people who believed in the image of security and solvency of characters such as those used by advertisers.

.

https://youtu.be/xD_4thIw1FQ

.

Most sports personalities, accustomed to selling their image for publicity, do so to the highest bidder without giving a damn whether they are selling more trainers or helping to wipe out the savings of humble families who believe that what Pau Gasol tells them can be trusted. It is difficult to apportion blame fairly: who is more to blame for small savers losing their money in these bank rescue operations: the bank manager, who is increasing capital or going public (Bankia) knowing full well that the investors he is deceiving are going to lose a large part of their savings? The regulator (BdE) who allows it, also knowing the critical situation of these balance sheets? The person who sells his image of credibility to convince those who without it would not trust that entity with their money? The bank employee who lies vilely to all the prey who sit at his table during the aggressive campaign to attract investment? The investor himself with his explosive cocktail of ignorance and greed? As the saying goes, between all of us the scammed and she alone is ruined...

.

In order not to be hypocritical, it is worth reflecting on another point. If the final destination of a failed bank is a bail-in, in other words, more debt that will have to be paid for with increases in our present and future taxes, every euro from a private investor that the bank captures - in collusion with the CEO, regulator, employee or publicist - will be one euro less that those of us who have not been duped by the whole gang will have to contribute. Therefore, leaving ethics aside, if other naive people plug the hole a little with their savings, the rest of us will have to pay less with our taxes. A vomitous political-financial jungle in every sense of the word, of course.

.

In the case of B. Popular, the disaster has been close to the crossbar and has only affected a priori the investors who trusted the institution as shareholders and the subordinated and preferred bondholders, while the depositors and the rest of taxpayers, for once, seem to have been spared another bank bail-in. But the million-dollar question is, in exchange for what? What has the government promised the Botín family to make them swallow such a toad? We will probably never know and it will remain, like the rest of the bail-outs and bank «reorganisations», indecipherably diluted in the tax returns that our children, grandchildren and great-grandchildren will pay for the rest of their lives.

.

The corporate rescue of Popular is nothing more than another symptom of the coming winter. This time the explosion has been controlled and concealed under the carpet at Santander, which today is at least 7 billion euros less solvent. But the persistent zero rates can already engrave another notch in its hilt of underground financial institutions. The problem is that when Germany can't take any more inflation and decides to raise rates, we in the south will need another central bank to keep them at zero. Then our banks and our prices will be able to lift their heads timidly, but our current accounts and assets in the south will be priced at a lower value than those in the north.

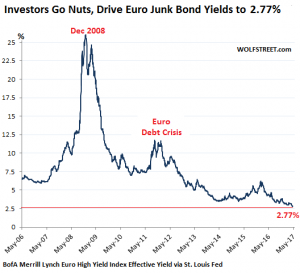

At the end of last week something unheard of happened, something absurd even among the absurdities of this New Normal that Central Banks have put us in: The average yield on junk bonds (the riskiest and most insolvent of corporate bonds) denominated in Euros fell to record lows of 2.77% per annum.

.

Already on 26 April, the absurdity of the ECB's negative yields policy hit a milestone, with yields on the most insolvent debt falling below 3% for the first time in history.

.

Comparatively, the most liquid and safe debt in the world, the 10-year US Treasury bond, yields 2.33% per annum, and the 30-year Treasury yields around 3%.

.

The following chart of the BofA Merrill Lynch Euro High Yield Index shows the madness in the Eurozone:

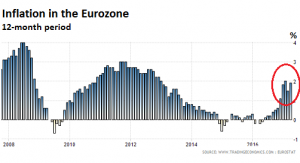

And it is not that these ridiculously low yields are the result of rampant deflation, despite the alarmism created in the last few months, no. The official annual inflation rate has been at 1.91 PPP3T and, as we can see in the following chart, it does not seem to be going away any time soon. Official annual inflation has been running at 1.9% and as we can see in the graph below, it does not look like it is going to disappear in the short term.

In other words, the real average yield on junk bonds, net of officially recognised inflation, as seen in the two indices above is now only 0.87% per annum! That is the return that bond buyers/investors get for lending their money to companies with junk ratings and manifest insolvencies for years, with risks of defaults (recognised by Fitch, Moody's and S&P) on the horizon more than considerable.

.

Against this backdrop, of course, it is not only European companies that want to raise fresh money. Like flies to honey, American companies are also flocking to the euro in search of euros from unsuspecting European investors in exchange for ridiculous interest rates. These are the so-called «Reverse Yankees», or issues by American companies in euros, eager for almost free credit. But why are European investors offering their money to insolvent debtors in exchange for so little? Have European investors gone mad? I'd better not answer you...

.

The answer lies in Draghi's efforts to implement his now reduced QE of 60 billion euros per year, which includes sovereign bonds, covered bonds, investment grade (IG) bonds and ABS. In addition, Draghi cut rates to negative -0.40%, thus intensifying the rise in debt prices and compressing yields on all debt, both sovereign and corporate (financial repression). What the ECB does not buy directly are junk bonds, but that does not mean that it does not end up with them in its cabinets (balance sheets), as it has bought and will buy paper that has become junk over time. And no one will be able to say that this was a misfortune that no one could have suspected, since much of this debt was already junk before it was bought and was given a rating upgrade by hammer and tongs to fit in with the politically correct requirements of the ECB.

.

As a result of this QE and NIRP (Negative Interest Rate Policy), many corporate bonds are now trading at yields below zero. For example the German 5-year bond is at -0.33%, which subjects investors to a very deep -2.23% after deducting official inflation! Obviously investors who want to achieve positive net (inflation-beating) returns, must either jump into the arms of much more insolvent and risky junk debt. Or they must fly into other currencies, such as USD debt. These are the NIRP Refugees, who «migrate» elsewhere to avoid the devastating effects of their indigenous debt.

.

The million-dollar question is why those affected by NIRP are risking so much for so little. Many are institutional investors who are obliged to buy euro bonds, such as insurance companies and euro fixed income funds. Moreover, with rising US rates, it is no longer even almost free to hedge EUR/USD currencies, as it was a couple of years ago. As a result, these institutional investors are condemned to buy wet paper at exorbitant prices and in exchange for ridiculous yields. Nor should we forget that these institutions are managing other people's money and not their own, what we will call DDO (Other People's Money), making it easier to take on bread for today and hunger for tomorrow, when this debt defaults or its price returns to more reasonable prices and generates huge losses for the unwary investors. The fact is that the managers of these institutions are paid to place these gigantic flows of DDOs, and they do so in line with the rest of the institutions. Because when collapse and losses, They will not be alone, as the rest of the institutions will suffer just like them. DDO that will blow up in everyone's face, in a very distributed and not very inculpatory way.

.

The more debt the ECB buys, the lower yields are in a perfect fish-bite, as well as other damage of incalculable consequences. Flooding the bond market with money is the perfect flight forward, satisfying the yields and capital gains needed by those who bought yesterday or last year. Play the game while the music is still playing, and no institution is going to stop before disaster strikes.

.

In addition to institutional investors, junk bonds are also sold at the price of gold to retail savers, unsuspecting investors who put their money in the «safe» and «guaranteed» funds sold to them by their corseted, sympathetic and trustworthy bankers (sic). And what has happened in the last few years, in which the music has continued to play non-stop, proves them right! Who hasn't made money buying this wet paper (sovereign or corporate) in the last 5 years? Why can't it continue to be like this for the next 5 years? Something like this thought the turkey the day before Christmas...

.

But the reality is that more and more issuers are turning to the European open bar. From runaway Spanish banks to the Mexican oil company Pemex, which placed 4.3 billion euros just a couple of months ago.

.

But bonds are not like shares. Bonds pay off (if you hold them long enough) at par. If you come to maturity, with these compressed rates, you can only make money if you have previously bought them at a discount. But in the current scenario, far from that, bonds are being bought in the secondary market above par! So what is the hope of all holders, traders and hedge funds of overpriced euro bonds? To get them out of the way early enough to gain a few pips before it is too late. But for institutional investors who have to hold them to maturity because their business model demands it, there will be no happy ending. Unless some clever institutionalist passes the hot potato in time to other, less experienced and more innocent hands, in the form of banking products that offer three times as much as a deposit, «with total security».

It is now official. In the covers The inevitable news of a death more than foretold by a few, who branded us as quasi-aliens for predicting the break-up of the Eurozone five years ago, has already been published all over Europe. Hollande and Merkel have chosen the pompous Palace of Versailles to announce that the EU of 27 has no future and that the Eurozone of 19 should at least go at two speeds. And so as not to panic the markets in the face of such an official statement, the announcement was staged with two guests of stone. The two guests with the largest - and therefore most dangerous - economies in the Eurozone: Italy and Spain.

.

In this way, the statement manages to give the desired image of North-South coordination. I mean coordination as such, not as an image of unity in any case. After all, it would be strange if the announcement of a two-speed Eurozone were staged exclusively with representatives of the first speed, wouldn't it? Moreover, as if the announcement were not already a hot enough potato in itself, it has been taken up by four presidents, three of whom are in precarious positions at the helm of their countries. Hence the precariousness also of the only apparent control of the situation.

.

Nor is the tone and vocabulary chosen by Hollande in the the interview a chorus of journalists from the media chosen ad hoc to cover the Versailles announcement (Le Monde, The Guardian, La Stampa and Süddeutsche Zeitung). When the journalists asked the French president why he was staging the announcement together with Merkel, Gentiloni and Rajoy, his answer was precisely scripted: «...the French president's answer to the question was: 'I am not a Frenchman, but a Frenchman.«Angela Merkel and I consult each other regularly. Before all European Councils and on all issues. It is in Europe's interest. But it is not an exclusive relationship. With the 60th anniversary of the treaty being celebrated in Rome on 25 March, it seemed logical to us to associate Italy and invite Spain«. In other words, Hollande and Merkel are managing the decisions, and for the staging (to be in the photo) willingly and graciously associate themselves with Italy (as a gesture of respect and recognition of a historical partner of the EU since its creation) and invitegenerously to Spain. Both as representatives of those of us who do not belong to the hard core of decision-making or to the high-speed economies. A gesture to reassure a periphery that might otherwise reject such a statement outright as totally alien to it if «someone of its own» is not included in the photo.

.

We are undoubtedly facing the official recognition of the opening of a melon that no one is even remotely sure how to handle. But whose staging, with representatives of the two speeds hand in hand and in apparent agreement (as it could not be otherwise), should open the eyes of all of us who seem condemned, due to our bad head/economy, to the 2nd speed. At this point we must insist once again on the warnings (here, here y here) that we have been making to investors in order to avoidance of asset depreciation(both financial and real estate) that such a broken Eurozone and 2nd speed inherently entail.

.

Now that it is no longer taboo or politically incorrect to talk openly about a two- or multi-speed Eurozone, political and financial analysts around the world have begun to publish its possible scenarios. Particularly surgical is the analysis of Wishart, Rojanasakul and Fraher from Bloomberg, in which they present 3 scenarios involving the break-up of the Euro. And 3 other scenarios that would allow maintaining a single Eurozone and a status quo as it is today for some time to come. In any case, we are already in a Europe that is somewhat more realistic and very different from the one that has been simulated for so many years. The 2017 ballot boxes will largely decide when the Eurozone breaks up and the future of today's Europe, which is much better than what happened in the old Europe whose destiny has historically been marked by wars. In the meantime, investors in the south should take safety measures and prepare to live in 2nd gear but enjoying 1st gear assets.

Es obvio que la irrupción de Trump en el escenario mundial cambia las reglas de juego en las que bancos centrales y euroburócratas nos habían aletargado. Y su acceso a la presidencia coincide en el tiempo con otros puntos de inflexión que por sí sólos ya merecerían centrar nuestra atención como inversores. Así, Trump potencia y acelera procesos como el Brexit, la subida de tipos del USD y la consiguiente venta de deuda soberana norteamericana, con las consecuencias que ello implica para las reservas monetarias de las mayores potencias mundiales.

.

Y si por si fuera poco, detrás de Trump está Steve Bannon, que deja la vehemencia de Trump a la altura del betún. El cargo creado ad hoc para Bannon, Estratega en Jefe, le confiere un carácter de hombre fuerte, fortísimo en el entorno del Presidente. No en balde inicialmente debía ser nombrado Chief of Staff, el cargo más influyente de la Casa Blanca, pero por presiones del partido republicano se acabó descartando Bannon en favor de Priebus.

.

Pues bien, dicho Steve Bannon, contradiciendo la versión oficial del Vice-Presidente Pence, comentó con el embajador alemán en Washington la necesidad de potenciar la relación bilateral Alemania-USA obviando la interlocución europea. Fuentes de Reuters filtraron el contenido de estas conversaciones y aseguran que Bannon y el embajador alemán hablaron de la UE como una construcción fallida y con muy poco futuro. Huelga decir que esta visión coincide totalmente con la del Ministro de Finanzas alemán, Wolfgang Schauble.

.

Por otra parte, Trump y Bannon potenciarán el Brexit hasta puntos impensables hasta hoy. Y aprovechando la excelente relación del Presidente norteamericano con la familia Real británica, se está planteando incluso la posibilidad de que los USA se unan a la Commonwealth. Un espaldarazo jamás visto a esta unión de Estados que en su mayoría formaron parte del Imperio Británico en el pasado. Y por supuesto, una puntilla para la moribunda UE, que está llevando la pre-negociación del Brexit al terreno de la amenaza y la hostilidad, quizá de manera poco estratégica.

.

Y en medio de este panorama, las subidas de tipos usd en puertas ya están generando ventas masivas de Treasuries por parte de bancos centrales que hasta hoy habían acumulado cantidades ingentes de ellos. Un cambio de escenario radical respecto a la última década. Y de consecuencias imprevisibles, sobre todo si tenemos en cuenta que uno de los mayores tenedores de deuda soberana norteamericana es el China. Sí, el mismo gigante (entre otros muchos) al que Trump pretende declarar una guerra comercial más que temeraria. Sobre todo pensando en que los chinos tienen el poder de abrir o cerrar el grifo de sus masivas reservas de Treasuries según las necesidades estratégicas de tipos de cambio USD/RMB o las amenazas políticas que a buen seguro veremos en los próximos meses.

.

Además, en Mayo puede detonarse otra bomba política nuclear y Le Pen puede llegar al poder. Una probabilidad mucho mayor de la que parecen descontar los mercados más visibles (bolsa y bonos), al menos así lo vaticinan hoy mismo desde Bloomberg: «If tail risks are to be believed, the risk of Frexit is larger than what is currently assumed«. Y sin olvidar que Alemania también va a tener en los próximos meses elecciones imprevisibles. Abróchense los cinturones y tomen medidas de seguridad. Especialmente aquellos inversores que creen que la Eurozona seguirá siendo la Eurozona, y los que confían que los euros de su cuenta corriente seguirán teniendo el mismo valor que los de los alemanes.

We have been made aware of phishing and spoofing attempts involving fraudulent email addresses and domains that closely resemble our official company communications. These unauthorized communications are not sent by our company and may falsely impersonate our employees or representatives.

Our company is not responsible for communications, requests, or transactions originating from fraudulent or unauthorized email addresses or domains. Please verify that all communications originate from our official email domain before responding or sharing any information.

If you receive a suspicious email claiming to be from our company, please do not respond, click any links, or provide any information. Contact us directly using the contact information published on this website to verify its authenticity.