China’s new financial experiment covers an area of 29 km²: Shanghai FTZ. A «free trade zone» in which the Communist Party’s economic restrictions are lifted as if by a stroke of political policy. In this financial centre, international investors will be exempt from the investment restrictions that apply elsewhere in China. And, note this: in this artificial oasis, the Chinese currency, the Renminbi (RMB), will be freely traded, as will its interest rates!

China’s new financial experiment covers an area of 29 km²: Shanghai FTZ. A «free trade zone» in which the Communist Party’s economic restrictions are lifted as if by a stroke of political policy. In this financial centre, international investors will be exempt from the investment restrictions that apply elsewhere in China. And, note this: in this artificial oasis, the Chinese currency, the Renminbi (RMB), will be freely traded, as will its interest rates!

Up to 18 sectors, ranging from finance to shipbuilding, will benefit from a level of regulatory relaxation never before seen on Chinese soil (Hong Kong cannot strictly be considered part of China). In fact, the new zone is considered the most significant political and financial reform undertaken by the Communist Party since Shenzhen was designated a «special economic zone» on the border with Hong Kong in 1980. This territory will effectively be outside Chinese customs control, being de facto a territory within China, but independent of it. Consequently, local and international companies (including banks) will be able to set up there freely and trade both domestically and internationally with complete flexibility, exchanging RMB for any other international currency.

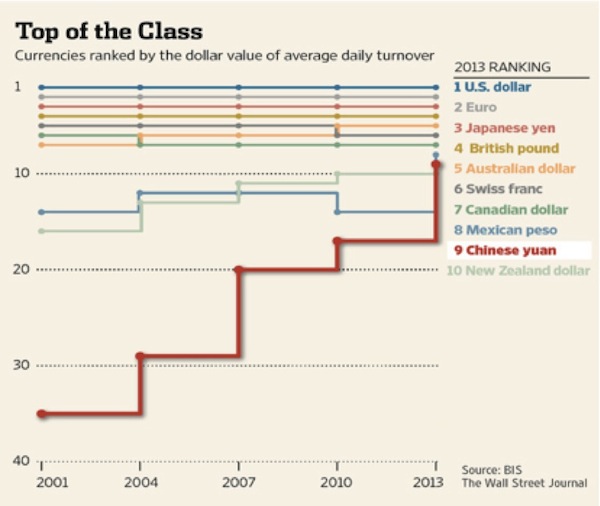

This controlled move towards greater openness is perfectly in line with the Chinese government’s aim of establishing the renminbi as a global reserve currency. And international trade between so-called Greater China and its neighbours in Oceania is already largely taking place with payments accepted in RMB (also known as the Yuan or by its abbreviation CNY). As you can see from the chart below, the growth in RMB trade has been spectacular over the last two years, with the currency now ranking ninth among global currencies.

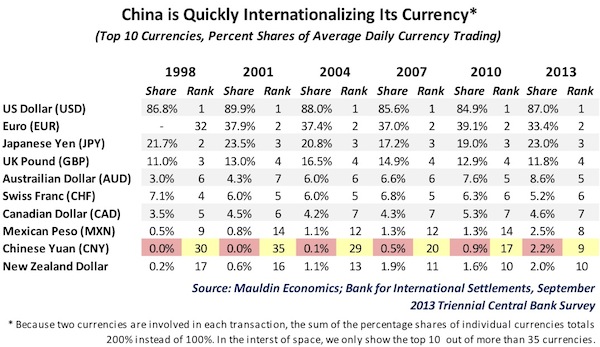

As can be seen in the chart below, only 2.21% of global transactions are currently conducted in RMB. However, its growth trajectory is spectacular, given that it was virtually non-existent 10 years ago and has increased 2.5-fold over the last three years. We also see an interesting trend in this table: the decline in the use of the euro as a currency for international transactions, which has fallen from 39.11% to 33.41% over the last three years – bear this in mind…

The acceleration that the Shanghai FTZ The role it will play in ensuring the international use of the Chinese currency grows in the coming years is beyond question. This is all the more true given that it is a financial centre which, together with Hong Kong, constitutes the only powerful and modern financial hubs in the whole of South-East Asia, the Chinese sphere of influence and Oceania. Furthermore, the Chinese government’s intention is clear, and it will not hesitate to use its vast foreign exchange reserves to achieve its strategic goals: to position its currency, slowly but steadily, at the forefront of the global economy.

It is certainly telling that, over the last few quarters, China has been building up substantial gold reserves, perhaps in anticipation that, at some point in the not-too-distant future, the global monetary system will return to the gold standard. At that point, the RMB would be the undisputed global reserve currency.

But let’s get down to practicalities. Does this process of opening up the Chinese currency present an opportunity to invest in it, capitalising on its appreciation? It is far from clear. For what might seem like common sense may not be so obvious when we consider that there are hundreds of millions of Chinese keen to invest outside their country (in the local stock market), and to do so in currencies other than the RMB.

For all these reasons, it seems that the Chinese government’s intention is to make this transition from a controlled currency to a global reserve currency in a very gradual manner. But what is clear is that the creation of this experiment known as Shanghai FTZ, is the embryo of the next global financial leader. And given that partners more suitable vehicles (investment funds/private equity); to stop investing in an economy with such potential over the coming months and years represents a huge opportunity cost for any investor. Investing where the middle class is growing is a vital criterion for achieving medium- and long-term returns. This is particularly true given the outlook we face of excessive debt, anaemic economic growth, and an economy addicted to the unsound stimulus measures of central banks.