For those of you for whom the trees of panic and volatility prevent you from seeing the forest of opportunities and returns that lie in the palm of your hands, let us explain Nick Maggiulli's simple, mathematical analysis of Ritholtz Wealth, which we fully endorse.

.

The crux of the matter is to shed light on asset purchases during times of panic. But first let us put the current crash in context.

.

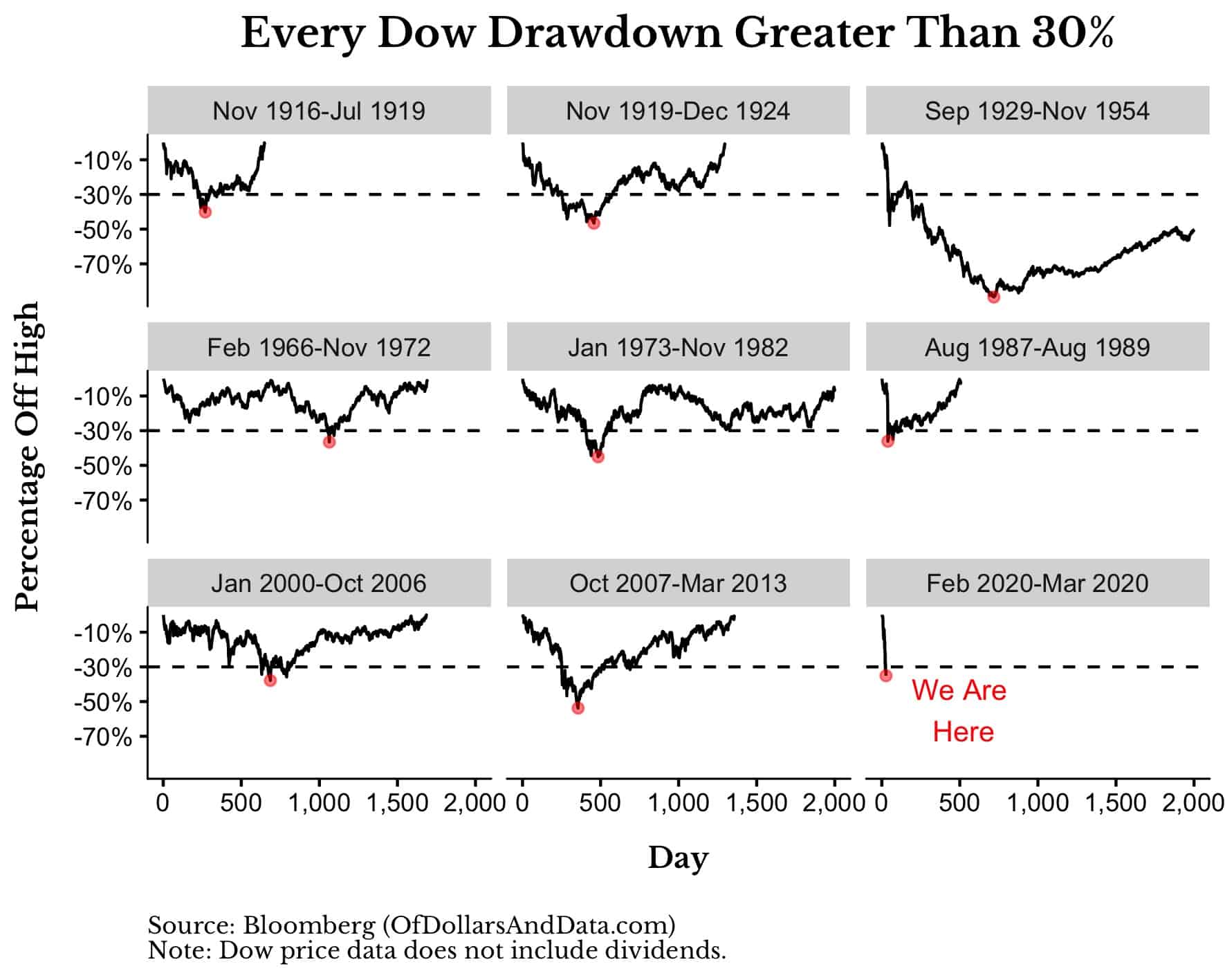

As of today, the low for the Dow Jones has occurred on 23 March 2020 and has been 35% from its highs, making it one of the worst months in the history of the US stock market.

.

If we analyse all the crashes above 30% since 1915, we see that this crash is one of the fastest and fastest we have ever had.

Moreover, while in the past we see the little red dot that signals the floor, at this moment we still do not know if we have already seen the low of last week or if it is still to come in this coronavirus crash.

.

Nevertheless, there is no doubt that these are golden times for investors buying equities now. Every euro or dollar we invest in today's markets will grow much more than those invested in previous months as soon as the markets recover. Because we all assume that sooner or later the markets will recover and humanity as a whole will eventually beat this virus as it has beaten other health crises before, right?

.

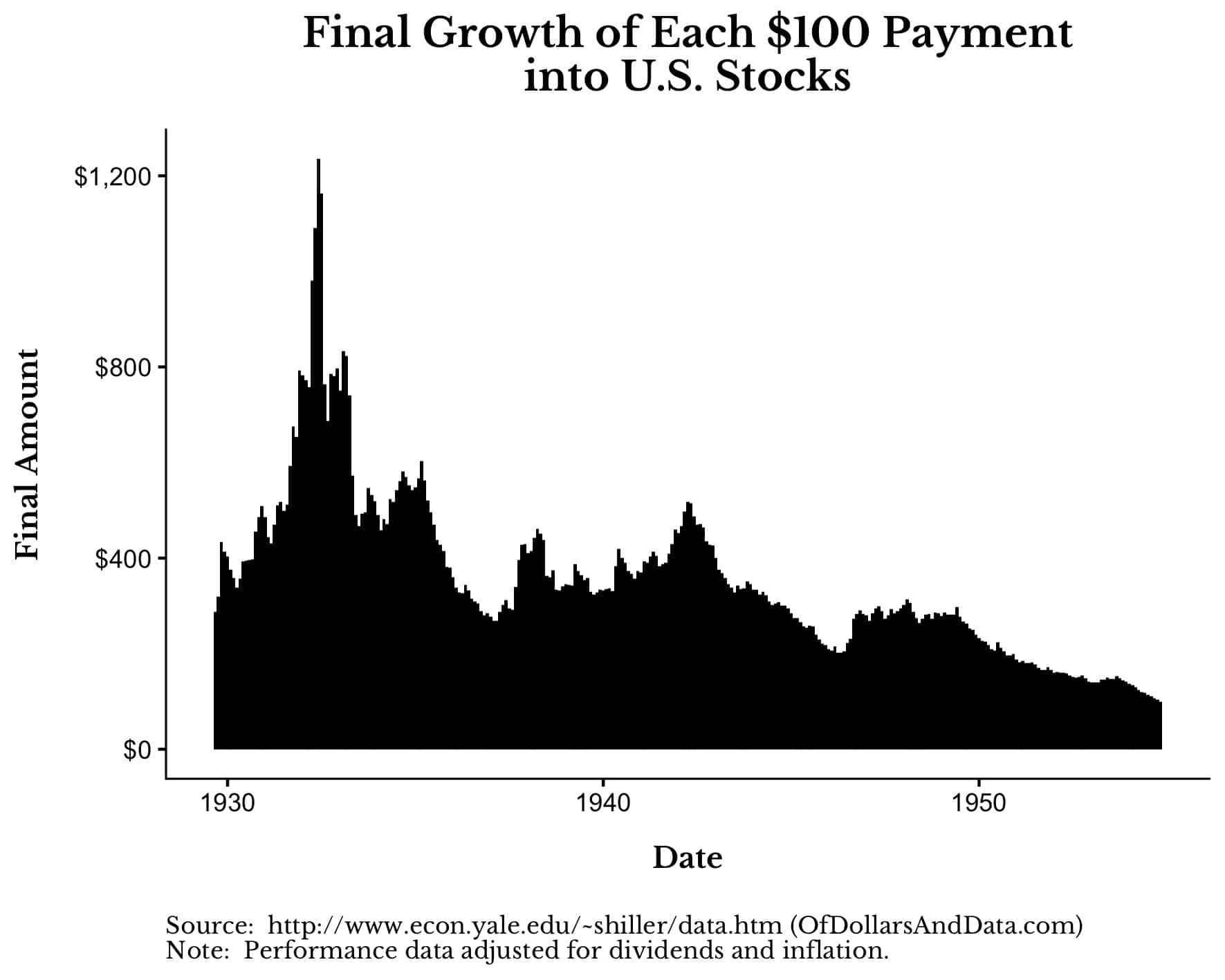

To demonstrate that every dollar invested today will yield much more than those invested before the crash, let us imagine that we decide to invest $100 every month in the US stock market from September 1929 to November 1954 (crash of 1929 and its subsequent long recovery).

.

If we had followed this strategy, this is what each $100 packet would have earned (including dividends and adjusted for inflation) until the recovery was completed in November 1954:

As you can see, the closer we bought to the low in the summer of 1932, the greater the long term benefit of that purchase. Each $100 invested at those lows grew $1200, which is three times as much as the $100 packs bought in 1930 ($400).

.

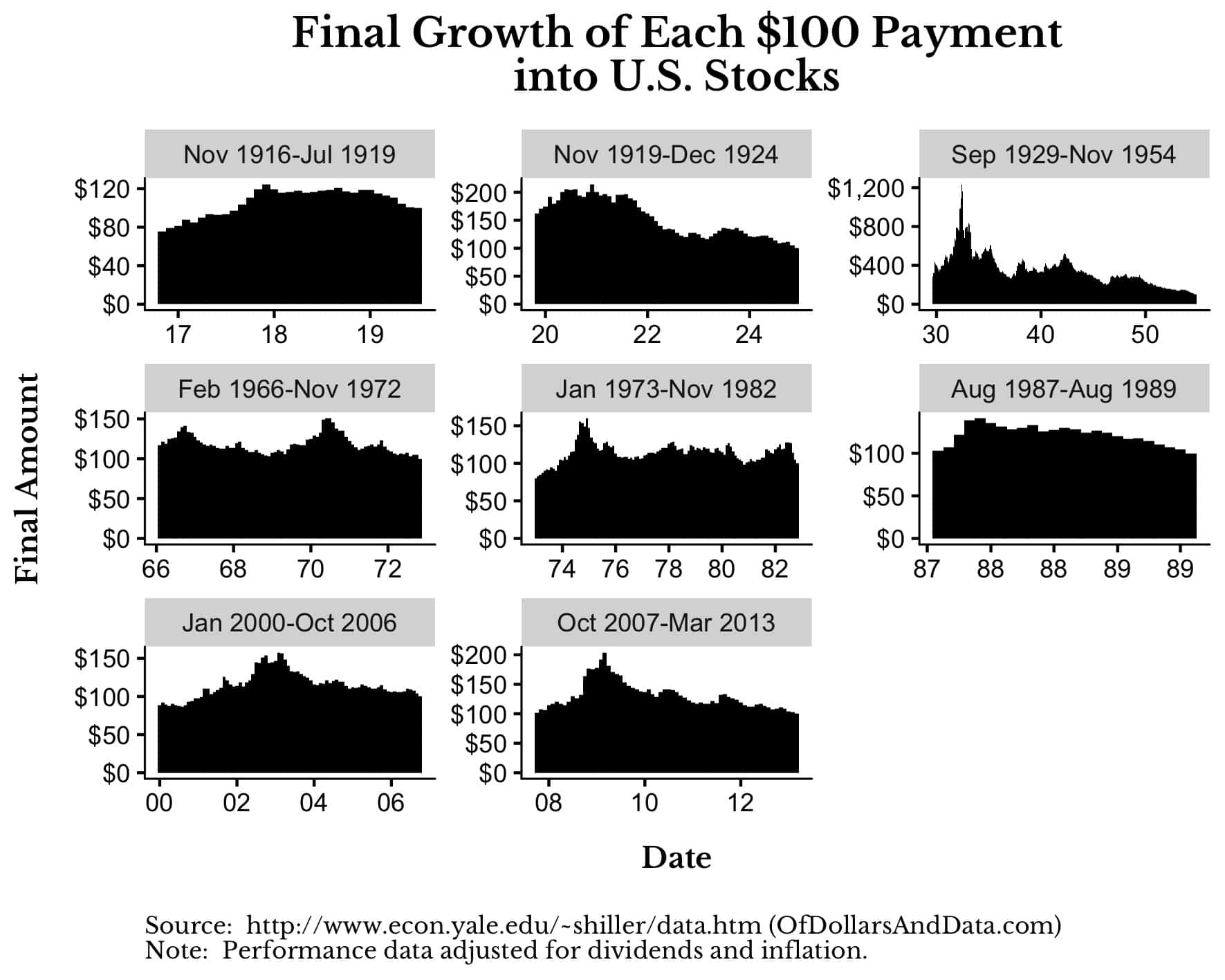

However, even if we look at the other falls above 30% shown in the first chart, we still see much higher profits if we buy during times of major panic and market declines:

This chart shows that buying near crashes (even if we don't hit their lows exactly) provides between 50 and 100% more profit compared to an investment at other times. That means that your $100 will grow $150 or $200 more (adjusted for inflation) when the market has recovered again.

.

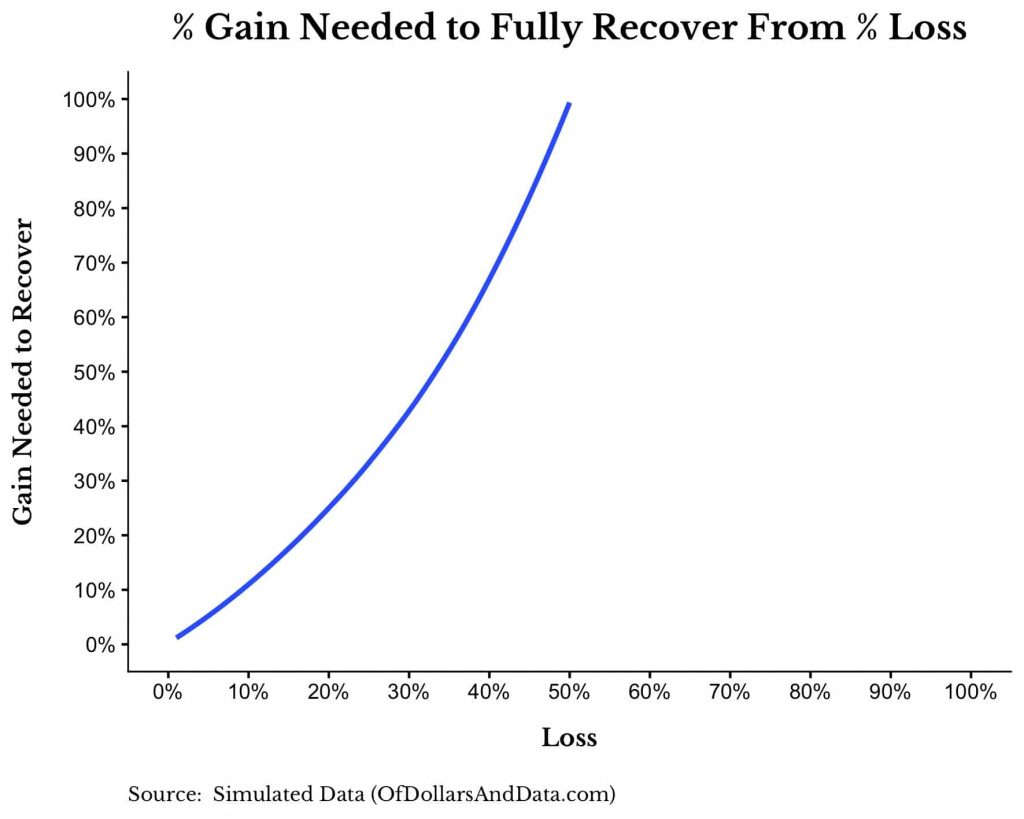

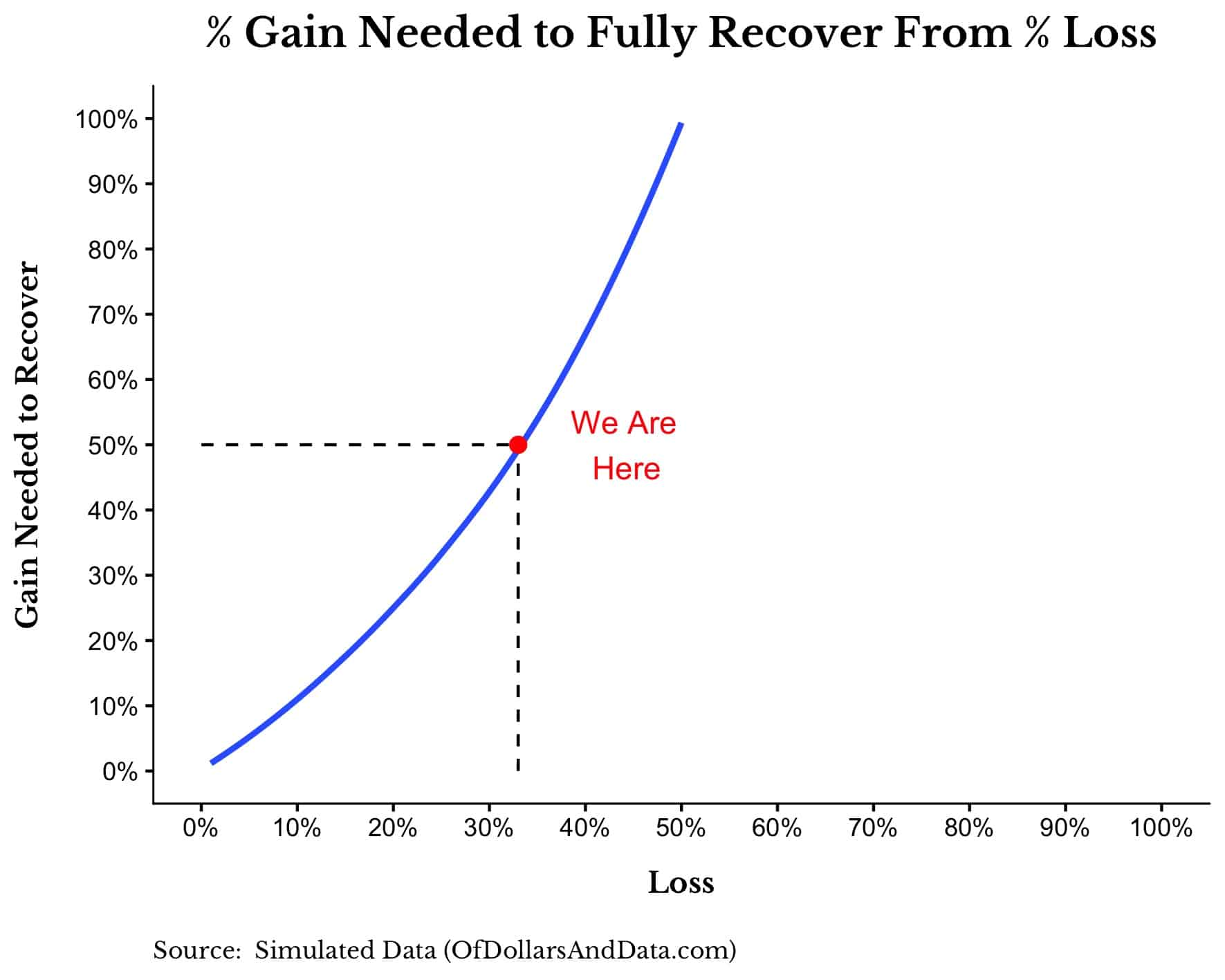

But where does such a spectacular increase come from? Well, besides being intuitive, its origin lies in simple mathematics: Every percentage loss requires a higher percentage gain to compensate for it. At this point in the film, it should not escape anyone's attention that a 10% fall requires an 11,11% rise to recover that loss. In the same way that a 20% loss requires a 25% rise and a 50% fall requires a 100% rise. You can see this exponential relationship very clearly in the graph below:

Let us now see what the chart would look like adapting it to the fall in the markets up to last week (-33%) and see the profit that would be needed to recover it:

If we do not see new lows, the recovery needed is 50%. And what a coincidence, for every $100 invested now they will generate $150 (a further 50%) when the recovery materialises.

.

But despite the obvious benefit of buying during the current panic, most investors are not doing so at all. Including those who have a lot of cash, either because they had it in other assets or because they sold during the crash in panic. And thank goodness they don't, because if they did, the crashes would no longer be crashes, and therefore the opportunities for good investors would vanish before they materialised. Excuses for not doing so can be diverse and very convincing for less good investors. Among them are «this time it's different» or «we don't know if it will fall further». As if a good investor is only one who is lucky enough to buy just on the day when the markets quote what will be the historic low of that crash. Remember that in graph 2 we talk about buying "as close as possible" to the low, without aiming to buy right on the bull's eye.

.

Let us now honestly answer the following question: How long do you think it will take for the markets to recover to the pre-pandemic highs? A month, a year, a decade? How long will it take for the indices to recover from that 33% decline? Answer yourselves.

.

Based on that answer, let us return again to the expected annual return in the future for our current investment. The equation is as follows:

Expected annual return = (1 + % Gain needed to recover)^(1/Number of years to recovery) - 1

But since we know that the percentage gain needed to recover is 50%, we can simplify it as follows:

Expected annual return = (1.5)^(1/Number of years to recovery) - 1

Therefore, if you think that the market will take time to recover:

- 1 year, then your expected annual return = 50%

- 2 years, then your expected annual return = 22%

- 3 years, then your expected annual return = 14%

- 4 years, then your expected annual return = 11%

- 5 years, then your expected annual return = 8%

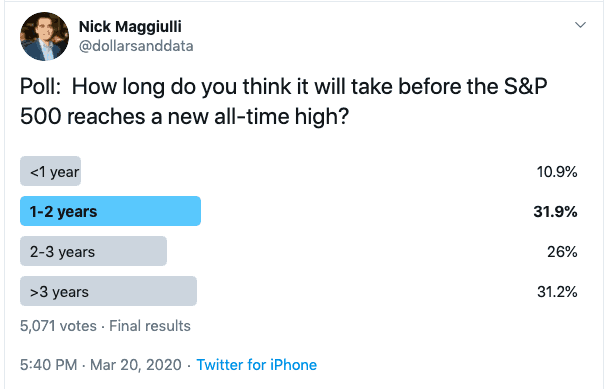

Even taking 5 years for a full recovery, the market would be offering you the same return as the US stock market has historically yielded. Nick Maggiulli asked this same question on twitter and found that two out of three of his poll participants believe that the recovery will come within 3 years.

That means that if the majority of respondents are correct, any investment made now, is going to yield between 14% and 50% annualised until the market recovers. Think about what this means. Investors who choose not to buy at this time are either giving up an annualised return in excess of 14% for the next 3 years, or they believe that the market will take more than 5 years to recover and despise annualised returns of less than 8%. In short, the only reasonable reason not to do so is if you already have all your money invested and have no more at the moment (time to sell grandma to invest more in the stock market, as he said...).

.

Of course, new black swans may occur on the planet, delaying the recovery of markets, as has been the case for decades in Japan, for example. But it seems unlikely, especially in efficient economies such as the US and growing economies such as China and the other Asian economic orbit. Moreover, note that throughout the article we are referring to the market, i.e. the indices. But imagine the figures that will be achieved by those who also have the possibility of investing in actively managed funds that significantly outperform the benchmark indices. In other words, those who invest in portfolios where the management team selects the companies with the greatest potential for recovery at this time (Healthcare sector in China, for example). And we will not tire of repeating that, although the vast majority of actively managed funds do not outperform their benchmarks, especially within the limited universe of funds marketed in Spain, there are world-renowned managers who have been doing so for decades. Unfortunately, however, they are not easily accessible to the average Spanish investor, as we explain in detail in «Why don't large international investors invest in the same funds as you?«.

.

As he once said Jim O'Shaughnesy, Many people confuse possibility with probability, and the two are almost opposites. Keep this in mind as you face new challenges that will come in these days.

.

One of the things that still surprises me is to see how simple mathematics can help us to clarify the thickets in which our own minds entangle us. Our fears and passions are our worst ally in the face of the crash caused by the covid19 virus. Objective figures are certainly a glimmer of sanity to handle Mr. Market's schizophrenia. And the numbers show us that, assuming the market (and even more so our well selected stocks by the world's best managers) will recover in the coming quarters or semesters, the returns we will get are very, very attractive. And therefore, any hypothetical new low in the stock markets would be nothing more than an additional buying opportunity and even higher profits. Fortunately for a minority, the majority do not see it this way and are still waiting to see the floor, like those who are permanently waiting to catch the next train, which will probably be an AVE train that does not stop at their particular station.